New Classical Critique. Aggregate Demand Write a simple version of the aggregate demand curve based...

36

New Classical Critique

-

Upload

dorian-maddox -

Category

Documents

-

view

222 -

download

0

Transcript of New Classical Critique. Aggregate Demand Write a simple version of the aggregate demand curve based...

New Classical Critique

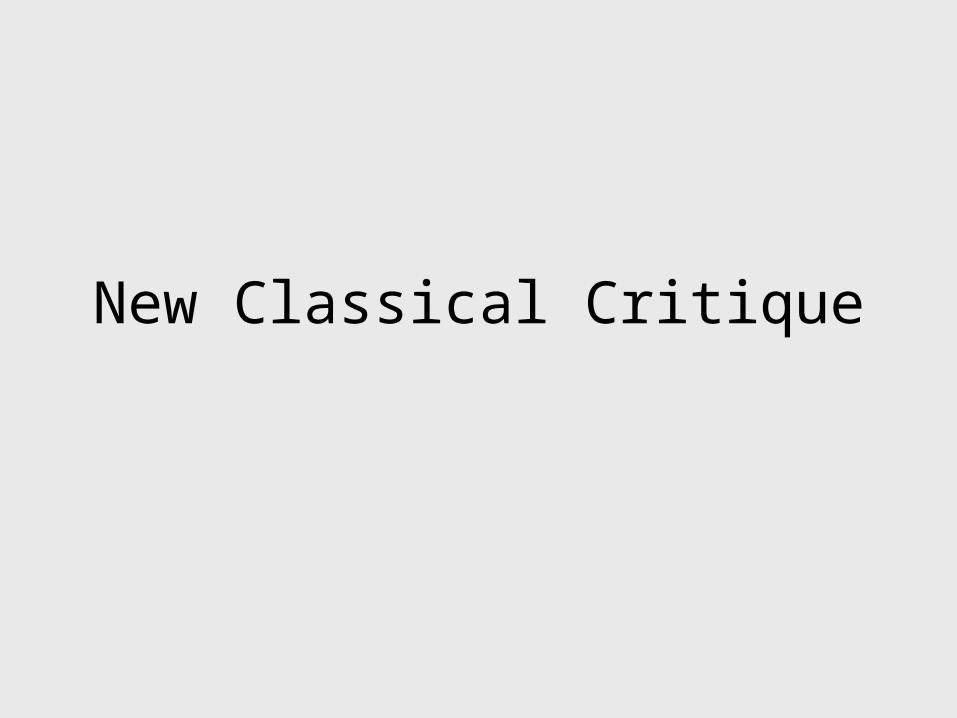

Aggregate Demand Write a simple version of the aggregate demand

curve based on the monetary policy rule. – αt: Expenditure shift

– μt: Monetary policy shift

– πtFED: Central Bank Measure of inflation.

:

:

:

t t t

FEDt t t

FED FEDt t t t t t t

IS y d r

MP r b

AD y d b d b

Supply Curve

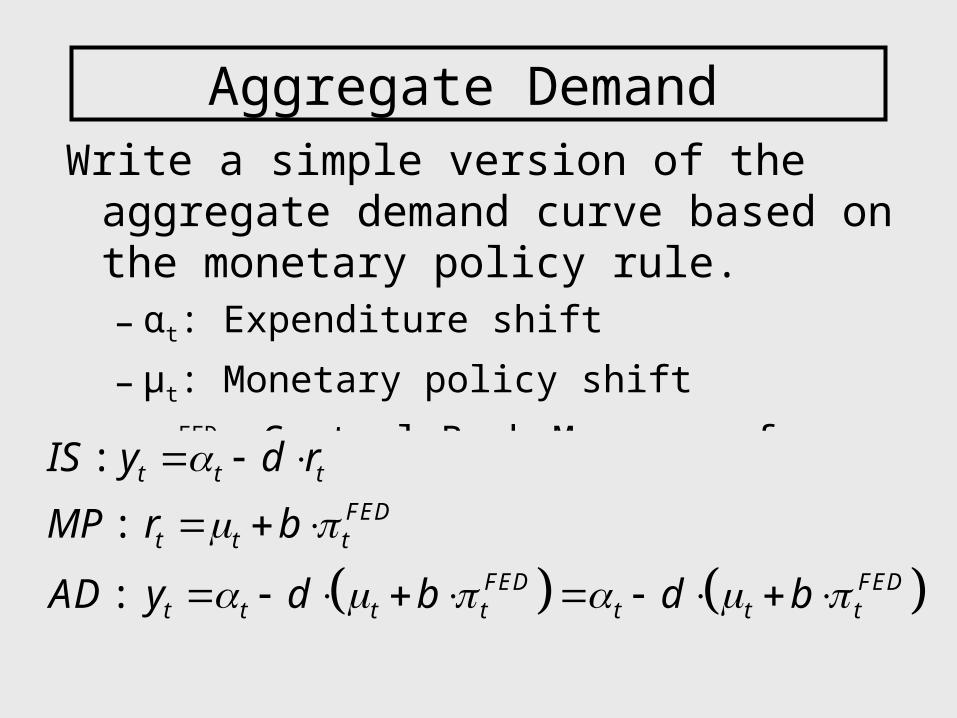

Output differs from potential output only to the degree that wage stickiness causes fluctuations in labor usage or due to temporary supply shocks (such as changes in the price of oil).

• A more realistic pricing rule, might set inflation as an increasing function of deviations from long-term output.

• SRAS: gW: Wage Growth, vt : Supply shift

Wt t t tg y y

Rational Expectations

• In early 1970’s, Lucas, Sargent, and Wallace pointed out logical flaw in story of adaptive expectations.

• In periods following a demand shock, workers expect that inflation equal to last years inflation, though clearly and systematically the inflation level will be accelerating.

• RE theory suggests that economic modeling of expectations about the future should be consistent with what the models say will predictably happen in the future.

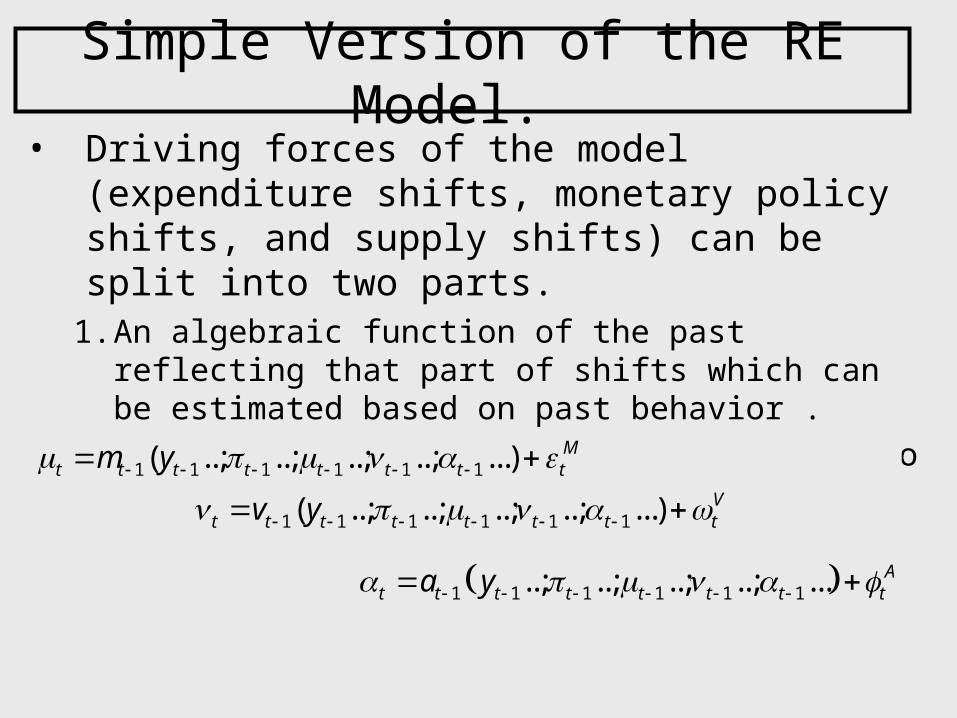

Simple Version of the RE Model. • Driving forces of the model (expenditure shifts,

monetary policy shifts, and supply shifts) can be split into two parts.

1. An algebraic function of the past reflecting that part of shifts which can be estimated based on past behavior .

2. Unpredictable white noise shocks with zero average value.

1 1 1 1 1 1

1 1 1 1 1 1

1 1 1 1 1 1

( ..; ..; ..; ..; ...)

( ..; ..; ..; ..; ...)

..; ..; ..; ..; ...

Mt t t t t t t t

Vt t t t t t t t

At t t t t t t t

m y

v y

a y

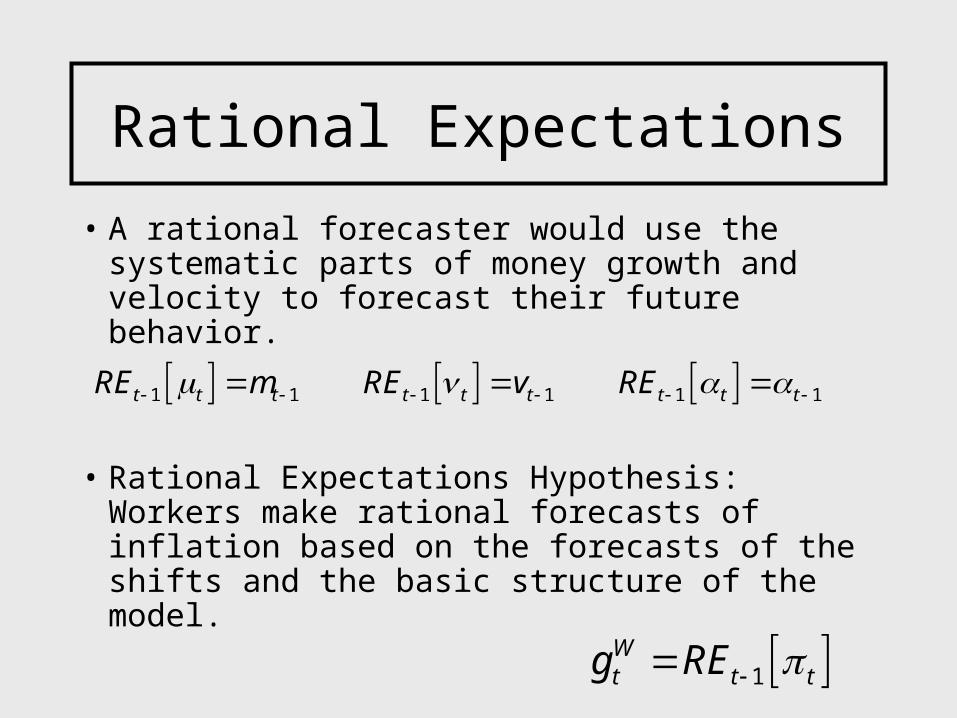

Rational Expectations

• A rational forecaster would use the systematic parts of money growth and velocity to forecast their future behavior.

• Rational Expectations Hypothesis: Workers make rational forecasts of inflation based on the forecasts of the shifts and the basic structure of the model.

1 1 1 1 1 1t t t t t t t t tRE m RE v RE

1Wt t tg RE

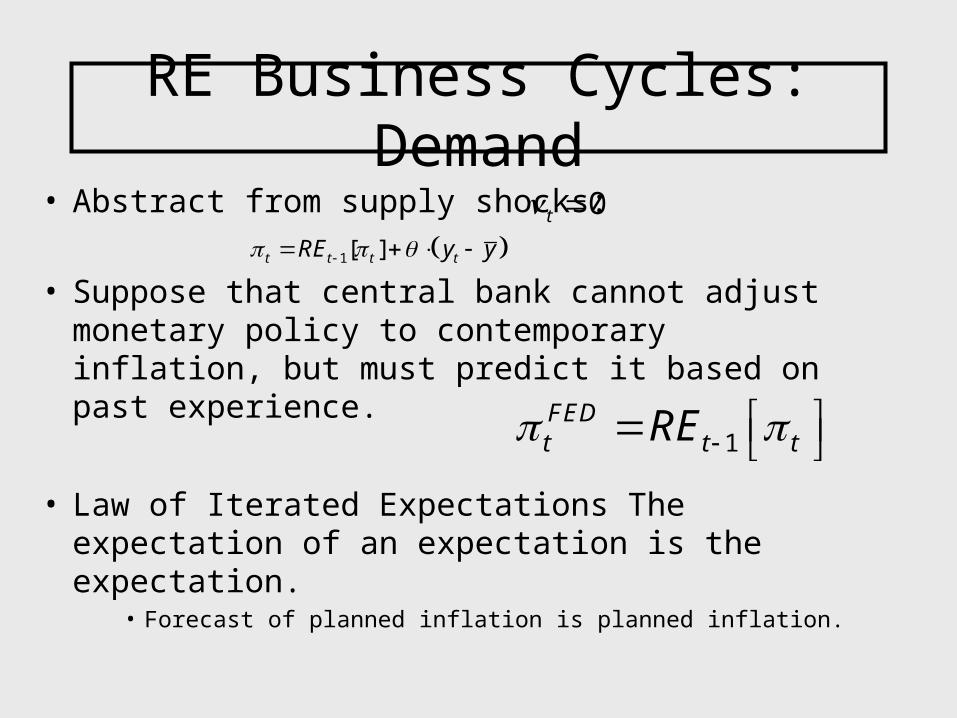

RE Business Cycles: Demand

• Abstract from supply shocks:

• Suppose that central bank cannot adjust monetary policy to contemporary inflation, but must predict it based on past experience.

• Law of Iterated Expectations The expectation of an expectation is the expectation.

• Forecast of planned inflation is planned inflation.

0t

1FEDt t tRE

1[ ]t t t tRE y y

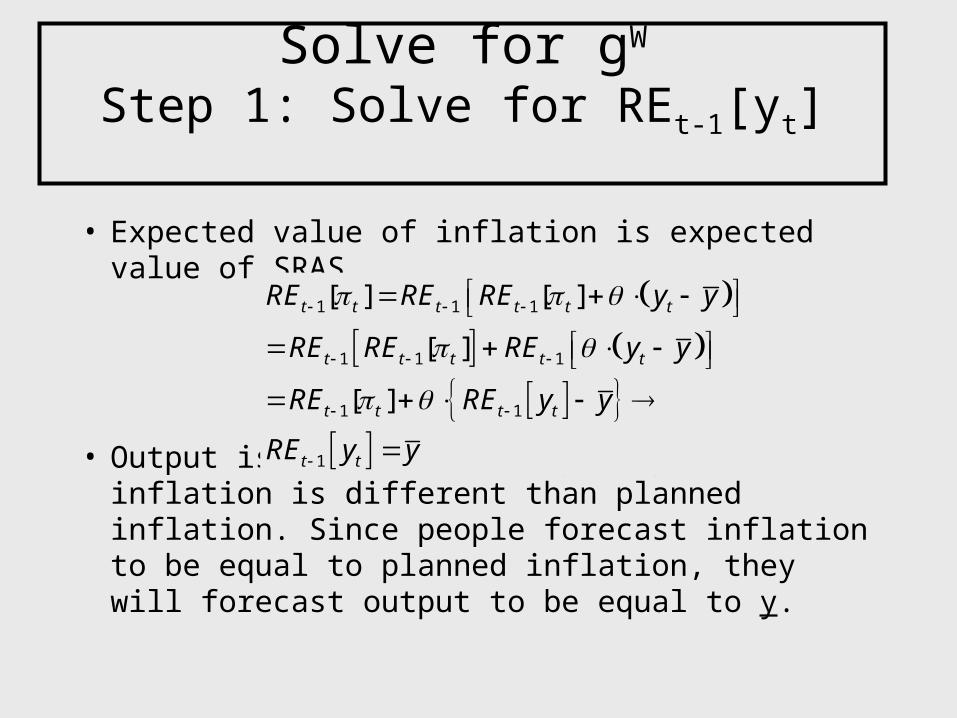

Solve for gW

Step 1: Solve for REt-1[yt]

• Expected value of inflation is expected value of SRAS

• Output is different from y only if inflation is different than planned inflation. Since people forecast inflation to be equal to planned inflation, they will forecast output to be equal to y.

1 1 1

1 1 1

1 1

1

[ ] [ ]

[ ]

[ ]

t t t t t t

t t t t t

t t t t

t t

RE RE RE y y

RE RE RE y y

RE RE y y

RE y y

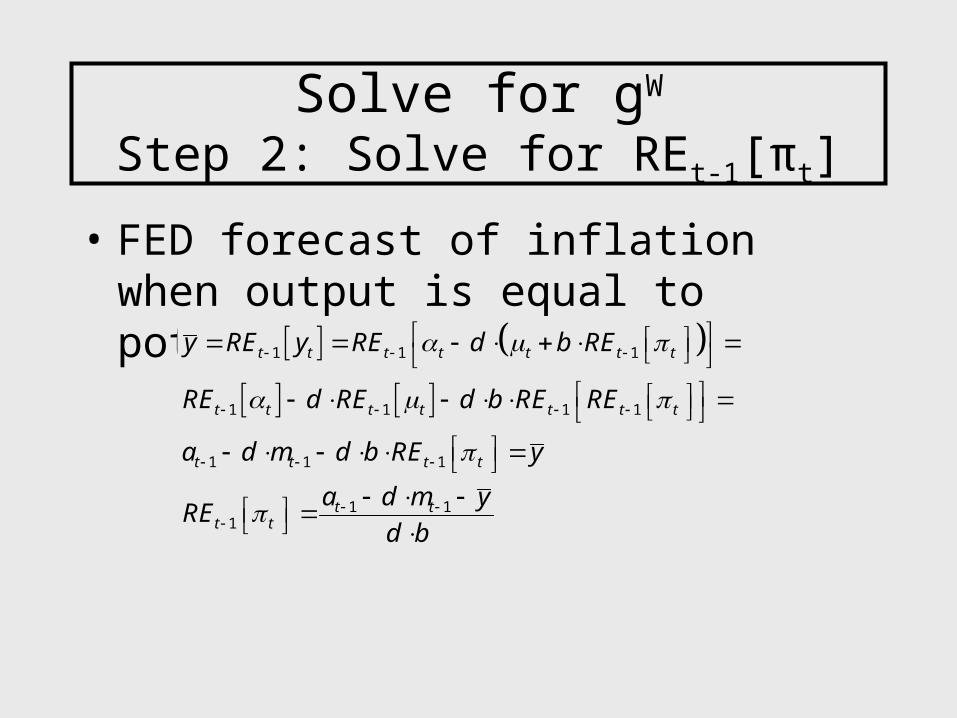

Solve for gW

Step 2: Solve for REt-1[πt]

• FED forecast of inflation when output is equal to potential

1 1 1

1 1 1 1

1 1 1

1 11

t t t t t t t

t t t t t t t

t t t t

t tt t

y RE y RE d b RE

RE d RE d b RE RE

a d m d b RE y

a d m yRE

d b

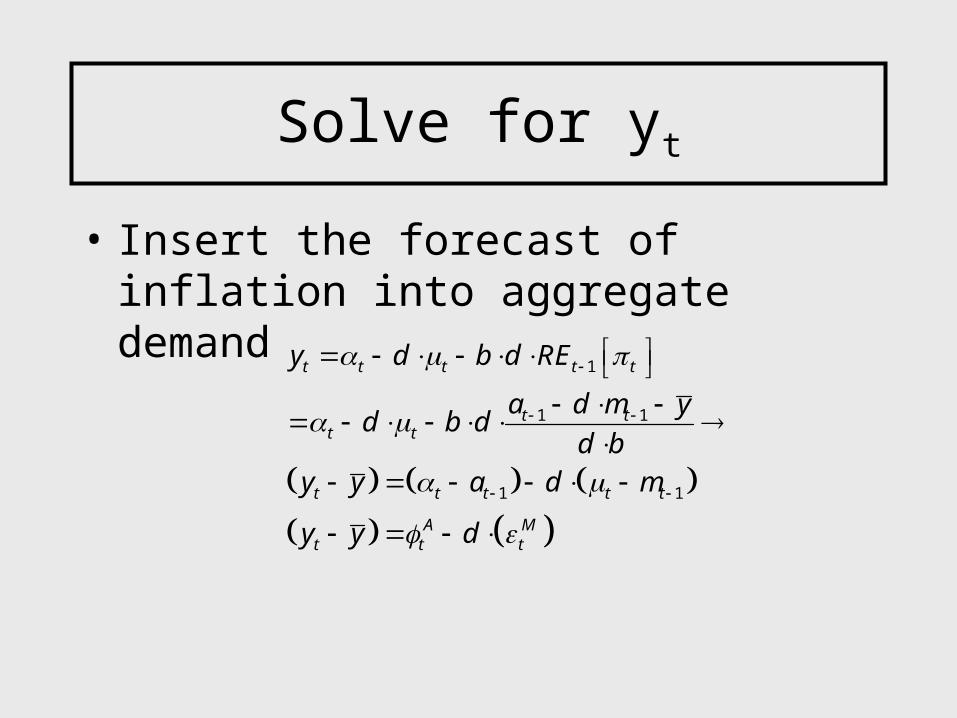

Solve for yt

• Insert the forecast of inflation into aggregate demand curve

1

1 1

1 1

t t t t t

t tt t

t t t t t

A Mt t t

y d b d RE

a d m yd b d

d by y a d m

y y d

Implications

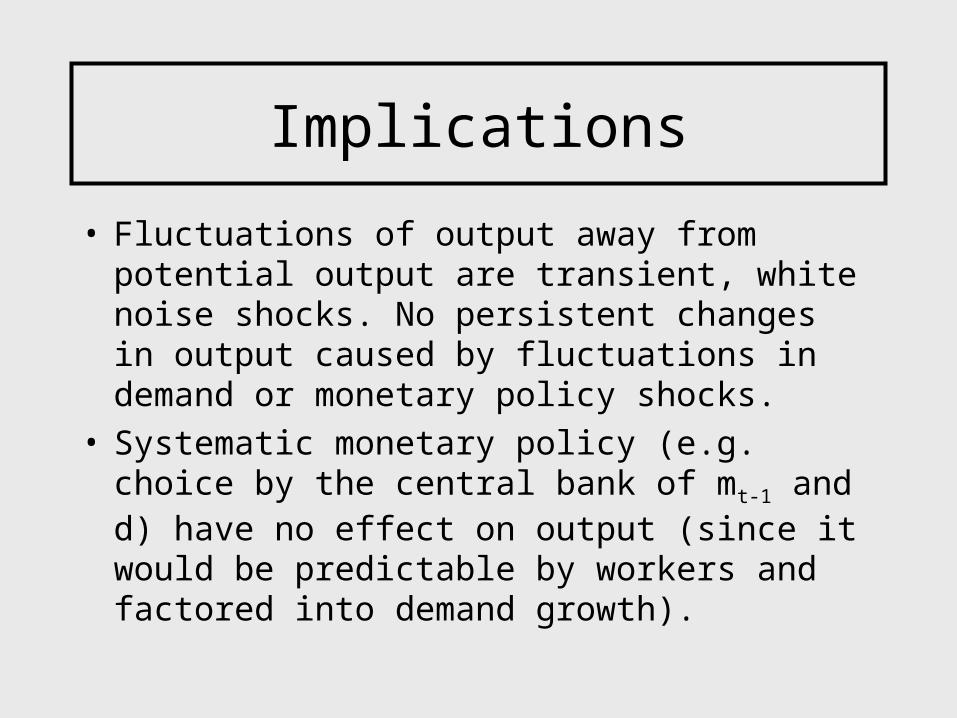

• Fluctuations of output away from potential output are transient, white noise shocks. No persistent changes in output caused by fluctuations in demand or monetary policy shocks.

• Systematic monetary policy (e.g. choice by the central bank of mt-1 and d) have no effect on output (since it would be predictable by workers and factored into demand growth).

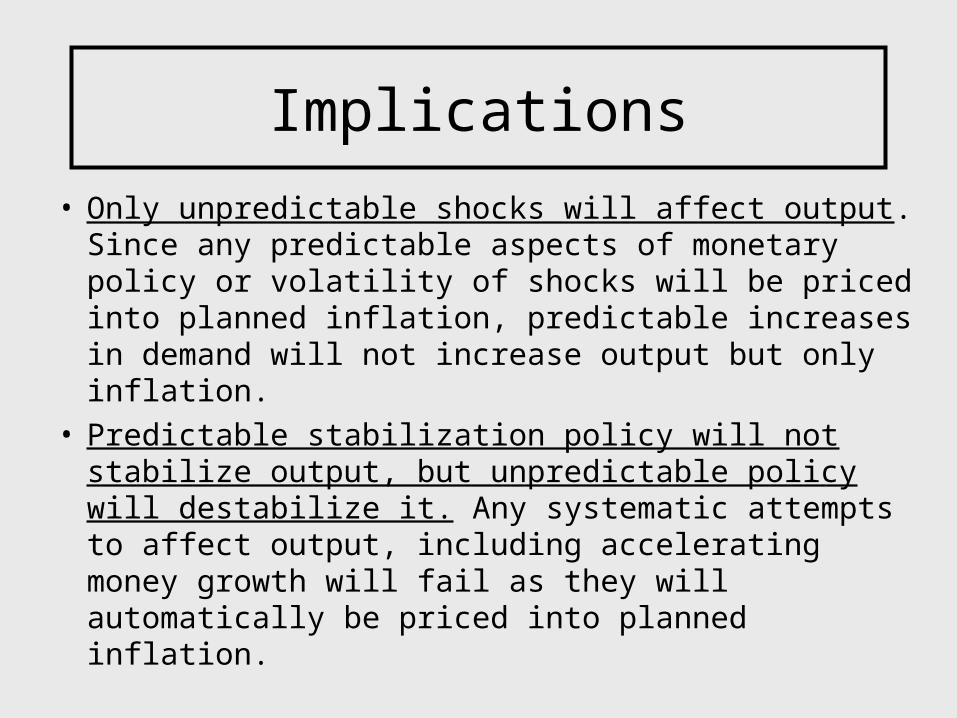

Implications

• Only unpredictable shocks will affect output. Since any predictable aspects of monetary policy or volatility of shocks will be priced into planned inflation, predictable increases in demand will not increase output but only inflation.

• Predictable stabilization policy will not stabilize output, but unpredictable policy will destabilize it. Any systematic attempts to affect output, including accelerating money growth will fail as they will automatically be priced into planned inflation.

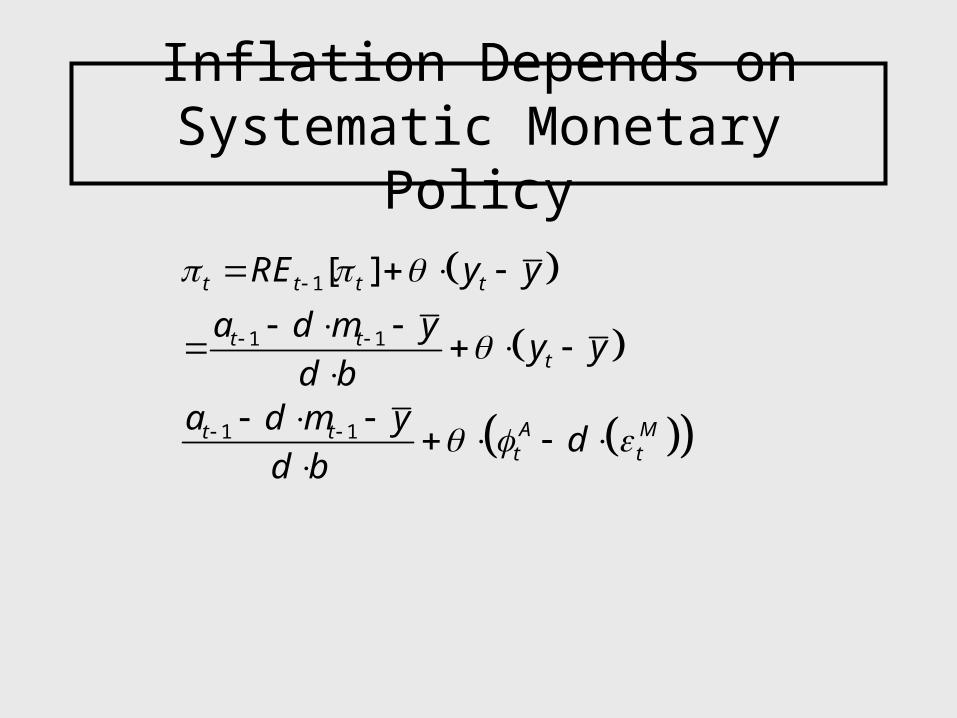

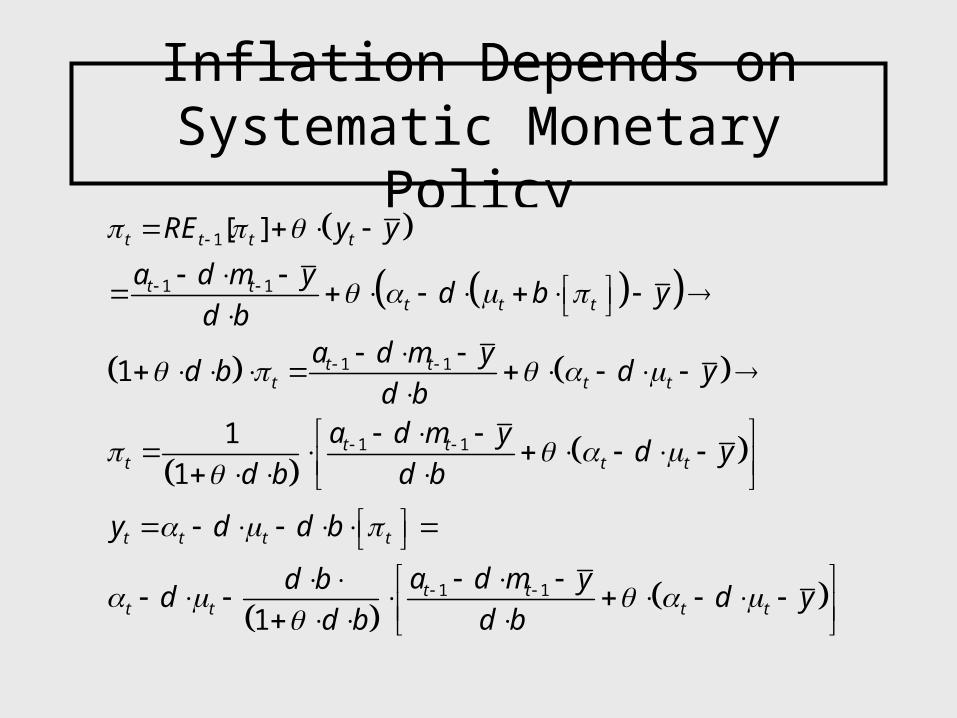

Inflation Depends on Systematic Monetary Policy

1

1 1

1 1

[ ]t t t t

t tt

A Mt tt t

RE y y

a d m yy y

d ba d m y

dd b

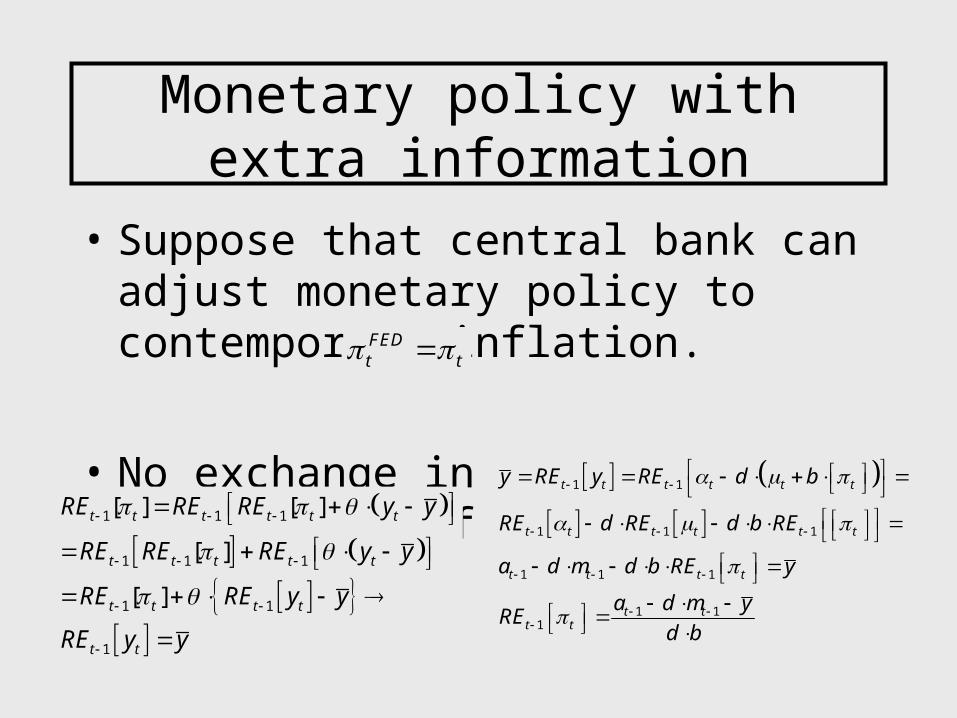

Monetary policy with extra information

• Suppose that central bank can adjust monetary policy to contemporary inflation.

• No exchange in workers expectation of inflation

FEDt t

1 1

1 1 1

1 1 1

1 11

t t t t t t

t t t t t t

t t t t

t tt t

y RE y RE d b

RE d RE d b RE

a d m d b RE y

a d m yRE

d b

1 1 1

1 1 1

1 1

1

[ ] [ ]

[ ]

[ ]

t t t t t t

t t t t t

t t t t

t t

RE RE RE y y

RE RE RE y y

RE RE y y

RE y y

Inflation Depends on Systematic Monetary Policy

1

1 1

1 1

1 1

1 1

[ ]

1

1

1

1

t t t t

t tt t t

t tt t t

t tt t t

t t t t

t tt t

RE y y

a d m yd b y

d ba d m y

d b d yd b

a d m yd y

d b d b

y d d b

a d m yd bd

d b d

t td yb

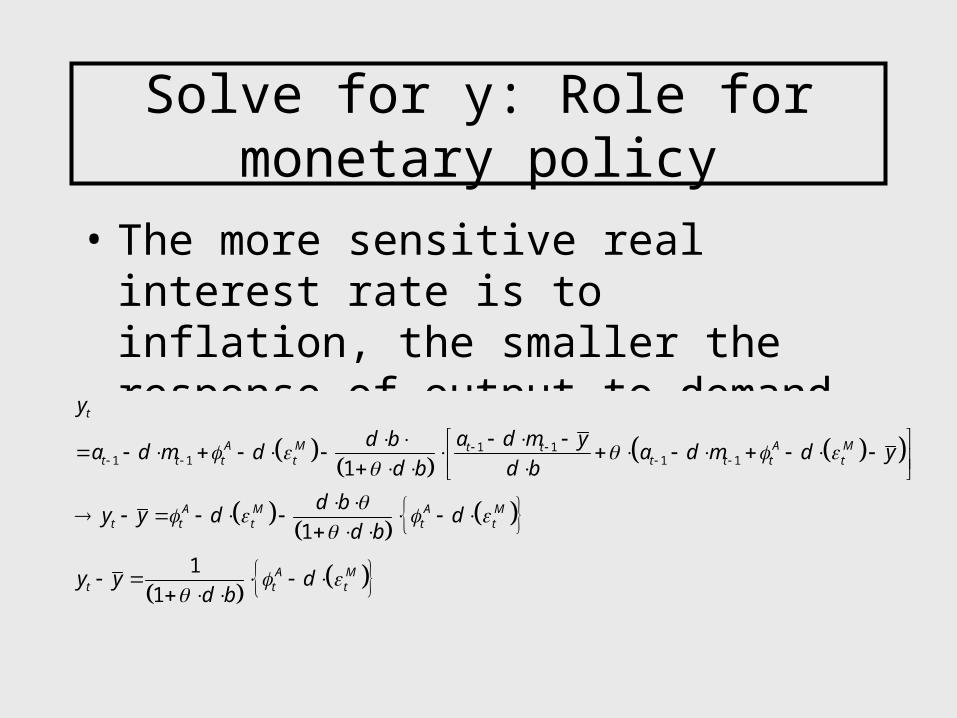

Solve for y: Role for monetary policy

• The more sensitive real interest rate is to inflation, the smaller the response of output to demand shocks.

1 11 1 1 11

1

1

1

t

A M A Mt tt t t t t t t t

A M A Mt t t t t

A Mt t t

y

a d m yd ba d m d a d m d y

d b d b

d by y d d

d b

y y dd b

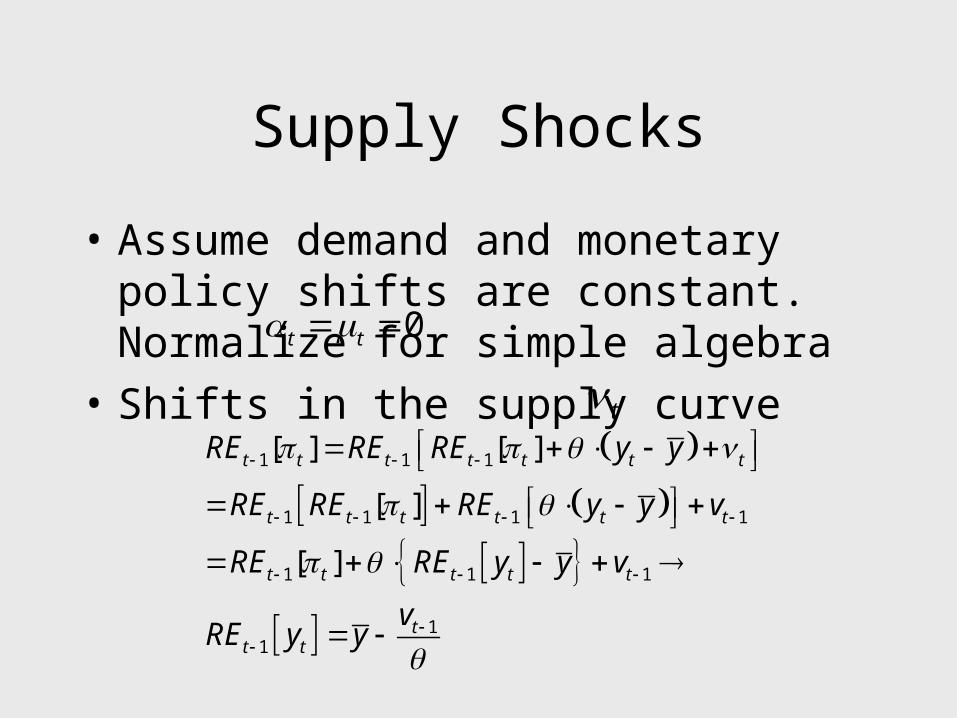

Supply Shocks

• Assume demand and monetary policy shifts are constant. Normalize for simple algebra

• Shifts in the supply curve 0t t

1 1 1

1 1 1 1

1 1 1

11

[ ] [ ]

[ ]

[ ]

t t t t t t t

t t t t t t

t t t t t

tt t

RE RE RE y y

RE RE RE y y v

RE RE y y v

vRE y y

t

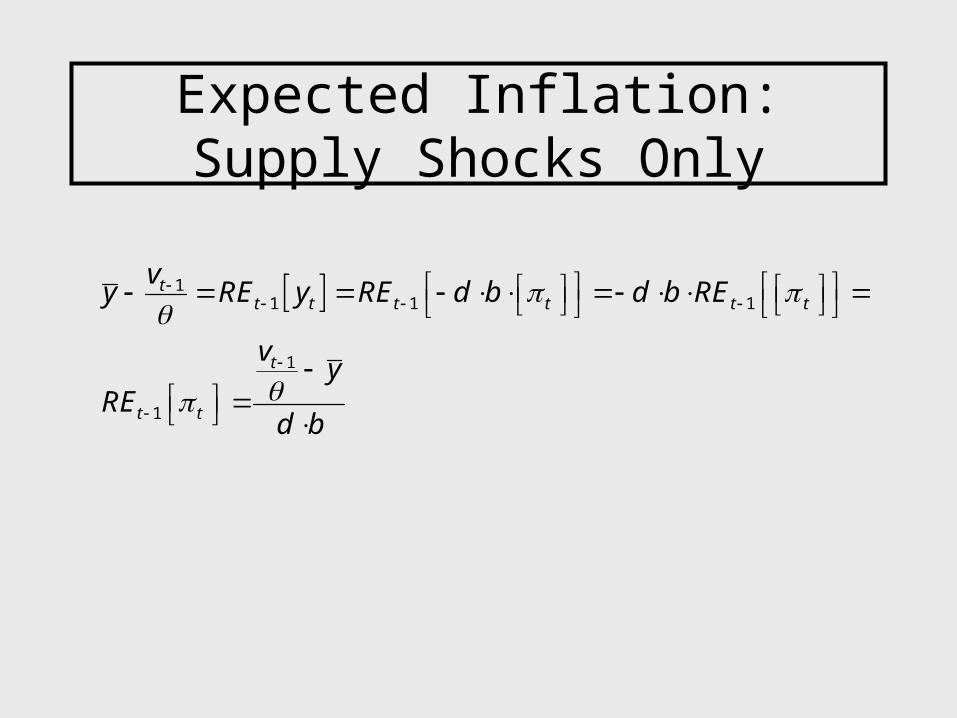

Expected Inflation: Supply Shocks Only

11 1 1

1

1

tt t t t t t

t

t t

vy RE y RE d b d b RE

vy

REd b

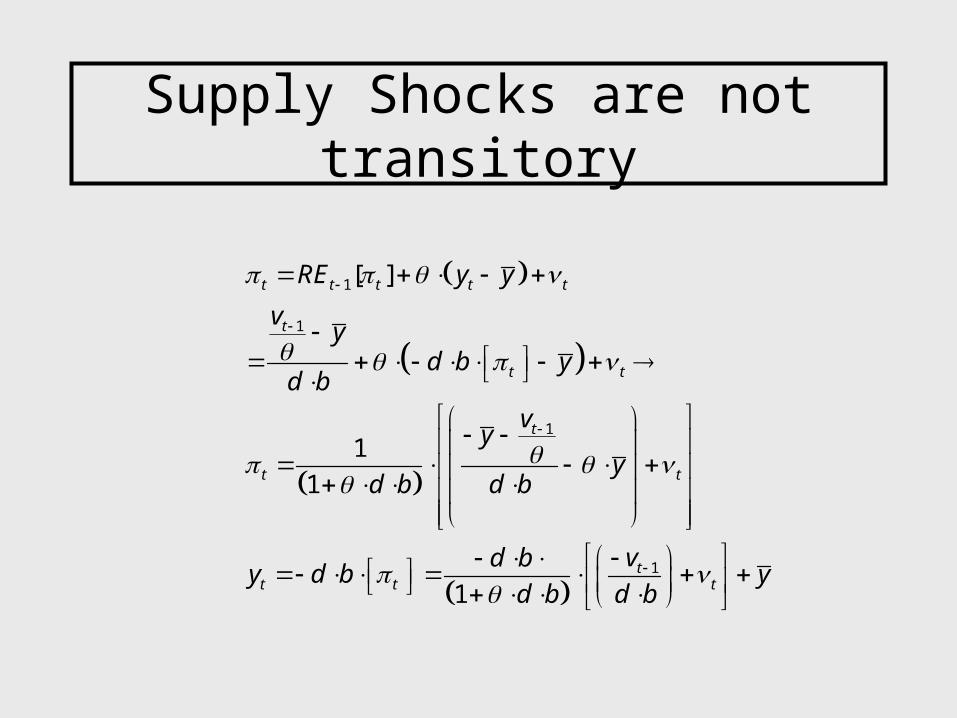

Supply Shocks are not transitory

1

1

1

1

[ ]

1

1

1

t t t t t

t

t t

t

t t

tt t t

RE y y

vy

d b yd b

vy

yd b d b

vd by d b y

d b d b

Nobel Prize Ideas

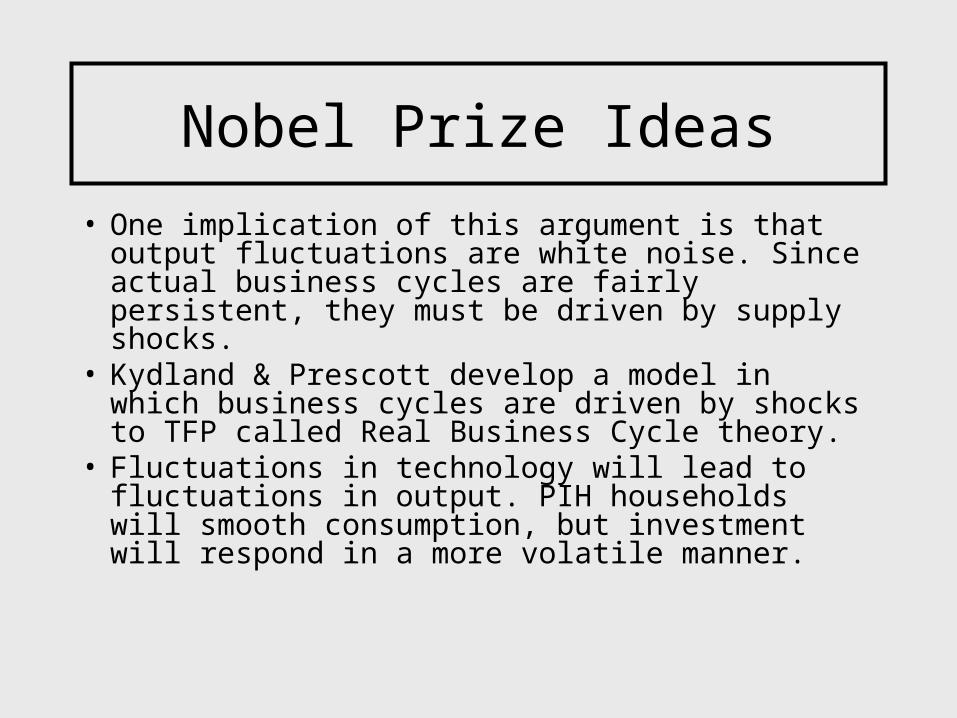

• One implication of this argument is that output fluctuations are white noise. Since actual business cycles are fairly persistent, they must be driven by supply shocks.

• Kydland & Prescott develop a model in which business cycles are driven by shocks to TFP called Real Business Cycle theory.

• Fluctuations in technology will lead to fluctuations in output. PIH households will smooth consumption, but investment will respond in a more volatile manner.

Technology shocks and labor

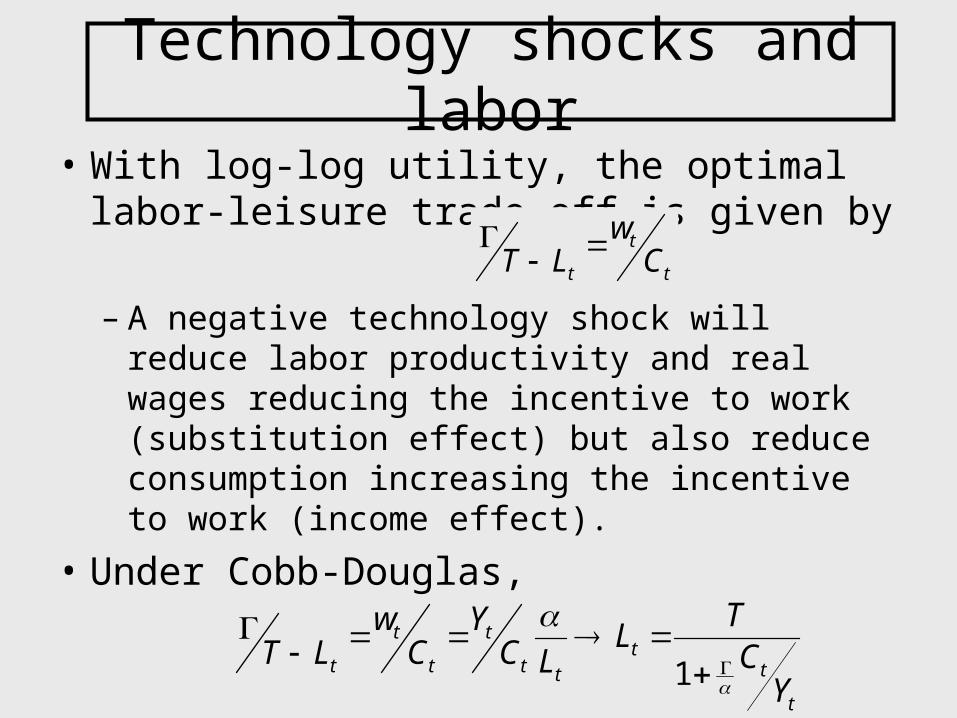

• With log-log utility, the optimal labor-leisure trade-off is given by

– A negative technology shock will reduce labor productivity and real wages reducing the incentive to work (substitution effect) but also reduce consumption increasing the incentive to work (income effect).

• Under Cobb-Douglas,

t

t t

wT L C

1

t tt

t t t tt

t

Tw Y LT L C C CLY

RBC Models

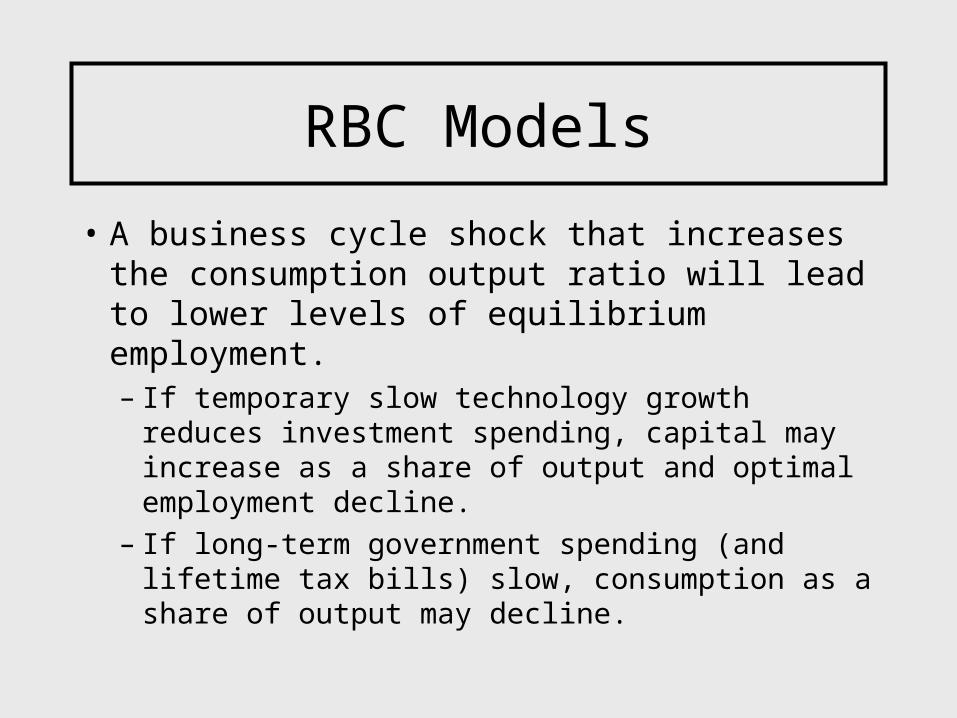

• A business cycle shock that increases the consumption output ratio will lead to lower levels of equilibrium employment.– If temporary slow technology growth reduces

investment spending, capital may increase as a share of output and optimal employment decline.

– If long-term government spending (and lifetime tax bills) slow, consumption as a share of output may decline.

Nobel Ideas pt. 2

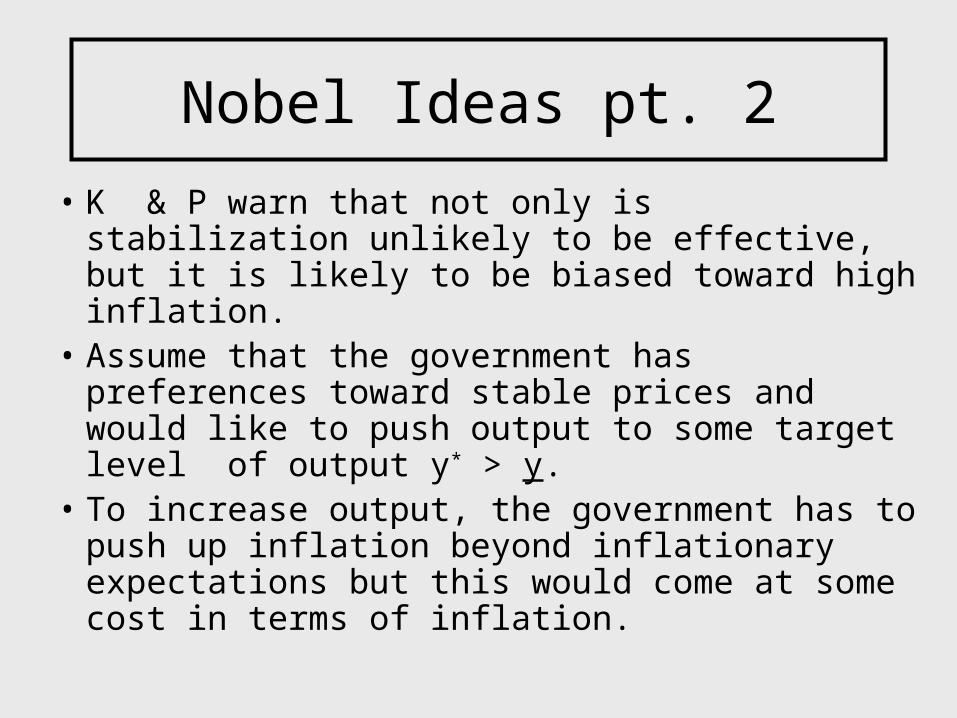

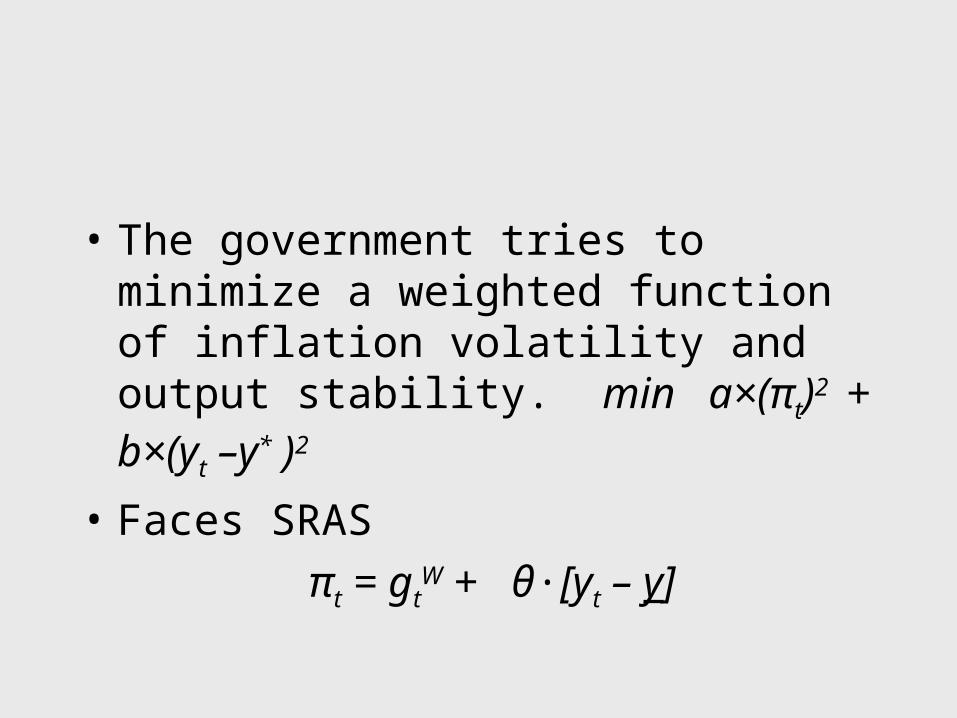

• K & P warn that not only is stabilization unlikely to be effective, but it is likely to be biased toward high inflation.

• Assume that the government has preferences toward stable prices and would like to push output to some target level of output y* > y.

• To increase output, the government has to push up inflation beyond inflationary expectations but this would come at some cost in terms of inflation.

• The government tries to minimize a weighted function of inflation volatility and output stability. min a×(πt)2

+ b×(yt –y* )2

• Faces SRAS

πt = gtW + θ∙[yt – y]

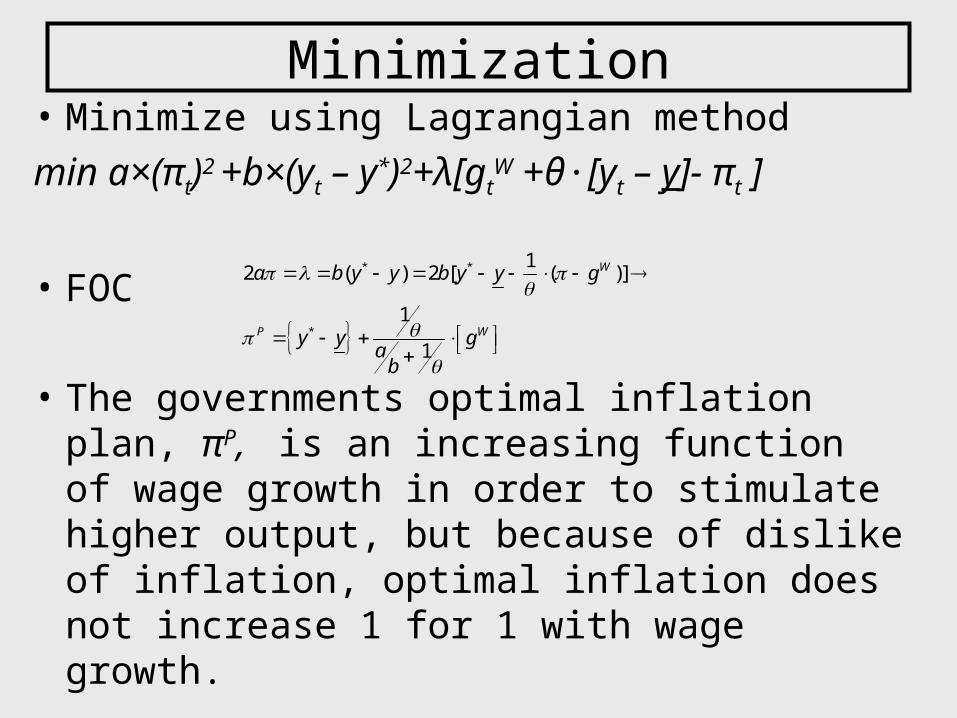

Minimization• Minimize using Lagrangian method

min a×(πt)2 +b×(yt – y*)2+λ[gt

W +θ∙[yt – y]- πt ]

• FOC

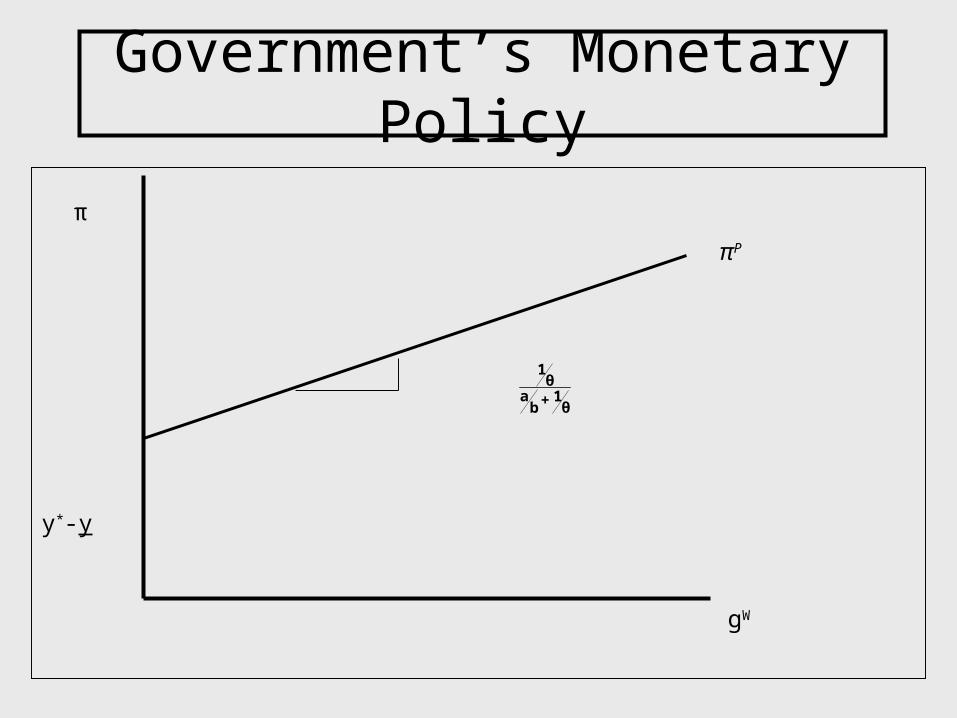

• The governments optimal inflation plan, πP, is an increasing function of wage growth in order to stimulate higher output, but because of dislike of inflation, optimal inflation does not increase 1 for 1 with wage growth.

* *

*

12 ( ) 2 [ ( )]

1

1

W

P W

a b y y b y y g

y y ga

b

Government’s Monetary Policy

y*-y

1θ

a 1+b θ

π

gW

πP

Rational Expectations

• If expectations were fixed, the government could achieve its goals, trading off higher inflation for higher output.

• However, if workers are rational forecasters, they should set their expectations about the governments monetary policy according to the way the government sets policy: RE[π] = πP

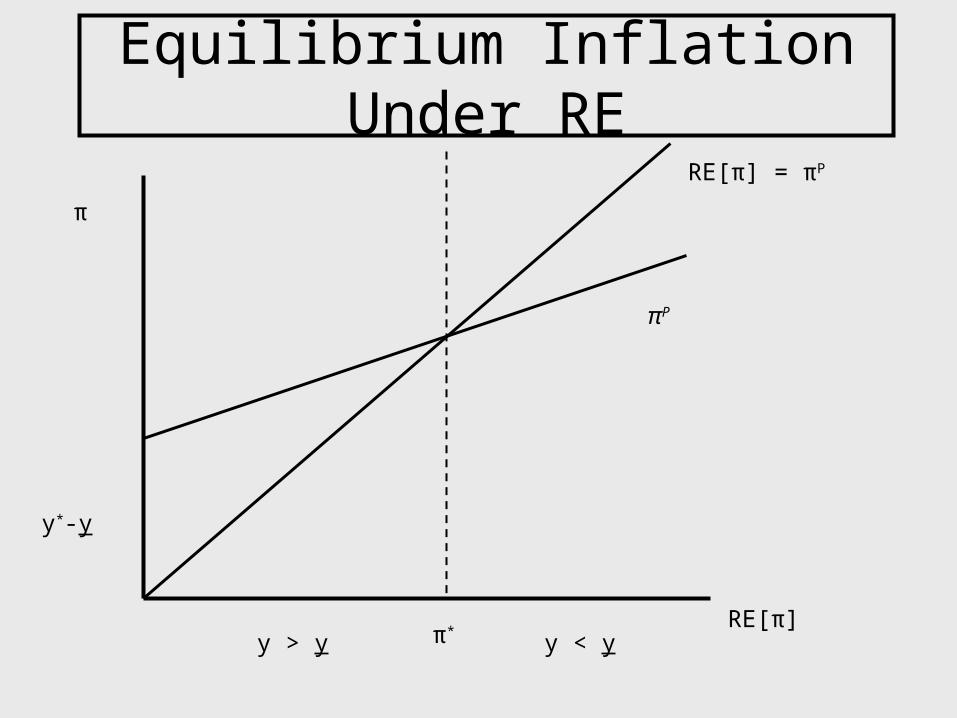

Equilibrium Inflation Under RE

y*-y

π

RE[π]

πP

RE[π] = πP

π*y > y y < y

Policy & Rational Expectations• Whenever RE[π] = πP then output will be equal to

long-term output. When workers have rational expectations, the government cannot push up output.

• However, their desire to boost output gives policy an inflationary bias. When they choose their optimal policy they will get high inflation, π*, and no boost in output.

• Government is better off sticking to a strict price stability rule π = 0. If workers set RE[π] = 0, the government could at least minimize inflation.

Credibility

• Government would benefit if they could build credibility for a low inflation policy. But can they?

• K&P argue not. Since workers know that if they came to expect π = 0 and demand low wage growth, the government would like to take advantage of the inflation-output tradeoff and run a higher than 0 inflation.

• A government with discretionary power cannot build credibility for a policy that would not be what the government would want to choose if it did build credibility.

Time Consistency & Rules vs. Discretion

• A time consistent policy is a policy plan that the government will want to stick to when it actually becomes time to implement it. – In this example, zero inflation is a time

inconsistent policy.

• K & P argue that the only way to implement a credible time inconsistent policy is to set up an institutional framework that will ignore the short-term goals of the government

Other Potentially Inconsistent Policies

• Low taxes on corporate profits/capital income. The government may propose a low corporate tax rate to encourage firms to invest in capital. But once the capital has been invested, the government may want to take a share of the profits.

• Fixed exchange rate.

Institutional policies

• Independent Central Bank with Conservative Central Banker. It is thought that professionals from financial community dislike monetary volatility. Giving one of these individuals the power to control money supply will move toward a low inflation commitment.

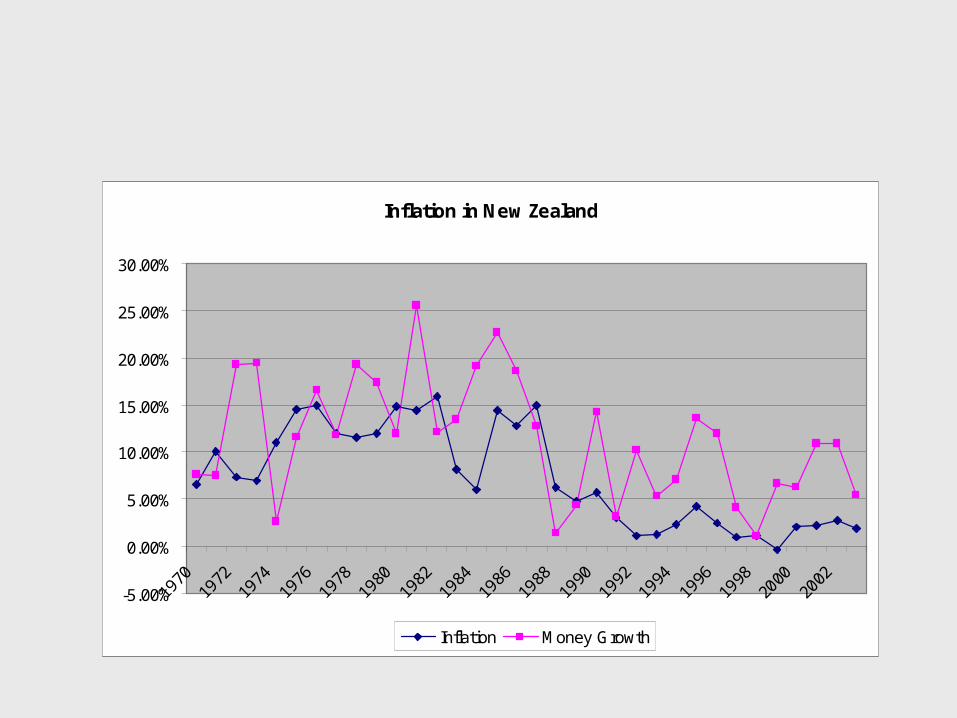

• Central Bank with a constitutional commitment toward low inflation. New Zealand’s central bank is instructed to follow an inflation-target in 1989.

Inflation in New Zealand

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Inflation Money Growth

Midterm Exam 3

• Tuesday, December 16 9-11– 3007 | (Thu) | 08:30-11:30

• Coverage: Fiscal Policy, Money, Keynesian Model, New Classical Critique

• Bring Calculator, Writing Instruments, 1 A4 sized paper with written notes.