Senior Distinction Papers: Class of 2015 · Africa, Egypt, France, ... as most efficient firms...

108

OMICRON DELTA EPSILON Journal of Economic Research The St. Olaf College Economics Department’s Senior Distinction Papers: Class of 2015

Transcript of Senior Distinction Papers: Class of 2015 · Africa, Egypt, France, ... as most efficient firms...

ΟΔΕOMICRON DELTA EPSILONJournal of Economic Research

The St. Olaf College Economics Department’s

Senior Distinction Papers: Class of 2015

2

Omicron Delta Epsilon International Honor Society in Economics

Beta Chapter: St. Olaf College

Executive Board 2015-2016 President: Alec Paulson

Vice President: Matthew Lasnier

ODE Journal Executive Editor: Joe Briesemeister

ODE Journal Associate Editor: Kelsey Myers

About Omicron Delta Epsilon

Omicron Delta Epsilon is one of the world’s largest academic honor societies.

The objectives of Omicron Delta Epsilon are recognition of scholastic

attainment and the honoring of outstanding achievements in economics, the

establishment of closer ties between students and faculty in economics within

colleges and universities, the publication of its official journal, The American

Economist, and the sponsoring of panels at professional meetings as well as the

Irving Fisher and Frank W. Taussig competitions.

Currently, Omicron Delta Epsilon has 578 chapters located in the United

States, Canada, Australia, the United Kingdom, Mexico, Puerto Rico, South

Africa, Egypt, France, and the United Arab Emirates. With such a broad

international base, chapter activities vary widely, ranging from invited

speakers, group discussions, dinners, and meetings, to special projects such

as review sessions and tutoring for students in economics. Omicron Delta

Epsilon plays a prominent role in the annual Honors Day celebrations at

many colleges and universities.

St. Olaf College’s Beta Chapter of Omicron Delta Epsilon aims to build a bridge

between the economics faculty and students, actively providing input and

assistance as needed to improve departmental events; they also publish an in-

house economics journal, encouraging, reviewing, selecting, and publishing

original work from economics students at the college.

3

The St. Olaf College Economics Department’s

Omicron Delta Epsilon Journal of Economic Research

___________________________________________________

Contents Fall 2015

___________________________________________________

Camille Morley: Sustainability Standards in

Agricultural Exports….....…………….………............4

Tim Tuscher: The Higher Education Predicament: An

Analysis and Solution…………………………....…..16

Erik Springer: Will Dodd-Frank Prevent the Next

Great Recession?.........................................................30

Audrey Kidwell: Post-Decision Regret and the Paradox

of Choice in the College Search..................................55

Brian Hickey: Argentina: The Justifications for which

Argentina Defaulted....................................................79

4

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

Sustainability Standards in Agricultural Exports

Camille Morley

1. Introduction

Faced with vivid images of climate change and environmental

degradation present in the world, economists ponder over practical

instruments to fight the destruction of natural capital. Still, efforts must be

focused on changing the cycle of environmental abuse instead of

compensating its negative externalities. Given the lack of an international

sovereign with power to install universal sustainability and pollution

standards, constituents looking for real impacts in welfare improvement face

a convoluted path to distributive justice of natural resources. In pursuit of

international policy conducted by an independent nation, policymakers must

acknowledge if considerations should be made to the welfare of its future

citizens as well as citizens beyond national borders. These intergenerational

and interspatial boundaries are certainly present in all economic policies, yet

the immanent nature of climate change and exploitation of natural capital

makes this a pressing issue needing immediate response.

In light of global connectivity and the mass movement of food, I

argue that there is an opportunity and responsibility for private, transnational

companies to involve themselves in both efforts. Often time developing

countries, especially those in the Sub-Saharan African region, face low land-

productivity exasperated by lack of capital and education to address

5

“Sustainability Standards in Agricultural Exports” - Camille Morley

constraints placed on their natural resources. Potential investment to

exporting firms in this region could not only provide a steady, reliable supply

for the private companies in the developed world, but also provide poverty

alleviating opportunities through income and education in the developing

world. A study by Arne Bigsten et al. finds a positive stimulus in

productivity after farms begin exporting in the Sub-Saharan African region.

Their research begs the question of causation regarding efficiency and

exporting, as most efficient firms export.1 However, the Heckscher-Ohlin

theorem of international trade confirms that exporting agricultural goods

would be beneficial for the Sub-Saharan region because it uses their abundant

production factors (land and labor) intensively.2 In this paper I will present a

policy proposal for implementing sustainability standards in the Sub-Saharan

region and explain the welfare benefits for constituents involved. Section 1

will discuss a model for my strategy based on the sanitary and phytosanitary

standards (SPS) implemented by the GATT in 1994. Section 2 will explain

the necessary organizational improvements for the smallholder farms on the

supplier side. Section 3 will overview a strategy for private, transnational

supermarkets and food corporations on the buyer-side. The conclusion will

review the welfare implications for all constituents given a successful

1 Winters, A. L., McCulloch, N., McKay, A. (2004). Trade Liberalization and Poverty: The Evidence So Far. Journal of Economic Literature, 42(1), 72-115. http://www.jstor.org/stable/3217037 2 Yarbrough, B., Yarbrough, R. (2005). The World Economy: Trade and Finance. Mason, Ohio: Thomson/South-

Western.

6

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

duplication and implementation of the model and offer insight on the

possibility of future universal sustainability standards.

2. Sanitary and Phytosantary Standards (SPS) Model

During the 1994 Uruguay Round of the GATT, SPS standards were

universally agreed upon to ensure the safety of fresh food (meat, seafood,

vegetables, etc.) being transported and consumed around the world. These

standards included controls on pesticide residues, microbial contamination,

parasites, drug residues, zootomic disease, mycotoxins, and adulterants.3

Unfortunately, the GATT-regulated SPS standards were often the most basic

level of safety standards, promoting individual countries (and their major

supermarkets) to implement further safety standards of their own, as seen in

the example the zero-residue supermarkets in the United Kingdom.4 In many

cases, developing countries would export their fresh food product only to

have it detained and discarded at the ports of importing countries for violating

SPS standards. Many opponents to these standards argued that they acted as a

barrier to trade and discriminated against developing nations lacking the

infrastructure and capital to meet the standards. Because fresh food exports

accounted for around fifty percent of total value of agricultural exports from

3 Unnevehr, L. J. (2000). Food Safety Issues and Fresh Food Exports from LDCs. Agricultural Economics. 23(2000), 231-240. 4 Martinez, M. G., Poole, N. (2004). The development of private fresh produce safety standards: implications for

developing Mediterranean exporting countries. Food Policy. 29(2004), 229-255. Doi:10.1016/j.foodpol.2004.04.002

7

“Sustainability Standards in Agricultural Exports” - Camille Morley

developing nations, the sellers from developing nations and buyers from

developed nations desperately needed organizational coordination.5

NGO certifying organizations met this need and became a way of

ensuring fresh food exports met these standards prior to leaving the

developing country; however, certification costs often limited smallholder

farm participation. In response, a wave of large private companies (Kraft

Foods, Proctor& Gamble, Jakobs Coffee, Ritter, Douwe Egberts) invested

and sponsored certification for these smaller farms, very similar to the

sponsorship movement for smallholder organic certification.6 A study

conducted by the Danish Institute of International Studies in collaboration

with the Sokine University of Agriculture in Tanzania examined the

implementation of these food safety standards on Lake Victoria. They found

that region doubled their fish exports between 1996 and 2005 because of

successful coordination of safety regulatory bodies.7 Private companies

provided credit to fisheries to improve their collection equipment, landing

sites, and temporary storage equipment (cooling buildings). Furthermore, the

establishment of new laboratories and inspection systems to ensured a

consistent, safe supply. Regional success was attributed to a multi-

5 Bolwig, S., Riisgaard, L. Gibbon, P., Ponte, S. (2013). Challenges of Agro-Food Standards Conformity: Lessons from East Africa and Policy Implications. European Journal of Development Research. 5, 411.

Doi:10.1057/edjr.2013.8 6 Bolwig, S., Riisgaard, L. Gibbon, P., Ponte, S. (2013). Challenges of Agro-Food Standards Conformity: Lessons from East Africa and Policy Implications. European Journal of Development Research. 5, 413.

Doi:10.1057/edjr.2013.8 7 Bolwig, S., Riisgaard, L. Gibbon, P., Ponte, S. (2013). Challenges of Agro-Food Standards Conformity: Lessons from East Africa and Policy Implications. European Journal of Development Research. 5, 416.

Doi:10.1057/edjr.2013.8

8

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

stakeholder organizational structure that promoted coordination between

NGOs, investing retailers (supermarkets), and a co-op of smallholder

fisheries, with minimal government involvement.8

3. Organizational Planning

Using the Lake Victoria study as a model, organizational restructuring

could offer similar success if implementing sustainability standards in the

Sub-Saharan region. The question remains, is the study transferable to

agricultural producers looking to improve sustainable practices? To answer

this question, I examine the influence of firm size for farms hoping to

improve their current agricultural techniques and expand their market for

crops.

In a study examining organic-certified smallholder farms in the

developing world that export food products to the EU, economists H.R.

Barret et. al. find that the smallholder farms have competitive prices in the

world market after certification. Additionally, the small size offers better

control on pests and weather fluctuations affecting the delicate crops. Yet the

expensive process of certification, knowledge of reputable certification

bodies, and need for a reliable marketing linkage often discourages

8 Bolwig, S., Riisgaard, L. Gibbon, P., Ponte, S. (2013). Challenges of Agro-Food Standards Conformity: Lessons

from East Africa and Policy Implications. European Journal of Development Research. 5, 410.

Doi:10.1057/edjr.2013.8

9

“Sustainability Standards in Agricultural Exports” - Camille Morley

smallholder farms from even attempting to get certified.9 Essentially, small-

size farms operate well once they are certified organic and have reliable

buyers, but the process of becoming certified and finding buyers is difficult

when lacking capital and opportunities for loans. Connecting this study to

Ronald Coase’s theory of firm size, he would assert that the small farm size

increases its organizational costs. Larger firms will face lower transaction

costs in the market.10

In terms of transferability to agriculture, co-ops are already widely

used in Latin America to convert groups of farms to organic agriculture and

export their products in the growing international market for organic food.11

When implementing sustainable practices, a smaller farm size might also be

beneficial in reducing malpractice and environmentally degrading “mass-

farming”. Barret’s study of organic co-ops in the developing world also states

that self-governed organizing groups help smallholder farms develop

business and localized technical skills that accompany the certification

process.12

Education would be a positive externality and development benefit

for farms originally unable to afford certification, sustainable technology, or

education on their own.

9 Barret, H. R., Browne, A. W., Harris, P.J.C., & Cadoret, K. (2001). Smallholder Farmers and Organic Certification: Accessing the EU Market from the Developing World. Biological Agriculture and Horticulture. 19(2),

185. 10 Coase, R. H. (1937). The Nature of the Firm. Economica. 4(16), 397. http://www.jstor.org/stable/2626876 11 Barret, H. R., Browne, A. W., Harris, P.J.C., & Cadoret, K. (2001). Smallholder Farmers and Organic

Certification: Accessing the EU Market from the Developing World. Biological Agriculture and Horticulture. 19(2),

184. 12 Barret, H. R., Browne, A. W., Harris, P.J.C., & Cadoret, K. (2001). Smallholder Farmers and Organic

Certification: Accessing the EU Market from the Developing World. Biological Agriculture and Horticulture. 19(2),

184.

10

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

Organization within a co-op is equally as important when considering

the diminishing return to the size of management presented in Coase’s theory.

Co-ops must use a thin management structure, essentially led by a single

“export specialist” who ensures compliance by each farm and works directly

with buyers. This structure reduces each individual farm’s transaction costs

while allowing them to maintain control over their small share of land. A

horizontal cooperation based on group responsibility and collective will

should offer better success and avoid administrative barriers caused by too

much vertical management. Furthermore, a cooperative agreement between

farmers gives the group more bargaining power when interacting with

international buyers. Collective power could prevent the exploitation of

smallholders by major “agriculturists”, the major agribusinesses not directly

involved in farming but dependent on the industry for selling products

(Monsanto, DuPont, etc.).13

4. Buyer-Side Incentives and Strategy

In his book, Ethics as Applied Ethics, Beckerman references the

emergence of cosmopolitanism, a notion that places moral equivalence and

impartiality focus on individuals regardless of national boundaries.14

Private

companies that have an international presence best address interspatial and

13 Tisdell, C. (2000). Coevolution, agricultural practices and sustainability: some major social and ecological issues.

International Journal of Agricultural Resources, Governance, and Ecology. 1(1), 6-16.

14 Beckerman, W. (2011). Economics as Applied Ethics: Value Judgments in Welfare Economics. New York, New

York: Palgrave Macmillan.

11

“Sustainability Standards in Agricultural Exports” - Camille Morley

intergenerational welfare issues from this position because their power

transcends national boundaries and exists due to their involvement in the

market.

Why should private companies be interested in paying for sustainably

produced food, let alone invest in technology for smallholder farms to uphold

these practices? I argue the promise of consistent long-run supply through

sustainable practices gives an important edge to global logistics strategy.

Furthermore, due to the growing demand for transparent supply-chains,

corporate social responsibility platforms are having a larger impact on

consumption trends in the developed world. A marketable “sustainable

brand” in the developed world is an important asset for transnational food

corporations, as some consumers now admit through their purchases that they

would prefer to buy a slightly more expensive vegetable knowing that it

wasn’t grown with water full of pesticide.15

Business decisions based solely

on ethics and “do-good” values might not be enough motivation to make an

investment; however, consistent supply and marketing strategy offer financial

benefits incentivizing private companies to take a stake in these projects.

Certainly for the success of a sustainable agriculture policy, clear

objectives must be created and recognized by all constituents involved.

Buyer-end supermarkets must collaborate with certifying NGOs and supplier

co-ops to ensure that sustainable standards are universally recognized.

15 Bolwig, S., Riisgaard, L. Gibbon, P., Ponte, S. (2013). Challenges of Agro-Food Standards Conformity: Lessons

from East Africa and Policy Implications. European Journal of Development Research. 5, 413.

Doi:10.1057/edjr.2013.8

12

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

Collaboration will also prevent differing levels of standards seen in the

implementation of SPS standards. These sustainable practices must reflect the

environmental needs of a region and be localized to preserve natural capital

unique to its environment. A simulation study implementing carbon-

sequestration practices in Kenya and Peru demonstrated the importance of

localizing strategy to maximize improvements to land productivity and

poverty reduction. Terracing provided more productivity increases carbon

preservation in Peruvian land whereas fertilizer usage had a larger effect to

crop yields in Kenya.16

A study by the Copenhagen Business School asserts the importance of

multi-stakeholder involvement connecting the end-consumers, private

companies (supermarkets), NGOs, and supplying farms to ensure

accountability and transparency in the supply chain.17

This extensive

coordination offers the best probability of success for observable welfare

improvements and should ensure the protection of all constituents involved.

Emphasis must also be placed on coordination and communication between

public and private solutions. If public assistance and regulation of

sustainability standards is too centralized, implementation might suffer from

slowed administration and inconsistent government funding. For this reason,

16 Antle, J. M., Stoorvogel, J. J. (2008). Agricultural carbon sequestration, poverty, and sustainability. Environment

and Development Economics, 13 (1), 344. Doi:10.1017/S1355770X08004324 17 Bolwig, S., Riisgaard, L. Gibbon, P., Ponte, S. (2013). Challenges of Agro-Food Standards Conformity: Lessons

from East Africa and Policy Implications. European Journal of Development Research. 5, 408-427.

Doi:10.1057/edjr.2013.8

13

“Sustainability Standards in Agricultural Exports” - Camille Morley

government involvement should only play a minor role and majority of

planning and implementation should be left to the private sector and NGOs.

5. Conclusion

A successful implementation of sustainability standards will offer

welfare benefits to all constituents involved instead of typical “winners” and

“losers”. In regards to supplier, smallholder farms, better practices will

preserve natural capital offering better crop yields and sustained income

through exporting. Organization into co-ops will promote communal support

for land-preserving practices and shared agricultural information and

education. These outcomes will diminish poverty at the micro-level. Buyer,

transnational companies will face a sustainable food supply that not only

ensures ease in supply-chain logistics, but also acts as a marketable aspect in

their corporate social responsibility platform. As sustainably-produced food

becomes a societal norm in the developed world that offers additional

poverty-reducing income to exporting farms in the developing world,

consumption preferences for sustainably produced food will accompany

poverty reduction in developing countries. Sustainability regulation will no

longer be viewed as a discriminating trade-barrier demanded by developed

countries.

Certainly implementing such sustainability standards as a WTO

technical- barrier-to-trade would enforce a unified front against

14

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

environmental degradation; however, the current stagnation in the Doha

rounds of the GATT proves this will not be possible anytime soon. The

plethora of issues regarding agricultural subsides in the developed world,

labor standards, and price stability already pose too much controversy

between developing and developed nations. For this reason, sustainability

standards implemented and demanded by private companies offer more

immediate response to interspatial and intergenerational welfare promotion,

but act as an important guide for an eventual universal recognized

sustainability standard.

15

“Sustainability Standards in Agricultural Exports” - Camille Morley

6. References

Antle, J. M., Stoorvogel, J. J. (2008). Agricultural carbon sequestration,

poverty, and sustainability. Environment and Development

Economics, 13 (1), 327-352. Doi:10.1017/S1355770X08004324

Barret, H. R., Browne, A. W., Harris, P.J.C., & Cadoret, K. (2001).

Smallholder Farmers and Organic Certification: Accessing the EU

Market from the Developing World. Biological Agriculture and

Horticulture. 19(2), 183-199.

Beckerman, W. (2011). Economics as Applied Ethics: Value Judgments in

Welfare Economics. New York, New York: Palgrave Macmillan.

Bolwig, S., Riisgaard, L. Gibbon, P., Ponte, S. (2013). Challenges of Agro-

Food Standards Conformity: Lessons from East Africa and Policy

Implications. European Journal of Development Research. 5, 408-

427. Doi:10.1057/edjr.2013.8

Coase, R. H. (1937). The Nature of the Firm. Economica. 4(16), 386-405.

http://www.jstor.org/stable/2626876

Martinez, M. G., Poole, N. (2004). The development of private fresh produce

safety standards: implications for developing Mediterranean exporting

countries. Food Policy. 29(2004), 229-255.

Doi:10.1016/j.foodpol.2004.04.002

Tisdell, C. (2000). Coevolution, agricultural practices and sustainability:

some major social and ecological issues. International Journal of

Agricultural Resources, Governance, and Ecology. 1(1), 6-16.

Unnevehr, L. J. (2000). Food Safety Issues and Fresh Food Exports from

LDCs. Agricultural Economics. 23(2000), 231-240.

Winters, A. L., McCulloch, N., McKay, A. (2004). Trade Liberalization and

Poverty: The Evidence So Far. Journal of Economic Literature, 42(1),

72-115. http://www.jstor.org/stable/3217037

Yarbrough, B., Yarbrough, R. (2005). The World Economy: Trade and

Finance. Mason, Ohio: Thomson/South-Western.

16

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

The Higher Education Predicament: An Analysis and

Solution Tim Tuscher

1. Introduction

For students in America, the rising costs of college tuition and the

burden of student loan debt may be deteriorating the personal value of a

college degree. On one hand, the cost of earning a college degree has never

been so steep, but on the other, the cost of failing to do so has never been so

severe. This is the great predicament of modern higher education that

confronts our society, and the effects of this intensifying situation have been

substantial. As the support system has fallen off, who pays for the cost of

higher education has dramatically shifted from the university and the state to

students and their families. So far policy makers and the decision making

bodies of higher education institutions alike have failed to resolve this

predicament.

What must first happen is a thorough investigation of the drivers of

rising costs of tuition in order to identify areas for improvement. After this

has been done, the role of government must be examined to determine how to

more efficiently support higher education. This paper explores these issues

comprehensively, relying on empirical analysis and the concept of

distributional fairness in order to propose a solution.

17

“The Higher Education Predicament: An Analysis and Solution” - Tim Tuscher

2. Analysis of the Current State of Higher Education

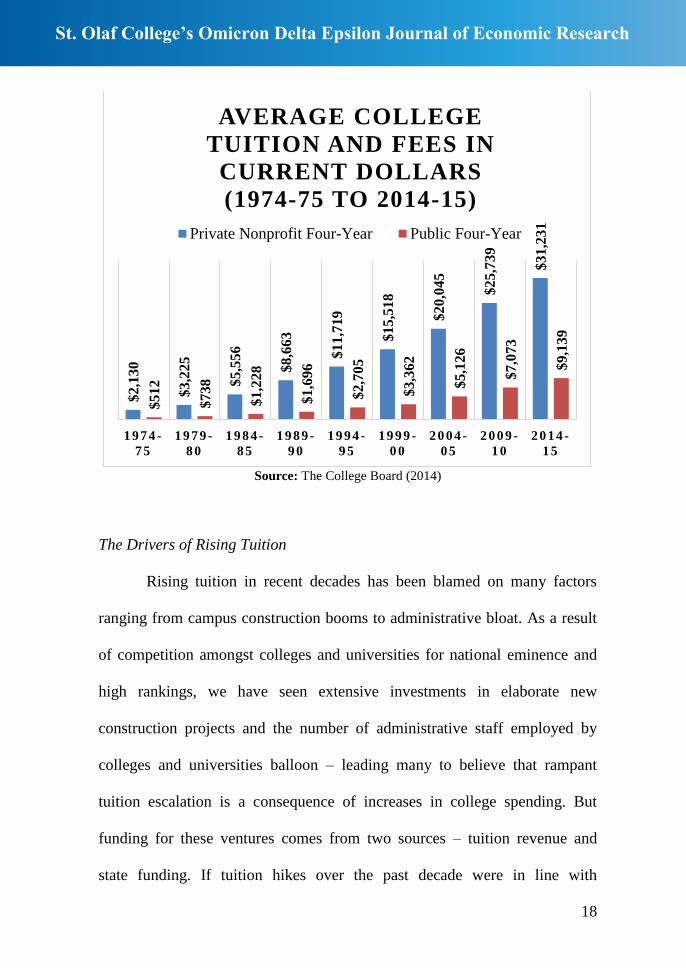

The Rising Price of Higher Education in America

College tuition rates in the United States have increased at a break

neck pace in the last forty years making it more difficult for many Americans

to pay for higher education. In the last forty years, average tuition rates at

private colleges and universities rose an astonishing 1,400 percent.

Meanwhile, public colleges and universities saw average tuition rates

skyrocket 1,700 percent over that same timeframe (The College Board,

2014). Today the cost of attendance, which includes tuition and fees and

room and board, at many four-year private colleges and out-of-state public

universities exceeds $250,000. For residents attending state universities, the

average four-year cost of attendance tops $80,000. These sums do not include

the opportunity cost of forgone earnings. The fact that college tuition has

risen nearly five times as fast as the consumer price index in the last 35 years,

and twice as fast medical care in the last decade further highlights how drastic

these tuition hikes have been (Belkin, 2013). So why has higher education

become so expensive?

18

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

Source: The College Board (2014)

The Drivers of Rising Tuition

Rising tuition in recent decades has been blamed on many factors

ranging from campus construction booms to administrative bloat. As a result

of competition amongst colleges and universities for national eminence and

high rankings, we have seen extensive investments in elaborate new

construction projects and the number of administrative staff employed by

colleges and universities balloon – leading many to believe that rampant

tuition escalation is a consequence of increases in college spending. But

funding for these ventures comes from two sources – tuition revenue and

state funding. If tuition hikes over the past decade were in line with

$2,1

30

$3,2

25

$5,5

56

$8,6

63

$11,7

19

$15,5

18

$20,0

45

$2

5,7

39

$3

1,2

31

$512

$738

$1,2

28

$1,6

96

$2,7

05

$3,3

62

$5,1

26

$7,0

73

$9,1

39

1 9 7 4 -

7 5

1 9 7 9 -

8 0

1 9 8 4 -

8 5

1 9 8 9 -

9 0

1 9 9 4 -

9 5

1 9 9 9 -

0 0

2 0 0 4 -

0 5

2 0 0 9 -

1 0

2 0 1 4 -

1 5

AVERAGE COLLEGE

TUITION AND FEES IN

CURRENT DOLLARS

(1974-75 TO 2014-15)

Private Nonprofit Four-Year Public Four-Year

19

“The Higher Education Predicament: An Analysis and Solution” - Tim Tuscher

expenditure increases, causality could be concluded. Yet, tuition prices in the

last decade rose 24 percent, three times as fast as overall expenditures per

student. These great tuition increases, coupled with low expenditure growth,

suggest that excessive spending cannot account for the degree to which

tuition prices have increased. The driving force behind tuition escalation over

the last decade, as it turns out, is declining state appropriations for higher

education (Hiltonsmith, 2015).

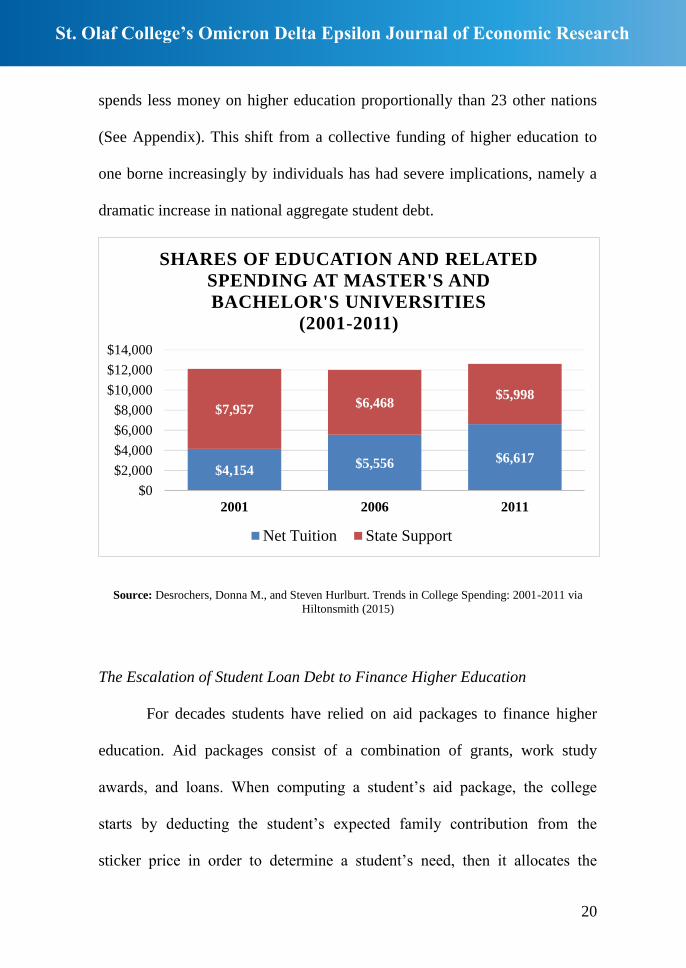

As tuition prices continue to soar, state appropriations for higher

education are deteriorating. The volatile economic environment put

tremendous strain on state budgets across the nation, and governments

decided they could no longer afford to bankroll universities as generously as

they had in previous years. As the figure below shows, state support for

master’s and bachelor’s universities fell 25 percent, $2,067 per student, in the

last decade in lockstep with tuition increases. This lack of funding has

resulted in an inability for colleges universities to offer the same level of

financial aid they had offered in the past. And thus, the depletion of state

funds forced universities and colleges to generate revenue elsewhere.

Elsewhere, as it turns out, came in the form of tuition increases to students.

The depletion of state caused a dramatic shift in the share of expenses paid

for by students and governments. The reality is that as of 2011, a public

higher education no longer exists. Over half of the costs of higher education

are paid for by tuition, a private source of capital. Internationally, the US

20

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

spends less money on higher education proportionally than 23 other nations

(See Appendix). This shift from a collective funding of higher education to

one borne increasingly by individuals has had severe implications, namely a

dramatic increase in national aggregate student debt.

Source: Desrochers, Donna M., and Steven Hurlburt. Trends in College Spending: 2001-2011 via

Hiltonsmith (2015)

The Escalation of Student Loan Debt to Finance Higher Education

For decades students have relied on aid packages to finance higher

education. Aid packages consist of a combination of grants, work study

awards, and loans. When computing a student’s aid package, the college

starts by deducting the student’s expected family contribution from the

sticker price in order to determine a student’s need, then it allocates the

$4,154 $5,556 $6,617

$7,957 $6,468

$5,998

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2001 2006 2011

SHARES OF EDUCATION AND RELATED

SPENDING AT MASTER'S AND

BACHELOR'S UNIVERSITIES

(2001-2011)

Net Tuition State Support

21

“The Higher Education Predicament: An Analysis and Solution” - Tim Tuscher

federal money the student is eligible for, and then and only then will the

university pull from its own resources to complete the student’s aid package.

For students, the portion of the bill that is left over after a student receives his

or her aid package has increased substantially in recent decades.

While the cost of going to college is rising, the cost of not going to

college has never been higher. “On virtually every measure of economic

well-being and career attainment—from personal earnings to job satisfaction

to the share employed full time—young college graduates are outperforming

their peers with less education. And when today’s young adults are compared

with previous generations, the disparity in economic outcomes between

college graduates and those with a high school diploma or less formal

schooling has never been greater in the modern era” (The Rising Cost of Not

Going to College, 2014).

These factors – the high cost of tuition, the shift from a collective

funding of higher education to one borne increasingly by individuals, and the

high cost of not going to college – have come at a time when average real

income growth has been stagnate in the United States, meaning higher

education is becoming increasingly less affordable for most Americans

(Lorin, 2014). American households faced the same budgetary pressures that

states faced during the recession, but one outcome of the recession and the

slow economic recovery is the stress that it has placed on household’s ability

to pay for college from their income and savings. This means families must

22

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

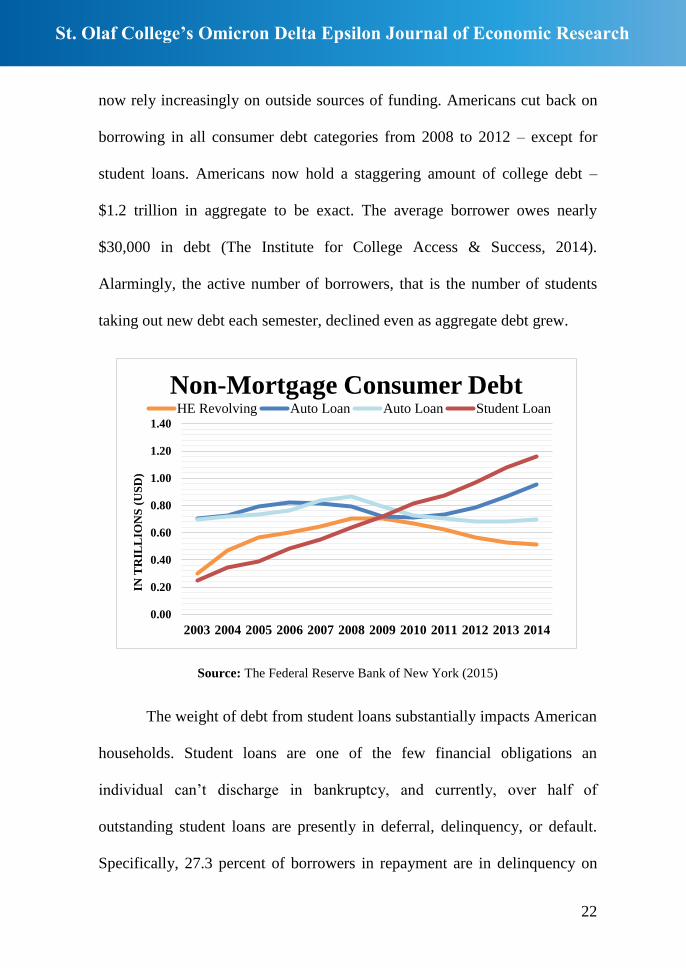

now rely increasingly on outside sources of funding. Americans cut back on

borrowing in all consumer debt categories from 2008 to 2012 – except for

student loans. Americans now hold a staggering amount of college debt –

$1.2 trillion in aggregate to be exact. The average borrower owes nearly

$30,000 in debt (The Institute for College Access & Success, 2014).

Alarmingly, the active number of borrowers, that is the number of students

taking out new debt each semester, declined even as aggregate debt grew.

Source: The Federal Reserve Bank of New York (2015)

The weight of debt from student loans substantially impacts American

households. Student loans are one of the few financial obligations an

individual can’t discharge in bankruptcy, and currently, over half of

outstanding student loans are presently in deferral, delinquency, or default.

Specifically, 27.3 percent of borrowers in repayment are in delinquency on

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

IN T

RIL

LIO

NS

(U

SD

)

Non-Mortgage Consumer Debt HE Revolving Auto Loan Auto Loan Student Loan

23

“The Higher Education Predicament: An Analysis and Solution” - Tim Tuscher

student loans, a percentage far higher than for other forms of consumer credit

including credit cards, mortgages and auto loans (Sánchez, 2015). Student

loan delinquencies and repayment problems create a very difficult downward

spiral and reduce a borrower’s ability to form their own households and

engage in the economy (Lee, 2015). There is, without question, cause for

growing concern over the debt burden many students take on to get a college

education because the ramifications of failing to keep tuition and debt loads

in check could be severe.

3. Friedman’s Solution

Significant effort must be made to reduce the costs of college tuition

or Americans will continue to borrow in order to finance higher education.

Declining state appropriations for higher education mean that many students

today have no choice but to take on significant debt to finance their

educations, the negative effects of which are becoming increasingly evident.

While there is no single course of action that the Federal Government can

take to deter the reliance on student debt, it can however implement several

policy measures to alleviate the burden of student debt. First, the government

must start viewing higher education as a priority. The government should

increase grants for students with the greatest financial need, adjust the

expected family contribution formula to encourage colleges and universities

24

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

to create more realistic aid packages, and restructure the student loan system

to make the debt burden more sustainable.

A more innovative approach, as proposed by Milton Friedman in The

Role of Government in Higher Education (1955), could transform the way we

think about higher education, but more importantly – the way we finance it.

To Friedman, the issue is that we as taxpayers socialize the losses associated

with student loans while at the same time privatizing the gains. When a low-

income borrower cannot service their student loan debt, they default, leaving

taxpayers to foot the bill. On the other hand, high-income borrowers

successfully service their loans then continue to individually benefit from the

dividends of the initial loan. His remedy to this dilemma isn’t for the

government to become a more favorable lender, but for it to become a savvy

investor.

Under Friedman’s plan, the government would provide students with

financial backing to pay for college and, in return, the students would pay a

percentage of their income back to the government each year – regardless of

the amount of money initially invested in them. The way things are currently,

when the government issues a loan it is agreeing with the borrower that it will

get back the principal plus interest, no more, no less. Once the borrower

repays the loan plus interest, he or she is free of the debt obligation. Under

this new system, a student who generates a big return on his or her education

investment shares it with taxpayers by repaying more than the original

25

“The Higher Education Predicament: An Analysis and Solution” - Tim Tuscher

investment. A student who doesn’t generate as great as a return, never pays

back the total amount invested in him or her. So rather than socializing the

losses and privatizing the gains, Friedman’s plan would socialize both the

losses and gains. Private arrangements could work towards the same ends.

The benefits of a private initiative are significant, as it would allow the

government to, according to Friedman, “serve its proper function of

improving the operation of the invisible hand without substituting the dead

hand of bureaucracy” while “eliminating existing imperfections in the capital

market and so widen the opportunity of individuals to make productive

investments in themselves.”

If we were to hold up the current American higher education system

to the Rawlsian ideal, we would discover a system that systematically

disadvantages the poor. Higher education, in its current state, does not

increase social mobility, but rather reinforces existing barriers. While there is

little common ground between social liberalists like John Rawls and free

market capitalists like Milton Friedman, there is reason to believe Rawls

would support a higher education solution packaged as an equity investment.

Friedman’s proposal would have significant impact on the equality of

opportunity in America and go a long way in eliminating the economic

barriers to higher education. However unlikely that it may be to return

ourselves to the original position and negotiate a new social contract behind a

veil of ignorance, we can negotiate a new way of financing higher education.

26

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

4. Conclusion

Higher education is a true public good – we depend on the system to

produce doctors, nurses, teachers, accountants and other professionals, as

well as to help us develop the critical thinking skills needed to succeed in a

very competitive global economy. Yet, it has become increasingly difficult to

afford higher education in America ever since states decided that they would

no longer bankroll as generously as they previously had. Tuition has spiraled

out of control. State funding on a per student basis has fallen off. And so the

burden of funding our higher education system has shifted from the university

and the state to students and their families. The result has been the debt-for-

diploma system in which most students fill the gap between what their

parents can pay, available grant aid and their earnings from part-time work,

by taking on student debt.

We must find a way out of this predicament. To do so, we must first

demand that the government appropriates more funding for higher education.

This will combat rising tuition fees. But restoring state support for higher

education is only a start. We need to establish new ways for families to

finance higher education without relying on massive loads of student debt.

One such way which Milton Friedman proposes is for the government and

private enterprises to engage in equity investments in students, so as to widen

access to higher education without leveraging their futures.

27

“The Higher Education Predicament: An Analysis and Solution” - Tim Tuscher

5. References

"A Flagging Model." The Economist. The Economist Newspaper, 28 March,

2015. Web. 18 April, 2015.

<http://www.economist.com/news/special-report/21646988-americas-

higher-education-system-no-longer-delivering-all-it-should-flagging-

model>>.

Beckerman, Wilfred. “Economics as applied ethics: value judgements in

welfare economics.” Palgrave Macmillan, 2010.

Belkin, Douglas. "How to Get College Tuition Under Control." WSJ. 8 Oct.

2013. Web. 3 May 2015.

Christensen, Clayton M., and Henry J. Eyring. The innovative university:

Changing the DNA of higher education from the inside out. John

Wiley & Sons, 2011.

Dewan, Shaila. "Wage Premium From College Is Said to Be Up." Economix.

11 February, 2014. Web. 21 April,

2015.<http://economix.blogs.nytimes.com/2014/02/11/wage-

premium-from-college-is-said-to-be-up/?_r=0>>.

Eberly, Jane and Martin, Carmel. “The Economic Case for Higher

Education” The Treasury Notes Blog. Web. 2 May 2015.

<http://www.treasury.gov/connect/blog/Pages/economics-of-higher-

education.aspx>.

Friedman, Milton. "The Role of Government in Education (1955)." The

Friedman Foundation for Educational Choice

RSS.<http://www.edchoice.org/The-Friedmans/The-Friedmans-on-

School-Choice/The-Role-of-Government-in-Education-

%281995%29.aspx>.

Hiltonsmith, Robert. "Pulling Up the Higher-Ed Ladder: Myth and Reality in

the Crisis of College Affordability." Demos.org. 5 May 2015. Web.

Jenkins, Jay. "The Ugly Truth Behind the Student Loan Crisis." 25 April,

2015. Web. 27 April, 2015. <http://www.fool.com/how-to-

invest/personal-finance/credit/2015/04/25/the-ugly-truth-behind-the-

student-loan-crisis.aspx>>.

Johansson, Per-Olov. “An introduction to modern welfare economics.”

Cambridge University Press, 1991.

Lee, Donghoon. "Household debt and credit: student debt." Federal Reserve

Bank of New York. February 28 (2013).

28

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

Lorin, Janet. "College Tuition in the U.S. Again Rises Faster Than Inflation."

Bloomberg.com. Bloomberg, 12 Nov. 2014. Web. 4 May 2015.

Mitchell, Josh. "The Student-Loan Problem Is Even Worse Than Official

Figures Indicate." Real Time Economics RSS. The Wall Street

Journal, 14 Apr. 2015. Web. 11 May 2015.

<http://blogs.wsj.com/economics/2015/04/14/the-student-loan-

problem-is-even-worse-than-official-figures-indicate/>.

Rawls, John. “A Theory of Justice.” Harvard university press, 2009.

Sánchez, Jaun. "Student Loan Delinquency: A Big Problem Getting Worse?" -

St. Louis Fed. N.p., n.d. Web. 11 May 2015.

<http://research.stlouisfed.org/publications/es/article/10344>.

Sharp, Ansel Miree, Charles A. Register, and Paul W. Grimes. “Economics of

social issues”. Plano, TX: Business Publications, 1988.

“The Institute for College Access & Success.” 2014. Quick Facts about

Student Debt. http://bit.ly/1lxjskr.

"The Rising Cost of Not Going to College." Pew Research Centers Social

Demographic Trends Project RSS. N.p., 11 Feb. 2014. Web.

<http://www.pewsocialtrends.org/2014/02/11/the-rising-cost-of-not-

going-to-college/>.

College Board. "Trends in College Pricing." Trends in College Pricing.

College Board, n.d. Web. 25 Apr. 2015.

<http://trends.collegeboard.org/sites/default/files/2014-trends-college-

pricing-final-web.pdf>.

29

“The Higher Education Predicament: An Analysis and Solution” - Tim Tuscher

6. Appendix

Proportions of Expenditures on Higher Education Institutions from Public,

Household, and Other Private Sources, 2010

Country Average Cost

of Tuition Public Household

Other

Private

1 Norway $19,050 96% 3% 1%

2 Finland $16,714 96% 4% 0%

3 Denmark $18,432 95% 5% 0%

4 Iceland $8,728 91% 8% 1%

5 Sweden $19,727 91% 0% 9%

6 Belgium $14,776 90% 5% 6%

7 Austria $15,007 88% 3% 10%

8 Slovenia $8,517 85% 11% 5%

9 France $14,699 82% 10% 8%

10 Ireland $15,911 81% 16% 2%

11 Czech Republic $7,338 79% 9% 12%

12 Spain $13,300 78% 18% 4%

13 Estonia $5,715 75% 18% 7%

14 Netherlands $17,254 72% 15% 13%

15 Poland $6,714 71% 23% 7%

16 Slovak Republic $6,768 70% 12% 18%

17 Mexico $7,872 70% 30% 0%

18 Portugal $9,498 69% 23% 8%

19 Italy $9,501 68% 24% 8%

20 New Zealand $10,418 66% 34% 0%

21 Canada $24,704 57% 20% 24%

22 Israel $10,876 54% 30% 16%

23 Australia $16,020 46% 39% 15%

24 United States $25,576 36% 48% 16%

25 Japan $18,191 34% 52% 14%

26 Korea $11,218 27% 47% 26%

27 United Kingdom $15,206 25% 56% 19%

28 Chile $6,794 22% 70% 8%

Source: The College Board (2014)

30

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

Will Dodd-Frank Prevent the Next Great Recession? Erik Springer

1. Abstract

This paper revisits the purported goals of the Dodd-Frank Wall Street

Reform and Consumer Protection Act of 2010, examining the strengths and

weaknesses of the law and concluding that the law is a framework from

which to build but ultimately weighed down by the complexity of its

piecemeal approach. The current literature will be surveyed and policy

recommendations proposed as guiding principles for successful future reform

and efficient regulation to prevent another financial crisis like the Great

Recession of 2008.

2. Introduction

The 2008 financial crisis was caused in large part by the bad banking

practices of Wall Street and poor oversight by government agencies. The

gruesome details are familiar: repo markets dried up in a liquidity crisis,

bonds including mortgage-backed securities lost value, Bear Stearns

collapsed, Lehman Brothers went bankrupt, government loan agencies Fannie

Mae and Freddie Mac went into receivership, and systemically important

firms like AIG received a massive bailout (Brunnermeier, 2009). Risky

decisions had few consequences as the U.S. federal government doled out

exorbitant sums of cash to stabilize the financial sector to prevent the Great

31

“Will Dodd-Frank Prevent the Next Great Recession?” - Erik Springer

Recession from becoming the Great Depression II. But taxpayers were

angered by having to prop up industries that paid huge bonuses to executives

even after the same individuals drove the world economy into the ground.

While it is clear that intervention was necessary, many argue it should have

come much earlier and some wanted Glass-Steagall reinstated.

In response, Congress passed the Dodd-Frank Wall Street Reform and

Consumer Protection Act of 2010 to prevent a similar scenario from

happening again. Better known as Dodd-Frank, the bill as originally written

left many of the finer details unresolved. Some of the specifics are still being

hashed out by regulatory agencies with Congressional oversight, but much of

the bill is finally in place. Early assessments of the bill were heavily

weighted toward speculation and outright partisanship rather than reasoned

evaluation. Now, more than four years after the passage of Dodd-Frank, it is

important to objectively appraise the law on its actual merits and limitations.

In 2011 Christopher Dodd—for whom the bill was named along with

Barney Frank—wrote an opinion editorial dispelling some myths about his

piece of legislation. Congressman Dodd (2011) responded forcefully (and

accurately) to his critics that it was the “uncertainty inherent in a non-

transparent and reckless financial system” that brought the economy to its

knees in the first place, not excessive regulation. In setting this record

straight, it is important to acknowledge that political demagoguery often

surrounds conversations about reform. As informed and outcome-oriented

32

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

citizens we must set aside ideology and focus instead on what works. Dodd-

Frank is not an intrusive market-stifling force or the answer to all problems.

Regulation is needed, and Dodd-Frank has an important role to play in

resetting the balance of power in the markets to prevent unscrupulous

practices in mortgage-backed securities, secret derivatives trading, and Catch-

22 situations with too-big-to-fail institutions. The legislative solution must

be evaluated in its ability to execute the objective for which Dodd said it was

ostensibly created. He claimed that “repealing it would return us to a time

when nobody knew what the Wall Street gamblers were doing until it was too

late,” and it is hard to argue that repeal would be a better idea than keeping

the law (Dodd, 2011). But this is not quite the right issue. Taxpayers and

voters need to know if the law can not only predict but also prevent the next

Great Recession. That is what this paper will explore.

This study of the law will show how Dodd-Frank establishes a

meaningful framework for reform but ultimately lacks the teeth necessary to

stop another collapse like 2008. To support this thesis I will first survey the

current literature on the topic, assess the strengths and weaknesses of Dodd-

Frank, and then present relevant case studies, policy implications, and

recommendations. Lastly the conclusion will include a summary discussing

how the next great recession can be prevented through straightforward rule

making, streamlined regulating bodies, and aggressive oversight of

systemically important institutions.

33

“Will Dodd-Frank Prevent the Next Great Recession?” - Erik Springer

3. Literature Review

The difficulty in surveying the current literature on Dodd-Frank stems

from the fact that few of the details were worked out when the law was

written in 2010 and many are still being argued over today. New regulatory

bodies have been formed and new practices adopted, but the legislation

remains largely untested. By all measures financial institutions are thriving

today, but it is difficult to attribute the absence of a financial meltdown to a

particular piece of legislation. Even if it were easy, catastrophic systemic

failure can take a while to materialize (there was after all a 79-year gap

between the beginning of the Great Depression and the Great Recession).

Despite the shortcomings listed above, Acharya et al. (2011) did an

effective job of explaining the accomplishments and limitations of Dodd-

Frank in its early days. They found that the law charges depository banks

with building firewalls, demands an orderly resolution to fires, and stops

taxpayers from footing the bill to put out financial fires. But Dodd-Frank

does not go far enough in regulating the shadow banking system, fails to

explain how to put out fires, and is weakened by organizations like Fannie

Mae and Freddie Mac that do not have enough protections in place and could

end up in receivership again. Furthermore, the bill does not strongly

disincentivize private individuals and institutions from putting the system at

risk and depends too heavily on coordination between the new CFPB and

other established regulatory agencies, many of which failed in their duties in

34

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

the lead up to 2008. Regulators deserve blame just like bankers; legislation

will not guarantee that regulators do their job in the future. These concerns

still exist today. But the authors also commented realistically on the

misguided opinion that re-implementing Glass-Steagall would solve all

problems related to modern financial markets and risk. Acharya et al. (2010)

concluded that Dodd-Frank is a meaningful framework for reform with

limitations that can be remedied in time.

Kroszner and Strahan (2011) followed up on earlier work and

examined the importance of writing sound rules that prevent fraud and risk

from being shuffled around to new markets. Their arguments are best left in

their own words: “First, reform should avoid the next round of regulatory

arbitrage in which business moves ‘into the shadows,’ where risks may

slowly accumulate like dead wood ready to ignite the next wildfire. Second,

reform ought to improve market transparency to reduce the uncertainty of

counterparty exposures and interlinkages between major players, thereby

lowering contagion risk” (Kroszner and Strahan, 2011, p. 243). They

expressed concern that Dodd-Frank is ineffective in its regulation of the

housing market and will incent banks to change their practices individually

without actually getting rid of risky practices across the industry. I will look

at their work by focusing on two separate issues: the lack of changes to

regulation in the housing market brought about by Dodd-Frank and the future

efforts that will likely be undertaken in parallel banking to avoid regulation.

35

“Will Dodd-Frank Prevent the Next Great Recession?” - Erik Springer

This last point is crucial. All rules and regulations must be assessed in terms

of their effectiveness at creating transparency. If rules have workarounds and

only encourage regulatory arbitrage, banks will inevitably restructure in order

to maintain opacity, leverage, and excessively risky profit-seeking activities.

By the time Robert Prasch analyzed Dodd-Frank, he came to very

different conclusions than Acharya and his colleagues had about a year prior.

Prasch (2012) argued that the lack of clear and explicit rules in Dodd-Frank

undermines any lasting impact on financial regulation and opined that the bill

was based on flawed premises in the first place. Contrary to Acharya, he

found that Dodd-Frank did not end too-big-to-fail institutions. Greater

consensus exists around the fact that excessive risk-taking still takes place.

Prasch advanced new solutions, notably suggesting the government employ a

similar budgetary process for regulatory agencies to that used by drug

agencies: allow the agencies to keep a percentage of the fines they impose.

This would immediately alter the goals of regulatory agencies and the fervor

with which they imposed major penalties. He also discussed Martin Shubik’s

suggestion that a “stress test” competition be put forth to motivate top

lawyers and economists to identify problems before they occur. Lastly, the

author noted that fraud is prevalent and rarely prosecuted. To his analysis I

would add that implicitly sanctioned fraud (like shadow or parallel banking)

is even worse. The parallel banking system has expanded greatly over the

past three or four decades and remains a significant source of economic risk.

36

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

Nazareth and Rosenberg (2013) continued this train of thought by

exploring the complexity of the U.S. regulatory system and the failure of

Dodd-Frank to improve the inefficiencies of government regulation. The

authors noted that numerous disparate regulatory agencies have grown up

through a piecemeal approach to regulation that has only grown in

complexity over the last 100 years. In this sense, Dodd-Frank missed an

opportunity to reform an archaic and convoluted system of regulation.

Congress’ inability to consolidate regulatory organizations—namely the SEC

and the Commodity Futures Trading Commission but also a number of

others—prohibits nimble regulation and effective communication between

regulators. I will use the example of the regulation of securities, futures, and

swaps as a case study of the problems associated with Dodd-Frank, a bill that

faces an uphill battle both politically and systemically. These difficulties will

be addressed toward the end of the paper as I explain the realities of

governing banks and financial markets with an eye towards suggesting

meaningful reform beyond Dodd-Frank.

Prager (2013) expressed great skepticism of future regulatory success

in exploring CEO compensation structures and their impact on risk-taking.

He outlined how compensation and incentives work to show that chief risk

officers could not restrain CEOs from overly-risky behavior in the lead up to

2008 and success by CEOs was largely based upon luck rather than skill.

Nothing has changed on this front, and CEOs remain incentivized to do more

37

“Will Dodd-Frank Prevent the Next Great Recession?” - Erik Springer

business—even if it means accepting opportunities with dangerous risk

profiles. When one investment bank begins offering innovative (and

reckless) services, others must follow suit to stay competitive. In Prager’s

view, this reality invalidates the effects of broad reforms like Dodd-Frank. It

will have limited value as the same bad incentives remain in the system and

markets are inherently difficult to predict, leaving even the best of bankers

ultimately at the whimsy of luck. However, the author’s claim that history

tells us that we cannot stop another panic is weakened by the fact that we

managed to do so relatively well from the 1930s into the early 2000s. A

more important set of tasks is to diagnose what was sacrificed with the repeal

of Glass-Steagall, what can be improved within Dodd-Frank, and how

regulators can stay one step ahead of developments in parallel banking.

While there are many different ways to deal with systemic risk across

the literature, Yellen (2011) discussed the weakness of monetary policy as an

instrument for systemic risk management because it has its own

macroeconomic goals of price stability and maximum employment.

Additionally, it is a very blunt instrument to handle systemic risk and

regulation is the key. Despite these facts, Yellen admitted that there are

occasions on which it could be appropriate to use monetary policy to stem

risk-taking behavior. Macroprudential policies are the primary driver of

security in the financial system (in accordance with Acharya and Richardson)

but Yellen notes that this is most effective when not working at odds with

38

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

monetary policy. Unfortunately, the economic environment of today is one

such situation in which the goals of macroprudential policies might be at odds

with the goals of monetary policy. For example, the Fed remained skittish

about stemming the flow of easy money for far too long and artificially

propped up the economy with QE3. Yellen’s analysis included policy

implications much like Prasch, but gave a more nuanced perspective: there is

no single method for stemming systemic risk. Yes, the Fed must work with

the CFPB, SEC, and many other agencies to predict and prevent another

Great Recession. And yet, the Fed has separate responsibilities. After

weighing the evidence, the author concluded that dramatic Congressional

action is the best solution for stemming systemic risk. For this reason

monetary policy will not play a major role in policy implications outlined

towards the end of this study.

4. Strengths of Dodd-Frank

Given the complexity of Dodd-Frank it is important to set the stage

for future discussion of the law with some background on the major aspects

and accomplishments of Dodd-Frank. Acharya et al (2011) highlight the

major achievements of the bill, which are reproduced in a slightly altered and

refocused list below:

Identifying and regulating systemic risk under auspices of the

Systemic Risk Council and the U.S. Treasury

39

“Will Dodd-Frank Prevent the Next Great Recession?” - Erik Springer

Recommending an end of too-big-to-fail by redirecting wind-down

costs onto shareholders and creditors

Broadening the responsibility and authority of the Federal Reserve to

include all systemic institutions

Imposing the Volker Rule, a limited version of Glass-Steagall

Increasing regulation and transparency in derivatives markets through

central clearing and oversight

Creating the Consumer Financial Protection Bureau to protect

consumer interests in lending practices and financial services

Each of these topics will be addressed with varying degrees of depth

depending on overall relevance to long-term reform. After considering the

accomplishments of the bill, I will turn to the weaknesses and future policy

improvements to be made.

At its core, Dodd-Frank takes a significant step forward in providing

insight into systemic risk. The creators of the legislation recognized that

banks are not the only organizations that can induce widespread risk into the

economy and therefore gave regulators the authority to deem certain

institutions to be of such consequence. Those who claim that the repeal of

Glass-Steagall was responsible for the 2008 crisis overlook the fact that the

Banking Act of 1933 did not have the authority to oversee many key financial

players today because the structure of our banking system has changes so

drastically in the ensuing eighty years. The new Systemic Risk Council

40

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

provides a private-sector perspective and research on a range of issues,

notably pursuing meaningful solutions for reform of the financial sector and

encouraging efficient government regulation. This additional oversight will

be critical moving forward in predicting risk within the United States and in

holding regulators accountable for identifying structural cracks in our

economy.

Perhaps the most popular element of Dodd-Frank is the creation of the

Consumer Financial Protection Bureau, an agency focused solely on

protecting consumers in the finance sector. Elizabeth Warren realized that

regulators too often saw their job as protecting banks, leading to the predatory

lending practices in home mortgages allowed in the years preceding 2008. As

Paul Krugman (2014) noted, this group is “doing much more to crack down”

than other agencies have in the past.

The Volcker Rule is another trend in the right direction. Acharya and

Richardson (2012) argued that the Volcker Rule could be an effective policy

tool in managing the systemic risk of firms. It has two levers that can be

pulled to stop banks from making risky decisions: capital requirements and

asset holding restrictions. First proposed by Paul Volcker, this component of

Dodd-Frank prevents banks from engaging in volatile proprietary trading and

investing clients’ money in hedge funds. It also limits bank holding

companies’ ability to bail out these kinds of risky investments (Acharya and

Richardson, 2012, p. 3). While partially stripped down from its original

41

“Will Dodd-Frank Prevent the Next Great Recession?” - Erik Springer

version at the behest of special interests, the Volcker Rule is finally going

into effect in 2014. It is already playing a role in separating investment from

commercial banking despite some shortcomings and loopholes.

Other largely unregulated areas of banking in the lead up to 2008

were derivatives markets. Academics almost universally agree that Dodd-

Frank is a monumental leap forward in the transparency of derivative trading.

Bear Stearns’ large derivatives practice made its collapse all the more

surprising because regulators did not understand the derivatives markets or

exposure risk. This occurred in part because of the Commodity Futures

Modernization Act of 2000, a bill that placed undue trust in the markets and

prohibited the regulation of derivatives. Under the new law enacted in 2010,

centralized clearing of many derivatives and transparency of over-the-counter

derivative trading will enable markets to be aware of counterparty risk.

Everyone will have an understanding of personal exposure to the risks taken

on by firms (Acharya et al, 2010, p. 46).

To many taxpayers, the most important (and contentious) purpose of

Dodd-Frank is preventing too-big-to-fail institutions from requiring

government funding. On front the law is a partial success. Regulators can

now designate systemically important financial institutions (SIFIs) and

increase scrutiny and capital requirements for these institutions. Such

companies must now prepare funeral plans and organized liquidation

procedures in case of institutional failure. Dodd-Frank also removes taxpayer

42

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

funding as an option for supporting wind-downs. This pushes the costs—and

responsibility—for poor management onto shareholders and creditors with

additional stipulations that management be fired in the event of disaster. To

encourage good behavior, any remaining costs are to be borne by large

surviving financial firms. In a way, this demands that firms act as their

brothers’ keeper and discourages bad banking practices on behalf of the

collective of firms. Better awareness of what is going on at SIFIs and

accountability to each other will theoretically decrease counterparty risk,

forcing firms to understand the ways that they are interlinked and all share

risk from the collapse of a company like Lehman Brothers. Despite these

steps forward, the law does not achieve the goal of eliminating too big to fail

institutions, a controversial goal but likely one that could address systemic

risk more thoroughly. It is optimistic to believe that firms will self-regulate

and hold each other in check; it just does not play out in reality and this

strategy does not adequately eliminate systemic risk.

5. Weaknesses and Omissions of Dodd-Frank

Dodd-Frank calculates individual institutions’ risk on an independent

basis, raising an important concern about the possibility of unchecked

systemic risk in the future. By its very nature, systemic risk is large-scale and

interconnected. HR 4173 Title I, Subtitle A, Sec. 113 (US Congress 2010)

discusses the stringency standards for assessing risk among systemically

43

“Will Dodd-Frank Prevent the Next Great Recession?” - Erik Springer

important financial institutions (SIFIs) but focuses regulatory practices

entirely on the bank-by-bank risk. There is no mention of the interaction

between a bank and other banks or the “comovement of that firm’s assets

with the aggregate financial sector in a crisis” (Acharya and Robinson 2012,

p. 10). Each firm’s risk is analyzed in a vacuum. Acharya and Robinson

neglect to mention that this is much like counterparty risk, when firms are not

aware of the interconnected nature of their hedging practices. And hedging is

ineffective when comovement of assets is incredibly strong (like it was in

2008). Imagine a scenario where Goldman Sachs buys CDOs from

Wachovia and buys insurance against them from Bear Stearns. Due to

counterparty risk and the comovement of assets, the investment is not

protected at all. Similarly, regulation is ineffective when it considers

financial institutions independent—particularly when they are actually as

interconnected as they have proven to be over the past decade.

Robert Prasch (2012) made a significant observation about the

intertwined nature of the financial system in criticizing Dodd-Frank’s efforts

at ending too-big-to-fail institutions. The current legislative solution

identifies these companies but does nothing to prevent them from existing.

Ultimately it is their very existence that endangers stability. It may sound

harsh, but forcing SIFIs to make funeral plans does not prevent the next

Lehman Brothers collapse from crushing the entire financial system and

tanking the economy. Certainly the government could take over SIFIs in a

44

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

crisis and resurrect them much like it did with General Motors. However

there is no guarantee that such a scenario would play out as profitably as the

GM deal, and the near misses of 2008 only made the largest banks bigger and

more systemically vital as J.P. Morgan Chase bought Washington Mutual,

Wells Fargo purchased Wachovia, and Bank of America acquired Merrill

Lynch. The government nearly begged to get some of these deals done to

protect the economy from further implosion. But the result was terrible for

limiting systemic risk. A slew of academics including Bair, Black, Galbraith,

and Johnson have found that massive banks are inherently hazardous to

economic stability (Prasch, 2012). The Great Recession should have taught

us that banking was too complicated; a comprehensive, modern form of

Glass-Steagall needed to be implemented in the wake of the Great Recession.

Instead the government turned to the largest financial institutions to save their

peers and in the process the government created even more bloated

systemically important companies.

Even the Volcker rule has shortcomings that damage its effectiveness.

In plain terms, the Volcker rule was emasculated by special interests. For

starters, it does not encompass all institutions. The concerns of many banks

were voiced effectively and as a result a number of institutions will be able to

dodge the policy. Loopholes crippled a policy that should have been enacted

as a blanket ban proprietary trading by bank holding companies. As it stands,

even the definition of “proprietary” is nebulous, endangering the Volcker

45

“Will Dodd-Frank Prevent the Next Great Recession?” - Erik Springer

Rule’s potential relevancy in the future. Banks may very well manage to

adapt to circumvent the policy by employing new techniques for leveraging

their assets. Kroszner and Strahan worry that selective regulatory arbitrage

will incentivize institutions to move risk to new markets and institutions,

which will only serve to “increase interlinkages and market opaqueness”

(2011, p. 244). This is an ominous thought and one with significant meaning.

Dodd-Frank may have redefined the rules of the game, but it did not prevent

banks from inventing their own entirely new games without rules.

Future regulatory success depends upon the oversight of financial

instruments that have not yet been created in the parallel (or shadow) banking

system. Federal deposit insurance, required reserve ratios, and capital

requirements are nonexistent in parallel banking. Since Dodd-Frank focuses

on censuring only the specific bad behaviors of the past, banks will adapt and

devise the next version of derivatives or credit default swaps to avoid the

current rules. This will hopefully be mitigated by the law’s ability to

designate SIFIs and increase regulation for these companies, but legislating

symptoms is a weak alternative for addressing systemic disease. It could take

ten or more years to understand if regulators are nimble enough under the

current laws to counteract new financial instruments. One thing is certain:

Dodd-Frank did not end the risks involved in the parallel banking system.

The parallel banking system remains completely interconnected with

traditional banking and risk is widespread.

46

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

6. Policy Recommendations

There are inherent dangers in assuming that policy-makers can create

fail-safe structures to avert economic downturns. To that end I will provide

some words of caution through the narrative and research of Jonas Prager

before outlining some proposals that may help prevent the next Great

Recession. Prager (2013) charted the path of Lehman Brothers and Goldman

Sachs through the course of the financial crisis to illustrate the similarities of

the firms. He found that risk management and boards of directors had no role

in whether firms weathered the storm or collapsed; misaligned incentives also

did not play the central role that some economists have envisioned. Luck

determined outcomes. Prager demonstrated that financial markets will

always be a bit like gambling. When the gamblers get too much money to

play with, somebody will inevitably lose big. Regulators can certainly

mitigate a recurrence of 2008, but prevention may be impossible.

Even strong banking legislation like Glass-Steagall has never been

entirely effective. While the Banking Act of 1933—Glass-Steagall as it came

to be known—did create the FDIC to insure deposits and separated

commercial banking from investment banking, it was never fail-safe

(Acharya et al, 2011). The regulation was sound for a time, but development

in financial systems made the law irrelevant within a few decades. Fragile

shadow (or parallel) banking grew up in the 1970s and 1980s, bringing with it

systemic risk that Glass-Steagall was incapable of addressing. Even the

47

“Will Dodd-Frank Prevent the Next Great Recession?” - Erik Springer

Volcker Rule, a modern version of the law, is insufficient due to watering

down and limited jurisdiction. To improve Dodd-Frank, the first change that

should be made is a blanket rewrite of the Volcker Rule to allow it unlimited

jurisdiction with zero loopholes. Banking interests crippled the policy’s

effectiveness by 2014 when the final language was solidified. In response,

Congress should amend Section 619 of Dodd-Frank by removing all

qualifiers and loopholes, stripping the Volcker Rule down to the following:

A banking entity shall not

(A) engage in proprietary trading; or

(B) acquire or retain any equity, partnership, other ownership interest in

or sponsor a hedge fund or private equity fund.

This is what Paul Volcker intended and this is the simplest and most

meaningful way to protect consumers’ assets held at banks.

The current complexity of the Volcker Rule highlights a major issue

with the larger financial system and rulemaking. Special interests obstruct

meaningful lawmaking and legislators’ piecemeal approach to regulation only

complicates oversight. Consider Dodd-Frank’s structure for a moment: the

law “implicates 25 regulators and creates 2 new ones” over the course of 849

pages of legislation and 398 open-ended rulemaking requirements (Nazareth

and Rosenberg, 2013). Regulation is not lean or coordinated. Overlapping

jurisdiction creates overregulation and underregulation within different parts

of the financial system. Sometimes both occur simultaneously, leading to

inconsistent regulation that drives undue costs onto the private sector. For

example, the regulation of securities, futures and swaps is split between the

48

St. Olaf College’s Omicron Delta Epsilon Journal of Economic Research

Securities and Exchange Commission (SEC) and the Commodity Futures

Trading Commission (CFTC) because of an archaic remnant of legislation

written in the 1970s that started the CFTC. Nazareth and Rosenberg (2013)

thoroughly explained the disorganized history of the CFTC, but all that is

worth noting here is that Dodd-Frank makes the problem worse through

provisions that impact both the SEC and the CFTC in interrelated ways. Dual