γλώσσες

Σελίδες

Νομικός

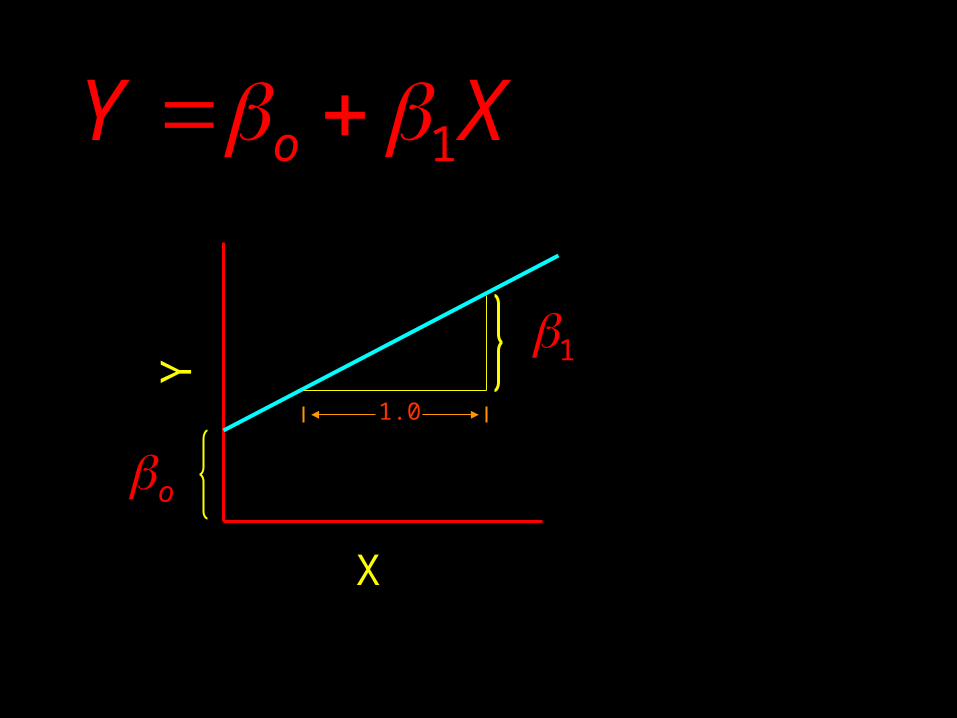

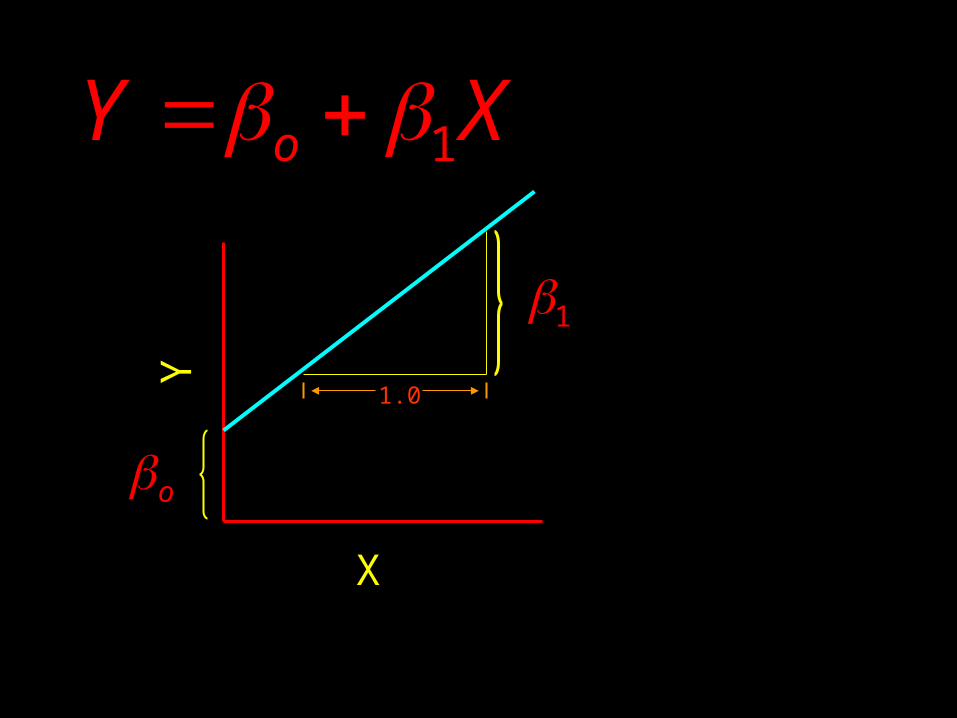

Simple Linear Regression (OLS)

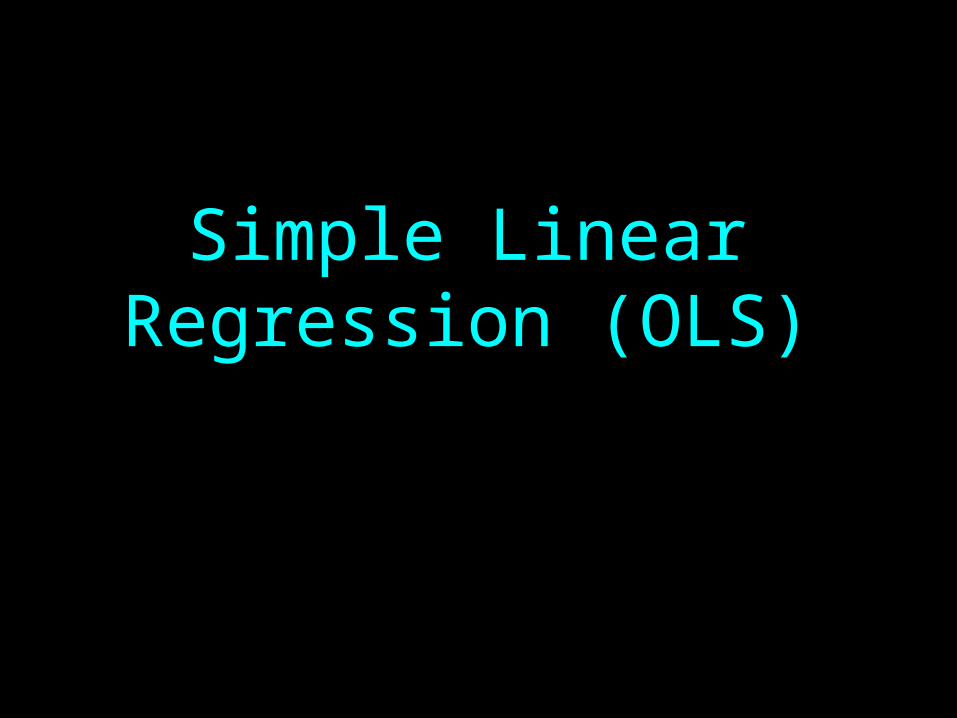

Types of Correlation

Positive correlation Negative correlation No correlation

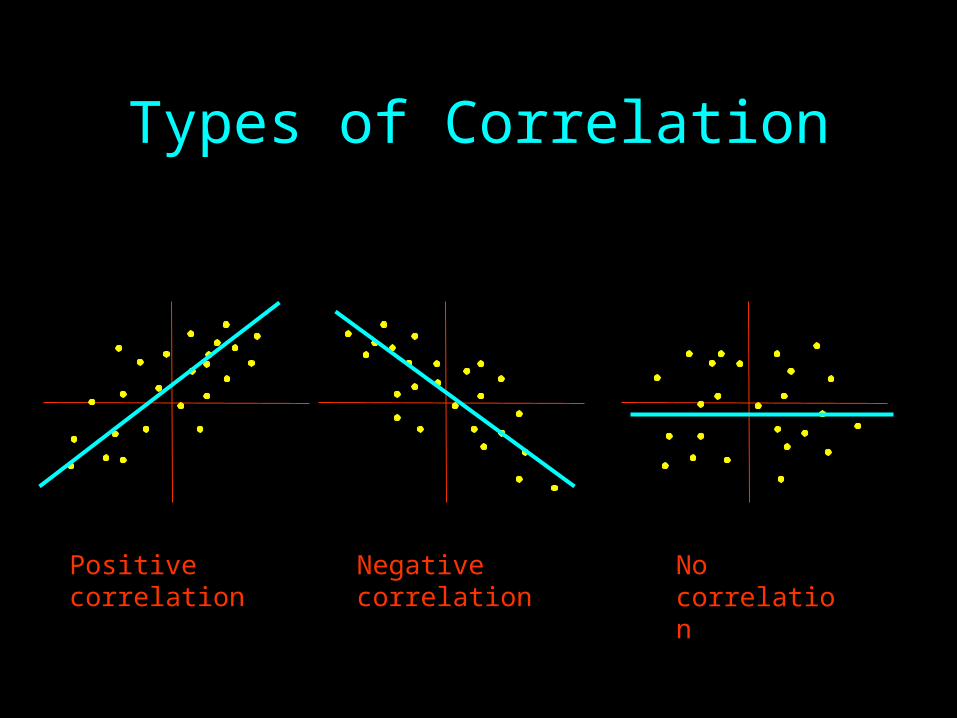

Simple linear regression describes the linear relationship between an independentvariable, plotted on the x-axis, and a dependent variable, plotted on the y-axis

Independent Variable (X)

depe

nden

t Var

iabl

e (Y

)

1oY X

X

Y

o1.0

1

1oY X

X

Y

o

1.0

1

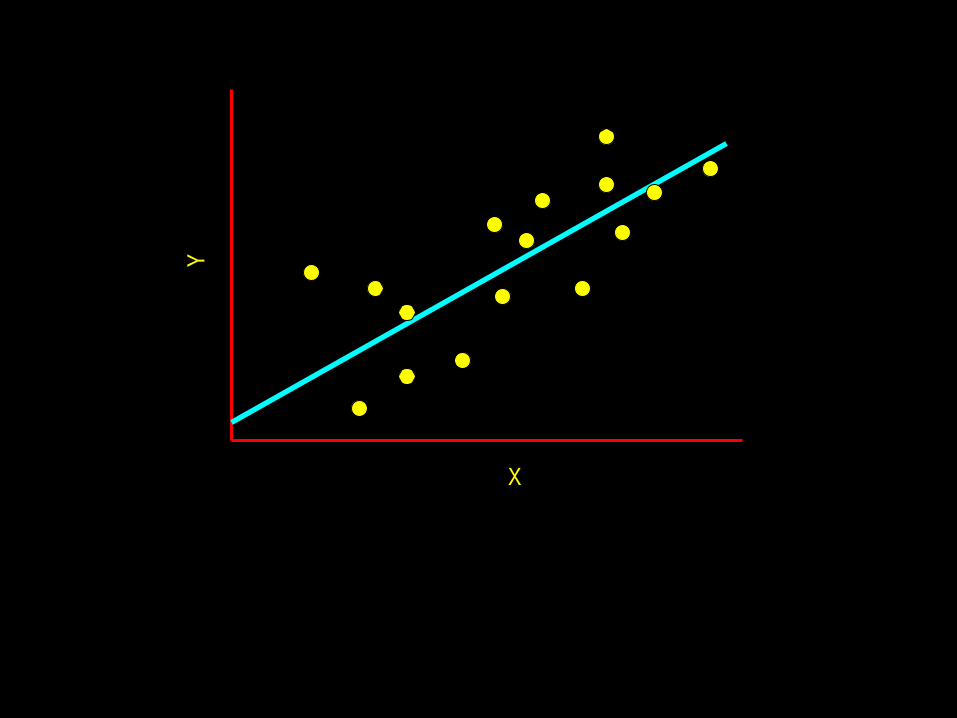

X

Y

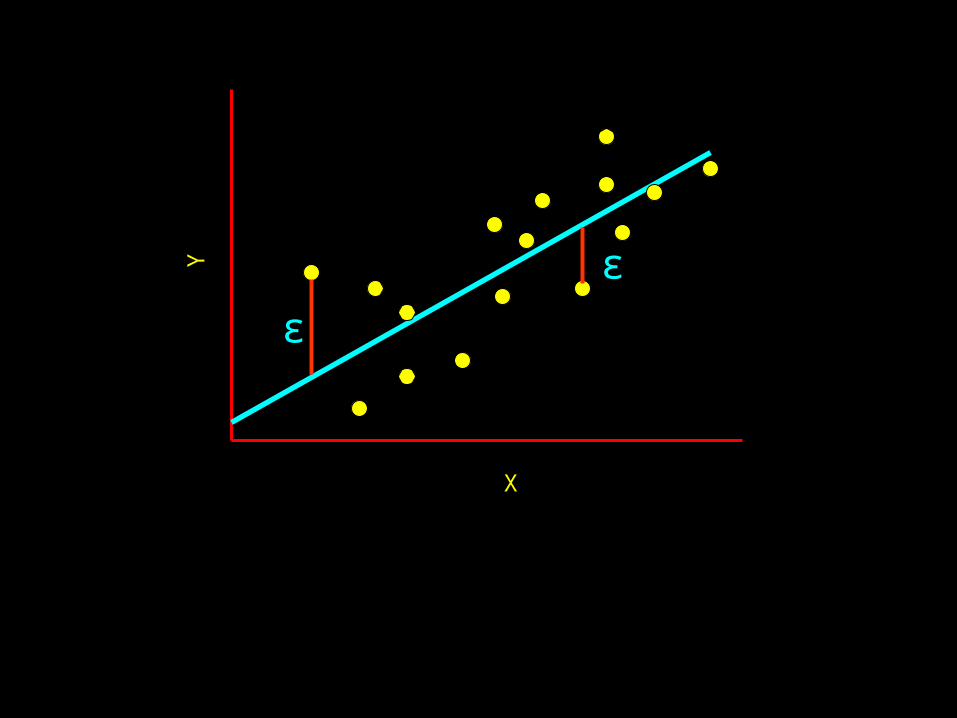

X

Y ε

ε

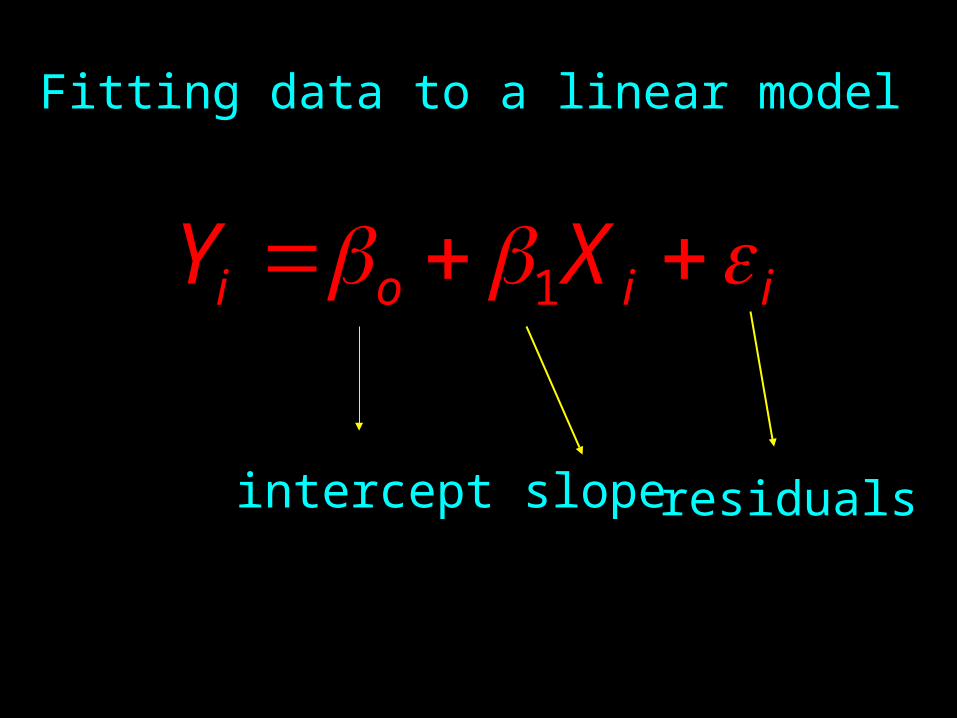

Fitting data to a linear model

1i o i iY X

intercept slope residuals

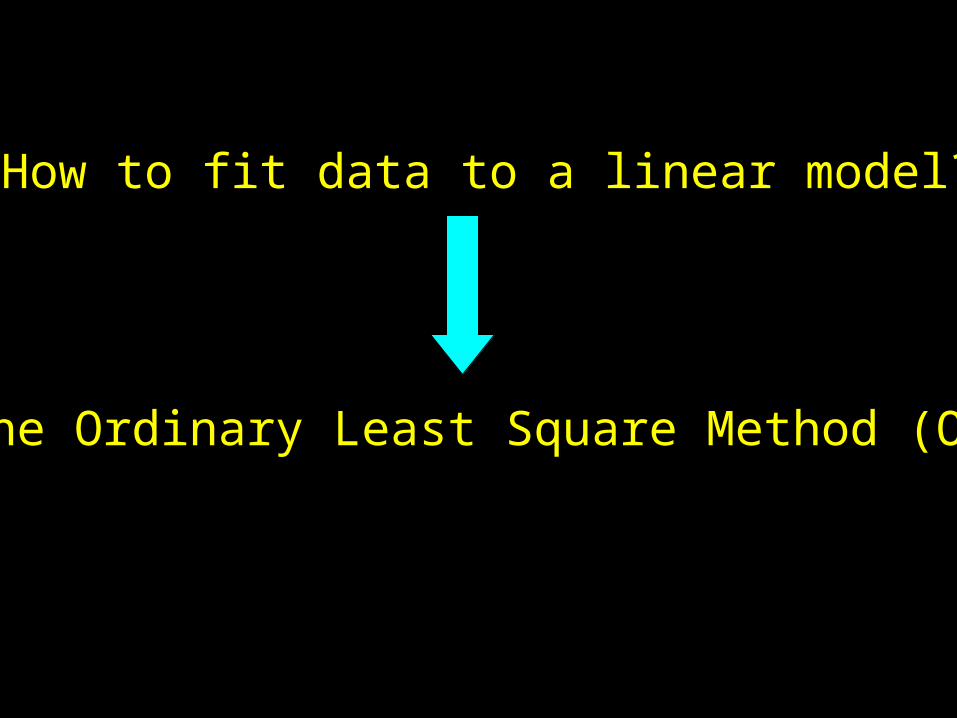

How to fit data to a linear model?

The Ordinary Least Square Method (OLS)

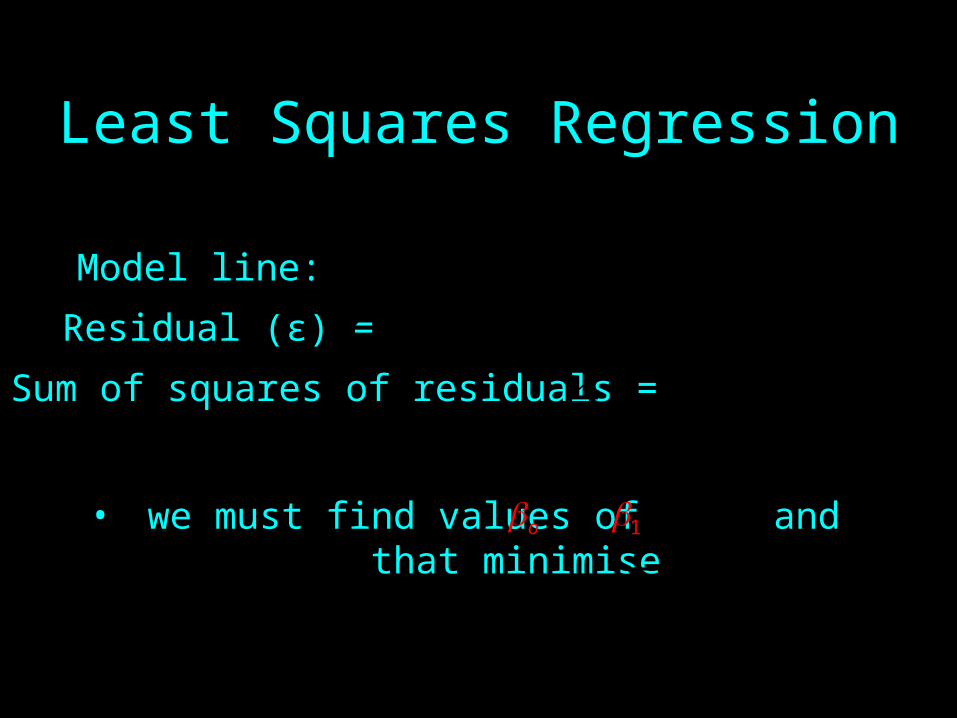

Least Squares Regression

Residual (ε) =

Sum of squares of residuals =

Model line:

• we must find values of and that minimise o 1

XY 10

YY

2)( YY

2)(min YY

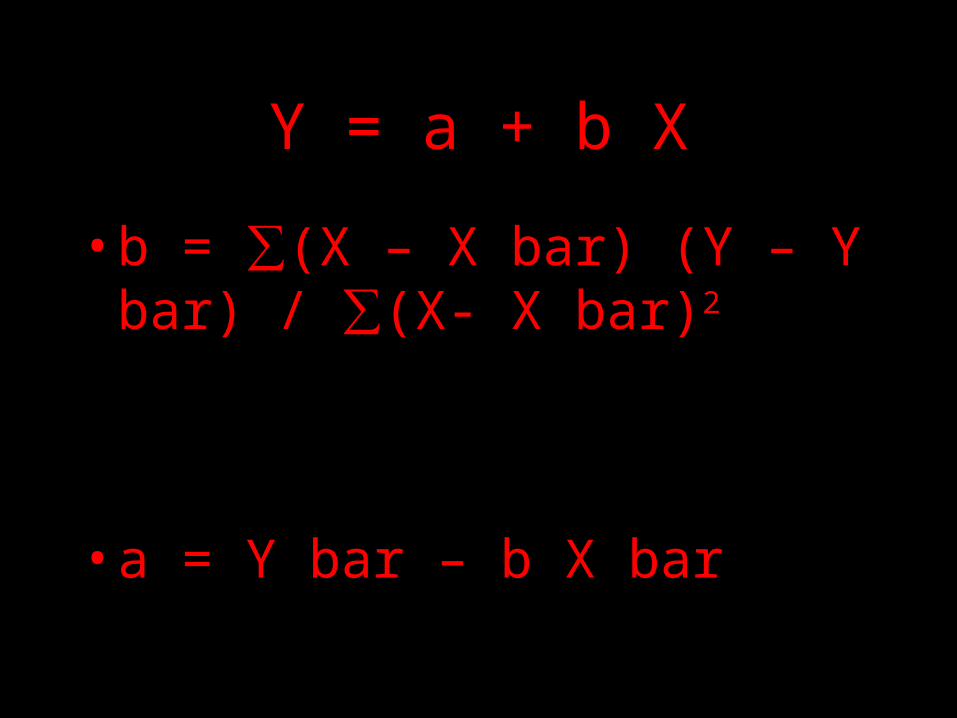

Y = a + b X

• b = ∑(X – X bar) (Y – Y bar) / ∑(X- X bar)2

• a = Y bar – b X bar

Regression Coefficients

21x

xy

xx

xy

S

Sb

XbYb 10

Required Statistics

nsobservatio ofnumber n

n

XX

n

YY

Descriptive Statistics

1

)( 1

2

n

YYYVar

n

i

1

)( 1

2

n

XXXVar

n

i

xxS

)(SSTS yy

xyS 1

),(Covar 1

n

YYXXYX

n

i

Regression Statistics

2)( YYSST

2)( YYSSR

2)( YYSSE

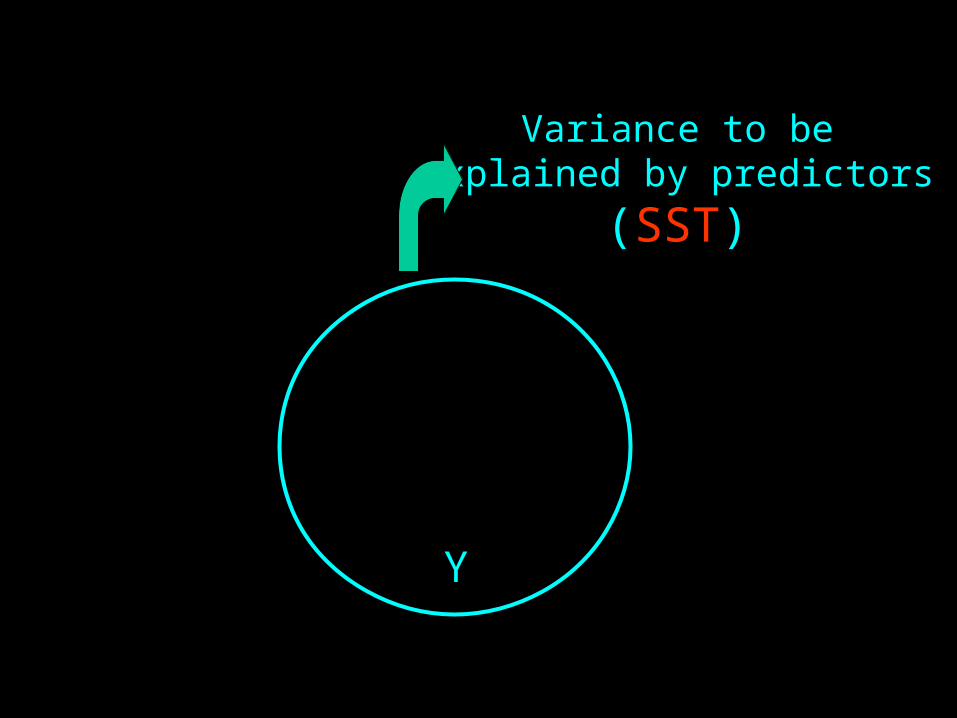

Y

Variance to beexplained by predictors

(SST)

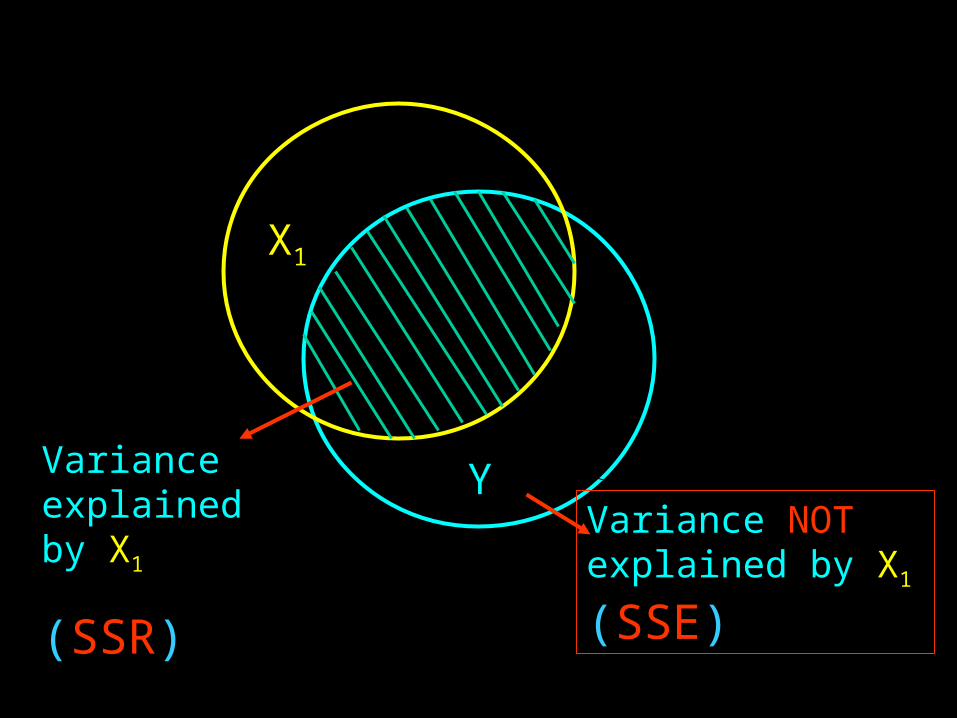

Y

X1

Variance NOT explained by X1

(SSE)

Variance explained by X1

(SSR)

SSESSRSST

Regression Statistics

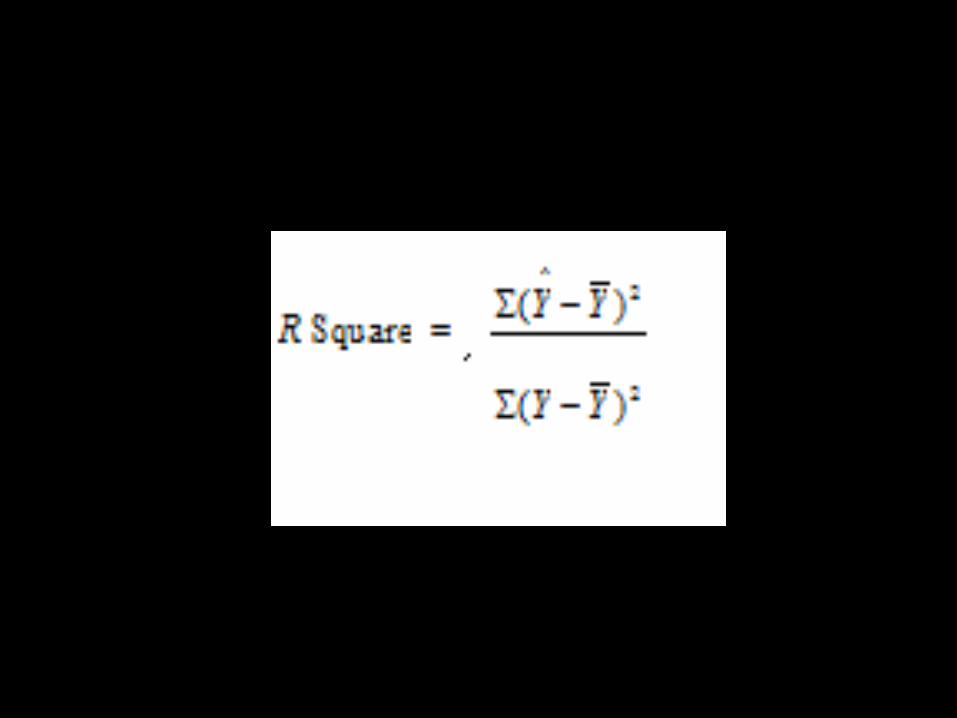

Regression Statistics

SST

SSRR 2

Coefficient of Determinationto judge the adequacy of the regression model

Regression Statistics

yx

xy

yyxx

xy

SS

SR

RR

2

Correlation

measures the strength of the linear association between two variables.

Standard Error for the regression model

MSES

n

SSES

SS

e

e

ee

2

2

22

2

Regression Statistics

2)( YYSSE

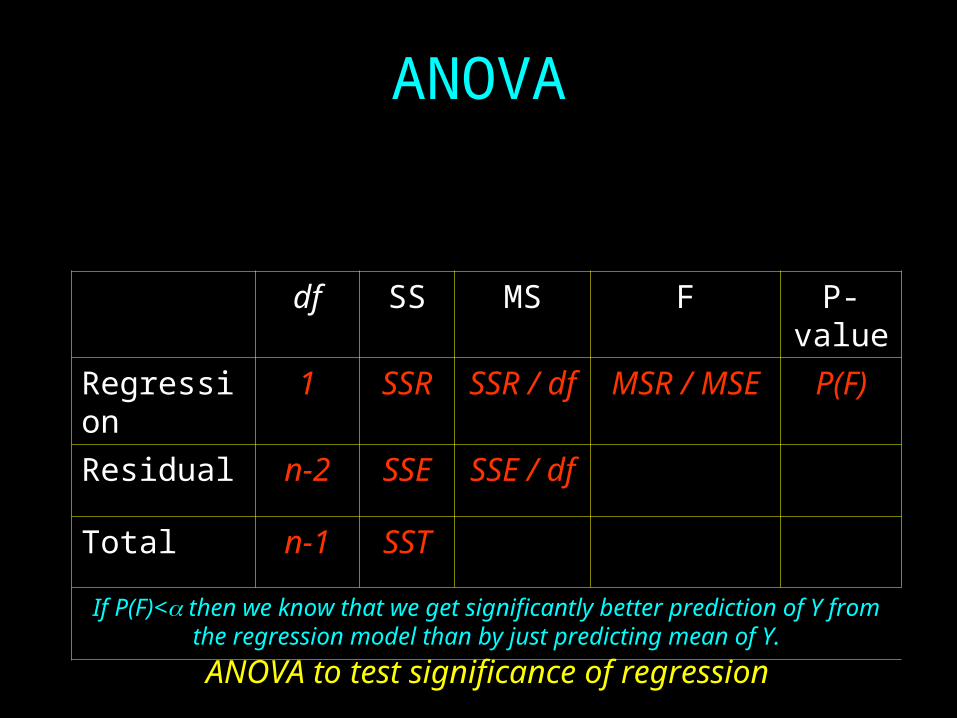

ANOVA

df SS MS F P-value

Regression 1 SSR SSR / df MSR / MSE P(F)

Residual n-2 SSE SSE / df

Total n-1 SST

If P(F)< then we know that we get significantly better prediction of Y from the regression model than by just predicting mean of Y.

ANOVA to test significance of regression

0:

0:

1

10

AH

H

Hypothesis Tests for Regression Coefficients

ib

iikn S

bt

)1(

0:

0:

1

0

i

i

H

H

Hypotheses Tests for Regression Coefficients

xx

eekn

SS

b

bS

bt

2

11

1

11)1( )(

0:

0:

1

10

AH

H

Hypothesis Tests on Regression Coefficients

xxe

ekn

SX

nS

b

bS

bt

22

00

0

00)1(

1)(

0:

0:

0

00

AH

H

Hypotheses Test the Correlation Coefficient

0:

0:0

AH

H

201

2

R

nRT

We would reject the null hypothesis if 2,2/0 ntt

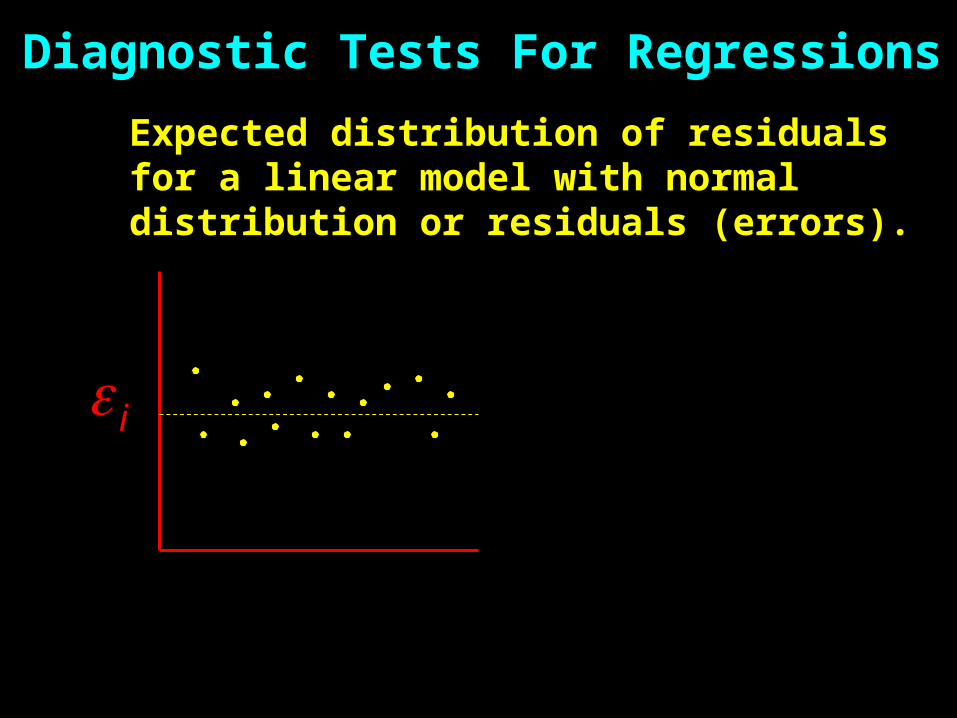

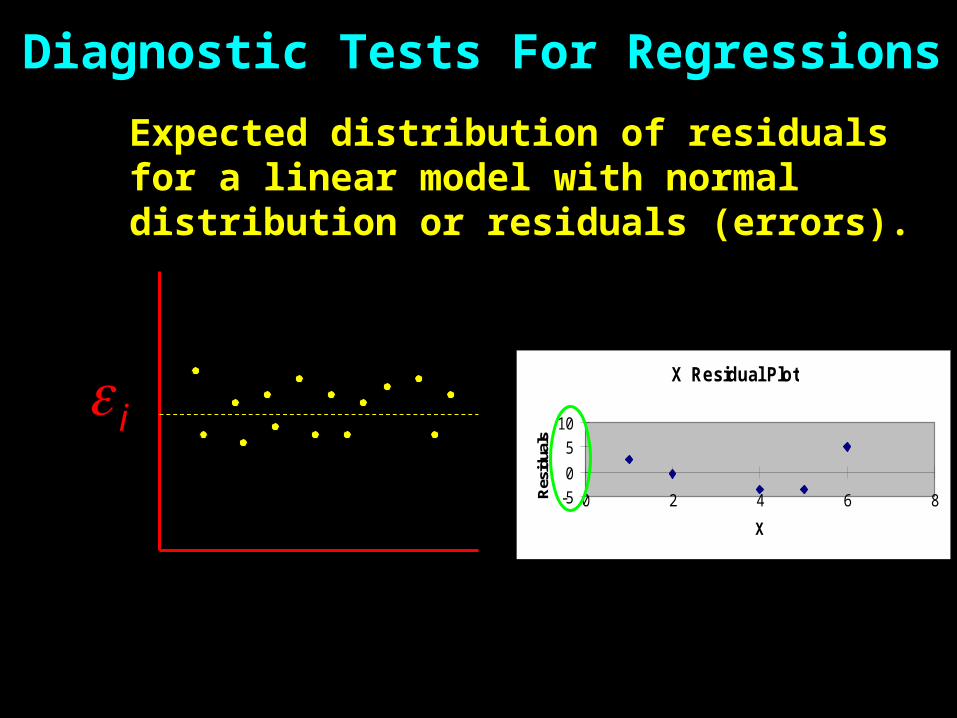

Diagnostic Tests For Regressions

i

Expected distribution of residuals for a linear model with normal distribution or residuals (errors).

iY

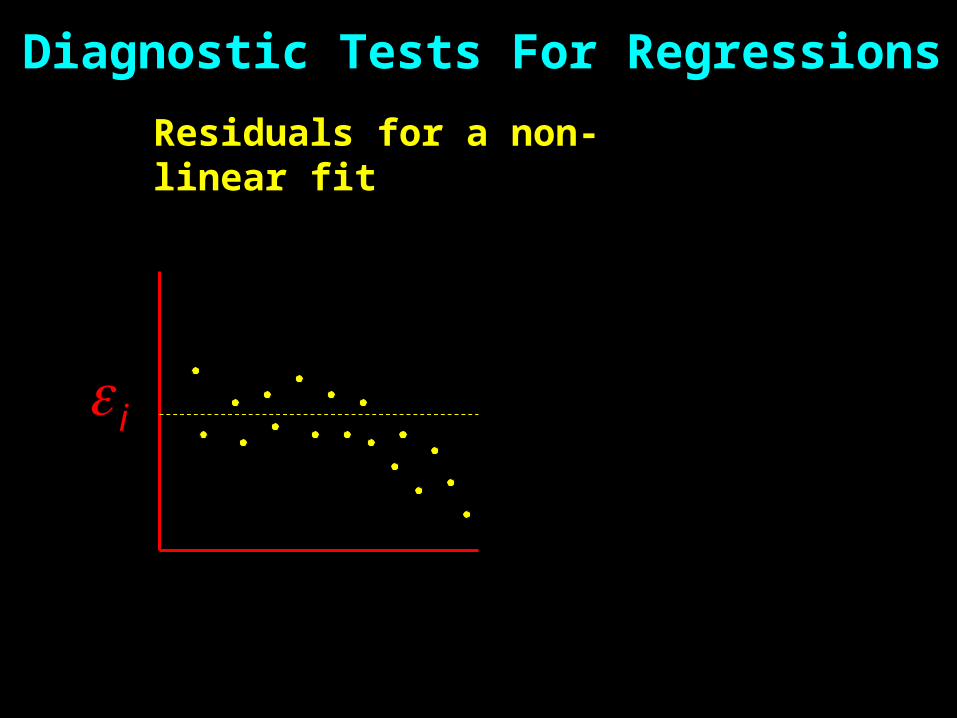

Diagnostic Tests For Regressions

i

Residuals for a non-linear fit

iY

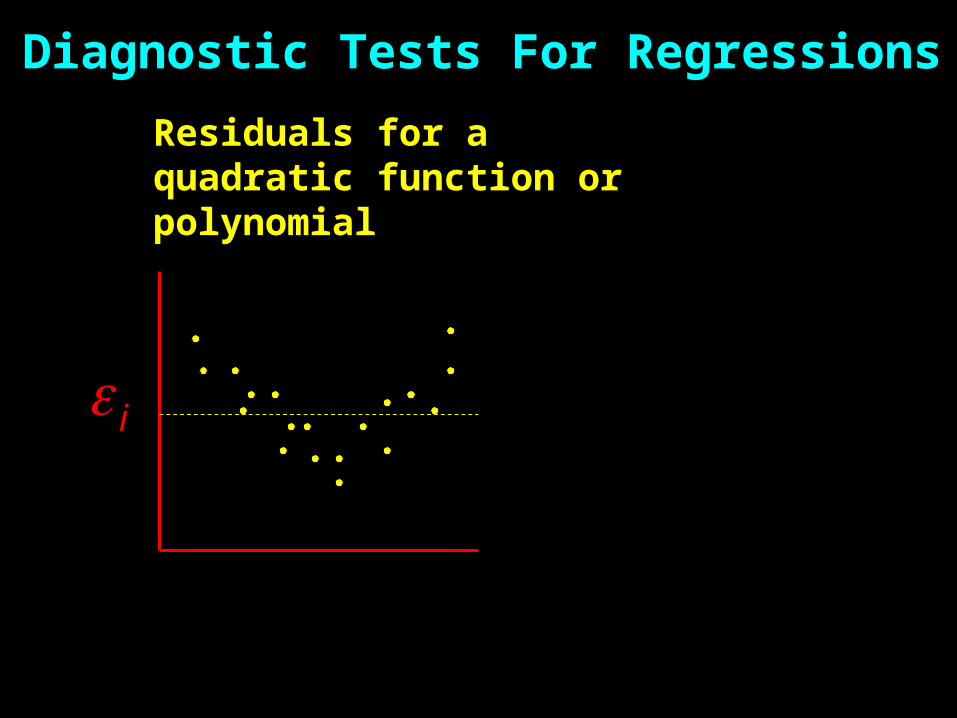

Diagnostic Tests For Regressions

i

Residuals for a quadratic function or polynomial

iY

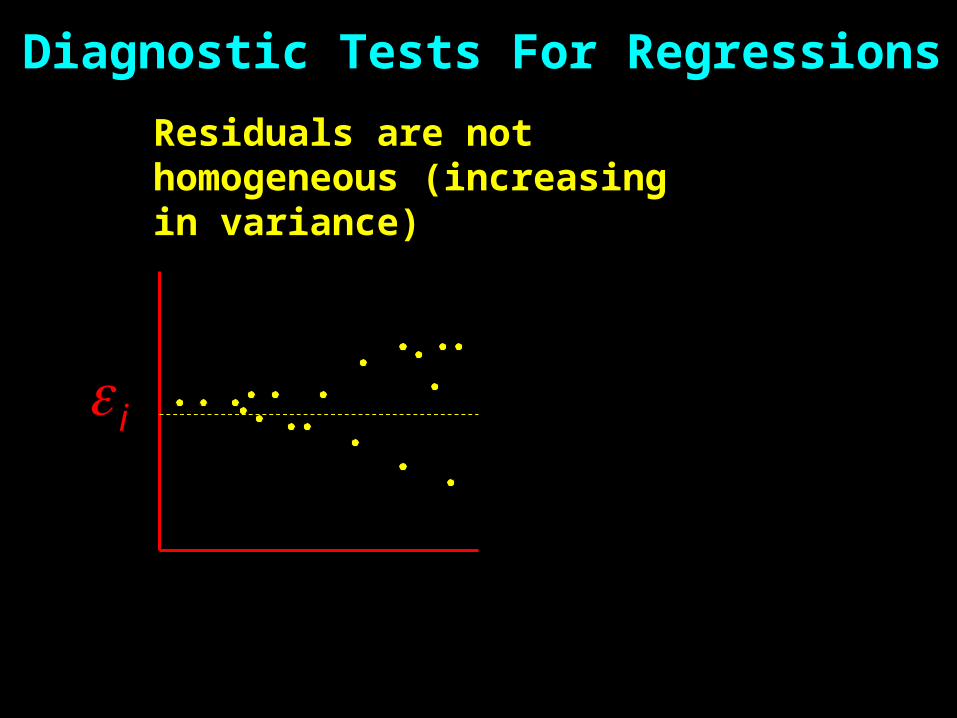

Diagnostic Tests For Regressions

i

Residuals are not homogeneous (increasing in variance)

iY

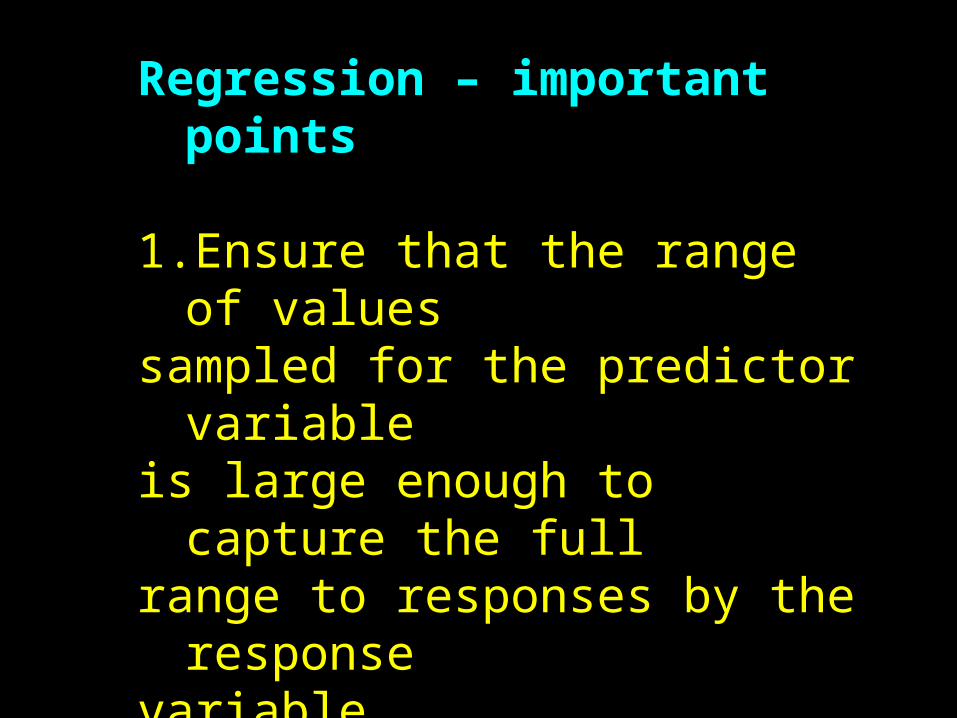

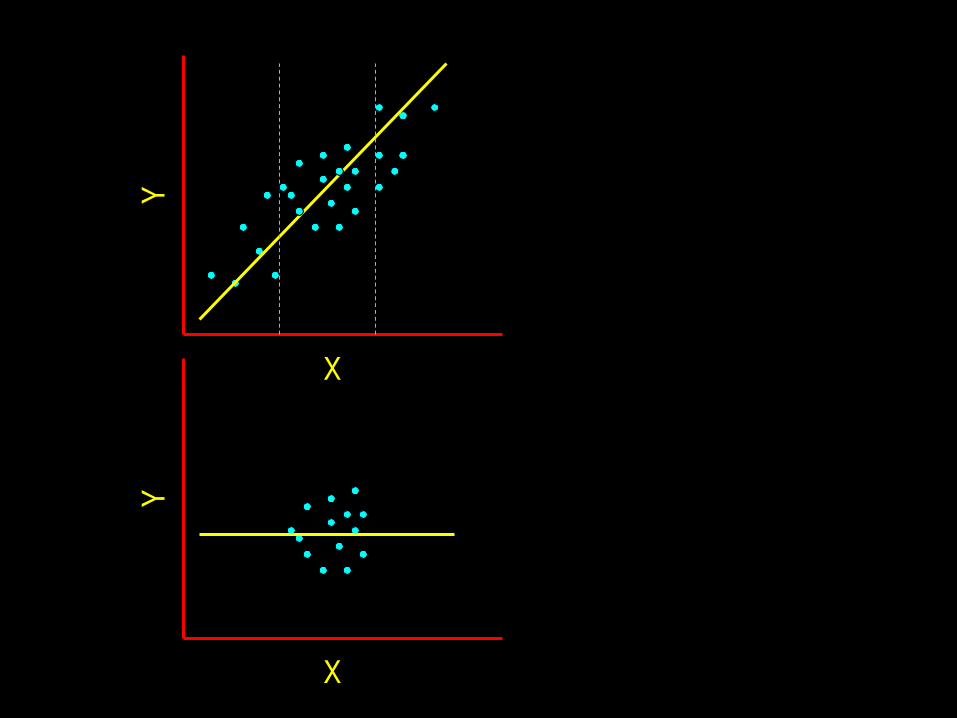

Regression – important points

1. Ensure that the range of valuessampled for the predictor variableis large enough to capture the fullrange to responses by the responsevariable.

X

Y

X

Y

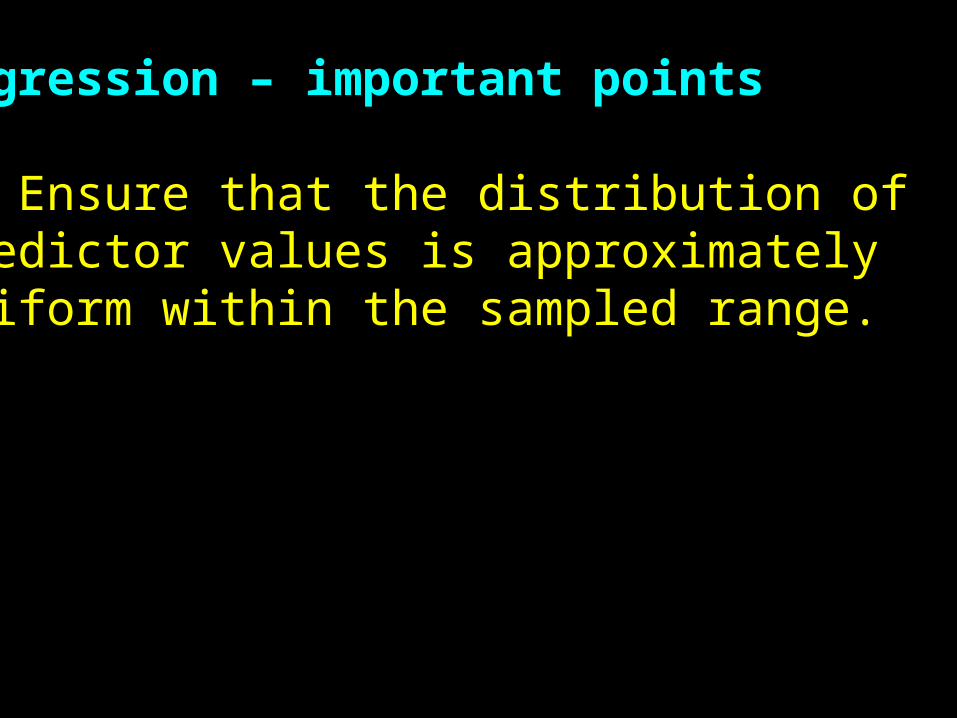

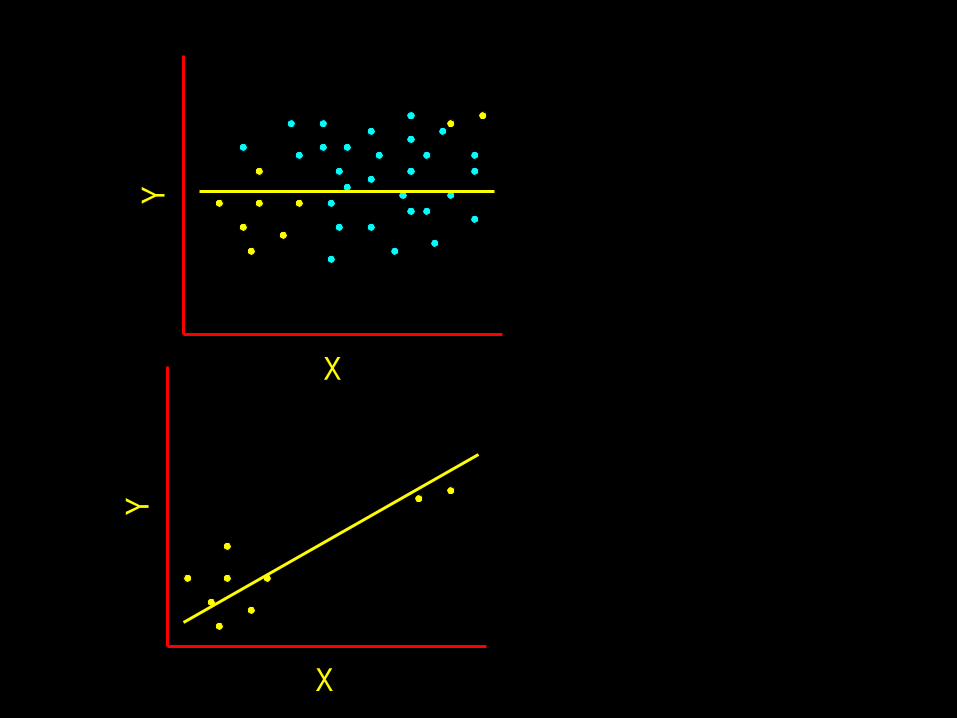

Regression – important points

2. Ensure that the distribution ofpredictor values is approximatelyuniform within the sampled range.

X

Y

X

Y

Assumptions of Regression

1. The linear model correctly describes the functional relationship between X and Y.

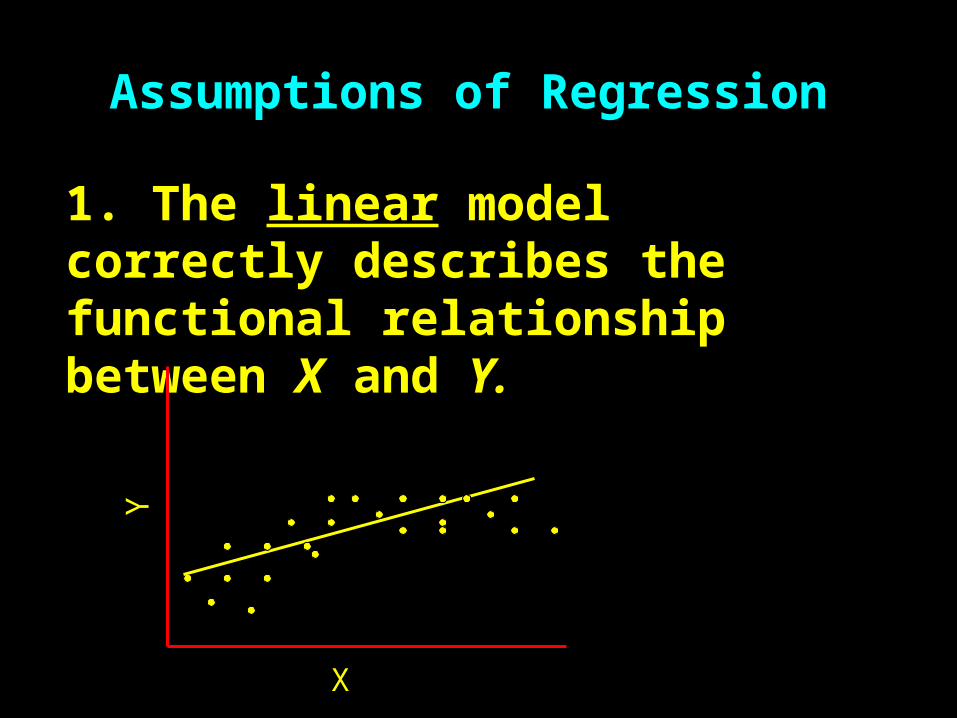

Assumptions of Regression

1. The linear model correctly describes the functional relationship between X and Y.

Y

X

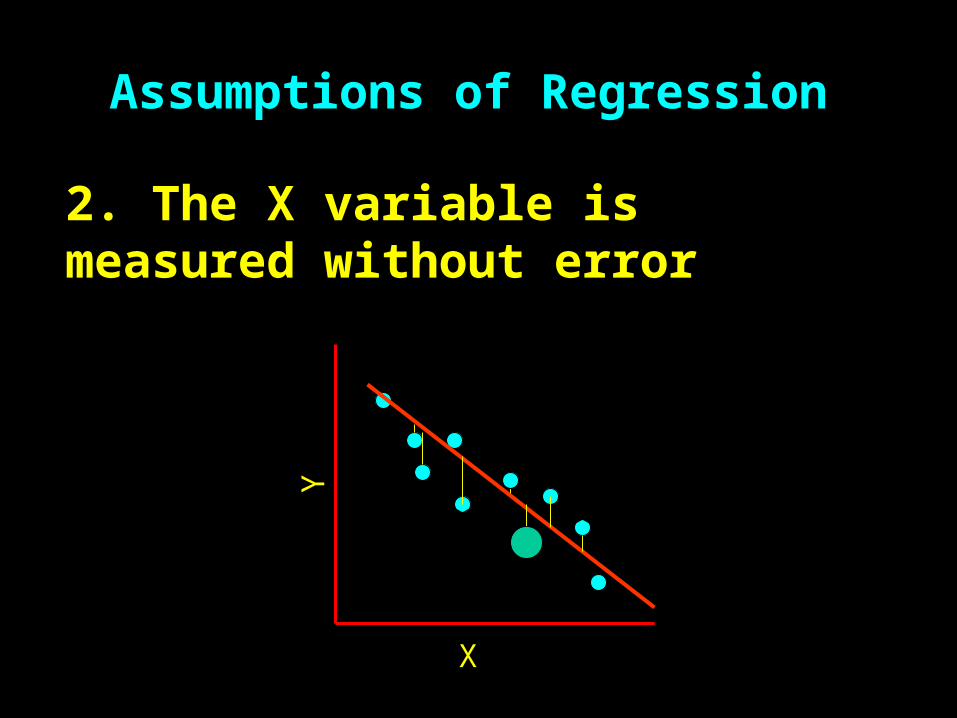

Assumptions of Regression

2. The X variable is measured without error

X

Y

Assumptions of Regression

3. For any given value of X, the sampled Y values are independent

4. Residuals (errors) are normally distributed.

5. Variances are constant along the regression line.

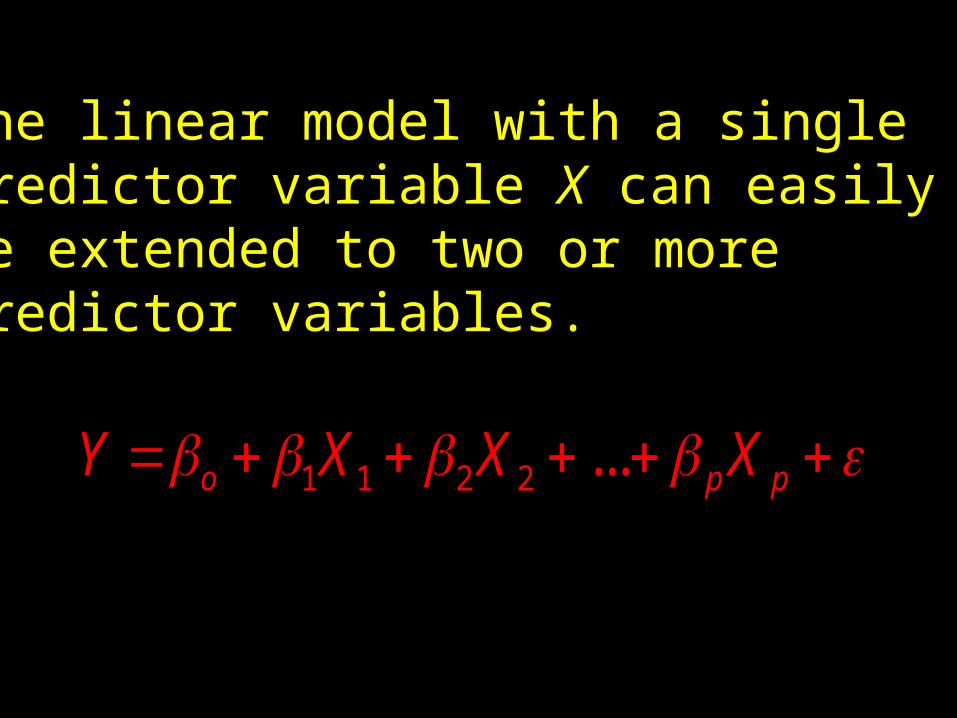

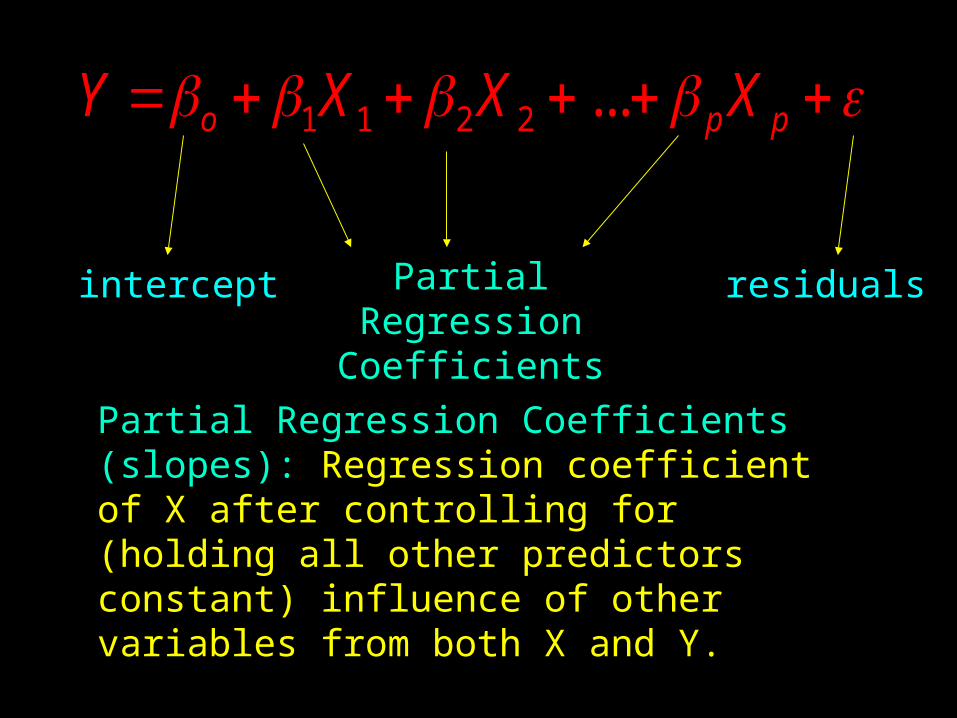

Multiple Linear Regression (MLR)

The linear model with a singlepredictor variable X can easily be extended to two or more predictor variables.

1 1 2 2 ...o p pY X X X

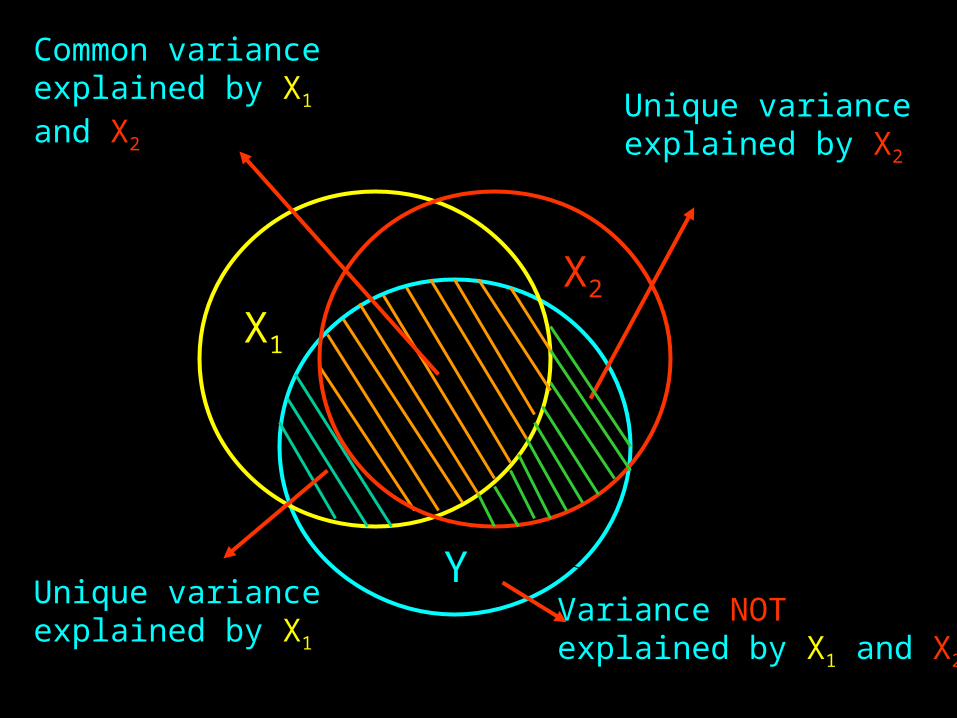

Y

X1

Variance NOT explained by X1 and X2

Unique variance explained by X1

Unique variance explained by X2

X2

Common variance explained by X1 and X2

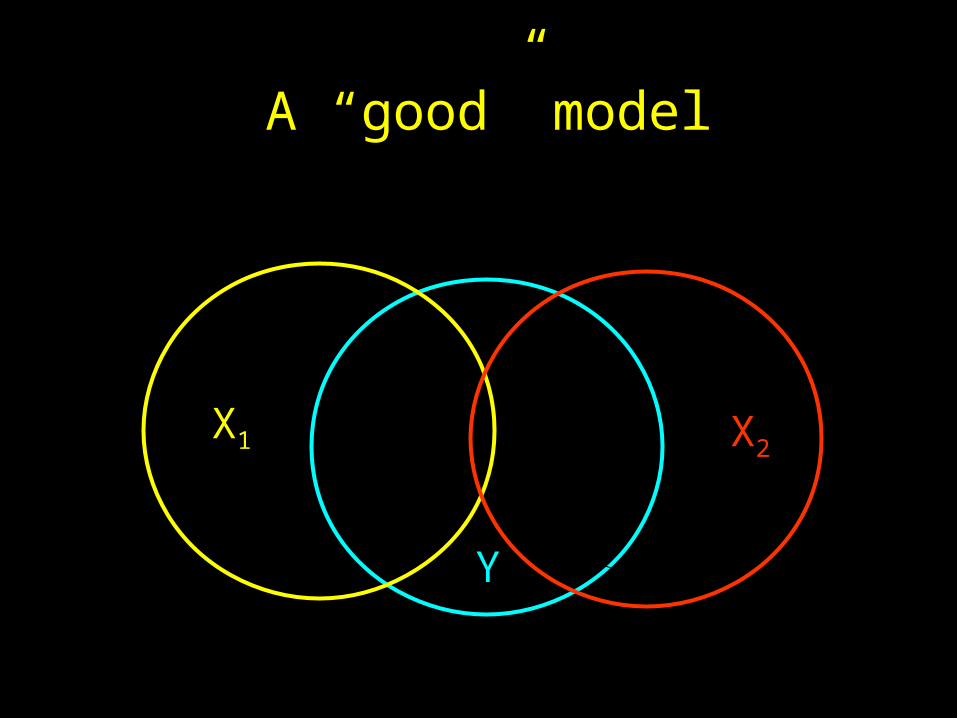

Y

X1 X2

A “good” model

Partial Regression Coefficients (slopes): Regression coefficient of X after controlling for (holding all other predictors constant) influence of other variables from both X and Y.

1 1 2 2 ...o p pY X X X

Partial Regression Coefficients

intercept residuals

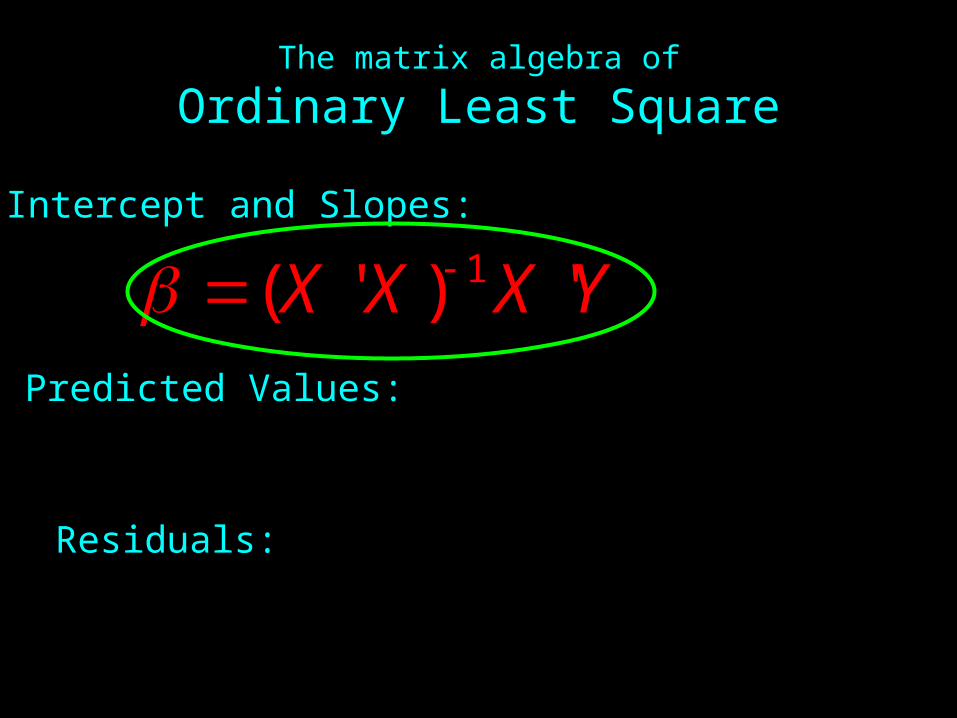

The matrix algebra of

Ordinary Least Square

1( ' ) 'X X X Y Predicted Values:

Residuals:

Intercept and Slopes:

XY

YY

Regression StatisticsHow good is our model?

2)( YYSST

2)( YYSSR

2)( YYSSE

Regression Statistics

SST

SSRR 2

Coefficient of Determinationto judge the adequacy of the regression model

Adjusted R2 are not biased!

n = sample sizek = number of independent variables

)1(1

11 22 R

kn

nRadj

Regression Statistics

Standard Error for the regression model

MSES

kn

SSES

SS

e

e

ee

2

2

22

1

Regression Statistics

2)( YYSSE

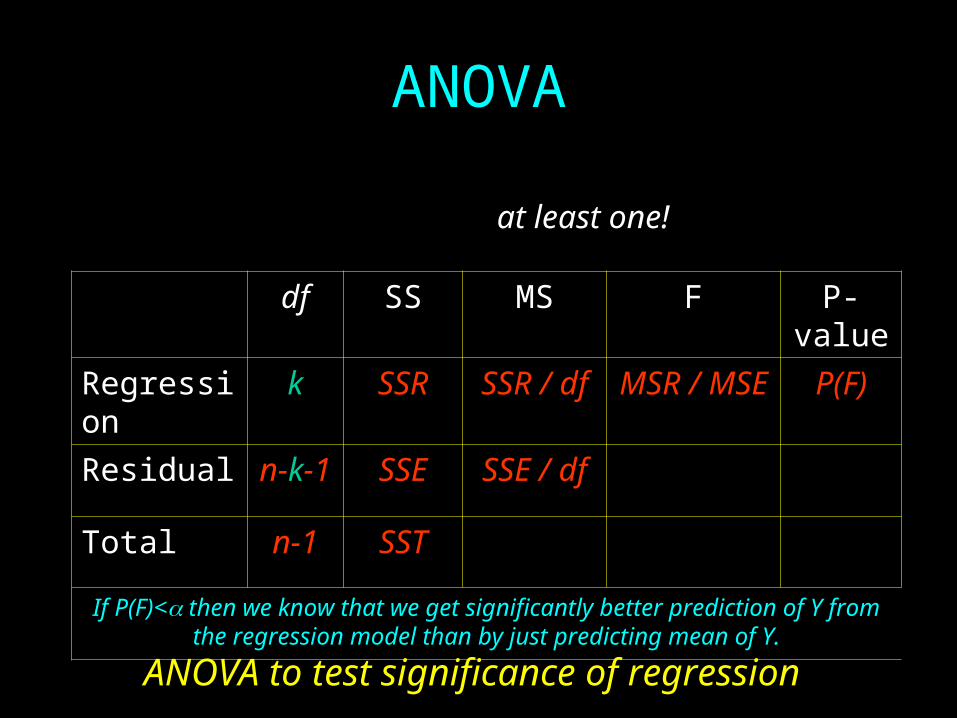

ANOVA

df SS MS F P-value

Regression k SSR SSR / df MSR / MSE P(F)

Residual n-k-1 SSE SSE / df

Total n-1 SST

If P(F)< then we know that we get significantly better prediction of Y from the regression model than by just predicting mean of Y.

ANOVA to test significance of regression

0:

0...: 210

iA

k

H

H

at least one!

Hypothesis Tests for Regression Coefficients

ib

iikn S

bt

)1(

0:

0:

1

0

i

i

H

H

Hypotheses Tests for Regression Coefficients

iie

ii

ie

ikn

CS

b

bS

bt

2

1)1( )(

0:

0:0

iA

i

H

H

xx

e

S

S 2

Diagnostic Tests For Regressions

i

Expected distribution of residuals for a linear model with normal distribution or residuals (errors).

iX

X Residual Plot

-5

0

5

10

0 2 4 6 8

XR

esid

uals

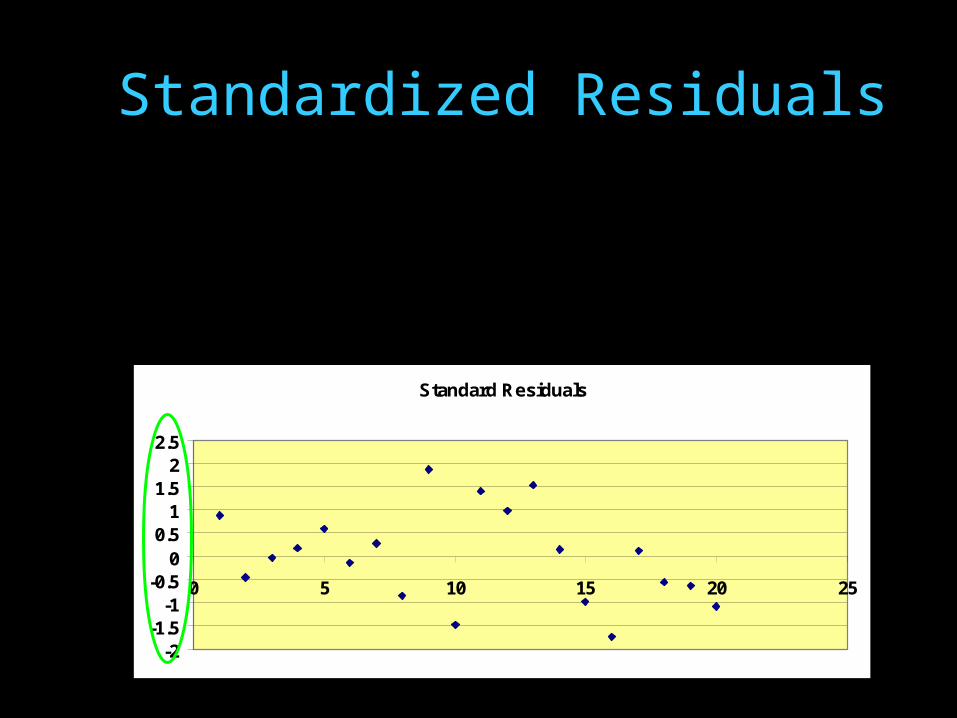

Standardized Residuals

2e

ii

S

ed

Standard Residuals

-2-1.5

-1-0.5

00.5

11.5

22.5

0 5 10 15 20 25

Avoiding predictors (Xs)

that do not contribute significantly

to model prediction

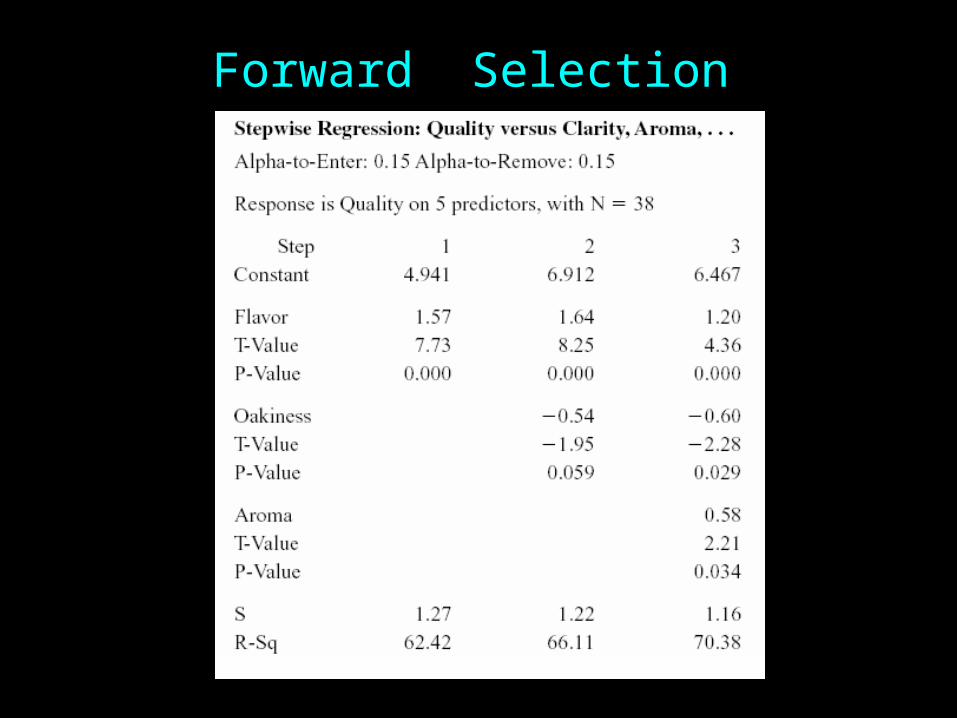

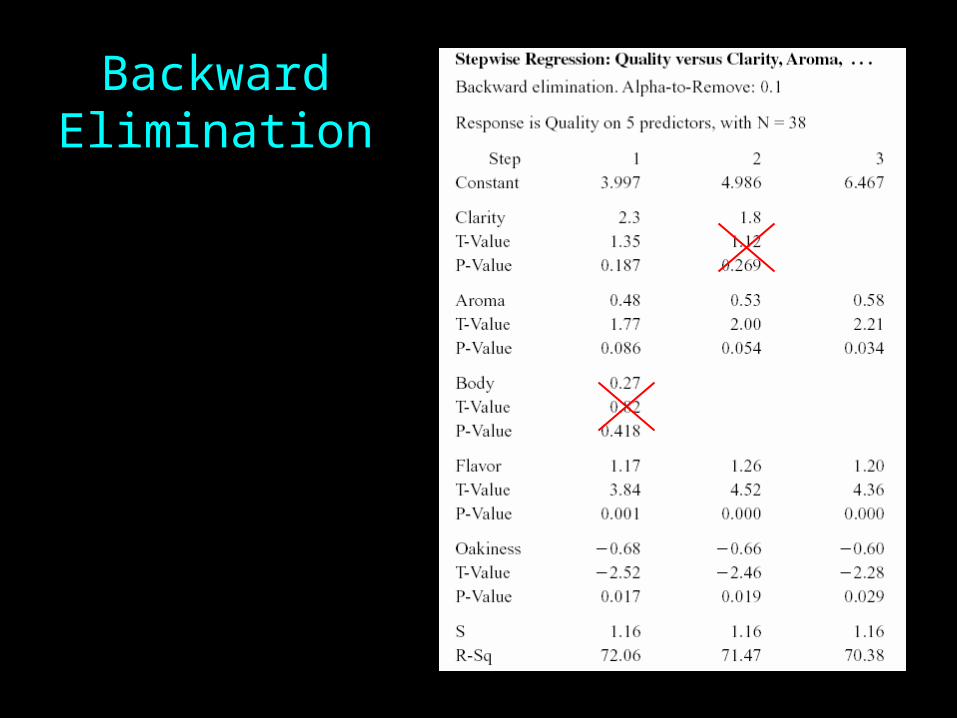

Model Selection

- Forward selectionThe ‘best’ predictor variables are entered, one by one.

- Backward eliminationThe ‘worst’ predictor variables are eliminated, one by one.

Model Selection

Forward Selection

BackwardElimination

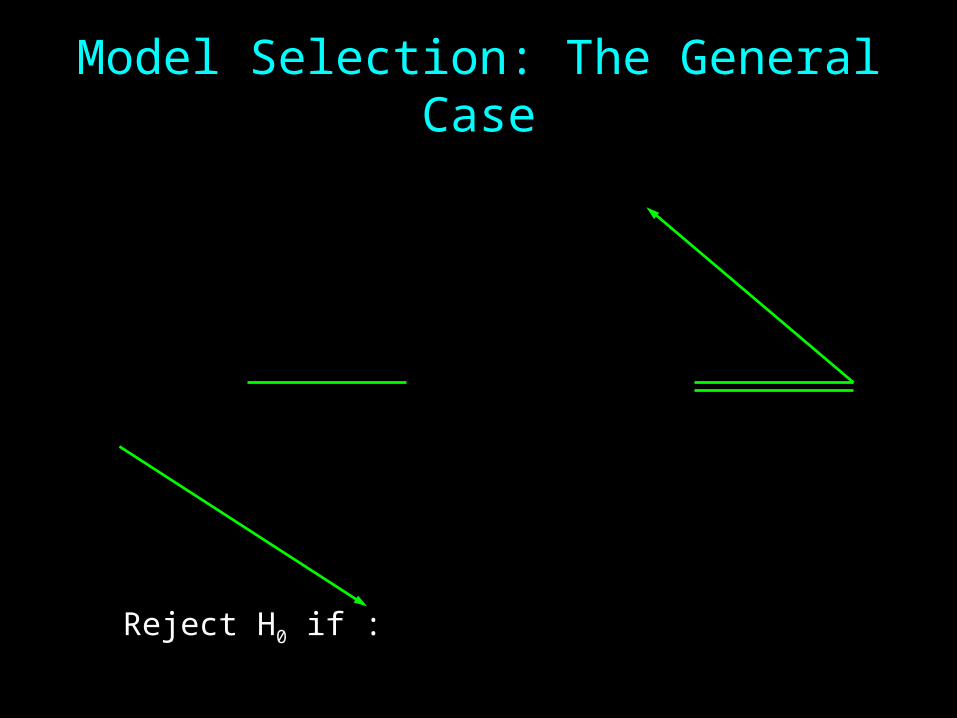

Model Selection: The General Case

1

),...,,,...,,(

),...,,,...,,(),...,,(

121

12121

kn

xxxxxSSEqk

xxxxxSSExxxSSE

Fkqq

kqqq

1,, knqkFF

zeronot in oneleast at :

0...:

1

210

H

H kqq

Reject H0 if :

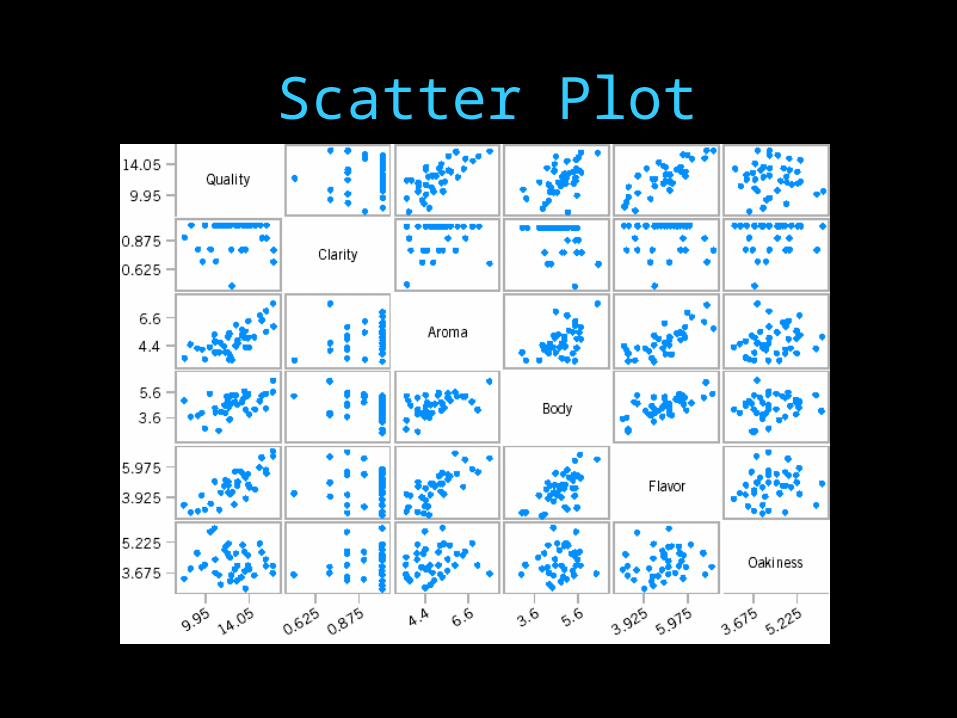

The degree of correlation between Xs.

A high degree of multicolinearity produces unacceptable uncertainty (large variance) in regression coefficient estimates (i.e., large sampling variation)

Imprecise estimates of slopes and even the signs of the coefficients may be misleading.

t-tests which fail to reveal significant factors.

Multicolinearity

Scatter Plot

Multicolinearity

If the F-test for significance of regression is significant, but tests on the individual regression coefficients are not, multicolinearity may be present.

Variance Inflation Factors (VIFs) are very useful measures of multicolinearity. If any VIF exceed 5, multicolinearity is a problem.

iii

i CR

VIF

21

1)(

Thank You!

Top Related