Making the Right Moves: Guiding α-Expansion using Local Primal-Dual Gaps

RISKS, ORGANIZATION AND STRUCTURE OF BANKING INDUSTRY IN CHINA

LECTURE 2

9/27/2017 1 ACEM, SJTU, Nan Li

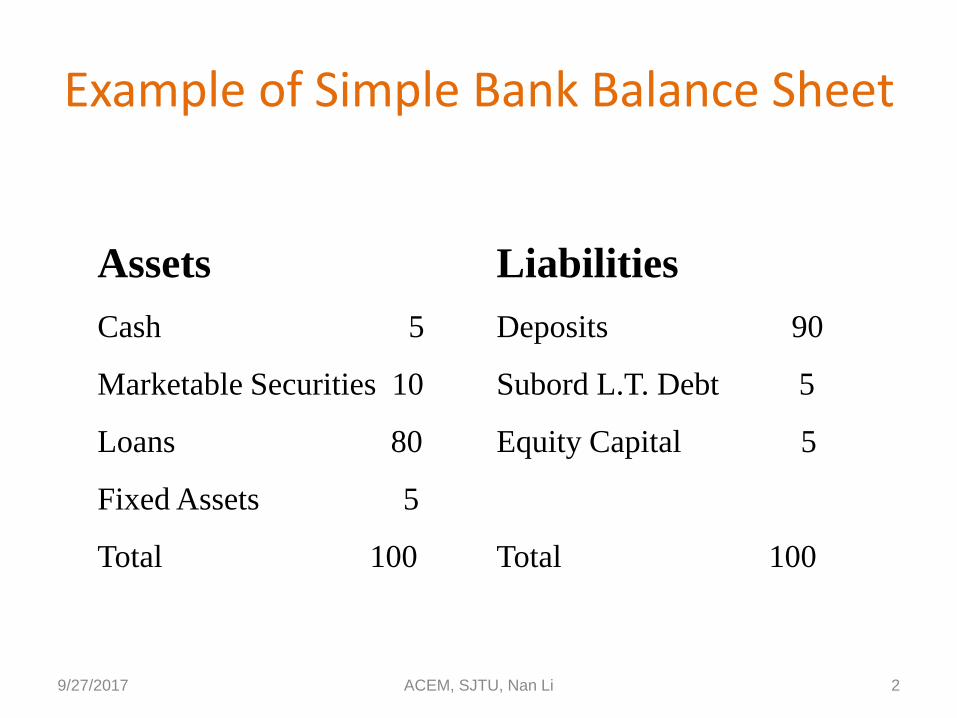

Example of Simple Bank Balance Sheet

Assets

Cash 5

Marketable Securities 10

Loans 80

Fixed Assets 5

Total 100

Liabilities

Deposits 90

Subord L.T. Debt 5

Equity Capital 5

Total 100

9/27/2017 2 ACEM, SJTU, Nan Li

Risks Faced by FIs

• What are the risks faced by the FIs when they provide the services to the economy?

– Interest Risk

– Credit Risk

– Liquidity Risk

9/27/2017 3 ACEM, SJTU, Nan Li

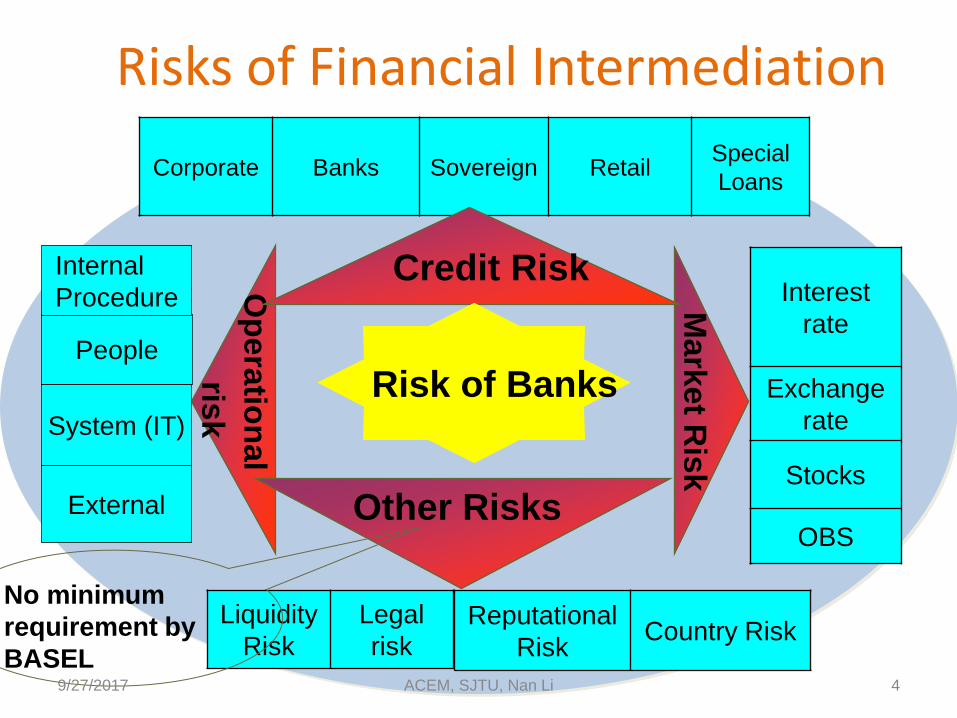

Corporate Banks Sovereign Retail Special

Loans

System (IT)

People

Internal

Procedure Interest

rate

Exchange

rate

Stocks

OBS

Liquidity

Risk

Legal

risk

Op

era

tion

al

risk

Credit Risk Ma

rke

t Ris

k

Other Risks

Reputational

Risk Country Risk

Risk of Banks

No minimum

requirement by

BASEL

External

Risks of Financial Intermediation

9/27/2017 4 ACEM, SJTU, Nan Li

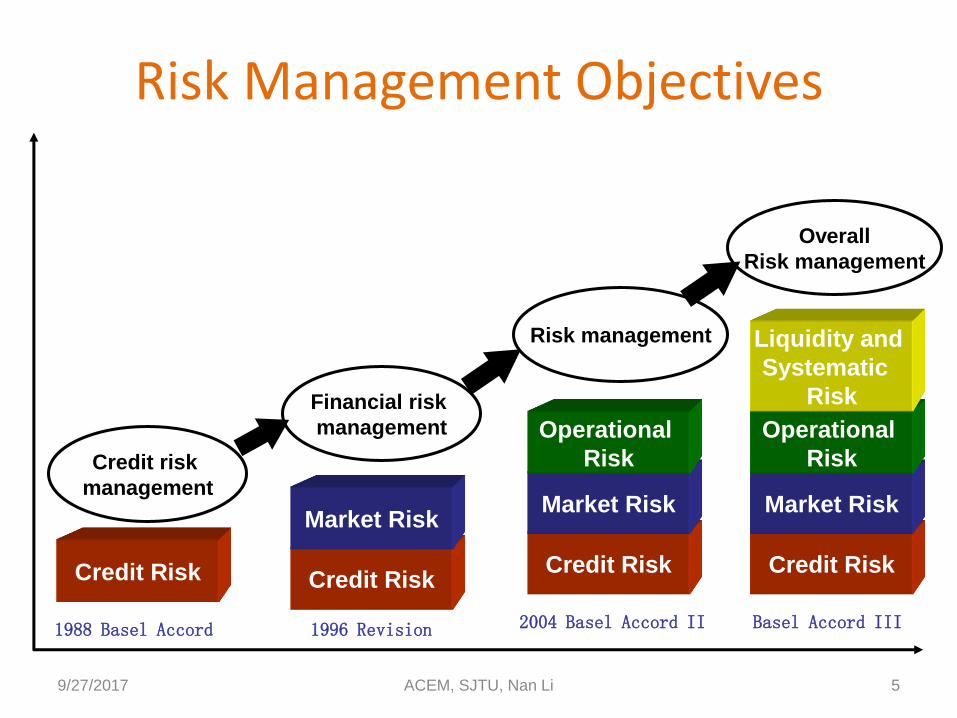

Risk Management Objectives

Credit Risk

Market Risk

Financial risk

management

Credit Risk

Market Risk

Operational

Risk

Risk management

Credit Risk

Credit risk

management

1988 Basel Accord 1996 Revision 2004 Basel Accord II

9/27/2017 5

Credit Risk

Market Risk

Operational

Risk

Liquidity and

Systematic

Risk

Overall

Risk management

Basel Accord III

ACEM, SJTU, Nan Li

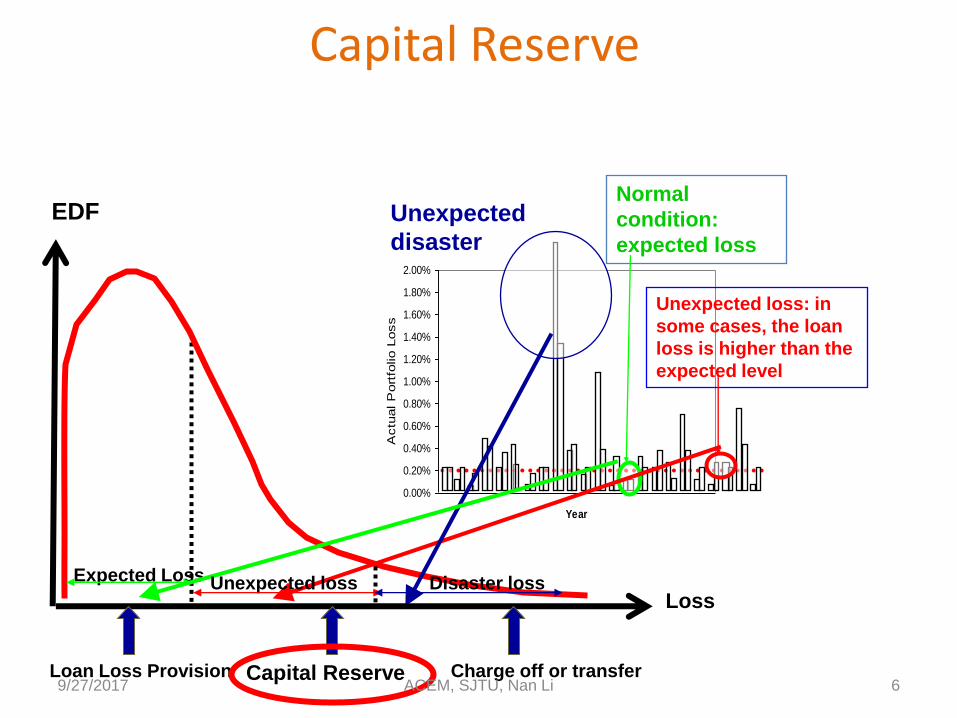

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

2.00%

Year

Actu

al P

ort

folio L

oss

Unexpected

disaster

Normal

condition:

expected loss

Unexpected loss: in

some cases, the loan

loss is higher than the

expected level

Expected Loss

Loss

EDF

Unexpected loss Disaster loss

Capital Reserve

Loan Loss Provision Capital Reserve Charge off or transfer 9/27/2017 6 ACEM, SJTU, Nan Li

Basel Accords in China • 2004/02: (localized)Basel I

– Definition of capital, similar with difference

– Risk weight and conversion factor of OBS activities

– Capital adequacy ratio 8%, (4% for core capital) same

– Detailed methods to compute interest rate risk, market risk (stock risk, exchange rate risk, commodity risk, option risk), capital requirement for market risk only applicable for large commercial banks

9/27/2017 7 ACEM, SJTU, Nan Li

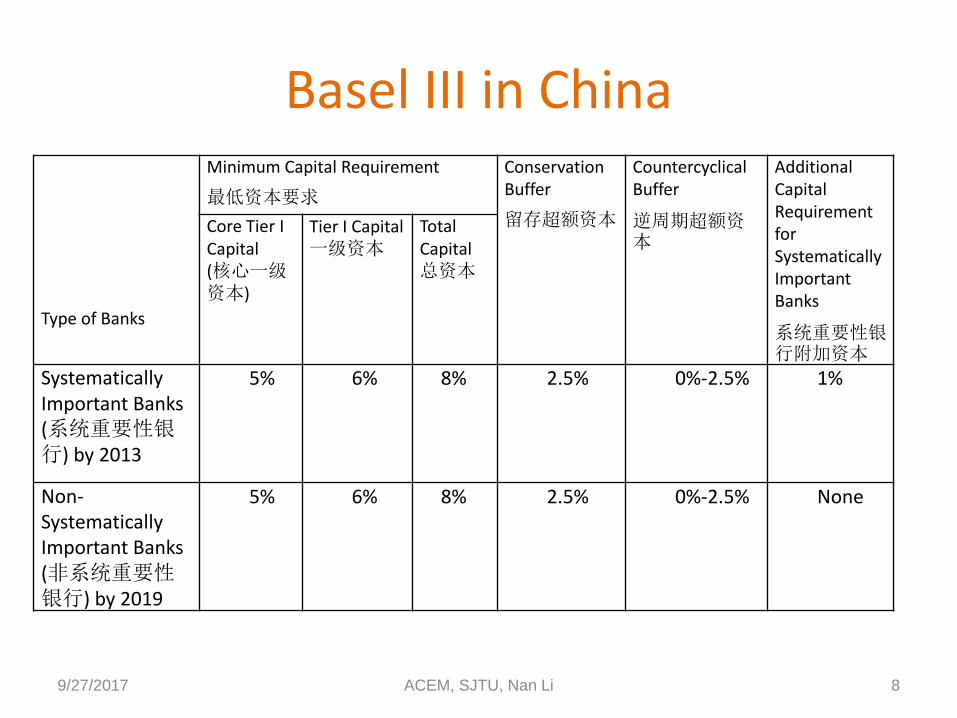

Basel III in China

Type of Banks

Minimum Capital Requirement

最低资本要求

Conservation Buffer

留存超额资本

Countercyclical Buffer

逆周期超额资本

Additional Capital Requirement for Systematically Important Banks

系统重要性银行附加资本

Core Tier I Capital (核心一级资本)

Tier I Capital 一级资本

Total Capital 总资本

Systematically Important Banks (系统重要性银行) by 2013

5% 6% 8% 2.5% 0%-2.5% 1%

Non-Systematically Important Banks (非系统重要性银行) by 2019

5% 6% 8% 2.5% 0%-2.5% None

9/27/2017 8 ACEM, SJTU, Nan Li

Basel Accords in China • 2007/02: Basel II starts

– Banks may choose to follow Basel II or Basel I – By 2012, 5 large SOCB and 1 joint stock bank apply for Basel II

• 2012/11/30: Basel III starts – Macro prudential and micro prudential policy – Capital and liquidity regulation – Improve both quantity and quality of the capital – Introduce new concept: conservation buffer, countercyclical buffer, leverage

ratio, liquidity coverage ratio, and stable funding ratio – Four key indices:

• Capital adequacy ratio • Leverage ratio • Loan Loss Provision • Liquidity Ratios

– Basel: LCR, NSFR – +China: liquidity ratio, loan-to-deposit ratio, core liability ratio, liquidity gap ratio, concertration

ratio, interbank deposit concerntration ratio

9/27/2017 9 ACEM, SJTU, Nan Li

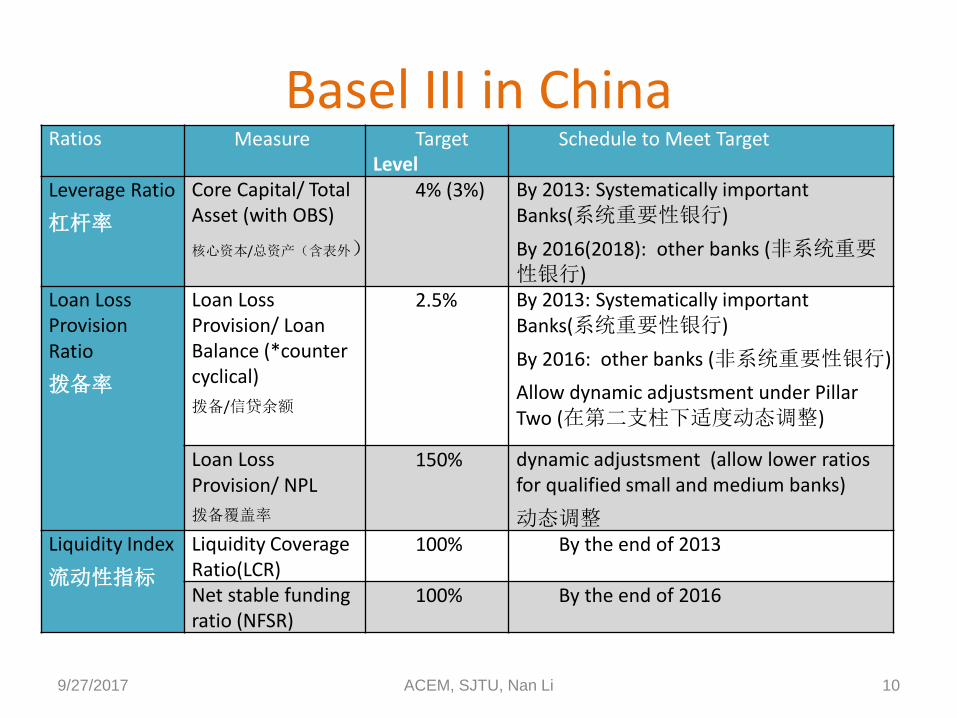

Basel III in China Ratios Measure Target

Level Schedule to Meet Target

Leverage Ratio

杠杆率

Core Capital/ Total Asset (with OBS)

核心资本/总资产(含表外)

4% (3%) By 2013: Systematically important Banks(系统重要性银行)

By 2016(2018): other banks (非系统重要性银行)

Loan Loss Provision Ratio

拨备率

Loan Loss Provision/ Loan Balance (*counter cyclical)

拨备/信贷余额

2.5% By 2013: Systematically important Banks(系统重要性银行)

By 2016: other banks (非系统重要性银行)

Allow dynamic adjustsment under Pillar Two (在第二支柱下适度动态调整)

Loan Loss Provision/ NPL

拨备覆盖率

150% dynamic adjustsment (allow lower ratios for qualified small and medium banks)

动态调整 Liquidity Index

流动性指标

Liquidity Coverage Ratio(LCR)

100% By the end of 2013

Net stable funding ratio (NFSR)

100% By the end of 2016

9/27/2017 10 ACEM, SJTU, Nan Li

Basel III in China

• By 2011Q4,

– Capital Adequacy Ratio: 12.7%

– Tier I capital Ratio: 10.2%

– Already meet and exceed the Basel III requirement (to be met by 2019)

– But still less than the 13.5% and 12.5% requirements in China for systematically and nonsystematically important banks, respectively, capital gap is 1 trillion RMB.

9/27/2017 11 ACEM, SJTU, Nan Li

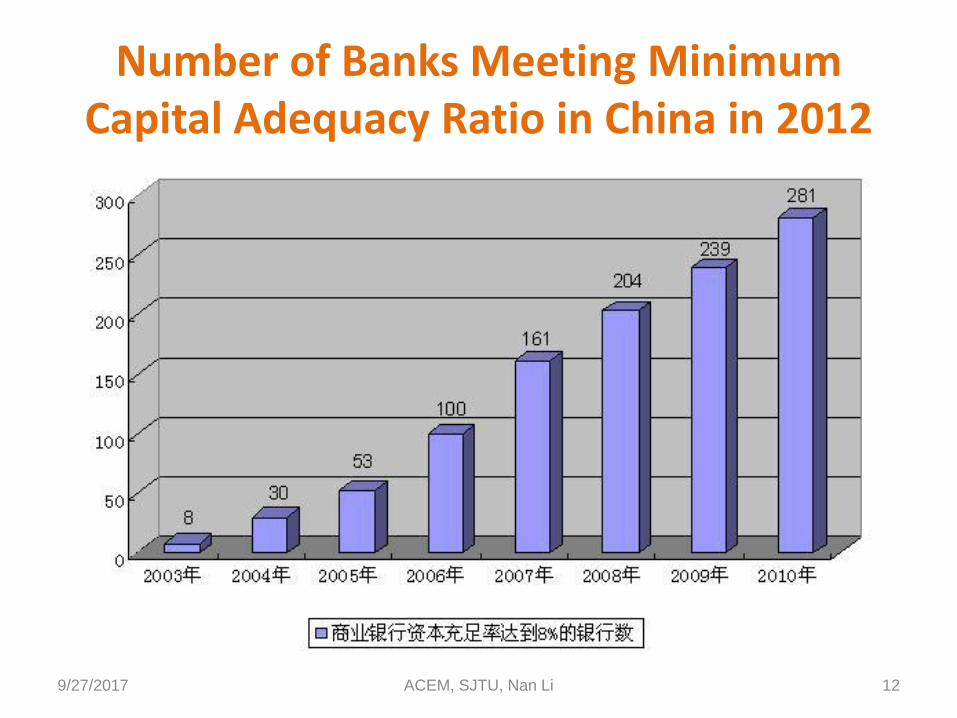

Number of Banks Meeting Minimum Capital Adequacy Ratio in China in 2012

9/27/2017 12 ACEM, SJTU, Nan Li

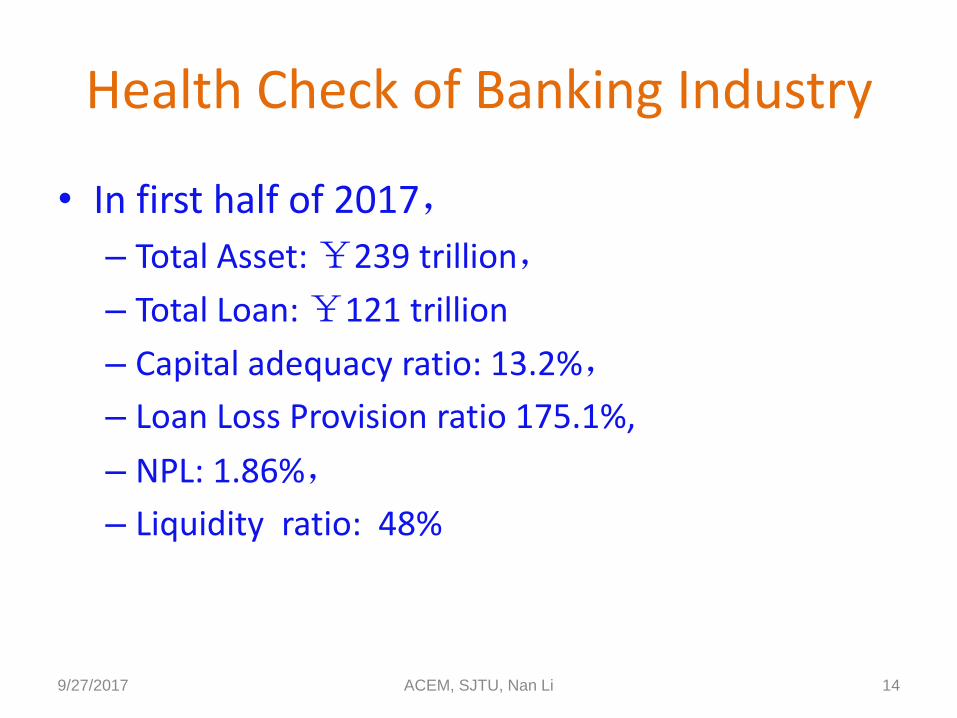

Health Check of Banking Industry

• In first half of 2017,

– Total Asset: ¥239 trillion,

– Total Loan: ¥121 trillion

– Capital adequacy ratio: 13.2%,

– Loan Loss Provision ratio 175.1%,

– NPL: 1.86%,

– Liquidity ratio: 48%

9/27/2017 14 ACEM, SJTU, Nan Li

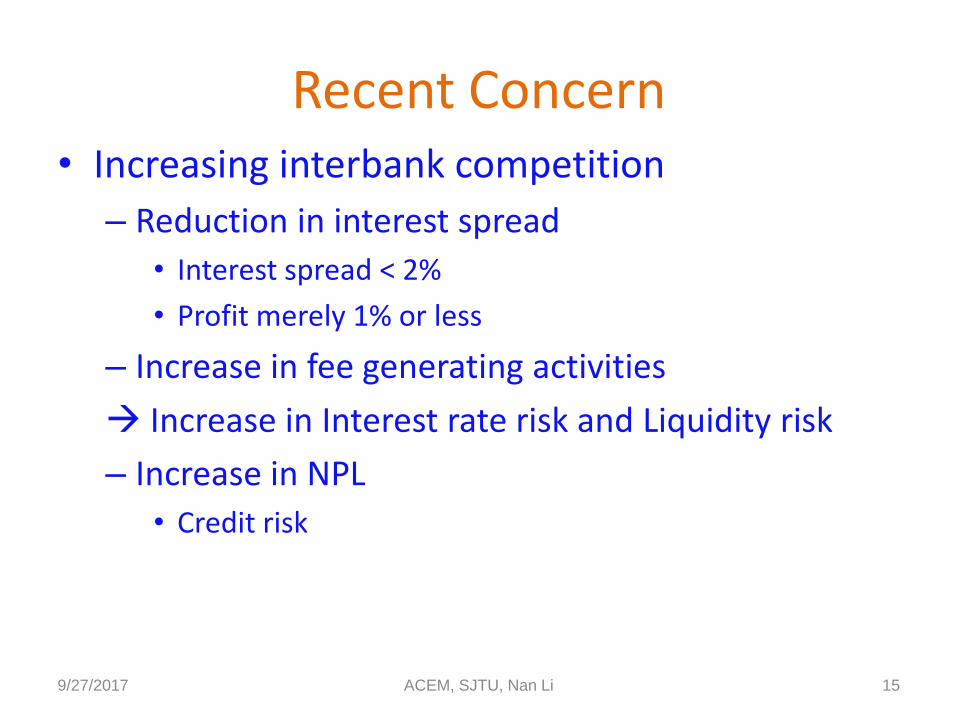

Recent Concern • Increasing interbank competition

– Reduction in interest spread

• Interest spread < 2%

• Profit merely 1% or less

– Increase in fee generating activities

Increase in Interest rate risk and Liquidity risk

– Increase in NPL

• Credit risk

9/27/2017 15 ACEM, SJTU, Nan Li

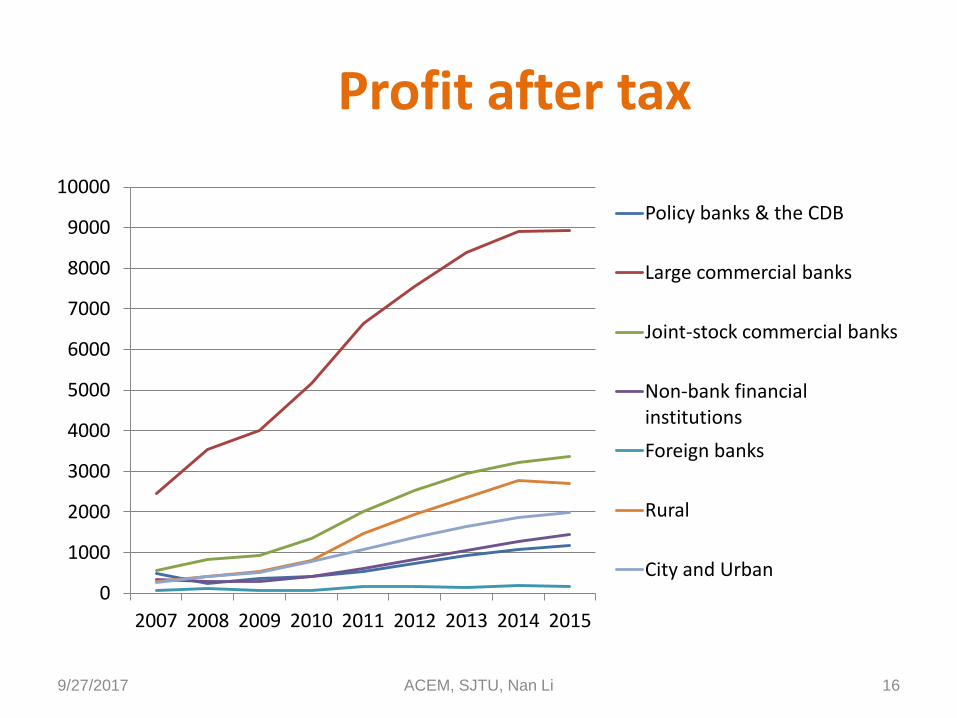

Profit after tax

9/27/2017 16

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2007 2008 2009 2010 2011 2012 2013 2014 2015

Policy banks & the CDB

Large commercial banks

Joint-stock commercial banks

Non-bank financial institutions

Foreign banks

Rural

City and Urban

ACEM, SJTU, Nan Li

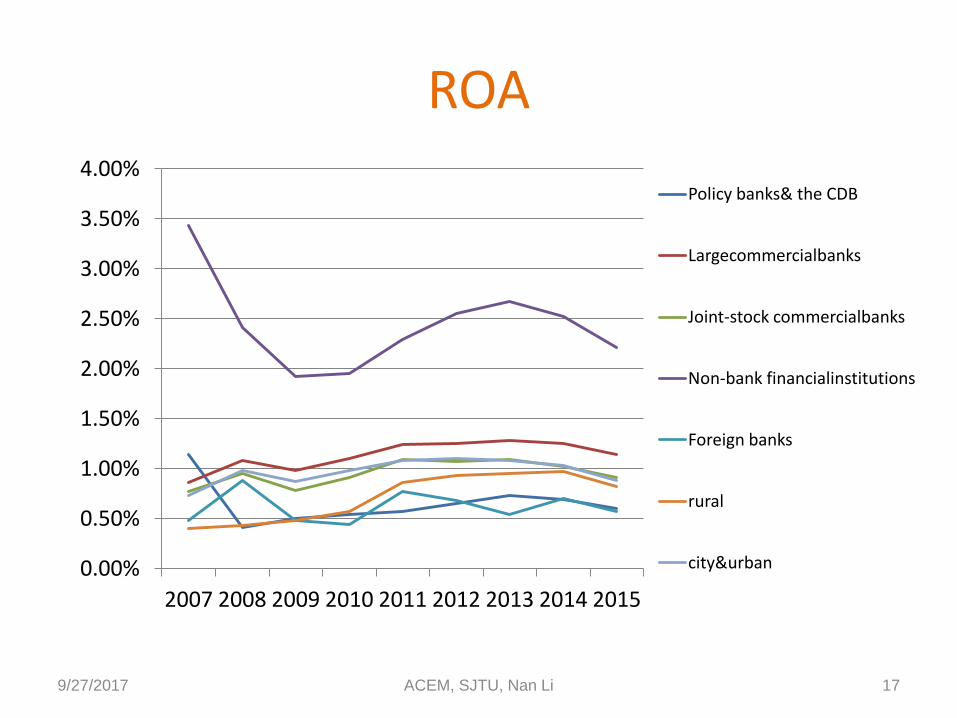

ROA

9/27/2017 17

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

2007 2008 2009 2010 2011 2012 2013 2014 2015

Policy banks& the CDB

Largecommercialbanks

Joint-stock commercialbanks

Non-bank financialinstitutions

Foreign banks

rural

city&urban

ACEM, SJTU, Nan Li

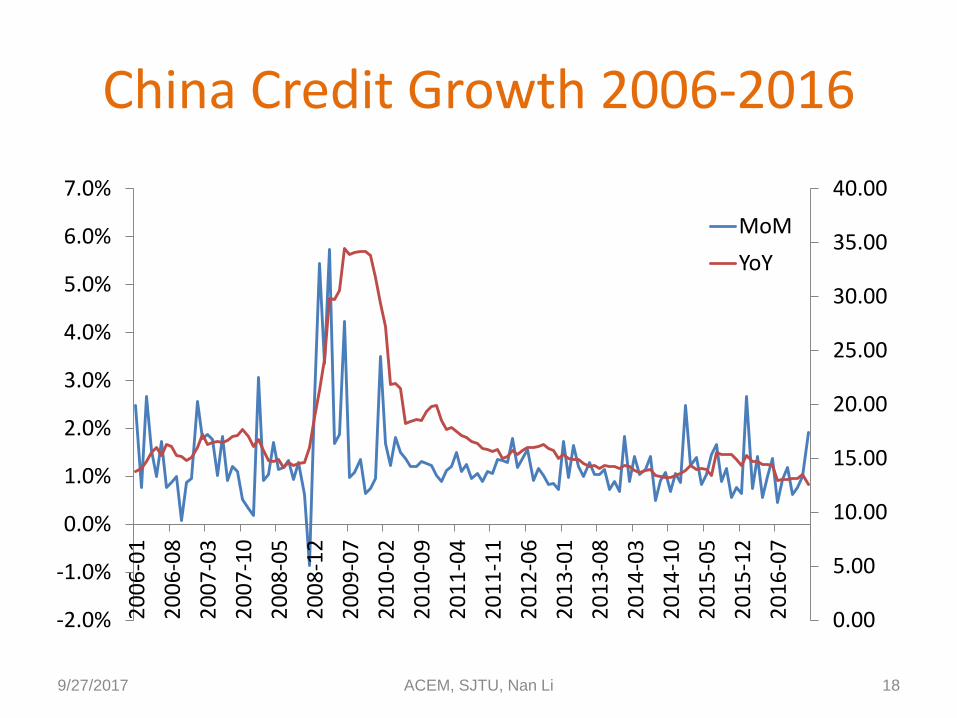

China Credit Growth 2006-2016

9/27/2017 18

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

20

06

-01

20

06

-08

20

07

-03

20

07

-10

20

08

-05

20

08

-12

20

09

-07

20

10

-02

20

10

-09

20

11

-04

20

11

-11

20

12

-06

20

13

-01

20

13

-08

20

14

-03

20

14

-10

20

15

-05

20

15

-12

20

16

-07

MoM

YoY

ACEM, SJTU, Nan Li

Quality of Credit in China

9/27/2017 19

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

20

06

-03

20

06

-10

20

07

-05

20

07

-12

20

08

-07

20

09

-02

20

09

-09

20

10

-04

20

10

-11

20

11

-06

20

12

-01

20

12

-08

20

13

-03

20

13

-10

20

14

-05

20

14

-12

20

15

-07

20

16

-02

20

16

-09

China Non-Performing Loans Growth Rate (Quarterly) 2006Q1-2016Q4

ACEM, SJTU, Nan Li

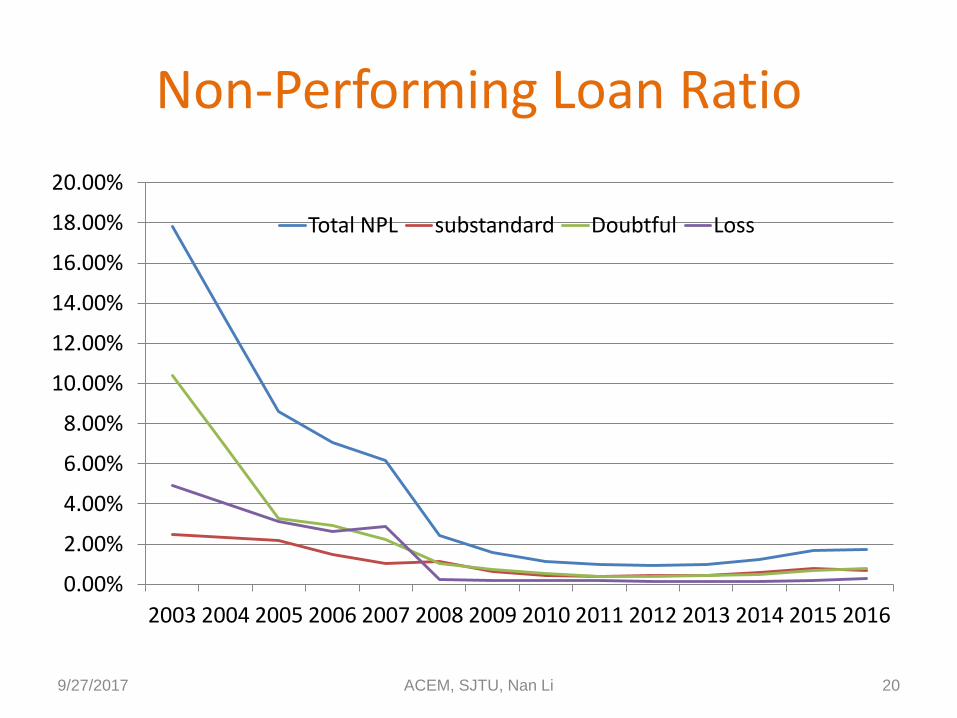

Non-Performing Loan Ratio

9/27/2017 20

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Total NPL substandard Doubtful Loss

ACEM, SJTU, Nan Li

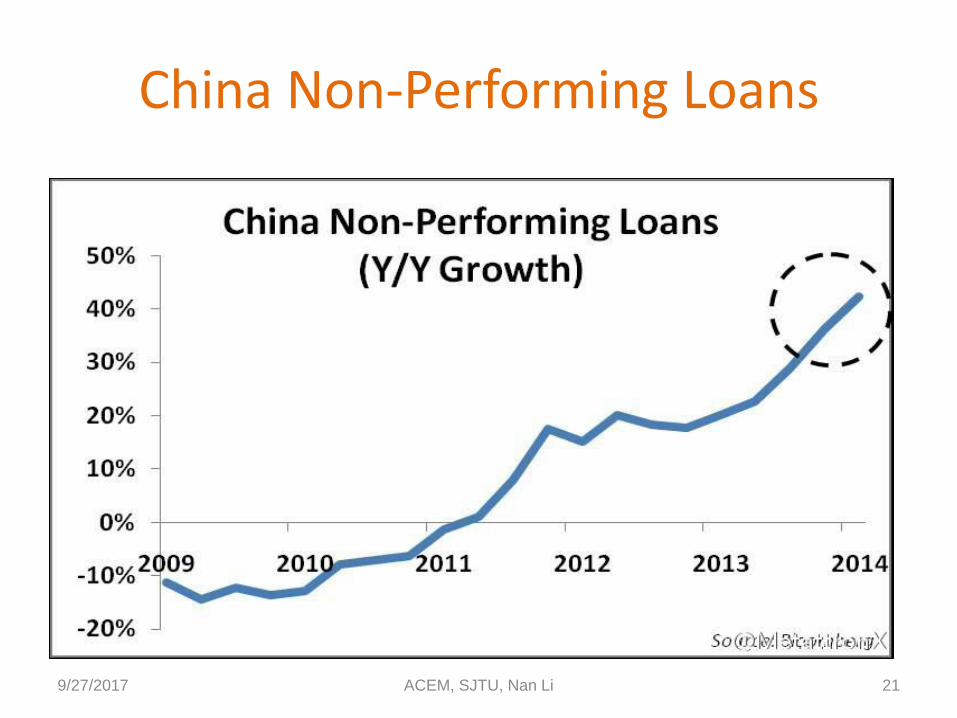

China Non-Performing Loans

9/27/2017 21 ACEM, SJTU, Nan Li

Risk Management

• How to manage these risks?

– Interest rate risk

– Credit risk

– Liquidity risk

9/27/2017 22 ACEM, SJTU, Nan Li

Interest Rate Risk: Models

• Repricing Gap Model

– Focuses on book value using accounting approach

– Main concern is net interest income

• Duration Model

– Focuses on market value

– Main concern is maintaining value and achieving targets

9/27/2017 23 ACEM, SJTU, Nan Li

Repricing Model

• Repricing or funding gap model based on book value.

– Contrasts with market value based maturity and duration models recommended by the Bank for International Settlements (BIS).

– Rate sensitivity means time to repricing.

– Repricing gap is the difference between the rate sensitivity of each asset and the rate sensitivity of each liability: RSA - RSL.

9/27/2017 24 ACEM, SJTU, Nan Li

Maturity Buckets

• Repricing can be the result of a rollover of an asset or liability, or because the asset is variable-rate instruments

• Commercial banks must report repricing gaps for assets and liabilities with maturities of: – One day.

– More than one day to three months.

– More than 3 three months to six months.

– More than six months to twelve months.

– More than one year to five years.

– Over five years.

9/27/2017 25 ACEM, SJTU, Nan Li

Applying the Repricing Model

• (Repricing Gap) GAPi = RSAi - RSLi

• Δ NIIi = (RSAi Δ Ri,A – RSLiΔ RiL)

• If Δ RA= Δ RL, then

Δ NIIi = GAPi*Δ Ri= (RSAi – RSLi)* Δ Ri

9/27/2017 26 ACEM, SJTU, Nan Li

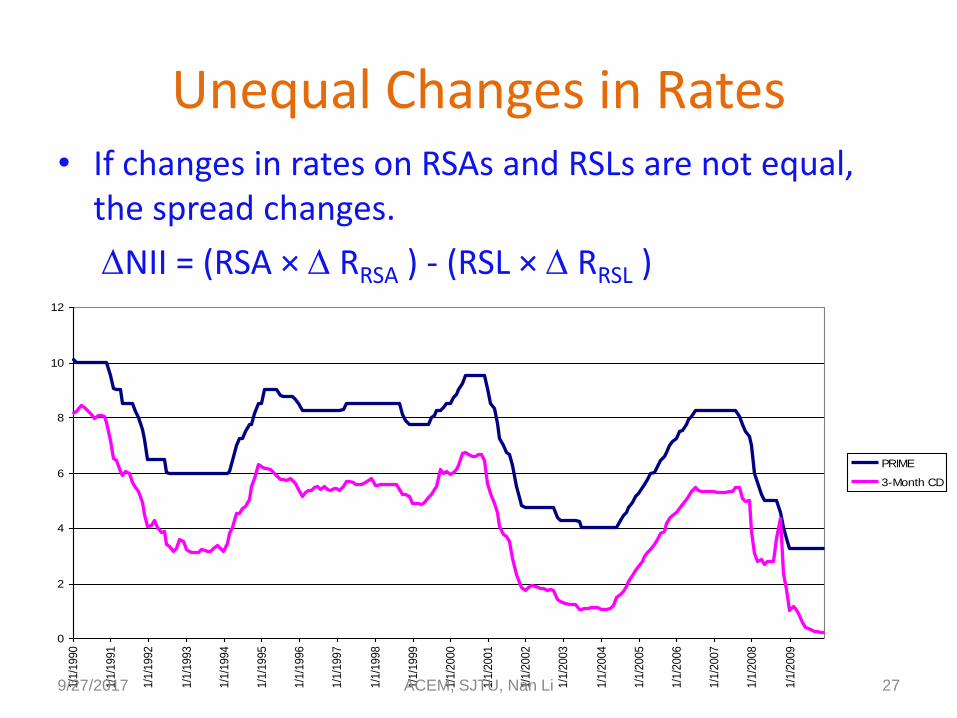

Unequal Changes in Rates • If changes in rates on RSAs and RSLs are not equal,

the spread changes.

NII = (RSA × RRSA ) - (RSL × RRSL )

0

2

4

6

8

10

12

1/1

/1990

1/1

/1991

1/1

/1992

1/1

/1993

1/1

/1994

1/1

/1995

1/1

/1996

1/1

/1997

1/1

/1998

1/1

/1999

1/1

/2000

1/1

/2001

1/1

/2002

1/1

/2003

1/1

/2004

1/1

/2005

1/1

/2006

1/1

/2007

1/1

/2008

1/1

/2009

PRIME

3-Month CD

9/27/2017 27 ACEM, SJTU, Nan Li

Duration Model

• A market value-based model for assessing and managing interest rate risk:

– Duration

– Computation of duration

– Economic interpretation

– Immunization using duration

– Problems in applying duration

9/27/2017 28 ACEM, SJTU, Nan Li

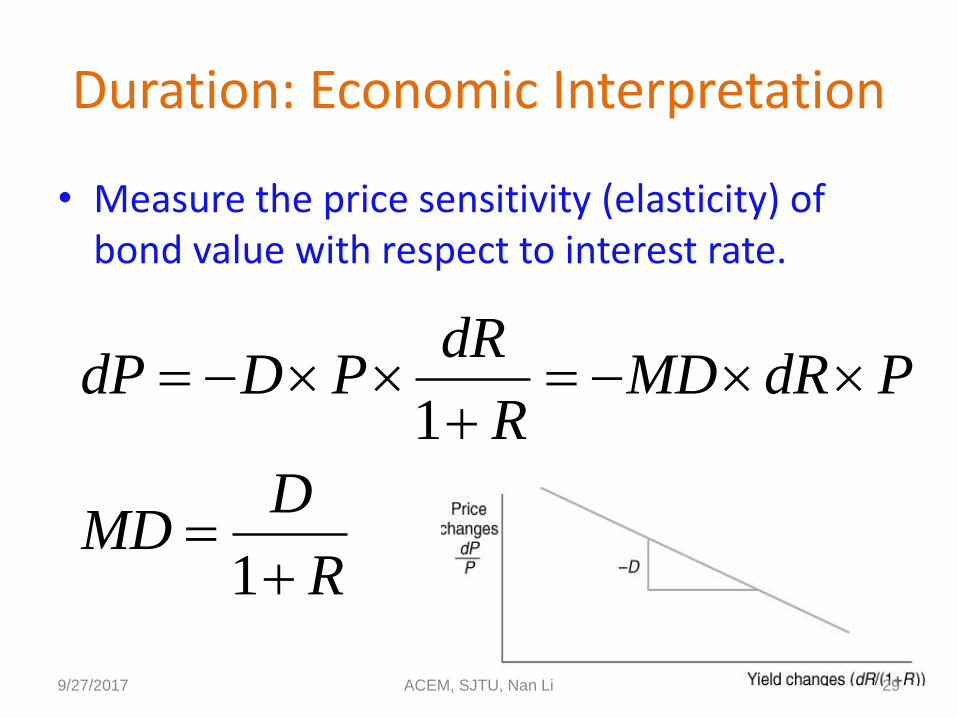

Duration: Economic Interpretation

• Measure the price sensitivity (elasticity) of bond value with respect to interest rate.

R

DMD

PdRMDR

dRPDdP

1

1

9/27/2017 29 ACEM, SJTU, Nan Li

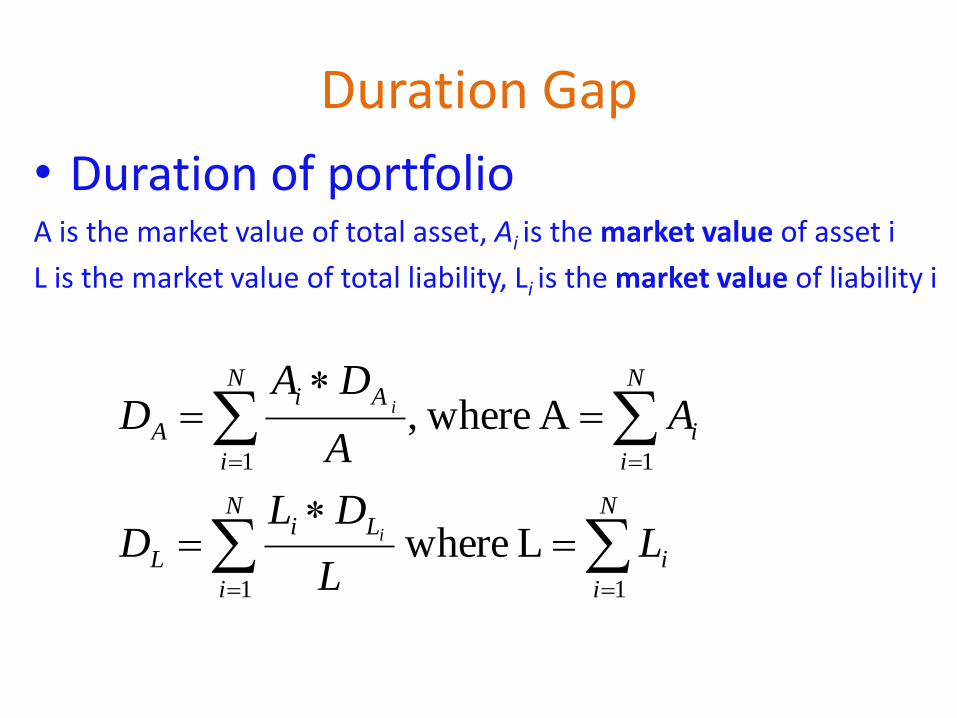

Duration Gap

• Duration of portfolio A is the market value of total asset, Ai is the market value of asset i

L is the market value of total liability, Li is the market value of liability i

N

i

i

N

i

Li

L

N

i

i

N

i

Ai

A

LL

DLD

AA

DAD

i

i

11

11

L where

A where,

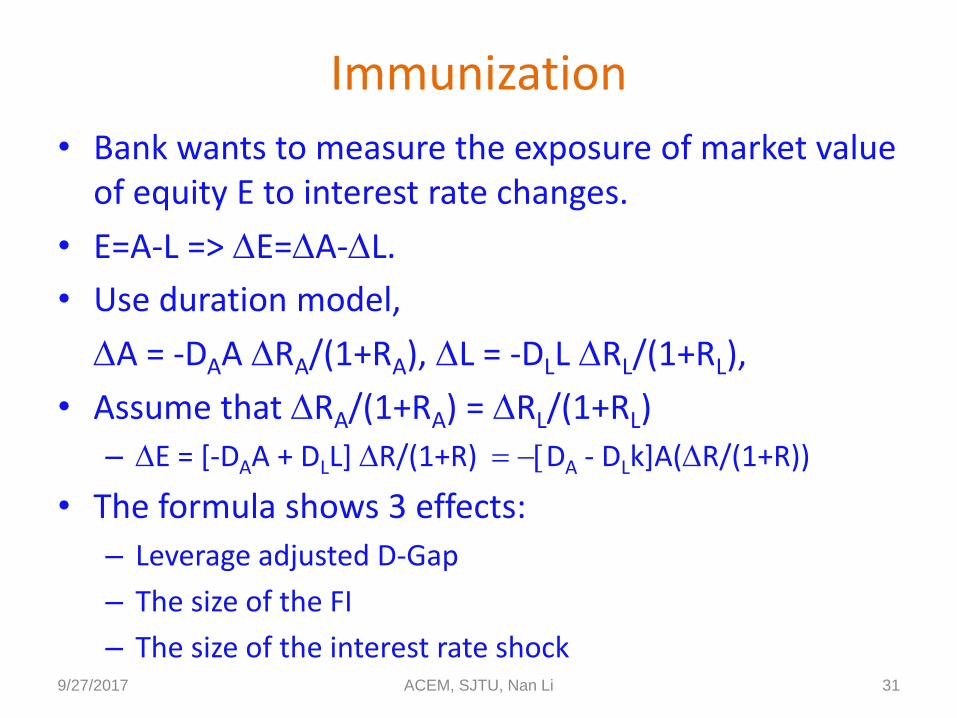

Immunization

• Bank wants to measure the exposure of market value of equity E to interest rate changes.

• E=A-L => E=A-L.

• Use duration model,

A = -DAA RA/(1+RA), L = -DLL RL/(1+RL),

• Assume that RA/(1+RA) = RL/(1+RL)

– E = [-DAA + DLL] R/(1+R) [DA - DLk]A(R/(1+R))

• The formula shows 3 effects:

– Leverage adjusted D-Gap

– The size of the FI

– The size of the interest rate shock 9/27/2017 31 ACEM, SJTU, Nan Li

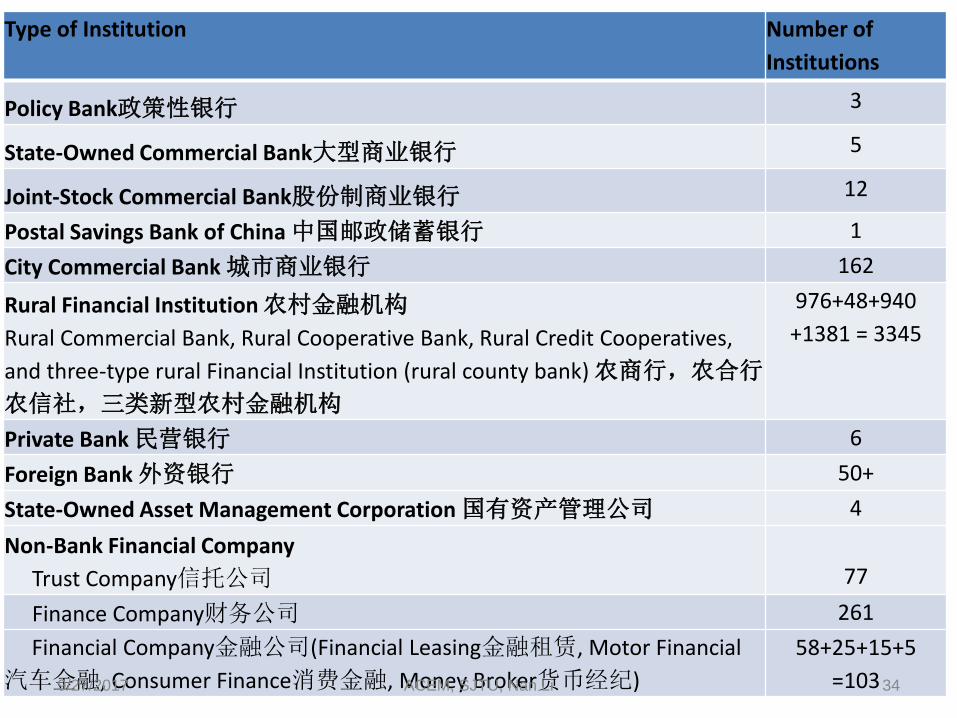

Financial Institutions in China • Banking (Depository) Institutions

– State-Owned Commercial Bank 大型商业银行 – Joint-Stock Commercial Bank 股份制商业银行 – City Commercial Bank 城市商业银行 – Rural Financial Institution 农村金融机构

• Rural Commercial Bank, 农村商业银行 • Rural Cooperative Bank, 农村合作银行 • Rural Credit Cooperatives, 农村信用社 • three-type rural Financial Institution (rural county bank, 三类新型农村金融机构)

– Postal Savings Bank of China 中国邮政储蓄银行 – Private Bank 民营银行 – Foreign Bank外资银行

9/27/2017 32 ACEM, SJTU, Nan Li

Financial Institutions in in China • Non Depository Financial Instiutions

– Policy Bank (政策性银行) – State-Owned Asset Management Corporation (国有资产管理公司) • Deals with the non-performing loans of state owned commercial

banks

• Non-banking Financial Instiutions – Trust Company 信托公司 – Finance Company 财务公司 – Financial Leasing Company 金融租赁公司 – Motor Finance Company 汽车金融公司 – Consumer Finance Company 消费金融公司 – Money Broker Company 货币经纪公司

9/27/2017 33 ACEM, SJTU, Nan Li

Type of Institution Number of

Institutions

Policy Bank政策性银行 3

State-Owned Commercial Bank大型商业银行 5

Joint-Stock Commercial Bank股份制商业银行 12

Postal Savings Bank of China 中国邮政储蓄银行 1

City Commercial Bank 城市商业银行 162

Rural Financial Institution 农村金融机构

Rural Commercial Bank, Rural Cooperative Bank, Rural Credit Cooperatives,

and three-type rural Financial Institution (rural county bank) 农商行,农合行,

农信社,三类新型农村金融机构

976+48+940

+1381 = 3345

Private Bank 民营银行 6

Foreign Bank 外资银行 50+

State-Owned Asset Management Corporation 国有资产管理公司 4

Non-Bank Financial Company

Trust Company信托公司

77

Finance Company财务公司 261

Financial Company金融公司(Financial Leasing金融租赁, Motor Financial

汽车金融, Consumer Finance消费金融, Money Broker货币经纪)

58+25+15+5

=103 9/27/2017 34 ACEM, SJTU, Nan Li

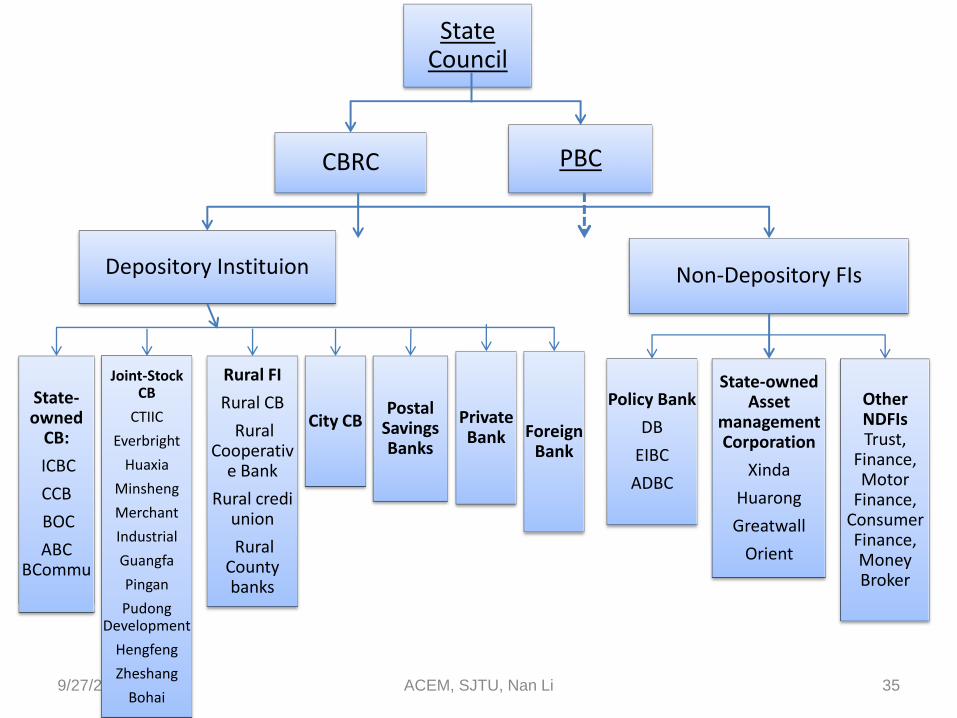

9/27/2017 35

State Council

PBC CBRC

Depository Instituion

State-owned

CB:

ICBC

CCB

BOC

ABC BCommu

Joint-Stock CB

CTIIC

Everbright

Huaxia

Minsheng

Merchant

Industrial

Guangfa

Pingan

Pudong Development

Hengfeng

Zheshang

Bohai

City CB

Rural FI

Rural CB

Rural Cooperativ

e Bank

Rural credi union

Rural County banks

Foreign Bank

Postal Savings Banks

Private Bank

Non-Depository FIs

Policy Bank

DB

EIBC

ADBC

State-owned Asset

management Corporation

Xinda

Huarong

Greatwall

Orient

Other NDFIs Trust,

Finance, Motor

Finance, Consumer Finance, Money Broker

ACEM, SJTU, Nan Li