Chapter 6 Efficient Diversification - Faculty Web Server -...

10

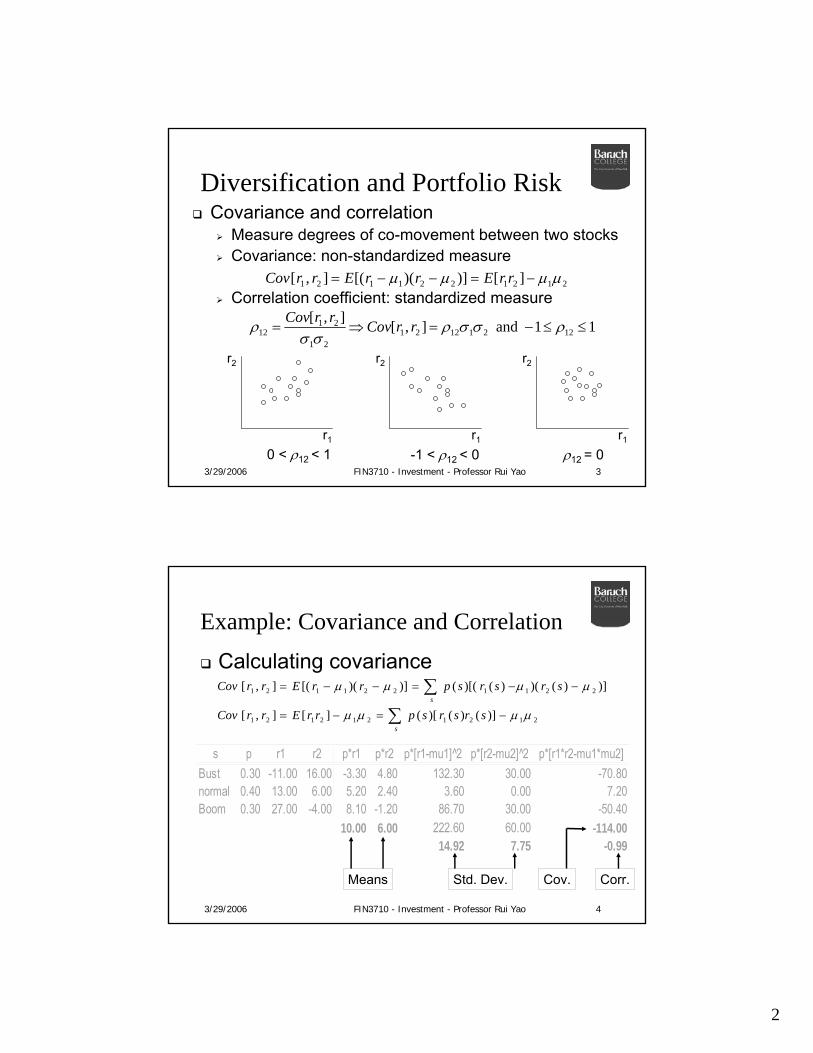

1 Chapter 6 Efficient Diversification 3/29/2006 FIN3710 - Investment - Professor Rui Yao 2 Diversification and Portfolio Risk Don’t put all your eggs in one basket Effect of portfolio diversification # of securities in the portfolio σ 5 10 15 20 Diversifiable risk, non-systematic risk, firm-specific risk, idiosyncratic risk Non-diversifiable risk, systematic risk, market risk, covariance risk

Transcript of Chapter 6 Efficient Diversification - Faculty Web Server -...

1

Chapter 6Efficient Diversification

3/29/2006 FIN3710 - Investment - Professor Rui Yao 2

Diversification and Portfolio RiskDon’t put all your eggs in one basketEffect of portfolio diversification

# of securities in the portfolio

σ

5 10 15 20

Diversifiable risk, non-systematic risk, firm-specific risk, idiosyncratic risk

Non-diversifiable risk, systematic risk, market risk, covariance risk

2

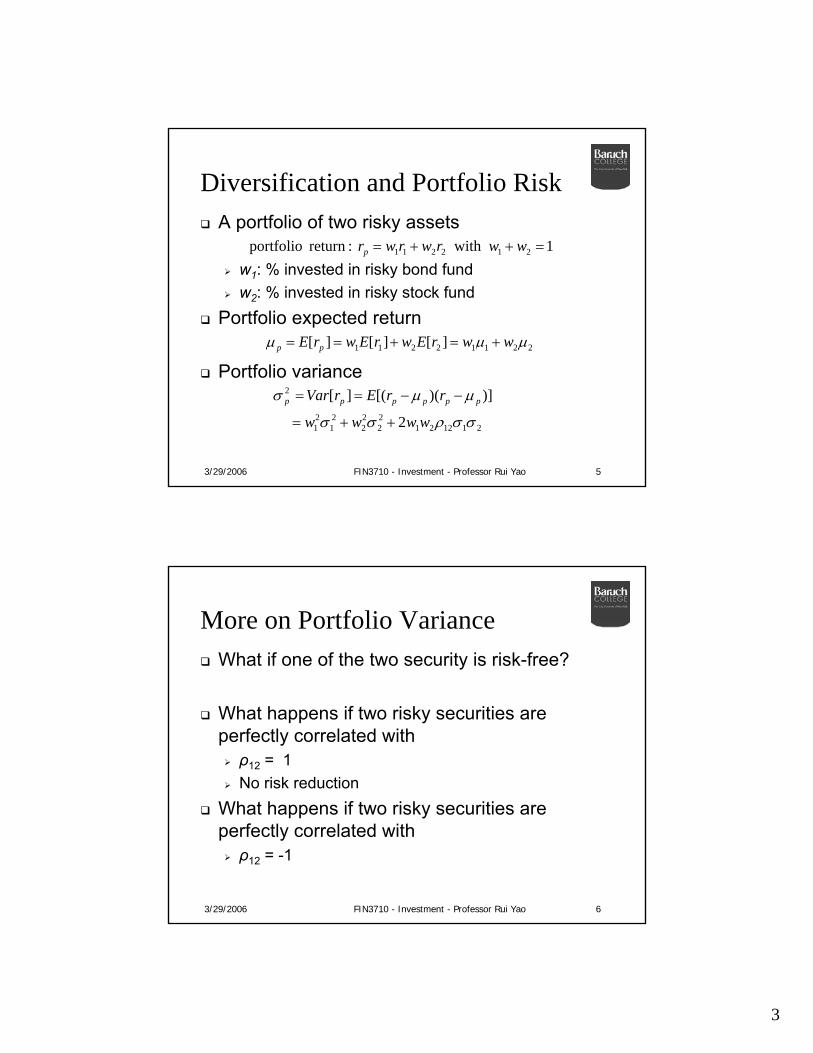

3/29/2006 FIN3710 - Investment - Professor Rui Yao 3

Diversification and Portfolio RiskCovariance and correlation

Measure degrees of co-movement between two stocksCovariance: non-standardized measure

Correlation coefficient: standardized measure

r1

r2

r1

r2

r1

r2

0 < ρ12 < 1 -1 < ρ12 < 0 ρ12 = 0

2121221121 ][)])([(],[ µµµµ −=−−= rrErrErrCov

11 and ],[],[12211221

21

2112 ≤≤−=⇒= ρσσρ

σσρ rrCovrrCov

3/29/2006 FIN3710 - Investment - Professor Rui Yao 4

Example: Covariance and CorrelationCalculating covariance

s p r1 r2 p*r1 p*r2 p*[r1-mu1] 2̂ p*[r2-mu2] 2̂ p*[r1*r2-mu1*mu2]Bust 0.30 -11.00 16.00 -3.30 4.80 132.30 30.00 -70.80normal 0.40 13.00 6.00 5.20 2.40 3.60 0.00 7.20Boom 0.30 27.00 -4.00 8.10 -1.20 86.70 30.00 -50.40

10.00 6.00 222.60 60.00 -114.0014.92 7.75 -0.99

Means Std. Dev. Cov. Corr.

2121212121

2211221121

)]()()[(][],[

)])()()()[(()])([(],[

µµµµ

µµµµ

−=−=

−−=−−=

∑

∑srsrsprrErrCov

srsrsprrErrCov

s

s

3

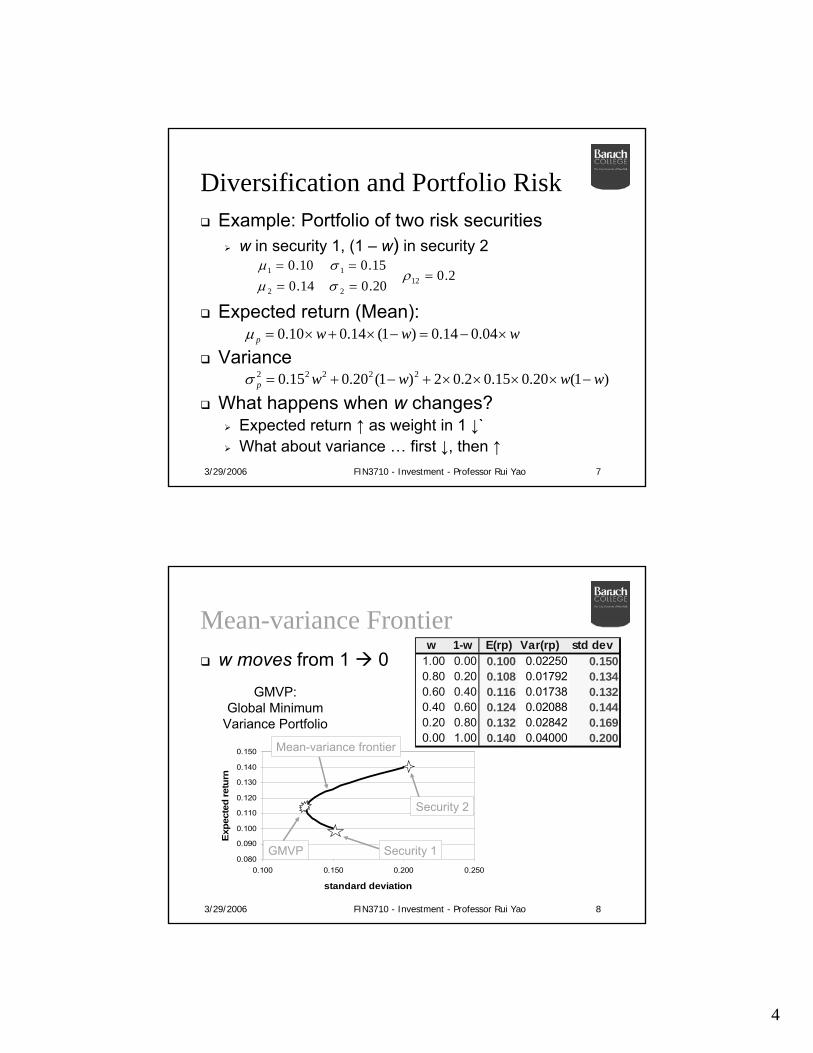

3/29/2006 FIN3710 - Investment - Professor Rui Yao 5

Diversification and Portfolio RiskA portfolio of two risky assets

w1: % invested in risky bond fundw2: % invested in risky stock fund

Portfolio expected return

Portfolio variance

1 with :return portfolio 212211 =++= wwrwrwrp

22112211 ][][][ µµµ wwrEwrEwrE pp +=+==

21122122

22

21

21

2

2

)])([(][

σσρσσ

µµσ

wwww

rrErVar pppppp

++=

−−==

3/29/2006 FIN3710 - Investment - Professor Rui Yao 6

More on Portfolio VarianceWhat if one of the two security is risk-free?

What happens if two risky securities are perfectly correlated with

ρ12 = 1No risk reduction

What happens if two risky securities are perfectly correlated with

ρ12 = -1

4

3/29/2006 FIN3710 - Investment - Professor Rui Yao 7

Diversification and Portfolio RiskExample: Portfolio of two risk securities

w in security 1, (1 – w) in security 2

Expected return (Mean):

Variance

What happens when w changes?Expected return ↑ as weight in 1 ↓`What about variance … first ↓, then ↑

2.020.014.015.010.0

1222

11 =====

ρσµσµ

wwwp ×−=−×+×= 04.014.0)1(14.010.0µ

)1(20.015.02.02)1(20.015.0 22222 wwwwp −××××+−+=σ

3/29/2006 FIN3710 - Investment - Professor Rui Yao 8

Mean-variance Frontierw moves from 1 0

w 1-w E(rp) Var(rp) std dev1.00 0.00 0.100 0.02250 0.1500.80 0.20 0.108 0.01792 0.1340.60 0.40 0.116 0.01738 0.1320.40 0.60 0.124 0.02088 0.1440.20 0.80 0.132 0.02842 0.1690.00 1.00 0.140 0.04000 0.200

0.080

0.090

0.100

0.110

0.120

0.130

0.140

0.150

0.100 0.150 0.200 0.250

standard deviation

Expe

cted

retu

rn

Security 1

Security 2

Mean-variance frontier

GMVP

GMVP: Global Minimum

Variance Portfolio

5

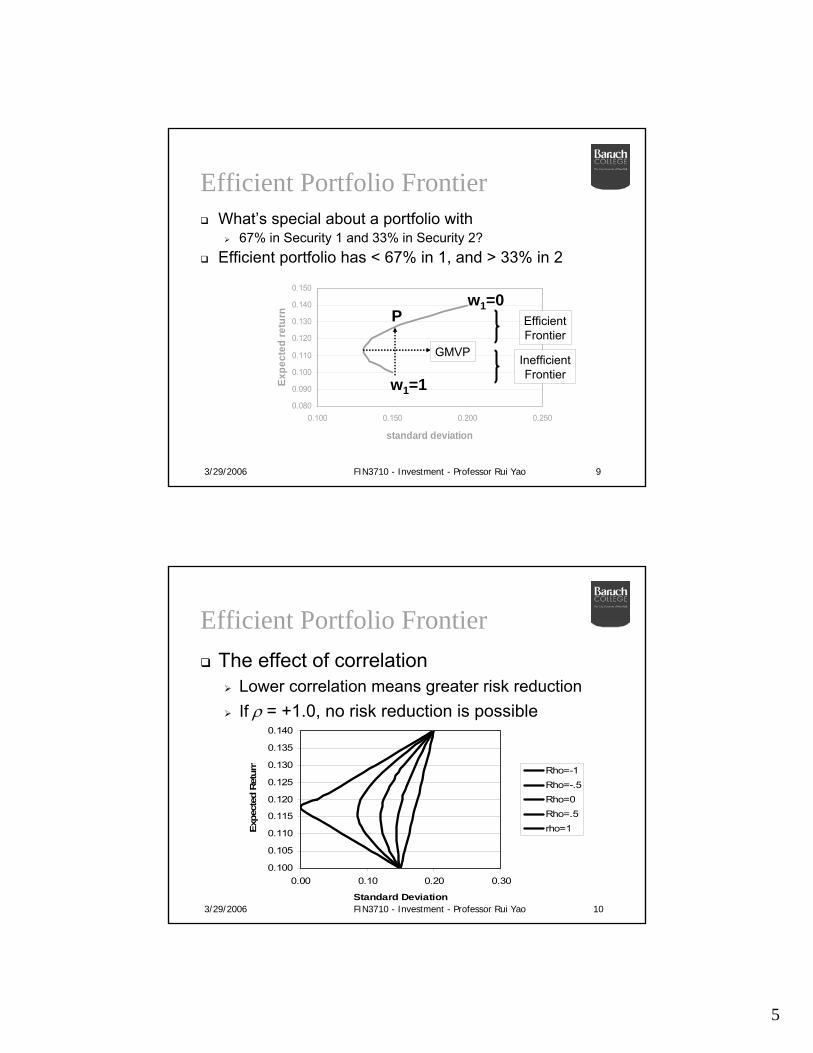

3/29/2006 FIN3710 - Investment - Professor Rui Yao 9

Efficient Portfolio FrontierWhat’s special about a portfolio with

67% in Security 1 and 33% in Security 2?Efficient portfolio has < 67% in 1, and > 33% in 2

0.080

0.090

0.100

0.110

0.120

0.130

0.140

0.150

0.100 0.150 0.200 0.250

standard deviation

Expe

cted

retu

rn

InefficientFrontier

EfficientFrontier

GMVP

w1=1

w1=0P

3/29/2006 FIN3710 - Investment - Professor Rui Yao 10

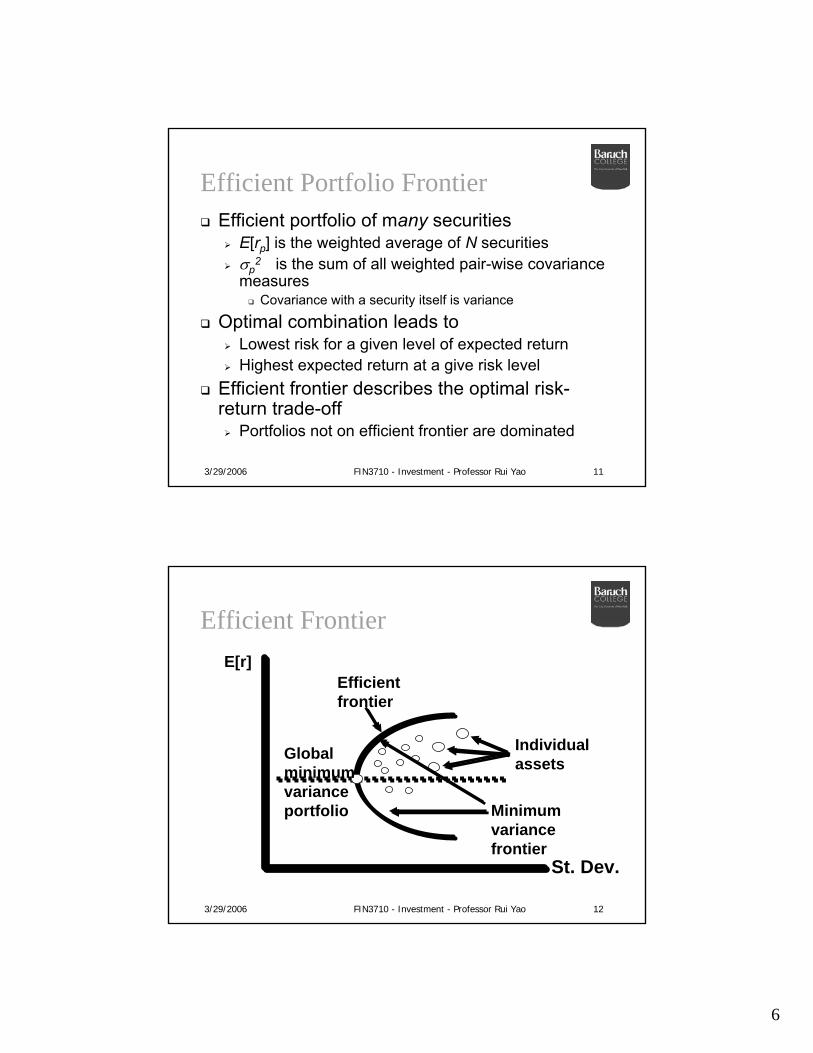

Efficient Portfolio FrontierThe effect of correlation

Lower correlation means greater risk reductionIf ρ = +1.0, no risk reduction is possible

0.100

0.105

0.110

0.115

0.120

0.125

0.130

0.135

0.140

0.00 0.10 0.20 0.30

Standard Deviation

Exp

ecte

d R

etur

n Rho=-1Rho=-.5Rho=0Rho=.5rho=1

6

3/29/2006 FIN3710 - Investment - Professor Rui Yao 11

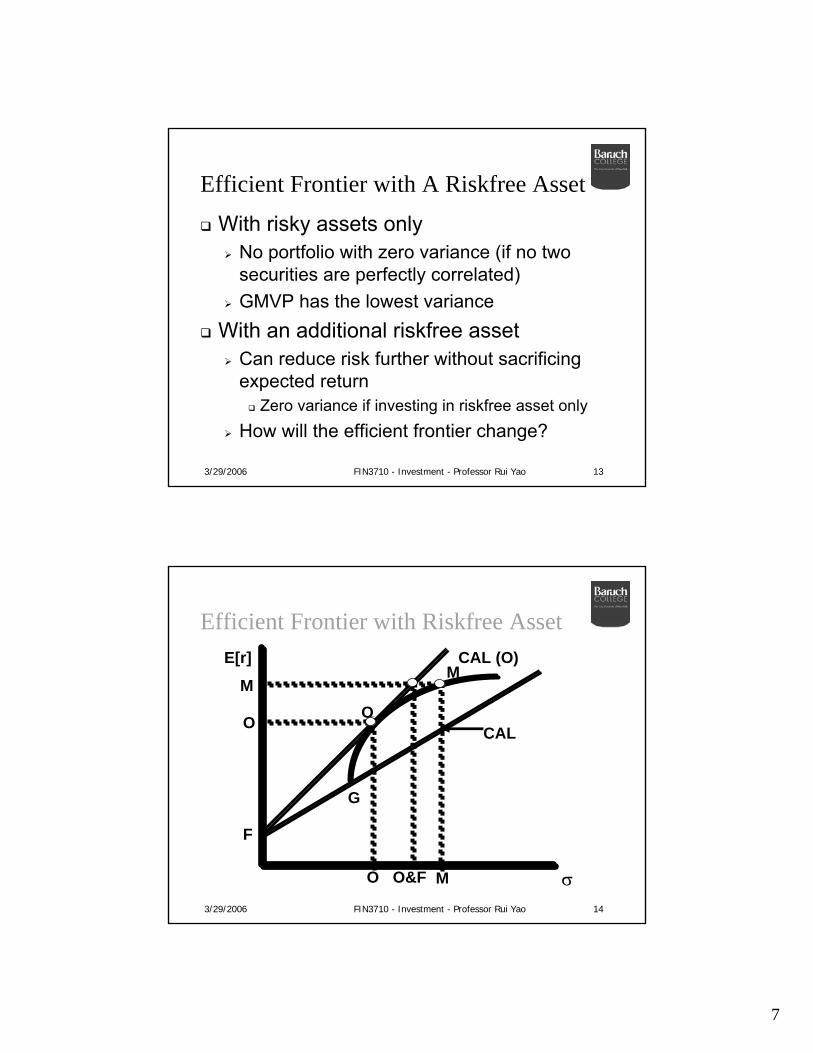

Efficient Portfolio FrontierEfficient portfolio of many securities

E[rp] is the weighted average of N securitiesσp

2 is the sum of all weighted pair-wise covariance measures

Covariance with a security itself is variance

Optimal combination leads to Lowest risk for a given level of expected returnHighest expected return at a give risk level

Efficient frontier describes the optimal risk-return trade-off

Portfolios not on efficient frontier are dominated

3/29/2006 FIN3710 - Investment - Professor Rui Yao 12

Efficient FrontierE[r]

Efficientfrontier

Globalminimumvarianceportfolio Minimum

variancefrontier

Individualassets

St. Dev.

7

3/29/2006 FIN3710 - Investment - Professor Rui Yao 13

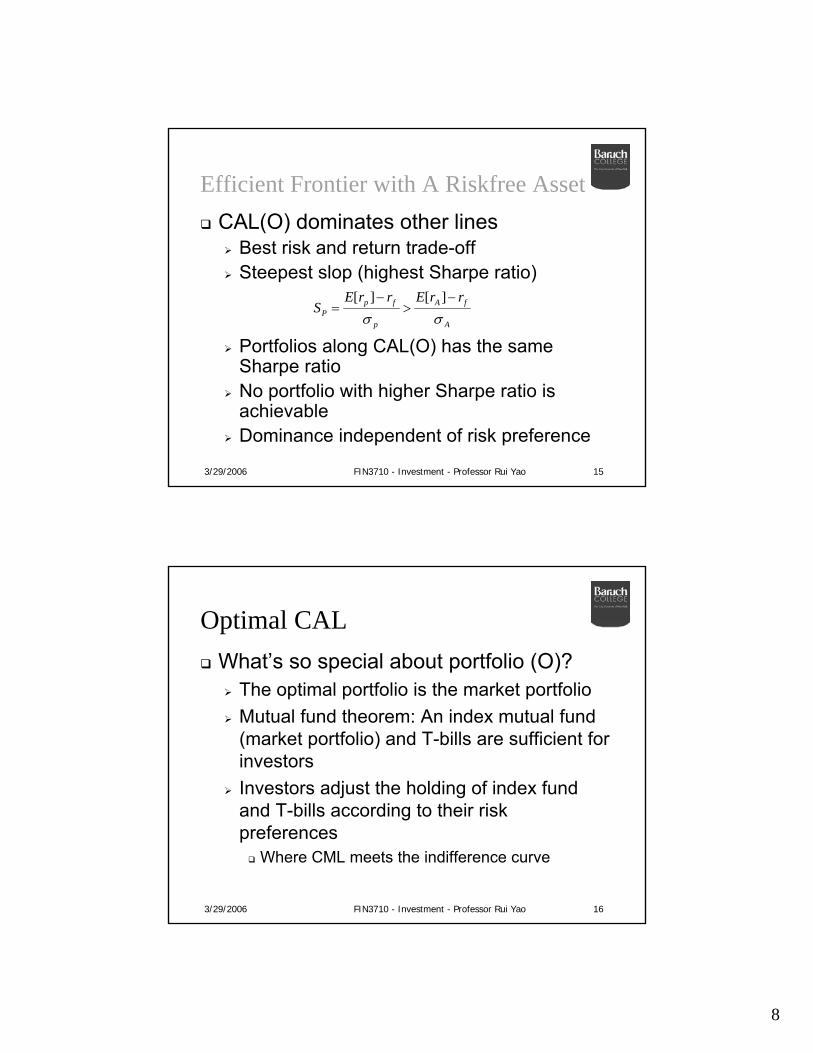

Efficient Frontier with A Riskfree AssetWith risky assets only

No portfolio with zero variance (if no two securities are perfectly correlated)GMVP has the lowest variance

With an additional riskfree assetCan reduce risk further without sacrificing expected return

Zero variance if investing in riskfree asset onlyHow will the efficient frontier change?

3/29/2006 FIN3710 - Investment - Professor Rui Yao 14

Efficient Frontier with Riskfree AssetE[r]

CAL

CAL (O)

M

O

F

O O&F M

G

O

M

σ

8

3/29/2006 FIN3710 - Investment - Professor Rui Yao 15

Efficient Frontier with A Riskfree AssetCAL(O) dominates other lines

Best risk and return trade-offSteepest slop (highest Sharpe ratio)

Portfolios along CAL(O) has the same Sharpe ratioNo portfolio with higher Sharpe ratio is achievableDominance independent of risk preference

A

fA

p

fpP

rrErrES

σσ−

>−

=][][

3/29/2006 FIN3710 - Investment - Professor Rui Yao 16

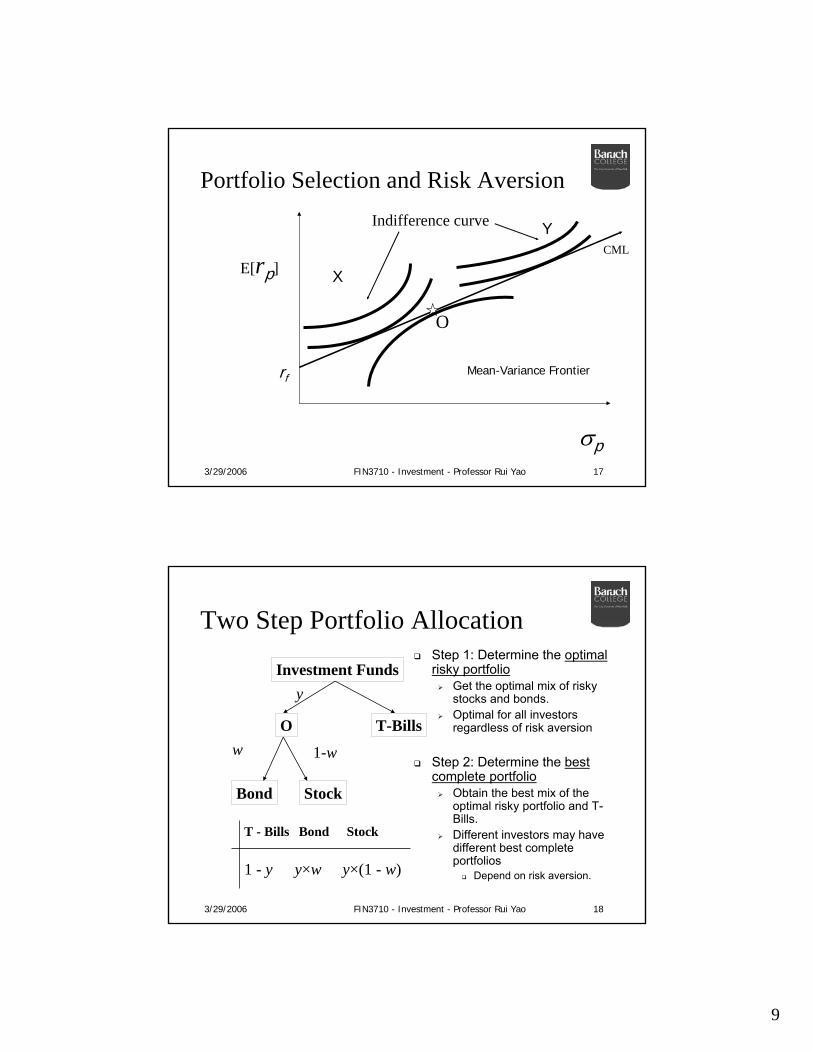

Optimal CALWhat’s so special about portfolio (O)?

The optimal portfolio is the market portfolioMutual fund theorem: An index mutual fund (market portfolio) and T-bills are sufficient for investorsInvestors adjust the holding of index fund and T-bills according to their risk preferences

Where CML meets the indifference curve

9

3/29/2006 FIN3710 - Investment - Professor Rui Yao 17

Portfolio Selection and Risk Aversion

E[rp]

σp

O

Indifference curve

CML

X

Y

Mean-Variance Frontierrf

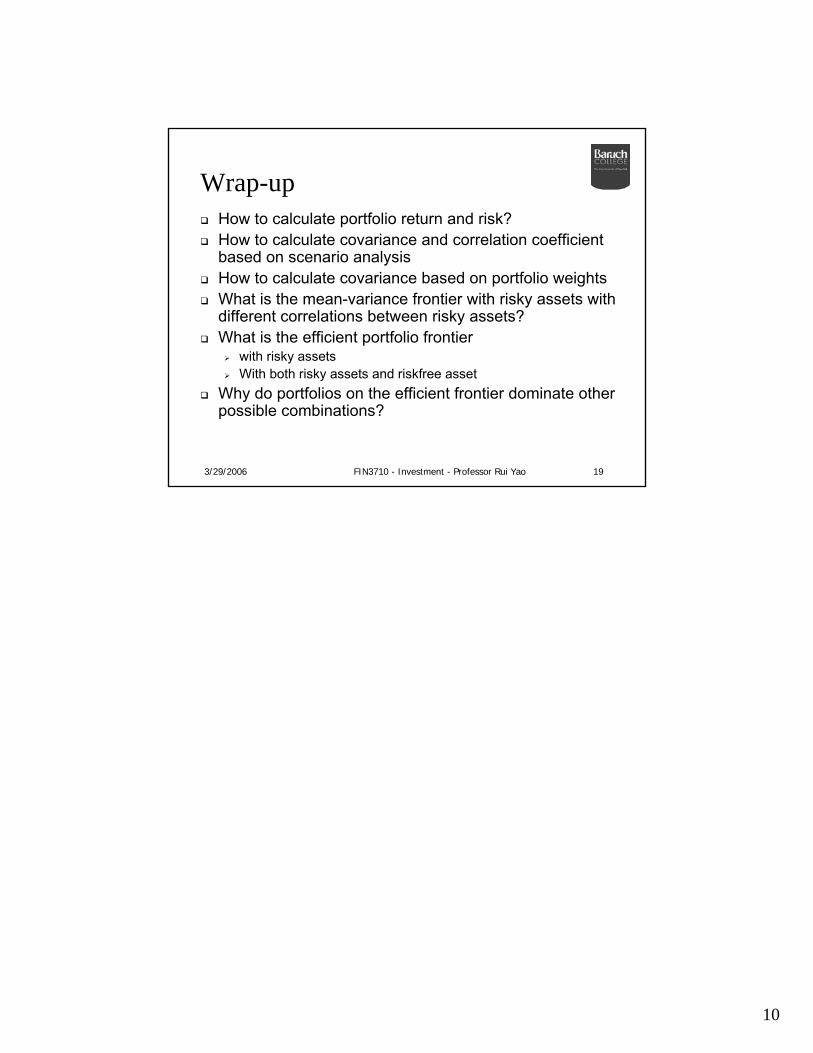

3/29/2006 FIN3710 - Investment - Professor Rui Yao 18

Two Step Portfolio AllocationStep 1: Determine the optimal risky portfolio

Get the optimal mix of risky stocks and bonds. Optimal for all investors regardless of risk aversion

Step 2: Determine the best complete portfolio

Obtain the best mix of the optimal risky portfolio and T-Bills. Different investors may have different best complete portfolios

Depend on risk aversion.

Investment Funds

O T-Bills

Bond Stock

w 1-w

T - Bills Bond Stock

1 - y y×w y×(1 - w)

y

10

3/29/2006 FIN3710 - Investment - Professor Rui Yao 19

Wrap-upHow to calculate portfolio return and risk?How to calculate covariance and correlation coefficient based on scenario analysisHow to calculate covariance based on portfolio weightsWhat is the mean-variance frontier with risky assets with different correlations between risky assets?What is the efficient portfolio frontier

with risky assets With both risky assets and riskfree asset

Why do portfolios on the efficient frontier dominate other possible combinations?