Cost of Capital - CAMPUT€¦ · BOOTH CAMPUT 2013 Cost of Capital . Professor Laurence Booth . CIT...

30

BOOTH CAMPUT 2013 Cost of Capital Professor Laurence Booth CIT Chair in Structured Finance Rotman School of Management University of Toronto

Transcript of Cost of Capital - CAMPUT€¦ · BOOTH CAMPUT 2013 Cost of Capital . Professor Laurence Booth . CIT...

BOOTH CAMPUT 2013

Cost of Capital

Professor Laurence Booth CIT Chair in Structured Finance Rotman School of Management

University of Toronto

BOOTH CAMPUT 2013

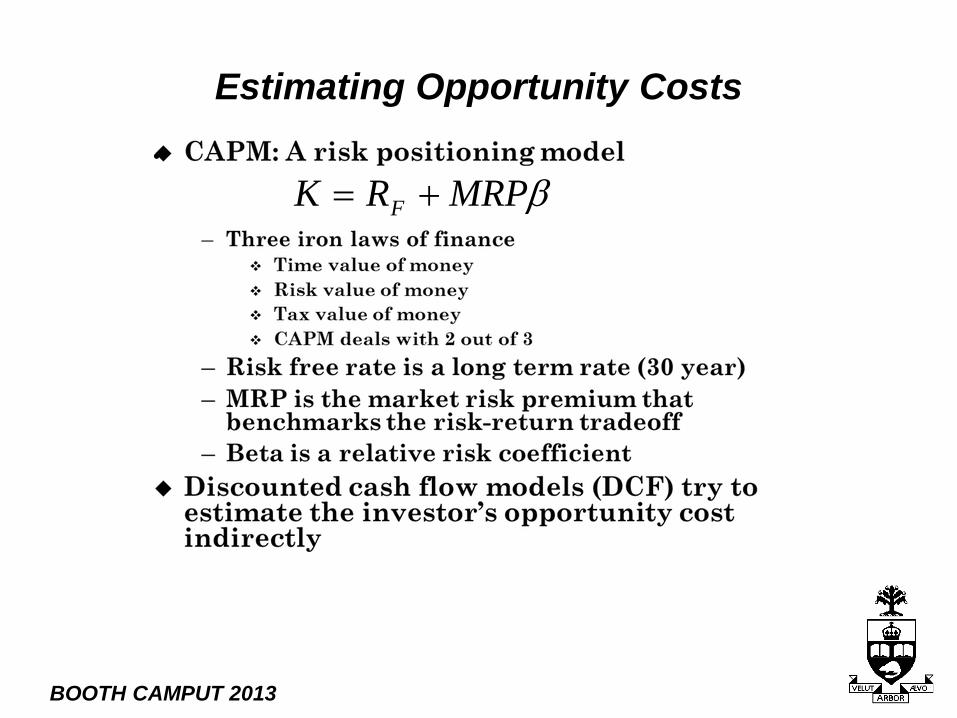

Estimating Opportunity Costs •

βMRPRK F +=

BOOTH CAMPUT 2013

Graham and Harvey (JFE 2001) Survey

BOOTH CAMPUT 2013

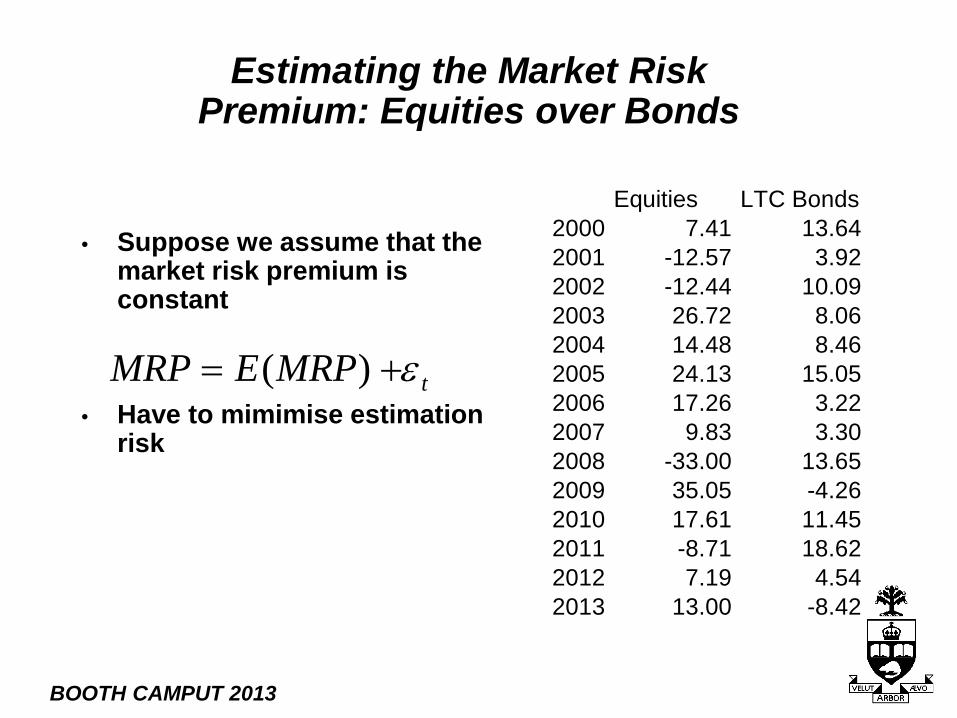

Estimating the Market Risk Premium: Equities over Bonds

• Suppose we assume that the market risk premium is constant

• Have to mimimise estimation risk

tMRPEMRP ε+= )(

Equities LTC Bonds2000 7.41 13.642001 -12.57 3.922002 -12.44 10.092003 26.72 8.062004 14.48 8.462005 24.13 15.052006 17.26 3.222007 9.83 3.302008 -33.00 13.652009 35.05 -4.262010 17.61 11.452011 -8.71 18.622012 7.19 4.542013 13.00 -8.42

BOOTH CAMPUT 2013

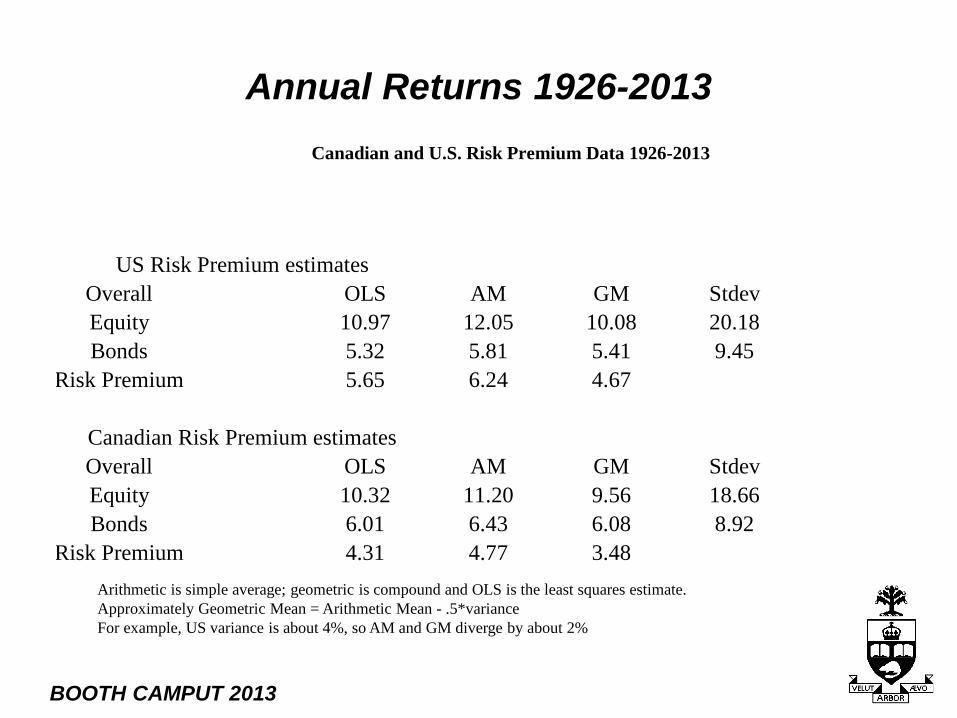

Annual Returns 1926-2013

Arithmetic is simple average; geometric is compound and OLS is the least squares estimate. Approximately Geometric Mean = Arithmetic Mean - .5*variance For example, US variance is about 4%, so AM and GM diverge by about 2%

Canadian and U.S. Risk Premium Data 1926-2013

US Risk Premium estimatesOverall OLS AM GM StdevEquity 10.97 12.05 10.08 20.18Bonds 5.32 5.81 5.41 9.45

Risk Premium 5.65 6.24 4.67

Canadian Risk Premium estimatesOverall OLS AM GM StdevEquity 10.32 11.20 9.56 18.66Bonds 6.01 6.43 6.08 8.92

Risk Premium 4.31 4.77 3.48

BOOTH CAMPUT 2013

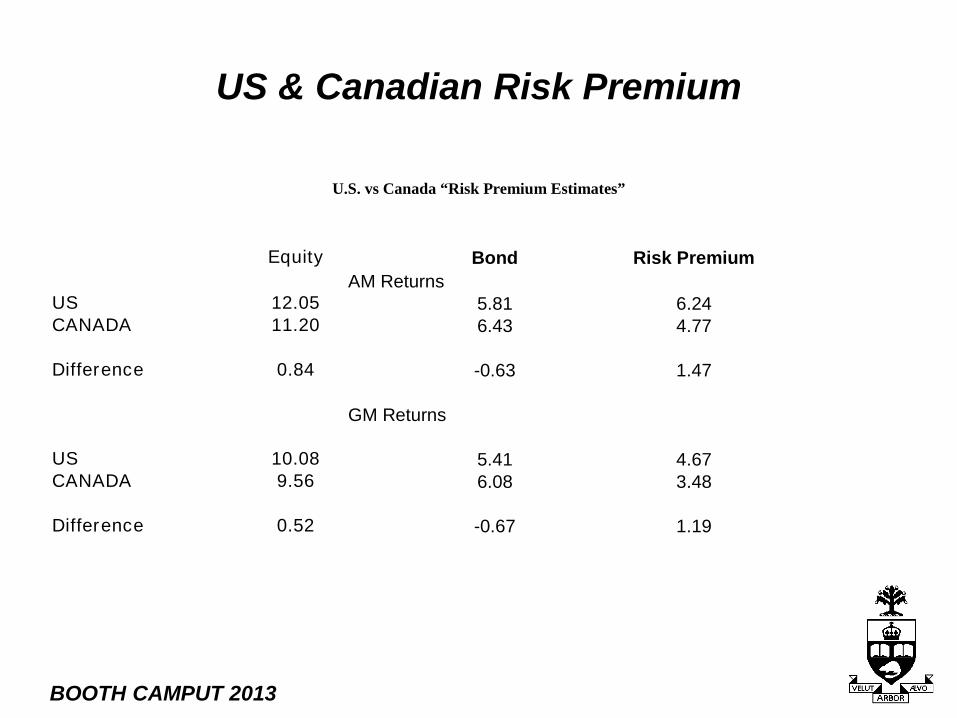

US & Canadian Risk Premium

U.S. vs Canada “Risk Premium Estimates”

Equity Bond Risk PremiumAM Returns

US 12.05 5.81 6.24CANADA 11.20 6.43 4.77

Difference 0.84 -0.63 1.47

GM Returns

US 10.08 5.41 4.67CANADA 9.56 6.08 3.48

Difference 0.52 -0.67 1.19

BOOTH CAMPUT 2013

Currency Composition of Major Country Reserve Fund Holdings

http://www.imf.org/external/np/sta/cofer/eng/index.htm

BOOTH CAMPUT 2013

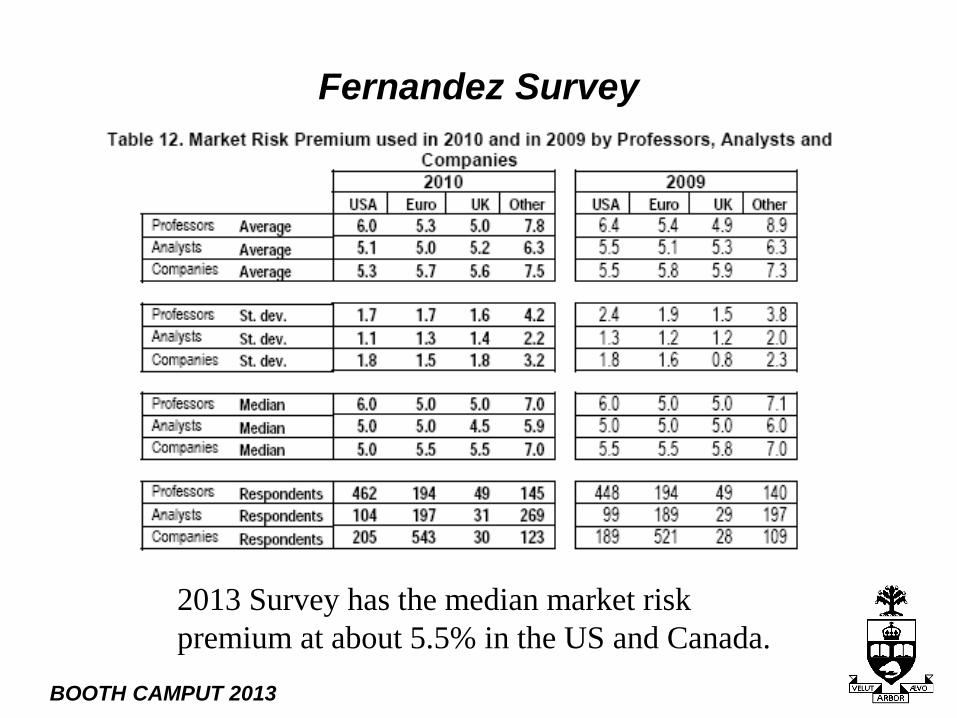

Fernandez Survey

2013 Survey has the median market risk premium at about 5.5% in the US and Canada.

BOOTH CAMPUT 2013

Utility Business Risk

• Short run • Ability to earn the allowed ROE • Return on capital

• Long run

• Stranded asset risk • Return of capital • “I want my money back!” (Greece and

PIIGS)

BOOTH CAMPUT 2013

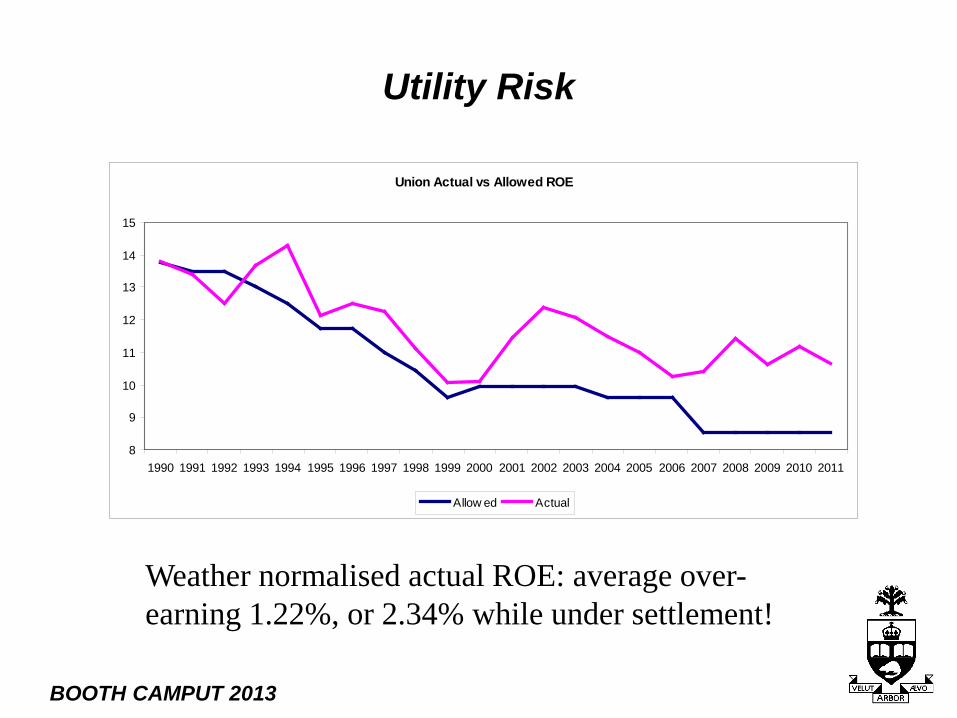

Utility Risk

Union Actual vs Allowed ROE

8

9

10

11

12

13

14

15

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Allow ed Actual

Weather normalised actual ROE: average over-earning 1.22%, or 2.34% while under settlement!

BOOTH CAMPUT 2013

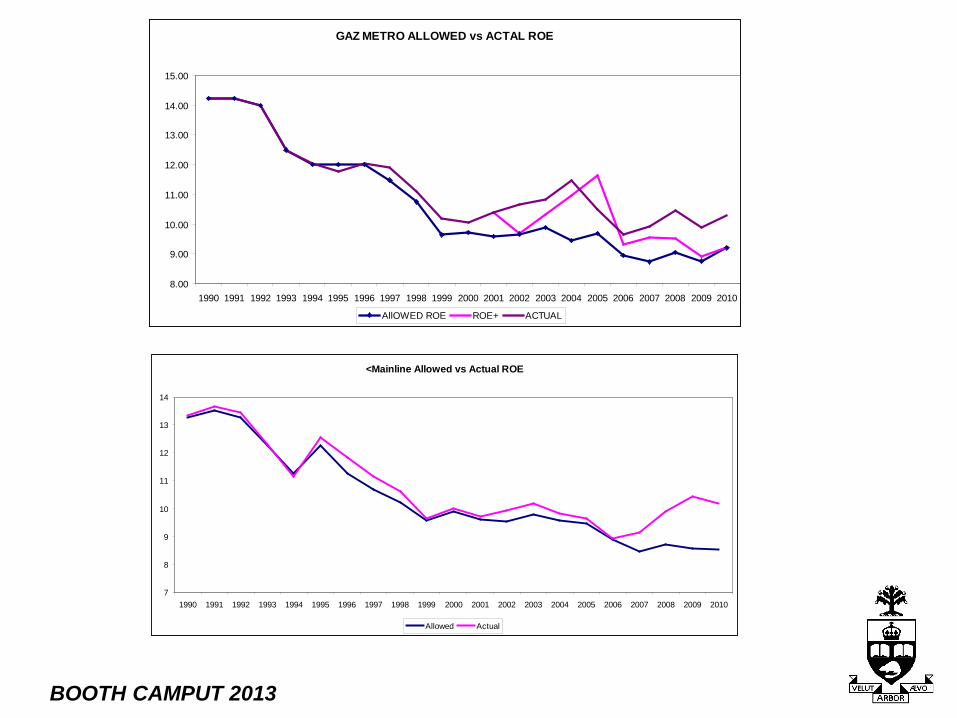

GAZ METRO ALLOWED vs ACTAL ROE

8.00

9.00

10.00

11.00

12.00

13.00

14.00

15.00

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

AllOWED ROE ROE+ ACTUAL

<Mainline Allowed vs Actual ROE

7

8

9

10

11

12

13

14

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Allowed Actual

BOOTH CAMPUT 2013

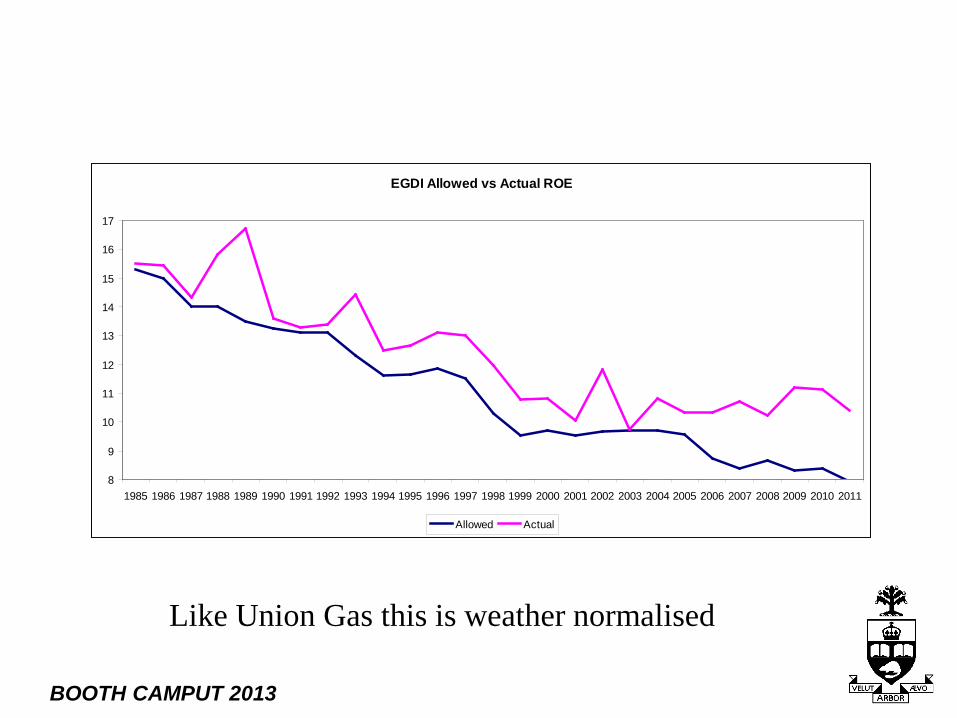

EGDI Allowed vs Actual ROE

8

9

10

11

12

13

14

15

16

17

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Allowed Actual

Like Union Gas this is weather normalised

BOOTH CAMPUT 2013

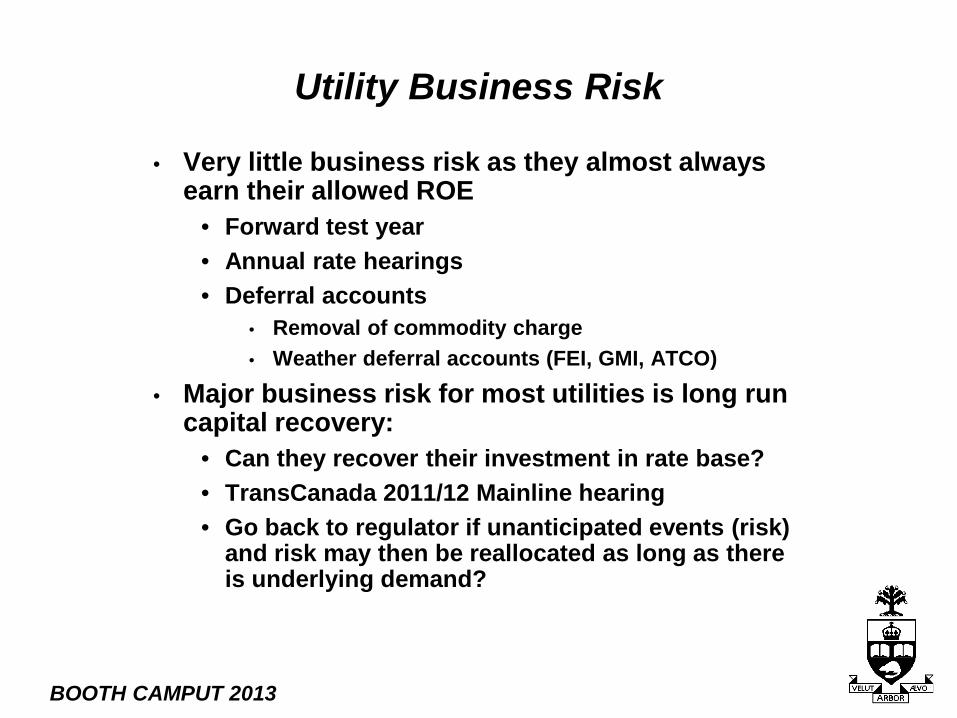

Utility Business Risk

• Very little business risk as they almost always earn their allowed ROE

• Forward test year • Annual rate hearings • Deferral accounts

• Removal of commodity charge • Weather deferral accounts (FEI, GMI, ATCO)

• Major business risk for most utilities is long run capital recovery:

• Can they recover their investment in rate base? • TransCanada 2011/12 Mainline hearing • Go back to regulator if unanticipated events (risk)

and risk may then be reallocated as long as there is underlying demand?

BOOTH CAMPUT 2013

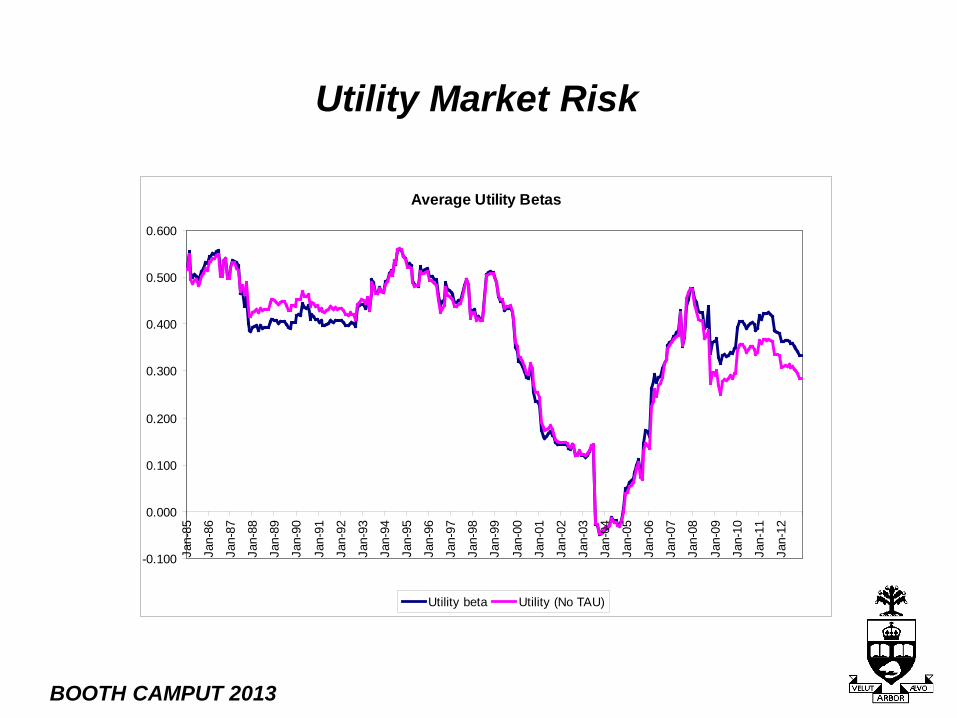

Utility Market Risk

Average Utility Betas

-0.100

0.000

0.100

0.200

0.300

0.400

0.500

0.600

Jan-

85

Jan-

86

Jan-

87

Jan-

88

Jan-

89

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Utility beta Utility (No TAU)

BOOTH CAMPUT 2013

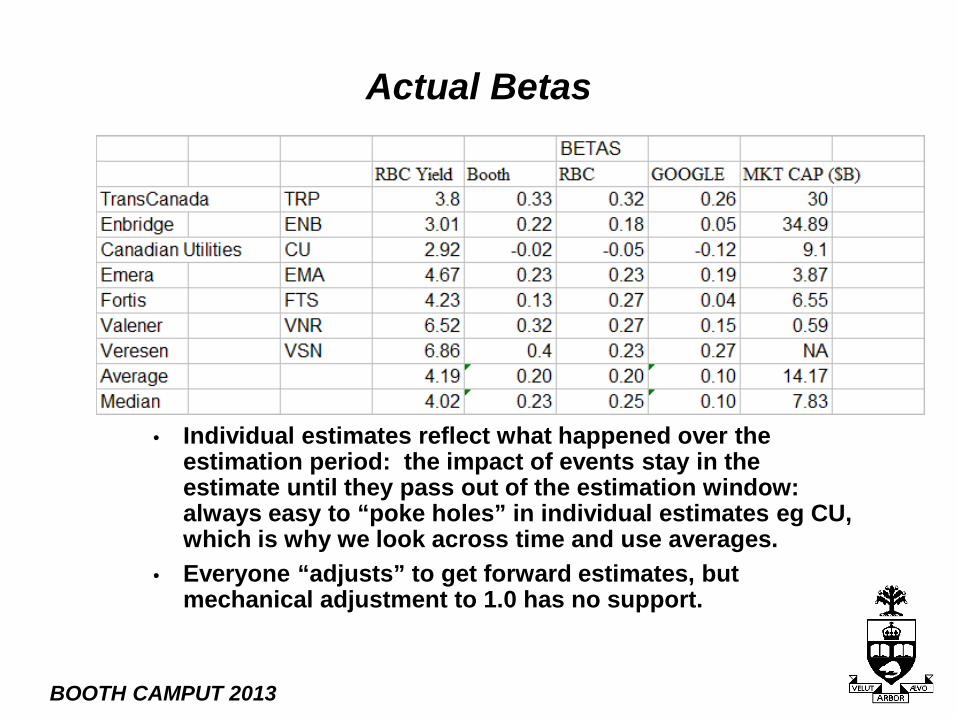

Actual Betas

• Individual estimates reflect what happened over the estimation period: the impact of events stay in the estimate until they pass out of the estimation window: always easy to “poke holes” in individual estimates eg CU, which is why we look across time and use averages.

• Everyone “adjusts” to get forward estimates, but mechanical adjustment to 1.0 has no support.

BOOTH CAMPUT 2013

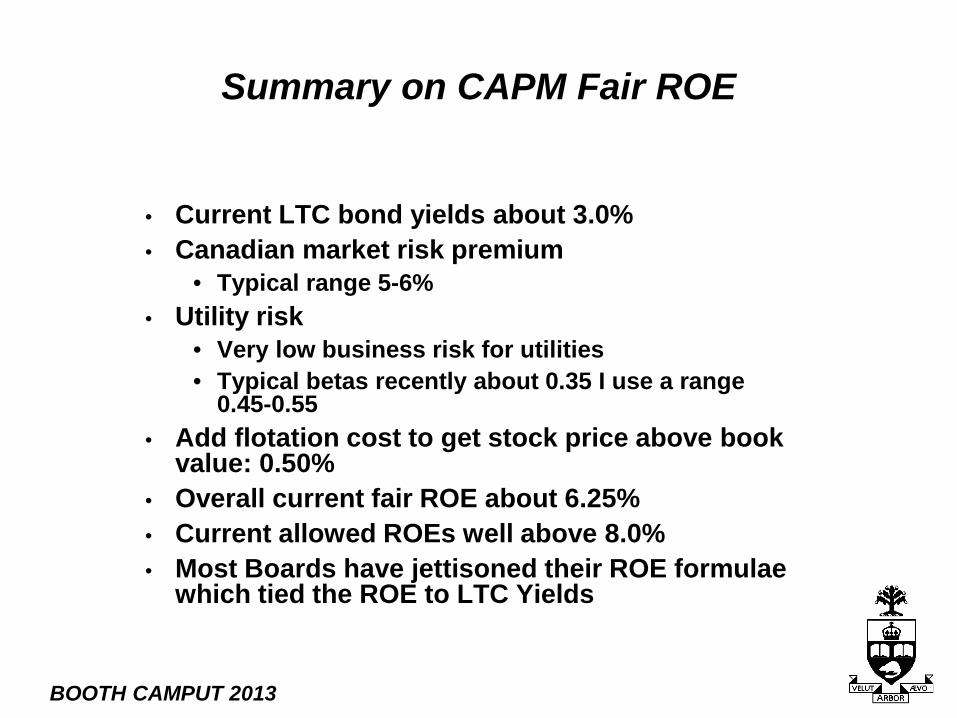

Summary on CAPM Fair ROE

• Current LTC bond yields about 3.0% • Canadian market risk premium

• Typical range 5-6% • Utility risk

• Very low business risk for utilities • Typical betas recently about 0.35 I use a range

0.45-0.55 • Add flotation cost to get stock price above book

value: 0.50% • Overall current fair ROE about 6.25% • Current allowed ROEs well above 8.0% • Most Boards have jettisoned their ROE formulae

which tied the ROE to LTC Yields

BOOTH CAMPUT 2013

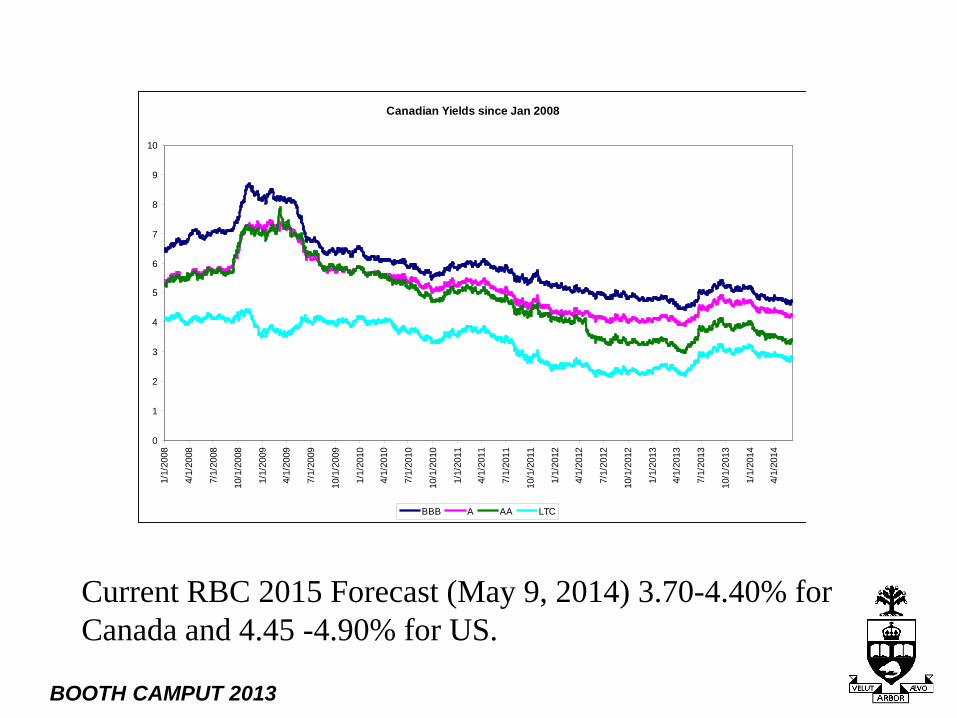

Current RBC 2015 Forecast (May 9, 2014) 3.70-4.40% for Canada and 4.45 -4.90% for US.

Canadian Yields since Jan 2008

0

1

2

3

4

5

6

7

8

9

10

1/1/

2008

4/1/

2008

7/1/

2008

10/1

/200

8

1/1/

2009

4/1/

2009

7/1/

2009

10/1

/200

9

1/1/

2010

4/1/

2010

7/1/

2010

10/1

/201

0

1/1/

2011

4/1/

2011

7/1/

2011

10/1

/201

1

1/1/

2012

4/1/

2012

7/1/

2012

10/1

/201

2

1/1/

2013

4/1/

2013

7/1/

2013

10/1

/201

3

1/1/

2014

4/1/

2014

BBB A AA LTC

BOOTH CAMPUT 2013

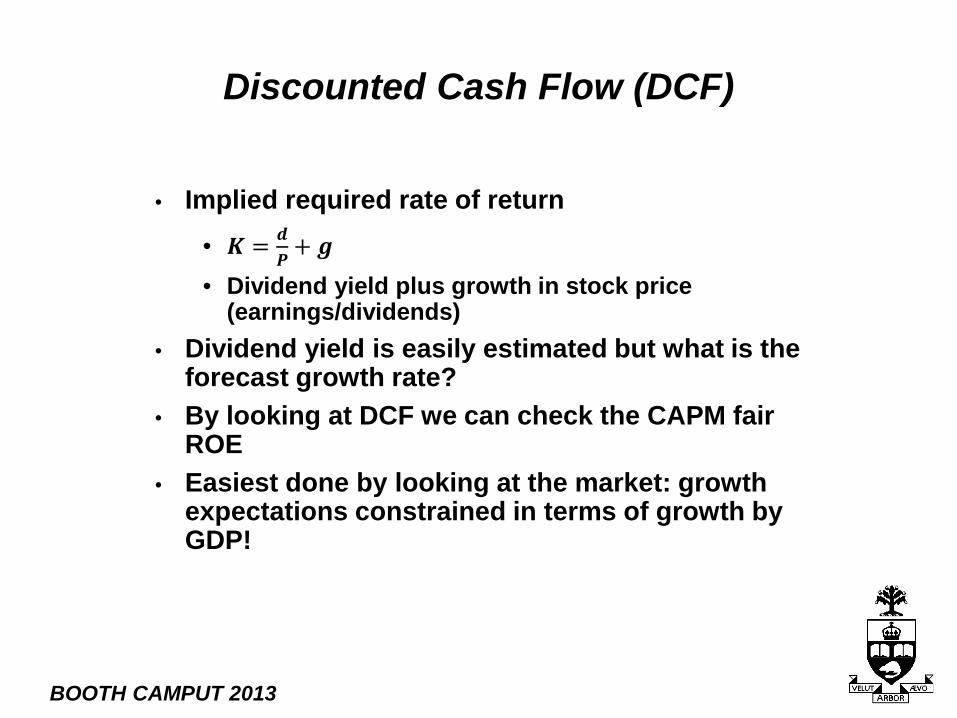

Discounted Cash Flow (DCF)

• Implied required rate of return • 𝑲 = 𝒅

𝑷+ 𝒈

• Dividend yield plus growth in stock price (earnings/dividends)

• Dividend yield is easily estimated but what is the forecast growth rate?

• By looking at DCF we can check the CAPM fair ROE

• Easiest done by looking at the market: growth expectations constrained in terms of growth by GDP!

BOOTH CAMPUT 2013

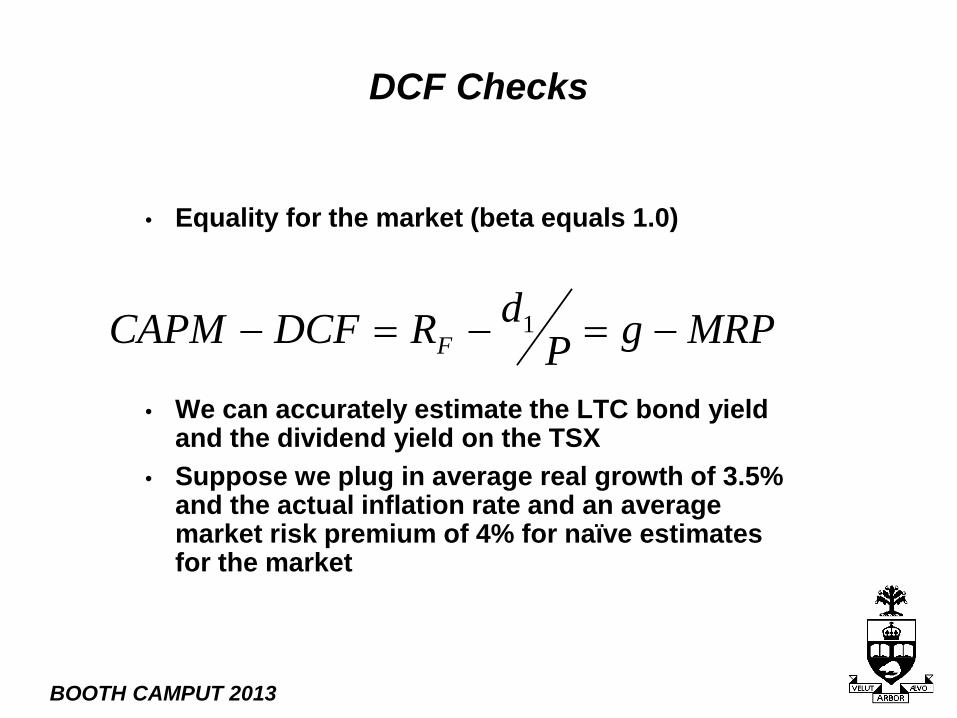

DCF Checks

• Equality for the market (beta equals 1.0)

• We can accurately estimate the LTC bond yield and the dividend yield on the TSX

• Suppose we plug in average real growth of 3.5% and the actual inflation rate and an average market risk premium of 4% for naïve estimates for the market

MRPgPdRDCFCAPM F −=−=− 1

BOOTH CAMPUT 2013

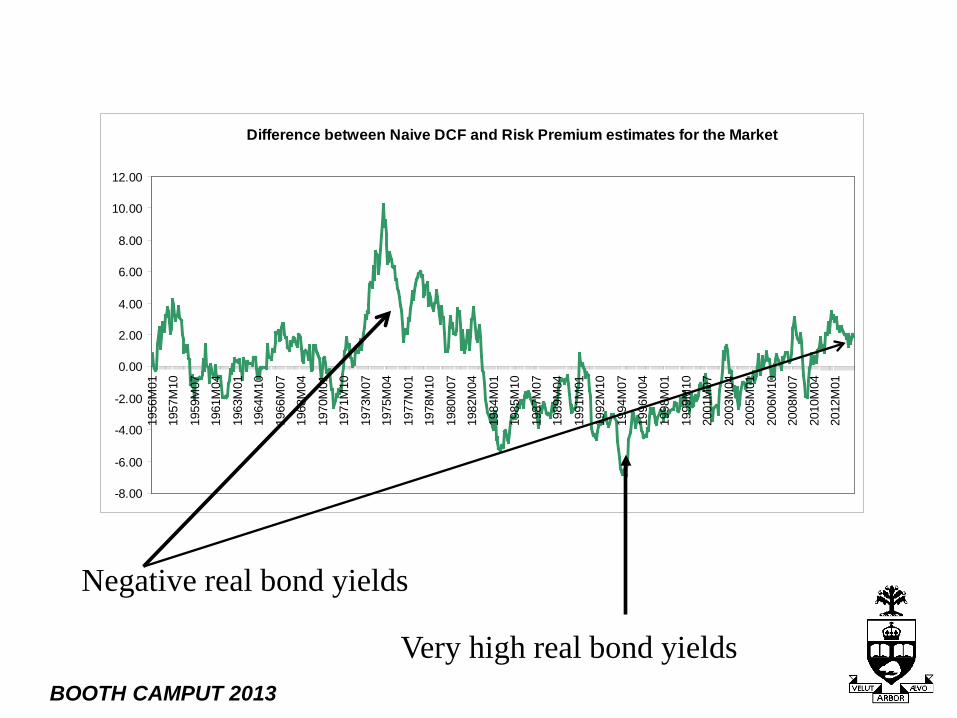

Negative real bond yields

Very high real bond yields

Difference between Naive DCF and Risk Premium estimates for the Market

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

1956

M01

1957

M10

1959

M07

1961

M04

1963

M01

1964

M10

1966

M07

1968

M04

1970

M01

1971

M10

1973

M07

1975

M04

1977

M01

1978

M10

1980

M07

1982

M04

1984

M01

1985

M10

1987

M07

1989

M04

1991

M01

1992

M10

1994

M07

1996

M04

1998

M01

1999

M10

2001

M07

2003

M04

2005

M01

2006

M10

2008

M07

2010

M04

2012

M01

BOOTH CAMPUT 2013

Insights

• DCF estimates exceed risk premium estimates during high inflation periods or low real bond yield periods

• CAPM estimates exceed DCF estimates during high real bond yield periods

• Current LTC yields of 3.0% have increased by 0.50% over the past year, but with expected inflation of 2% are not a good investment for a taxable investor: built in loss of money.

• CAPM may under-estimate fair ROE if you use current forecast LTC yields, but not as bad as a year ago

BOOTH CAMPUT 2013

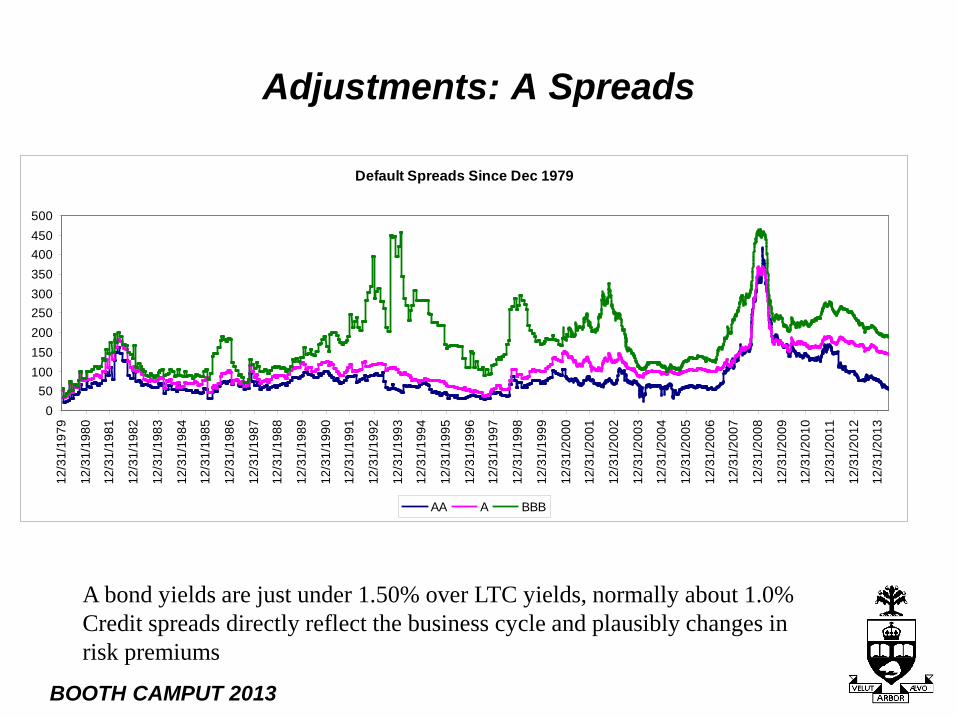

Adjustments: A Spreads

A bond yields are just under 1.50% over LTC yields, normally about 1.0% Credit spreads directly reflect the business cycle and plausibly changes in risk premiums

Default Spreads Since Dec 1979

050

100150200250300350400450500

12/3

1/19

79

12/3

1/19

80

12/3

1/19

81

12/3

1/19

82

12/3

1/19

83

12/3

1/19

84

12/3

1/19

85

12/3

1/19

86

12/3

1/19

87

12/3

1/19

88

12/3

1/19

89

12/3

1/19

90

12/3

1/19

91

12/3

1/19

92

12/3

1/19

93

12/3

1/19

94

12/3

1/19

95

12/3

1/19

96

12/3

1/19

97

12/3

1/19

98

12/3

1/19

99

12/3

1/20

00

12/3

1/20

01

12/3

1/20

02

12/3

1/20

03

12/3

1/20

04

12/3

1/20

05

12/3

1/20

06

12/3

1/20

07

12/3

1/20

08

12/3

1/20

09

12/3

1/20

10

12/3

1/20

11

12/3

1/20

12

12/3

1/20

13

AA A BBB

BOOTH CAMPUT 2013

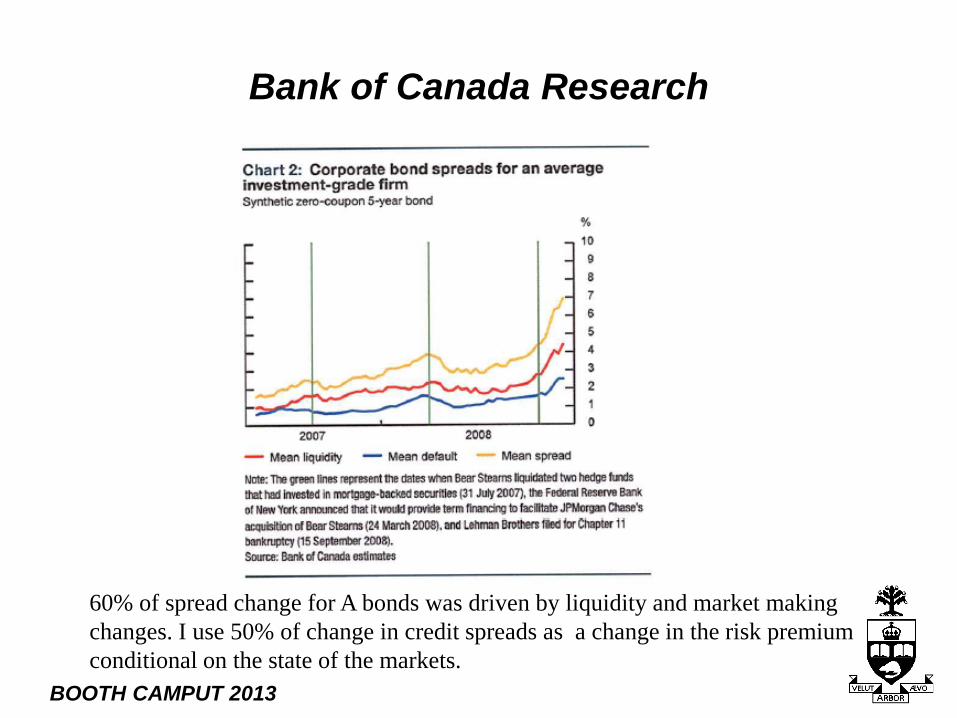

Bank of Canada Research

60% of spread change for A bonds was driven by liquidity and market making changes. I use 50% of change in credit spreads as a change in the risk premium conditional on the state of the markets.

BOOTH CAMPUT 2013

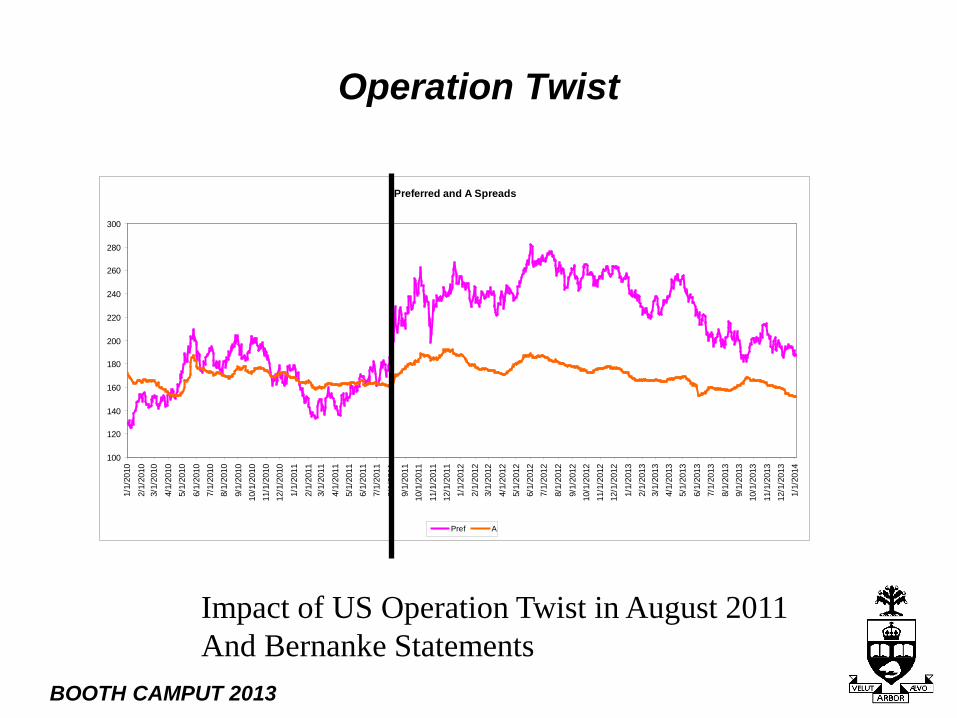

Impact of US Operation Twist in August 2011 And Bernanke Statements

Operation Twist

Preferred and A Spreads

100

120

140

160

180

200

220

240

260

280

300

1/1/

2010

2/1/

2010

3/1/

2010

4/1/

2010

5/1/

2010

6/1/

2010

7/1/

2010

8/1/

2010

9/1/

2010

10/1

/201

011

/1/2

010

12/1

/201

0

1/1/

2011

2/1/

2011

3/1/

2011

4/1/

2011

5/1/

2011

6/1/

2011

7/1/

2011

8/1/

2011

9/1/

2011

10/1

/201

1

11/1

/201

112

/1/2

011

1/1/

2012

2/1/

2012

3/1/

2012

4/1/

2012

5/1/

2012

6/1/

2012

7/1/

2012

8/1/

2012

9/1/

2012

10/1

/201

211

/1/2

012

12/1

/201

2

1/1/

2013

2/1/

2013

3/1/

2013

4/1/

2013

5/1/

2013

6/1/

2013

7/1/

2013

8/1/

2013

9/1/

2013

10/1

/201

3

11/1

/201

312

/1/2

013

1/1/

2014

Pref A

BOOTH CAMPUT 2013

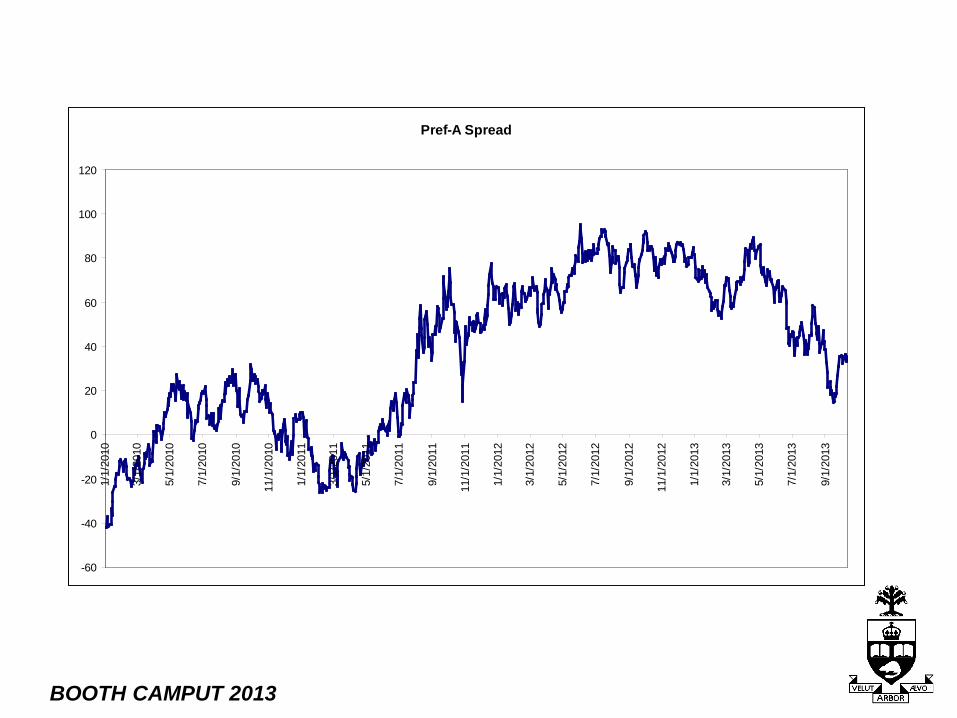

Pref-A Spread

-60

-40

-20

0

20

40

60

80

100

120

1/1/

2010

3/1/

2010

5/1/

2010

7/1/

2010

9/1/

2010

11/1

/201

0

1/1/

2011

3/1/

2011

5/1/

2011

7/1/

2011

9/1/

2011

11/1

/201

1

1/1/

2012

3/1/

2012

5/1/

2012

7/1/

2012

9/1/

2012

11/1

/201

2

1/1/

2013

3/1/

2013

5/1/

2013

7/1/

2013

9/1/

2013

BOOTH CAMPUT 2013

Current CAPM Adjustments

• “A” Spread Adjustment

• Used by OEB and Regie • Add 50% of the change in the A spread to adjust

the utility risk premium • Operation Twist

• Minimum LTC forecast yield of 4.0% • Until recently added 0.80% to very low forecast

LTC yields. Explicitly accepted by BCUC and Newfoundland PUB.

• Overall I currently recommend about 7.50% as a fair ROE

BOOTH CAMPUT 2013

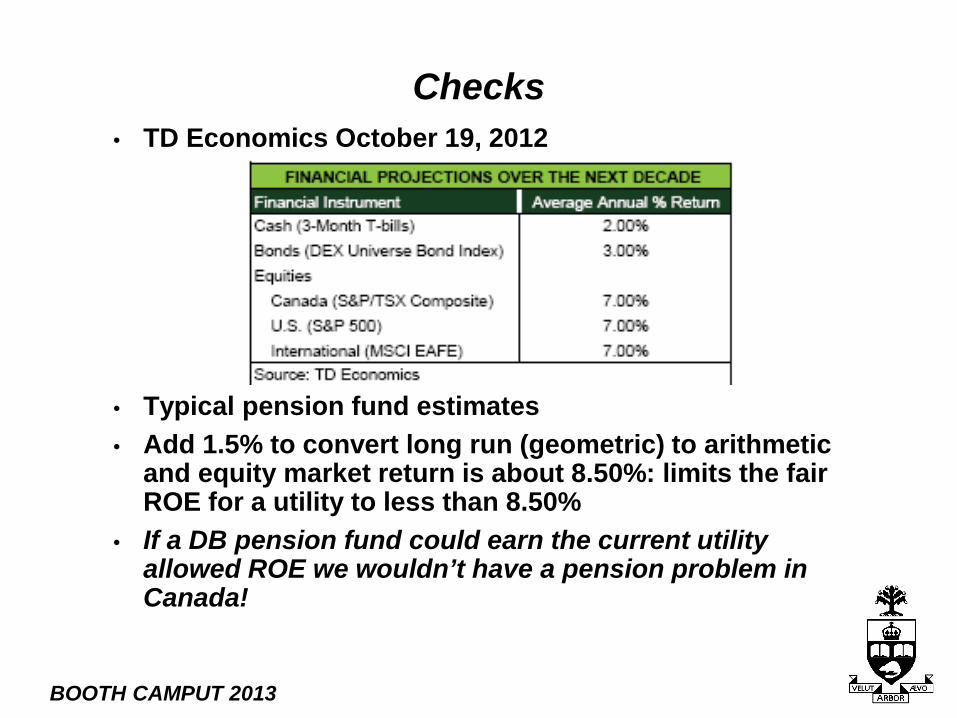

Checks • TD Economics October 19, 2012

• Typical pension fund estimates • Add 1.5% to convert long run (geometric) to arithmetic

and equity market return is about 8.50%: limits the fair ROE for a utility to less than 8.50%

• If a DB pension fund could earn the current utility allowed ROE we wouldn’t have a pension problem in Canada!

BOOTH CAMPUT 2013

“The most the owners in aggregate can earn between now and judgment day is what their businesses in aggregate earn.(italics in original) True by buying and selling that is clever or lucky, investor A may take more than his share of the pie at the expense of investor B. And yes, all investors feel richer when stocks soar. But an owner can exit only by having someone take his place. If one investor sells high, another must buy high. For owners as a whole, there is simply no magic - no shower of money from outer space – that will enable them to extract wealth from their companies beyond that created by the companies themselves.” Warren Buffet

BOOTH CAMPUT 2013

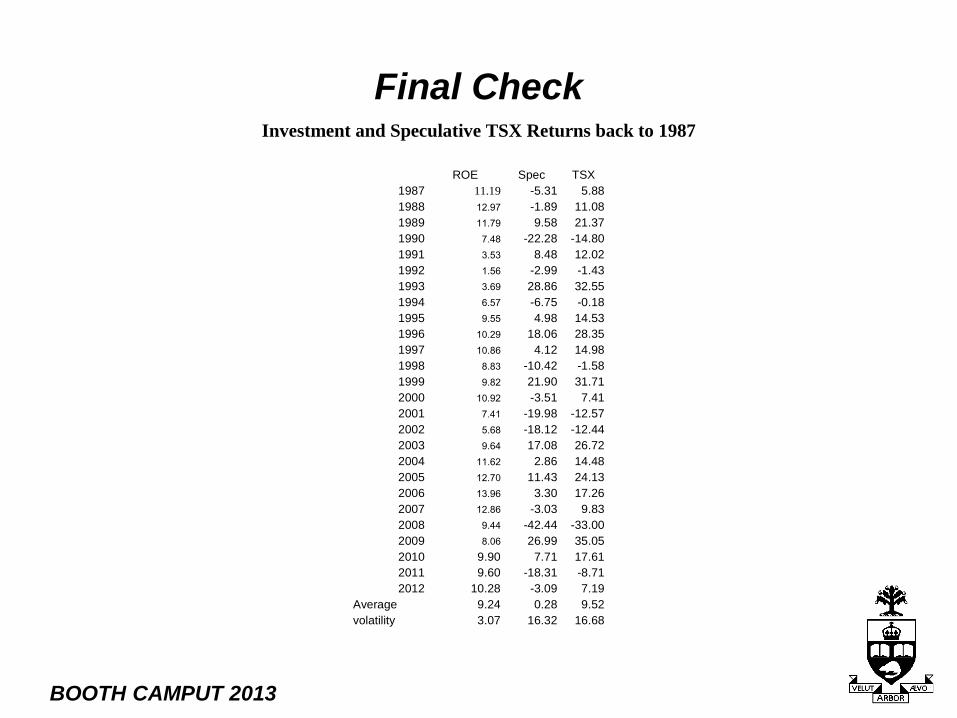

Final Check Investment and Speculative TSX Returns back to 1987

ROE Spec TSX1987 11.19 -5.31 5.881988 12.97 -1.89 11.081989 11.79 9.58 21.371990 7.48 -22.28 -14.801991 3.53 8.48 12.021992 1.56 -2.99 -1.431993 3.69 28.86 32.551994 6.57 -6.75 -0.181995 9.55 4.98 14.531996 10.29 18.06 28.351997 10.86 4.12 14.981998 8.83 -10.42 -1.581999 9.82 21.90 31.712000 10.92 -3.51 7.412001 7.41 -19.98 -12.572002 5.68 -18.12 -12.442003 9.64 17.08 26.722004 11.62 2.86 14.482005 12.70 11.43 24.132006 13.96 3.30 17.262007 12.86 -3.03 9.832008 9.44 -42.44 -33.002009 8.06 26.99 35.052010 9.90 7.71 17.612011 9.60 -18.31 -8.712012 10.28 -3.09 7.19

Average 9.24 0.28 9.52volatility 3.07 16.32 16.68

BOOTH CAMPUT 2013

Conclusions • Can not mechanically do much in finance

• Markets constantly changing • I have been accused of using judgment!

• Three iron laws of finance • Time value of money • Risk value of money • Tax value of money

• Business cycle effects on spreads and betas • Impact of US government in bond market

• Bond market currently not a market “opportunity cost” • Long rates being set by the global policy maker (RBC) • Stock market as a whole to earn 9-10%.