Quarantine diaries: The impact of COVID-19 in the Greek banking … · 2020. 7. 27. · in Greece...

24

Quarantine diaries: The impact of COVID-19 in the Greek banking sector and credit risk Athens, March 2020

Transcript of Quarantine diaries: The impact of COVID-19 in the Greek banking … · 2020. 7. 27. · in Greece...

Quarantine diaries:The impact of COVID-19 in the Greek banking sector and credit riskAthens, March 2020

Foreword

© 2020 Deloitte Central Mediterranean. All rights reserved.

“Οἱ ἄνθρωποι γνωρίζουν τὰ γινόμενα.Τὰ μέλλοντα γνωρίζουν οἱ θεοί,πλήρεις καὶ μόνοι κάτοχοι πάντων τῶν φώτων.Ἐκ τῶν μελλόντων οἱ σοφοὶ τὰ προσερχόμεναἀντιλαμβάνονται. Ἡ ἀκοὴαὐτῶν κάποτε ἐν ὥραις σοβαρῶν σπουδῶνταράττεται. Ἡ μυστικὴ βοὴτοὺς ἔρχεται τῶν πλησιαζόντων γεγονότων.Καὶ τὴν προσέχουν εὐλαβεῖς. Ἐνῶ εἰς τὴν ὁδὸνἔξω, οὐδὲν ἀκούουν οἱ λαοί”.

Σοφοί δέ προσιόντων, Κ. Π. Καβάφης

Since only few weeks ago, mankind is facing an unprecedented crisis with direct impacts on public health, way of living and economy. COVID-19 outbreak poses unprecedented challenges to human societies, policy makers, businesses and financial institutions across the globe.

This document is chiefly addressed to decision makers and banking practitioners although our hope is that it could serve as a point of reference to wider parts of the society. Its main purpose is to outline the main implications of the COVID-19 outbreak foreseen at this preliminary stage in the Greek banking sector with a focus on credit risk.

The disruption and implications of COVID-19 are already imminent in the society and economy. Rapidly changing social norms, restrictions on transportation, slowdown in the level of economic activity, possible disruptions in the supply chain, high degrees of volatility in the markets and shock in the market sentiment constitute some of the preliminary challenges to deal with. Responses from governments and regulators are intense but as the outbreak prompts high social and financial stakes with unknown outcomes at this moment, substantial adjustments and policy actions should still be expected in order to mitigate the impact of the disease in the global and domestic economies.

Despite the global nature of the outbreak, Greek banks are facing the challenge to deal with a new type of crisis after only a profound “small break” from a prolonged period of turbulence. In this context, decision makers and practitioners need to understand the implications of the outbreak caused as a result of COVID-19 and manage effectively the risks stemming from it in order to ensure resilience. At this moment no one can provide a reasonable estimate about how long the outbreak will last and as such timely responses are necessary.

With the aim to tread along these unfamiliar paths with confidence, holistic approaches are needed in order to mitigate the impact of this “black swan” event to the degree possible. If the common goal, is to preserve social and financial stability and resilience in this turbulent era, it is in our joint interest to help motivate all forces available to win this battle.

The impact of COVID-19 in the Greek banking sector and credit risk 2

Contents

© 2020 Deloitte Central Mediterranean. All rights reserved.

Foreword

01 | Background information

02 | Economic impact of COVID-19

03 | Regulatory response to address the challenges of COVID-19

04 | NPE target plan implications

05 | IFRS 9 ECL Measurement

06 | Impact on modelling practices

07 | Regulatory capital impact

08 | Appendix: Deloitte Contacts

The impact of COVID-19 in the Greek banking sector and credit risk 3

01. Background information

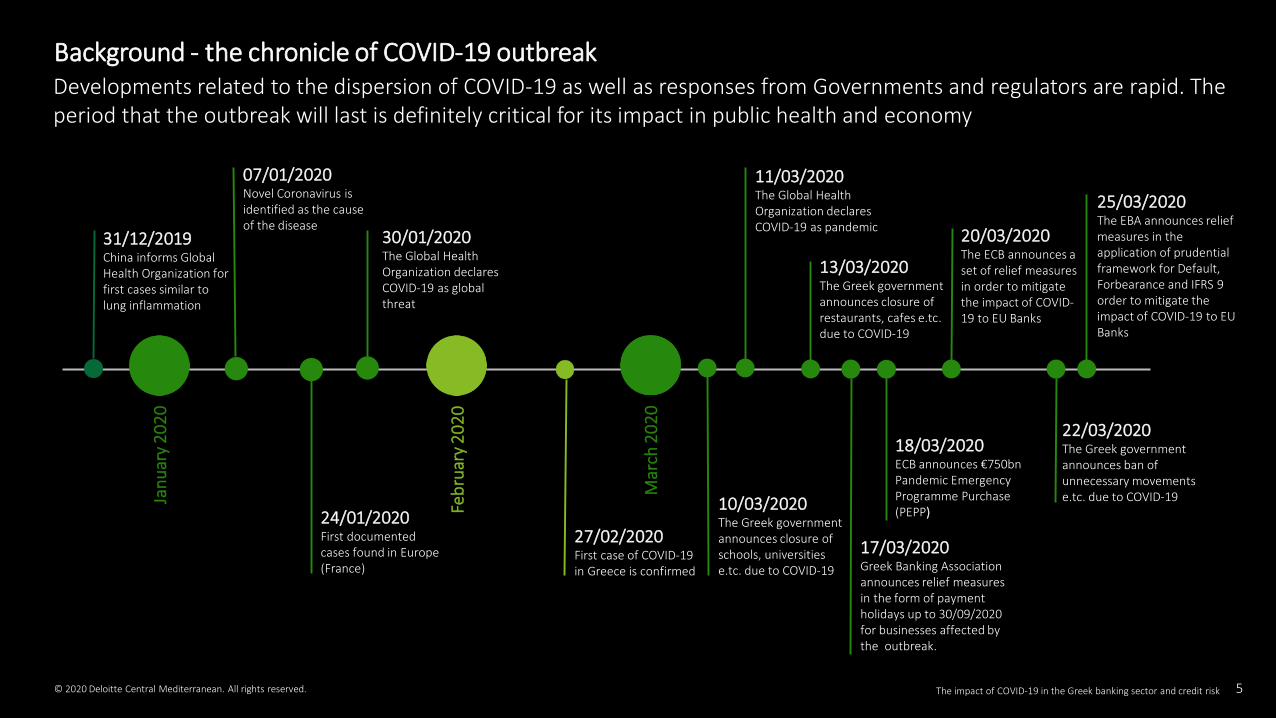

Background - the chronicle of COVID-19 outbreak

07/01/2020Novel Coronavirus is identified as the cause of the disease

24/01/2020First documented cases found in Europe (France)

31/12/2019China informs Global Health Organization for first cases similar to lung inflammation

20/03/2020The ECB announces a set of relief measures in order to mitigate the impact of COVID-19 to EU Banks

30/01/2020The Global Health Organization declares COVID-19 as global threat

27/02/2020First case of COVID-19 in Greece is confirmed

Jan

uar

y 2

02

0

Feb

ruar

y 2

02

0

Mar

ch 2

02

0

Developments related to the dispersion of COVID-19 as well as responses from Governments and regulators are rapid. The period that the outbreak will last is definitely critical for its impact in public health and economy

17/03/2020Greek Banking Association announces relief measures in the form of payment holidays up to 30/09/2020 for businesses affected by the outbreak.

11/03/2020The Global Health Organization declares COVID-19 as pandemic

10/03/2020The Greek government announces closure of schools, universities e.tc. due to COVID-19

13/03/2020The Greek government announces closure of restaurants, cafes e.tc. due to COVID-19

22/03/2020The Greek government announces ban of unnecessary movements e.tc. due to COVID-19

18/03/2020ECB announces €750bn Pandemic Emergency Programme Purchase (PEPP)

© 2020 Deloitte Central Mediterranean. All rights reserved.

25/03/2020The EBA announces relief measures in the application of prudential framework for Default, Forbearance and IFRS 9 order to mitigate the impact of COVID-19 to EU Banks

The impact of COVID-19 in the Greek banking sector and credit risk 5

China

France

Germany

Greece

Iran

Italy

Japan

Netherlands

Singapore

South Korea

Spain

Sweden

Switzerland

United Kingdom

USA

0

250

500

1,000

2,000

4,000

8,000

16,000

32,000

64,000

128,000

256,000

0 5 10 15 20 25 30 40 50 60 70

Days Since 100th Confirmed Case

Cum

ula

tive N

um

ber

of C

ases

Data as of 2/4/2020

Cumulative Cases from COVID-19, Selected Countries

1,000

10,000

50,000

250,000

0 20 40 60

days_elapsed

cu_cases

Greece

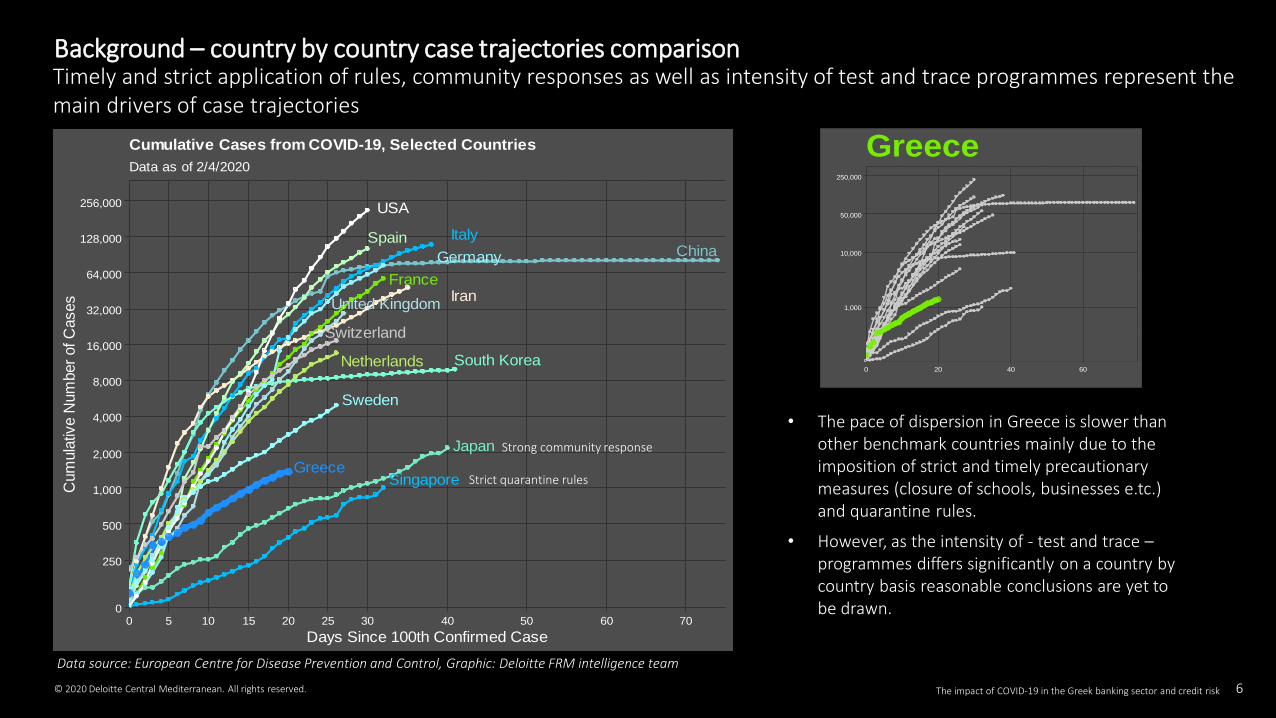

Background – country by country case trajectories comparisonTimely and strict application of rules, community responses as well as intensity of test and trace programmes represent the main drivers of case trajectories

© 2020 Deloitte Central Mediterranean. All rights reserved.

Data source: European Centre for Disease Prevention and Control, Graphic: Deloitte FRM intelligence team

Strict quarantine rules

Strong community response

• The pace of dispersion in Greece is slower than other benchmark countries mainly due to the imposition of strict and timely precautionary measures (closure of schools, businesses e.tc.) and quarantine rules.

• However, as the intensity of - test and trace –programmes differs significantly on a country by country basis reasonable conclusions are yet to be drawn.

The impact of COVID-19 in the Greek banking sector and credit risk 6

02. Economic impact of COVID-19

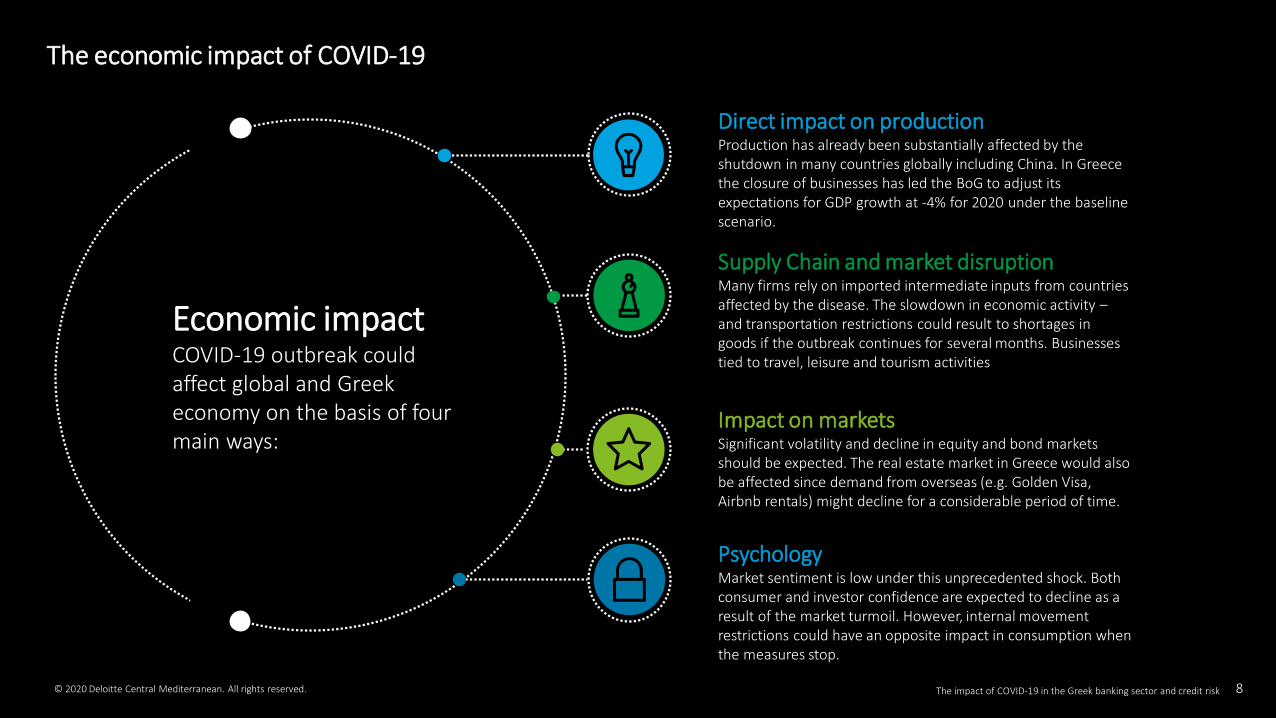

Economic impactCOVID-19 outbreak could affect global and Greek economy on the basis of four main ways:

Supply Chain and market disruptionMany firms rely on imported intermediate inputs from countries affected by the disease. The slowdown in economic activity –and transportation restrictions could result to shortages in goods if the outbreak continues for several months. Businesses tied to travel, leisure and tourism activities

Impact on marketsSignificant volatility and decline in equity and bond markets should be expected. The real estate market in Greece would also be affected since demand from overseas (e.g. Golden Visa, Airbnb rentals) might decline for a considerable period of time.

Direct impact on productionProduction has already been substantially affected by the shutdown in many countries globally including China. In Greece the closure of businesses has led the BoG to adjust its expectations for GDP growth at -4% for 2020 under the baseline scenario.

PsychologyMarket sentiment is low under this unprecedented shock. Both consumer and investor confidence are expected to decline as a result of the market turmoil. However, internal movement restrictions could have an opposite impact in consumption when the measures stop.

The economic impact of COVID-19

© 2020 Deloitte Central Mediterranean. All rights reserved. The impact of COVID-19 in the Greek banking sector and credit risk 8

03. Regulatory response to address the challenges of COVID-19

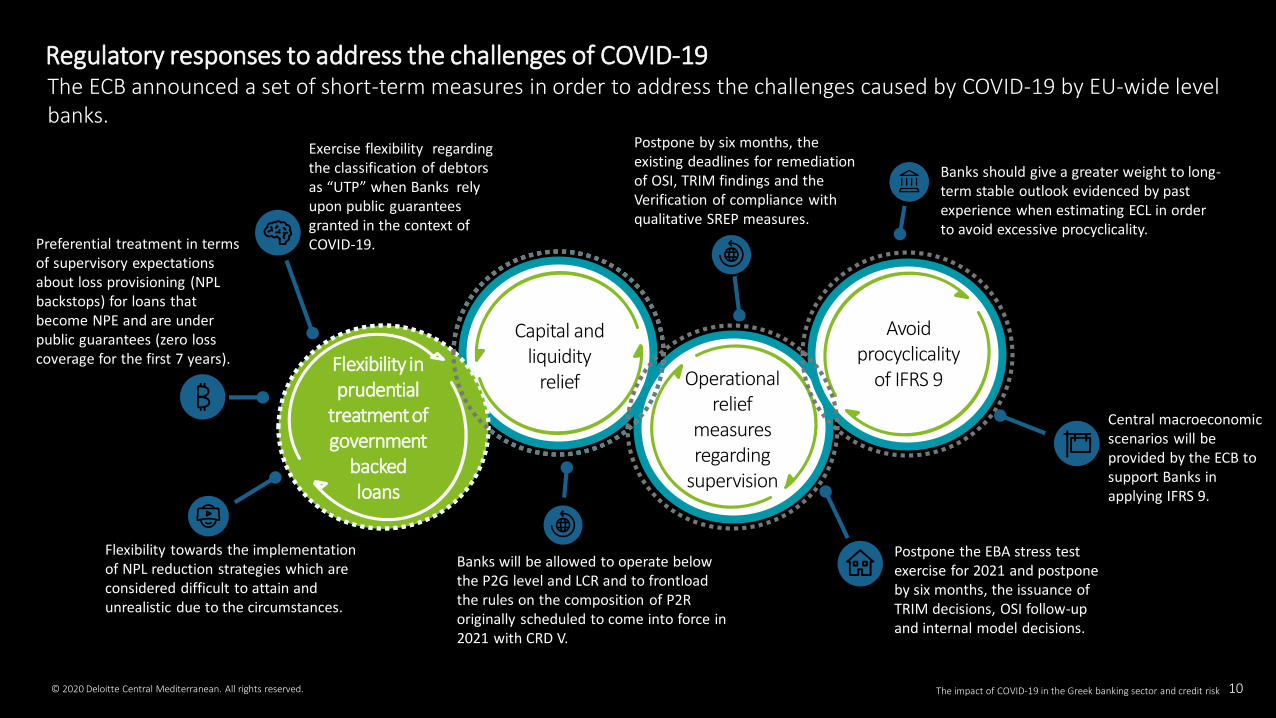

Regulatory responses to address the challenges of COVID-19

Flexibility in prudential

treatment of government

backed loans

Avoid procyclicality

of IFRS 9Operational relief

measures regarding

supervision

Capital and liquidity

relief

Postpone by six months, the existing deadlines for remediation of OSI, TRIM findings and the Verification of compliance with qualitative SREP measures.

Banks should give a greater weight to long-term stable outlook evidenced by past experience when estimating ECL in order to avoid excessive procyclicality.

Flexibility towards the implementation of NPL reduction strategies which are considered difficult to attain and unrealistic due to the circumstances.

Postpone the EBA stress test exercise for 2021 and postponeby six months, the issuance of TRIM decisions, OSI follow-up and internal model decisions.

Exercise flexibility regardingthe classification of debtors as “UTP” when Banks rely upon public guarantees granted in the context of COVID-19. Preferential treatment in terms

of supervisory expectations about loss provisioning (NPL backstops) for loans that become NPE and are under public guarantees (zero loss coverage for the first 7 years).

Central macroeconomic scenarios will be provided by the ECB to support Banks in applying IFRS 9.

Banks will be allowed to operate below the P2G level and LCR and to frontloadthe rules on the composition of P2R originally scheduled to come into force in 2021 with CRD V.

© 2020 Deloitte Central Mediterranean. All rights reserved.

The ECB announced a set of short-term measures in order to address the challenges caused by COVID-19 by EU-wide level banks.

The impact of COVID-19 in the Greek banking sector and credit risk 10

11

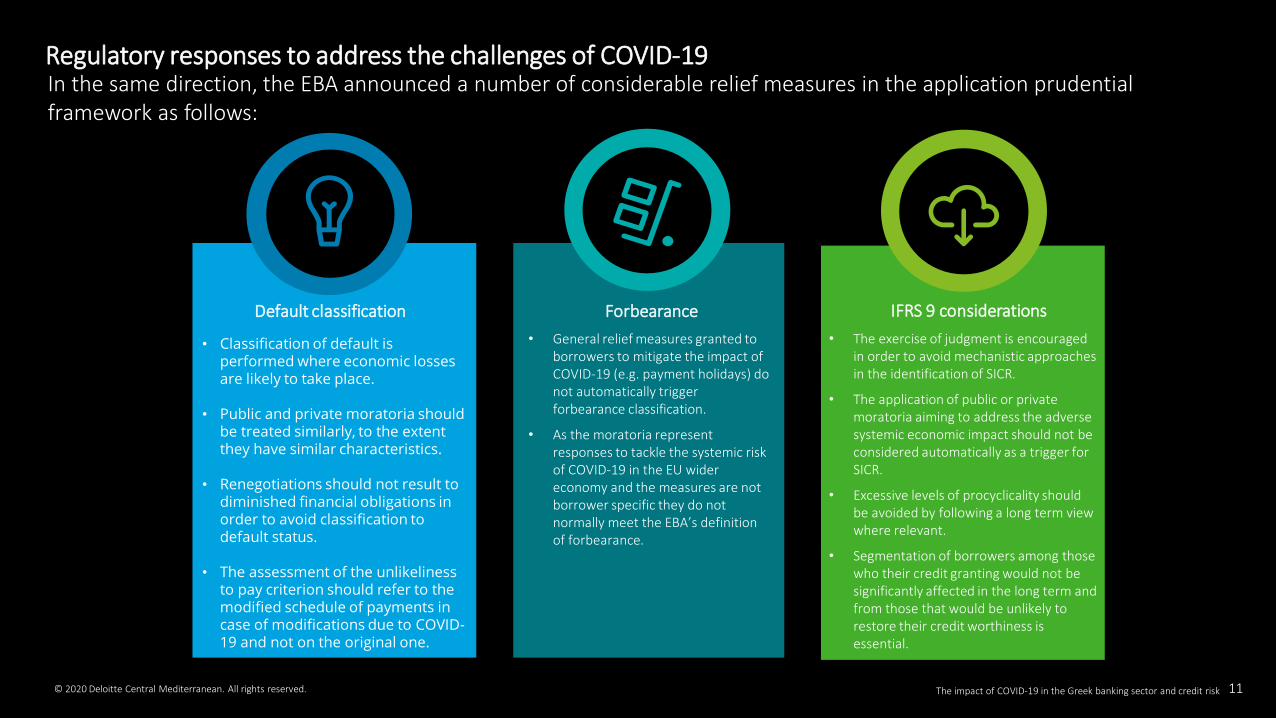

Regulatory responses to address the challenges of COVID-19In the same direction, the EBA announced a number of considerable relief measures in the application prudential framework as follows:

© 2020 Deloitte Central Mediterranean. All rights reserved.

• Classification of default is performed where economic losses are likely to take place.

• Public and private moratoria should be treated similarly, to the extent they have similar characteristics.

• Renegotiations should not result to diminished financial obligations in order to avoid classification to default status.

• The assessment of the unlikeliness to pay criterion should refer to the modified schedule of payments in case of modifications due to COVID-19 and not on the original one.

Default classification

• General relief measures granted to borrowers to mitigate the impact of COVID-19 (e.g. payment holidays) do not automatically trigger forbearance classification.

• As the moratoria represent responses to tackle the systemic risk of COVID-19 in the EU wider economy and the measures are not borrower specific they do not normally meet the EBA’s definition of forbearance.

Forbearance

• The exercise of judgment is encouraged in order to avoid mechanistic approaches in the identification of SICR.

• The application of public or private moratoria aiming to address the adverse systemic economic impact should not be considered automatically as a trigger for SICR.

• Excessive levels of procyclicality should be avoided by following a long term view where relevant.

• Segmentation of borrowers among those who their credit granting would not be significantly affected in the long term and from those that would be unlikely to restore their credit worthiness is essential.

IFRS 9 considerations

The impact of COVID-19 in the Greek banking sector and credit risk 11

12

Voice analytics

G/L Data Ingestion

Transaction data ingestion

Transaction data ingestion

Credit scenario and stress testing for deal structuring

Fraud alerts

Portfolio Management

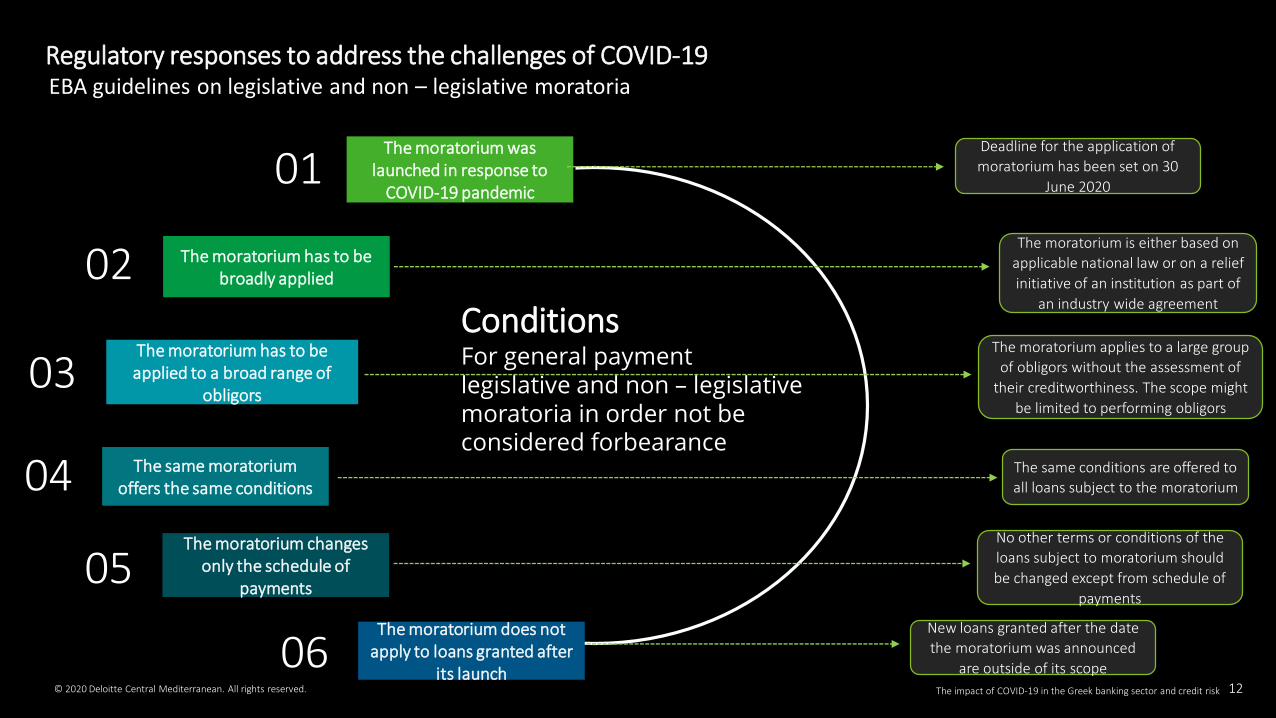

Regulatory responses to address the challenges of COVID-19EBA guidelines on legislative and non – legislative moratoria

© 2020 Deloitte Central Mediterranean. All rights reserved.

ConditionsFor general payment legislative and non – legislative moratoria in order not be considered forbearance

The moratorium was launched in response to

COVID-19 pandemic01

The moratorium has to be broadly applied02

The moratorium has to be applied to a broad range of

obligors03

The same moratorium offers the same conditions04

The moratorium changes only the schedule of

payments05

The moratorium does not apply to loans granted after

its launch06

Deadline for the application of

moratorium has been set on 30

June 2020

The moratorium is either based on

applicable national law or on a relief

initiative of an institution as part of

an industry wide agreement

The moratorium applies to a large group

of obligors without the assessment of

their creditworthiness. The scope might

be limited to performing obligors

The same conditions are offered to

all loans subject to the moratorium

No other terms or conditions of the

loans subject to moratorium should

be changed except from schedule of

payments

New loans granted after the date

the moratorium was announced

are outside of its scope

The impact of COVID-19 in the Greek banking sector and credit risk 12

13

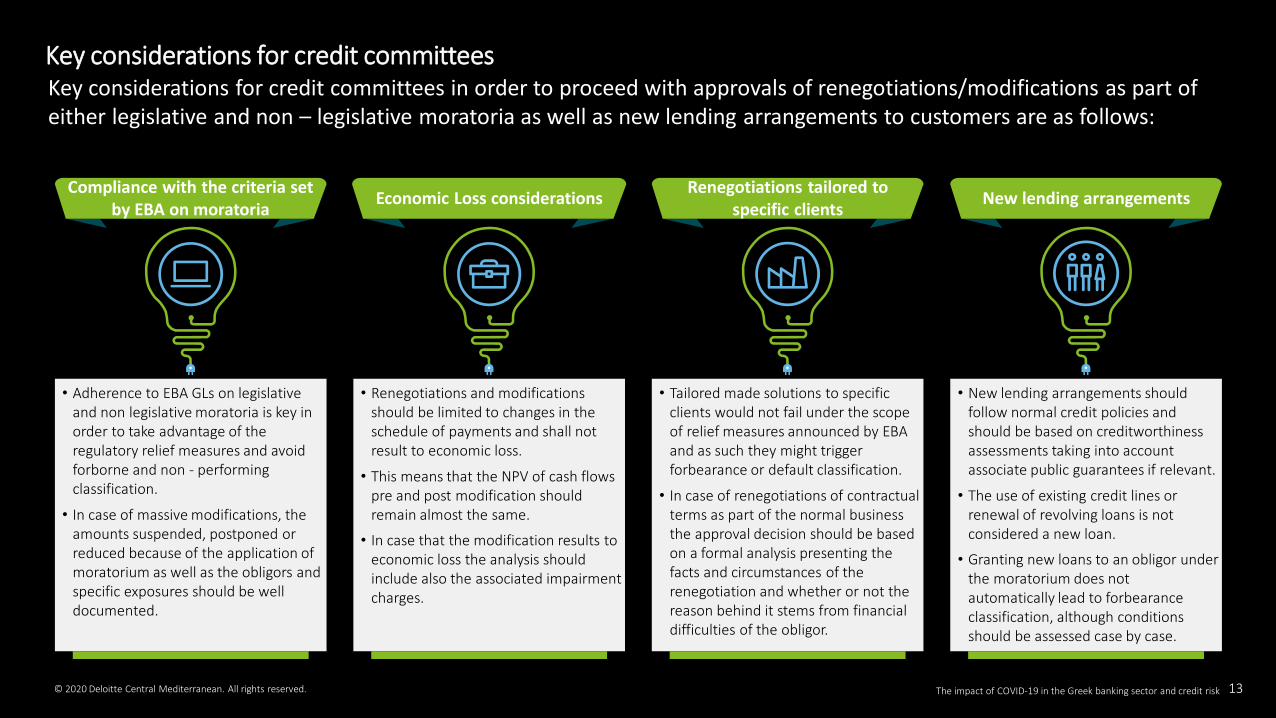

Key considerations for credit committeesKey considerations for credit committees in order to proceed with approvals of renegotiations/modifications as part of either legislative and non – legislative moratoria as well as new lending arrangements to customers are as follows:

© 2020 Deloitte Central Mediterranean. All rights reserved.

Compliance with the criteria set by EBA on moratoria

• Adherence to EBA GLs on legislative and non legislative moratoria is key in order to take advantage of the regulatory relief measures and avoid forborne and non - performing classification.

• In case of massive modifications, the amounts suspended, postponed or reduced because of the application of moratorium as well as the obligors and specific exposures should be well documented.

Economic Loss considerations

• Renegotiations and modifications should be limited to changes in the schedule of payments and shall not result to economic loss.

• This means that the NPV of cash flows pre and post modification should remain almost the same.

• In case that the modification results to economic loss the analysis should include also the associated impairment charges.

Renegotiations tailored to specific clients

• Tailored made solutions to specific clients would not fail under the scope of relief measures announced by EBA and as such they might trigger forbearance or default classification.

• In case of renegotiations of contractual terms as part of the normal business the approval decision should be based on a formal analysis presenting the facts and circumstances of the renegotiation and whether or not the reason behind it stems from financial difficulties of the obligor.

New lending arrangements

• New lending arrangements should follow normal credit policies and should be based on creditworthiness assessments taking into account associate public guarantees if relevant.

• The use of existing credit lines or renewal of revolving loans is not considered a new loan.

• Granting new loans to an obligor under the moratorium does not automatically lead to forbearance classification, although conditions should be assessed case by case.

The impact of COVID-19 in the Greek banking sector and credit risk 13

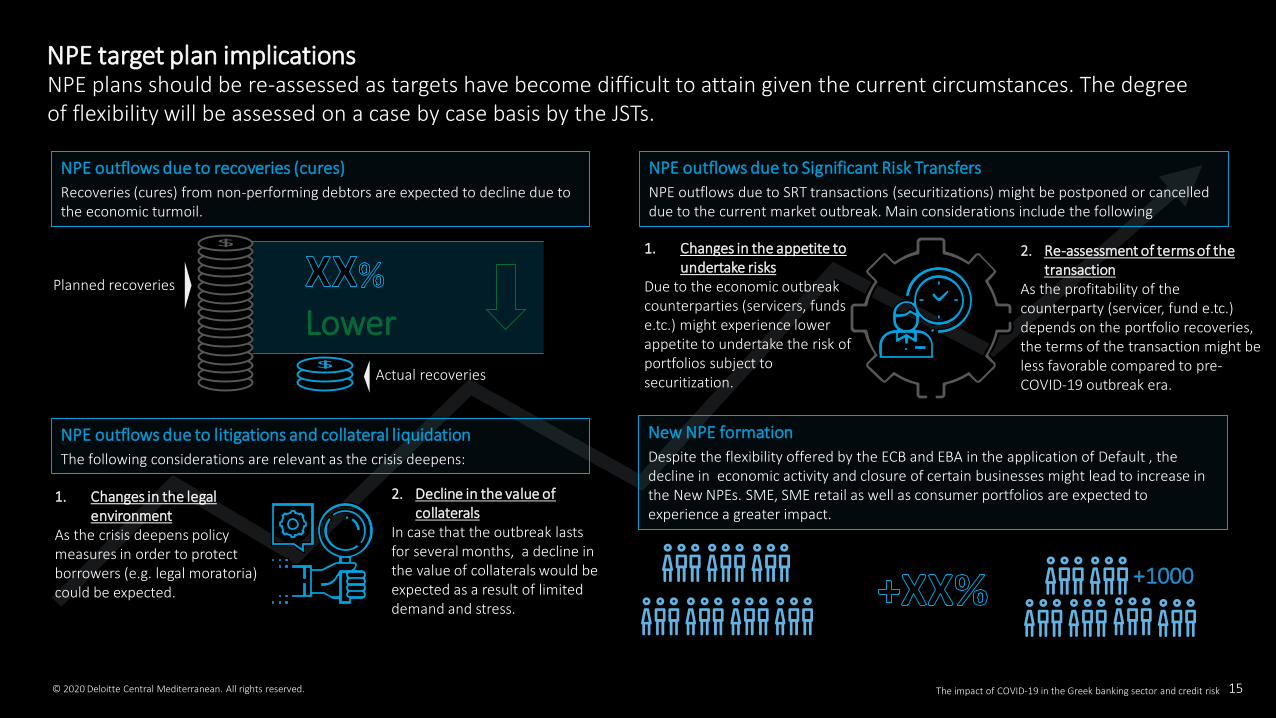

04. NPE target plan implications

Lower

NPE outflows due to recoveries (cures)

Recoveries (cures) from non-performing debtors are expected to decline due to the economic turmoil.

NPE outflows due to Significant Risk Transfers

NPE outflows due to SRT transactions (securitizations) might be postponed or cancelled due to the current market outbreak. Main considerations include the following

Planned recoveries

Actual recoveries

1. Changes in the appetite to undertake risks

Due to the economic outbreak counterparties (servicers, funds e.tc.) might experience lower appetite to undertake the risk of portfolios subject to securitization.

NPE outflows due to litigations and collateral liquidation

The following considerations are relevant as the crisis deepens:

New NPE formation

Despite the flexibility offered by the ECB and EBA in the application of Default , the decline in economic activity and closure of certain businesses might lead to increase in the New NPEs. SME, SME retail as well as consumer portfolios are expected to experience a greater impact.

+1000

NPE plans should be re-assessed as targets have become difficult to attain given the current circumstances. The degree of flexibility will be assessed on a case by case basis by the JSTs.

NPE target plan implications

2. Re-assessment of terms of the transaction

As the profitability of the counterparty (servicer, fund e.tc.) depends on the portfolio recoveries, the terms of the transaction might be less favorable compared to pre-COVID-19 outbreak era.

1. Changes in the legal environment

As the crisis deepens policy measures in order to protect borrowers (e.g. legal moratoria) could be expected.

2. Decline in the value of collaterals

In case that the outbreak lasts for several months, a decline in the value of collaterals would be expected as a result of limited demand and stress.

© 2020 Deloitte Central Mediterranean. All rights reserved. The impact of COVID-19 in the Greek banking sector and credit risk 15

05. IFRS 9 ECL Measurement

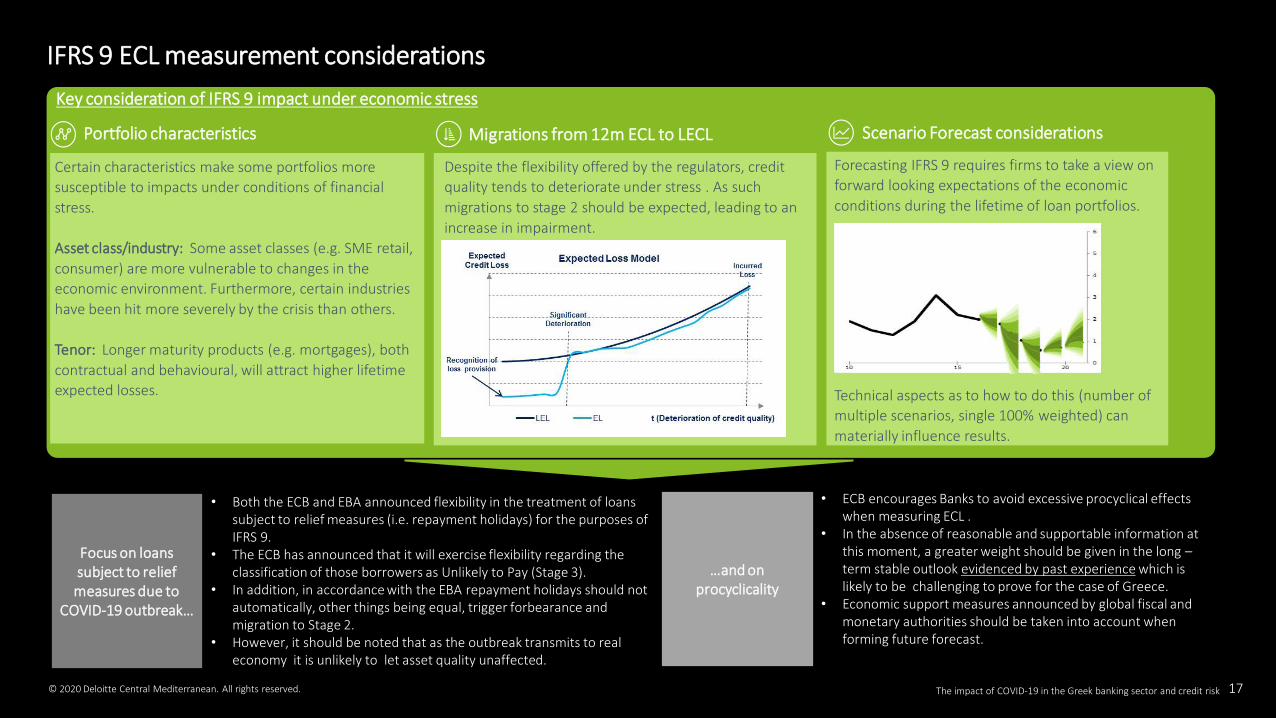

IFRS 9 ECL measurement considerations

Scenario Forecast considerations

Despite the flexibility offered by the regulators, credit

quality tends to deteriorate under stress . As such

migrations to stage 2 should be expected, leading to an

increase in impairment.

Migrations from 12m ECL to LECL

Key consideration of IFRS 9 impact under economic stress

Portfolio characteristics

Certain characteristics make some portfolios more

susceptible to impacts under conditions of financial

stress.

Asset class/industry: Some asset classes (e.g. SME retail,

consumer) are more vulnerable to changes in the

economic environment. Furthermore, certain industries

have been hit more severely by the crisis than others.

Tenor: Longer maturity products (e.g. mortgages), both

contractual and behavioural, will attract higher lifetime

expected losses.

Focus on loans subject to relief measures due to

COVID-19 outbreak…

…and on procyclicality

• Both the ECB and EBA announced flexibility in the treatment of loans subject to relief measures (i.e. repayment holidays) for the purposes of IFRS 9.

• The ECB has announced that it will exercise flexibility regarding the classification of those borrowers as Unlikely to Pay (Stage 3).

• In addition, in accordance with the EBA repayment holidays should not automatically, other things being equal, trigger forbearance and migration to Stage 2.

• However, it should be noted that as the outbreak transmits to real economy it is unlikely to let asset quality unaffected.

• ECB encourages Banks to avoid excessive procyclical effects when measuring ECL .

• In the absence of reasonable and supportable information at this moment, a greater weight should be given in the long –term stable outlook evidenced by past experience which is likely to be challenging to prove for the case of Greece.

• Economic support measures announced by global fiscal and monetary authorities should be taken into account when forming future forecast.

© 2020 Deloitte Central Mediterranean. All rights reserved.

Forecasting IFRS 9 requires firms to take a view on

forward looking expectations of the economic

conditions during the lifetime of loan portfolios.

Technical aspects as to how to do this (number of

multiple scenarios, single 100% weighted) can

materially influence results.

The impact of COVID-19 in the Greek banking sector and credit risk 17

06. Impact on modelling practices

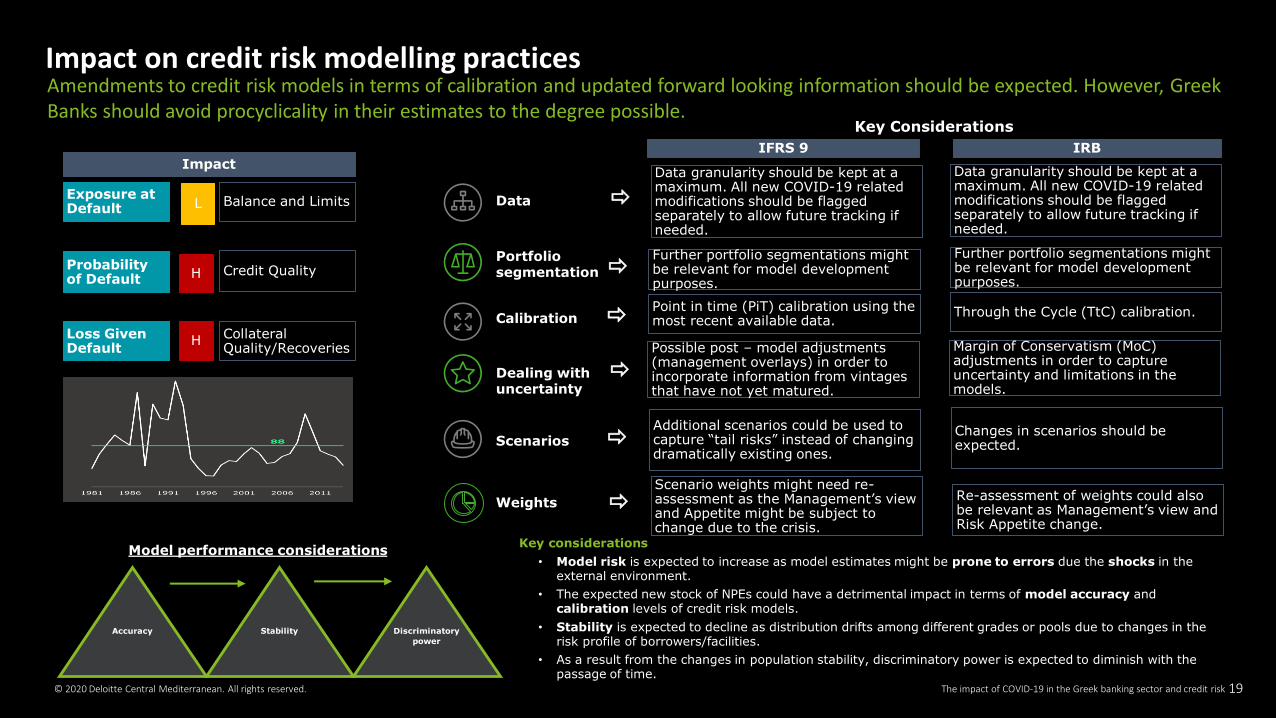

Amendments to credit risk models in terms of calibration and updated forward looking information should be expected. However, Greek Banks should avoid procyclicality in their estimates to the degree possible.

Impact on credit risk modelling practices

Loss Given Default

Probability of Default

Exposure at Default

Additional scenarios could be used to capture “tail risks” instead of changing dramatically existing ones.

Possible post – model adjustments (management overlays) in order to incorporate information from vintages that have not yet matured.

Point in time (PiT) calibration using the most recent available data.

Key Considerations

Collateral Quality/Recoveries

Credit Quality

Balance and LimitsL

H

Impact

H

IFRS 9 IRB

Changes in scenarios should be expected.

Margin of Conservatism (MoC) adjustments in order to capture uncertainty and limitations in the models.

Through the Cycle (TtC) calibration.

Scenario weights might need re-assessment as the Management’s view and Appetite might be subject to change due to the crisis.

Re-assessment of weights could also be relevant as Management’s view and Risk Appetite change.

Accuracy Stability Discriminatory

power

Model performance considerations Key considerations

• Model risk is expected to increase as model estimates might be prone to errors due the shocks in the external environment.

• The expected new stock of NPEs could have a detrimental impact in terms of model accuracy and calibration levels of credit risk models.

• Stability is expected to decline as distribution drifts among different grades or pools due to changes in the risk profile of borrowers/facilities.

• As a result from the changes in population stability, discriminatory power is expected to diminish with the passage of time.

© 2020 Deloitte Central Mediterranean. All rights reserved. The impact of COVID-19 in the Greek banking sector and credit risk

Data granularity should be kept at a maximum. All new COVID-19 related modifications should be flagged separately to allow future tracking if needed.

Data granularity should be kept at a maximum. All new COVID-19 related modifications should be flagged separately to allow future tracking if needed.

Further portfolio segmentations might be relevant for model development purposes.

Further portfolio segmentations might be relevant for model development purposes.

Scenarios

Portfolio segmentation

Calibration

Dealing with uncertainty

Weights

Data

19

07. Regulatory capital impact

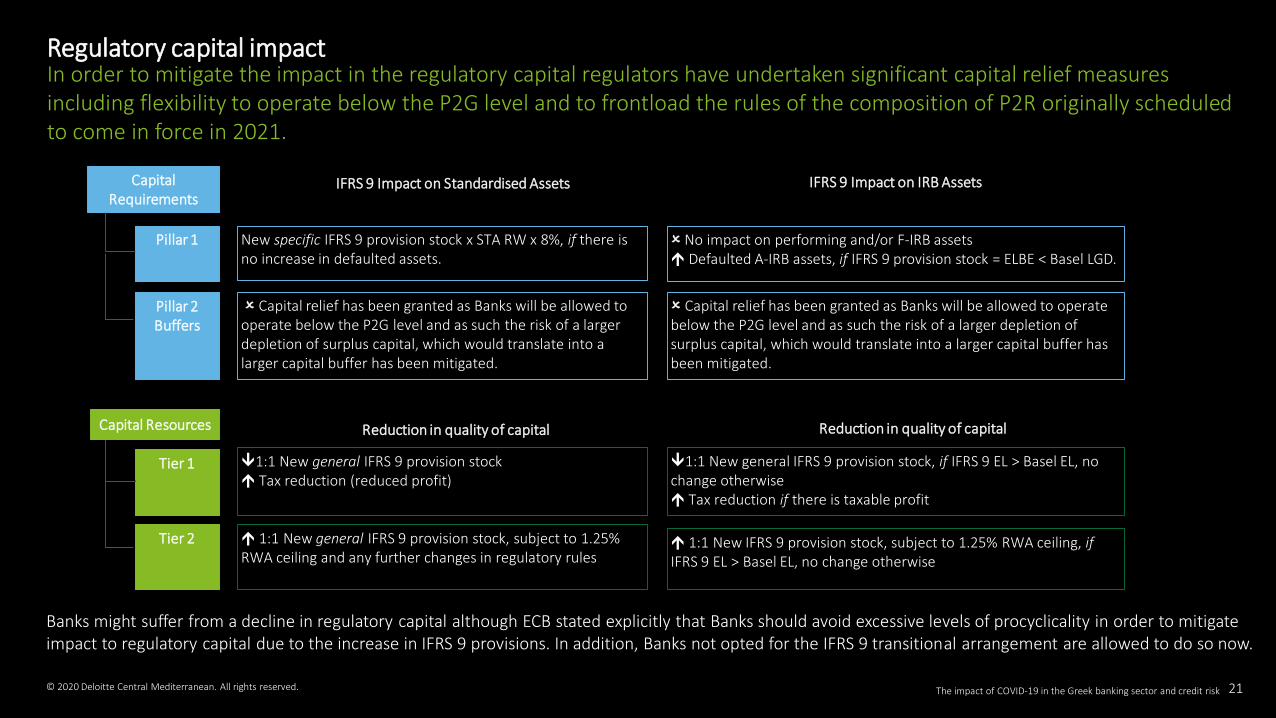

Regulatory capital impact

IFRS 9 Impact on Standardised AssetsCapital Requirements

Pillar 1

Pillar 2 Buffers

Tier 1

Tier 2

New specific IFRS 9 provision stock x STA RW x 8%, if there is no increase in defaulted assets.

Capital relief has been granted as Banks will be allowed to operate below the P2G level and as such the risk of a larger depletion of surplus capital, which would translate into a larger capital buffer has been mitigated.

1:1 New general IFRS 9 provision stock Tax reduction (reduced profit)

1:1 New general IFRS 9 provision stock, subject to 1.25% RWA ceiling and any further changes in regulatory rules

Reduction in quality of capital

No impact on performing and/or F-IRB assets Defaulted A-IRB assets, if IFRS 9 provision stock = ELBE < Basel LGD.

Capital relief has been granted as Banks will be allowed to operate below the P2G level and as such the risk of a larger depletion of surplus capital, which would translate into a larger capital buffer has been mitigated.

1:1 New general IFRS 9 provision stock, if IFRS 9 EL > Basel EL, no change otherwise Tax reduction if there is taxable profit

1:1 New IFRS 9 provision stock, subject to 1.25% RWA ceiling, ifIFRS 9 EL > Basel EL, no change otherwise

Reduction in quality of capital

IFRS 9 Impact on IRB Assets

Capital Resources

Banks might suffer from a decline in regulatory capital although ECB stated explicitly that Banks should avoid excessive levels of procyclicality in order to mitigate impact to regulatory capital due to the increase in IFRS 9 provisions. In addition, Banks not opted for the IFRS 9 transitional arrangement are allowed to do so now.

In order to mitigate the impact in the regulatory capital regulators have undertaken significant capital relief measures including flexibility to operate below the P2G level and to frontload the rules of the composition of P2R originally scheduled to come in force in 2021.

© 2020 Deloitte Central Mediterranean. All rights reserved. The impact of COVID-19 in the Greek banking sector and credit risk 21

08. Appendix: Deloitte Contacts

Deloitte Contacts

© 2020 Deloitte Central Mediterranean. All rights reserved.

Alithia Diakatos

Partner, RA Leader, RA

+30 210 6781176

Alexandra Kostara

Partner, FSI Leader, A&A

+30 210 6781152

Spyridon Bisisidis

FRM Director, RA

+30 213 0881434

Serafim Papaioannou

Senior Manager, RA

+30 213 0881920

George Goutsos

Manager, RA

+30 210 6781170

Alexandros Karagiannidis

Senior Manager, RA

+30 210 6781358

The impact of COVID-19 in the Greek banking sector and credit risk 23

This document has been prepared by Deloitte Business Solutions Societe Anonyme of Business Consultants, Deloitte Certified Public Accountants Societe Anonyme, Deloitte Business Process Solutions Single Member Societe Anonyme for the Provision of Accounting Services and Deloitte Alexander Competence Center Single Member Societe Anonyme of Business Consultants.

Deloitte Business Solutions Societe Anonyme of Business Consultants, a Greek company, registered in Greece with registered number 000665201000 and its registered office at Marousi Attika, 3a Fragkokklisias & Granikou str., 151 25, Deloitte Certified Public Accountants Societe Anonyme, a Greek company, registered in Greece with registered number 0001223601000 and its registered office at Marousi-Attica, 3a Fragkokklisias & Granikou str., 151 25, Deloitte Business Process Solutions Single Member Societe Anonyme for the Provision of Accounting Services, a Greek company, registered in Greece with registered number 0009622801000 and its registered office at Marousi Attica, 3a Fragkokklisias & Granikou str., 151 25 and Deloitte Alexander Competence Center Single Member Societe Anonyme of Business Consultants, a Greek company, registered in Greece with registered number 144724504000 and its registered office at Thessaloniki, Municipality of Pylaia -Chortiatis of Thessaloniki, Vepe Technopolis Thessaloniki (5th and 3rd street), are one of the Deloitte Central Mediterranean S.r.l. (“DCM”) Countries. DCM, a company limited by guarantee registered in Italy with registered number 09599600963 and its registered office at Via Tortona no. 25, 20144, Milan, Italy is one of the Deloitte NSE LLP Geographies. Deloitte NSE LLP is a UK limited liability partnership and member firm of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”).

DTTL and each of its member firms are legally separate and independent entities. DTTL, Deloitte NSE LLP and Deloitte Central Mediterranean S.r.l. do not provide services to clients. Please see www.deloitte.com/about to learn more about our global network of member firms.

This document and its contents are confidential and prepared solely for your use, and may not be reproduced, redistributed or passed on to any other person in whole or in part, unless otherwise expressly agreed with you. No other party is entitled to rely on this document for any purpose whatsoever and we accept no liability to any other party, who is provided with or obtains access or relies to this document.

© 2020 Deloitte Central Mediterranean. All rights reserved.

![Estimating and Simulating a [-3pt] SIRD Model of COVID-19 ...chadj/Covid/NH-ExtendedResults2.pdfEstimating and Simulating a SIRD Model of COVID-19 for Many Countries, States, and Cities](https://static.fdocument.org/doc/165x107/5eda14a1b3745412b570ba7c/estimating-and-simulating-a-3pt-sird-model-of-covid-19-chadjcovidnh-extendedresults2pdf.jpg)

![Estimating and Simulating a [-3pt] SIRD Model of COVID-19 for [ …chadj/Covid/PER-Extended... · 2020. 10. 11. · Apr May Jun Jul Aug Sep Oct 2020 0 5 10 15 20 25 Daily deaths per](https://static.fdocument.org/doc/165x107/6117ff1ed974933d761bb603/estimating-and-simulating-a-3pt-sird-model-of-covid-19-for-chadjcovidper-extended.jpg)

![Estimating and Simulating a [-3pt] SIRD Model of COVID-19 ...chadj/Covid/ITA-Extended...(Light bars = New York City, for comparison) 22/39 Italy: Re-Opening (α =0) Mar Apr May Jun](https://static.fdocument.org/doc/165x107/5f929326211bb32fd856a912/estimating-and-simulating-a-3pt-sird-model-of-covid-19-chadjcovidita-extended.jpg)