A Concise Summary of @RISK Probability Distribution Functions

75

A Concise Summary of @RISK Probability Distribution Functions Copyright 2002 Palisade Corporation All Rights Reserved

Transcript of A Concise Summary of @RISK Probability Distribution Functions

A Concise Summary of @RISK Probability Distribution Functions

Copyright 2002 Palisade Corporation

All Rights Reserved

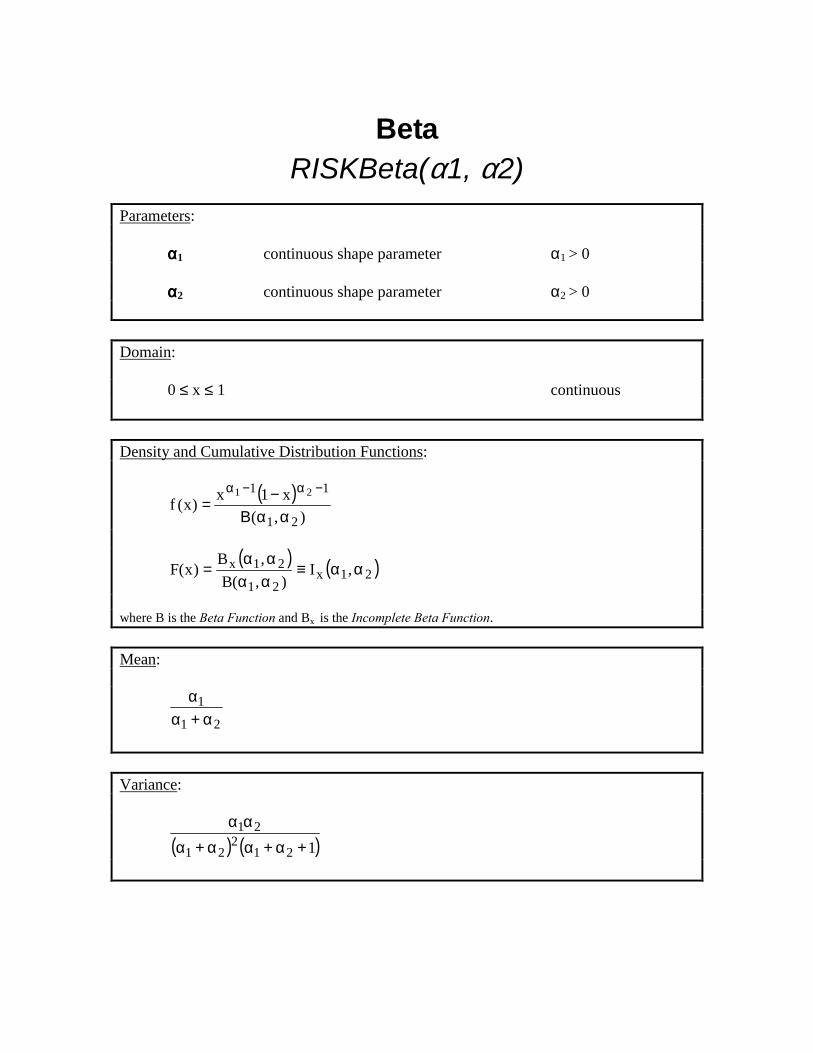

Beta RISKBeta(α1, α2)

Parameters: αααα1 continuous shape parameter α1 > 0 αααα2 continuous shape parameter α2 > 0 Domain: 0 ≤ x ≤ 1 continuous

Density and Cumulative Distribution Functions:

( )),(

x1x)x(f21

11 21

ααΒ−=

−α−α

( ) ( )21x21

21x ,I),(B

,B)x(F αα≡

αααα

=

where B is the Beta Function and Bx is the Incomplete Beta Function. Mean:

21

1α+α

α

Variance:

( ) ( )1212

21

21

+α+αα+ααα

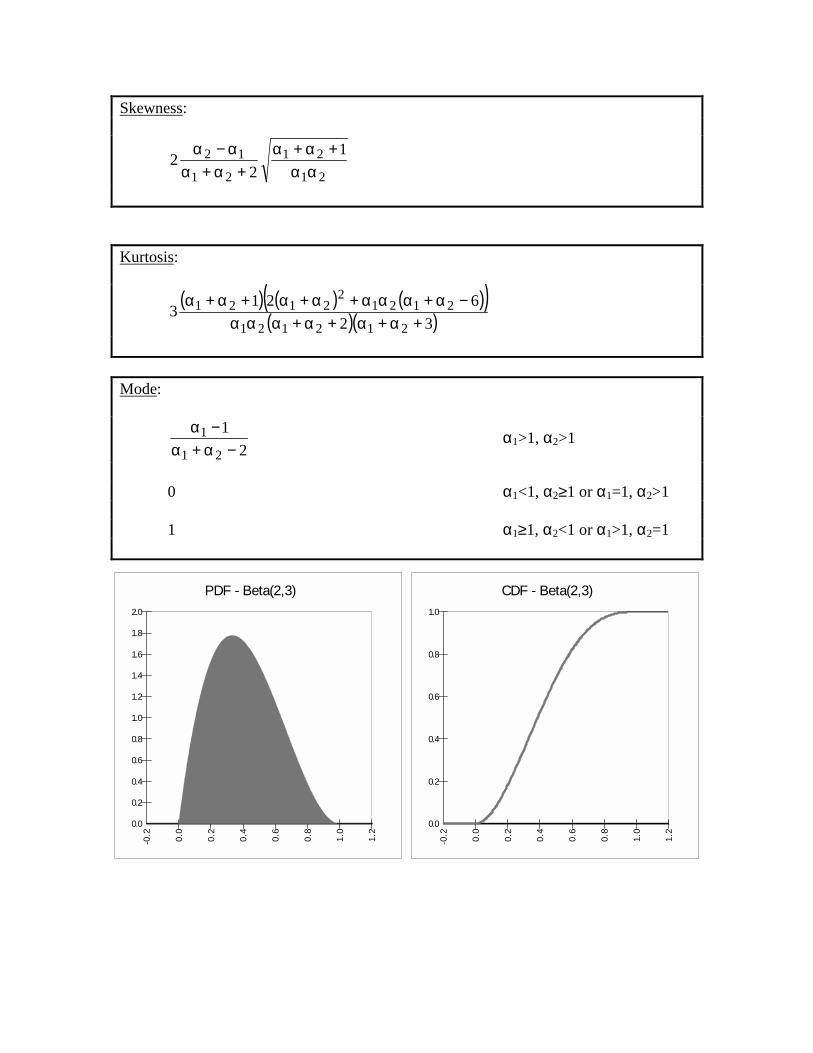

Skewness:

21

21

21

12 12

2αα

+α+α+α+α

α−α

Kurtosis:

( ) ( ) ( )( )

( )( )32621

3212121

21212

2121+α+α+α+ααα

−α+ααα+α+α+α+α

Mode:

21

21

1−α+α

−α α1>1, α2>1

0 α1<1, α2≥1 or α1=1, α2>1 1 α1≥1, α2<1 or α1>1, α2=1

PDF - Beta(2,3)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

-0.2 0.0

0.2

0.4

0.6

0.8

1.0

1.2

CDF - Beta(2,3)

0.0

0.2

0.4

0.6

0.8

1.0

-0.2 0.0

0.2

0.4

0.6

0.8

1.0

1.2

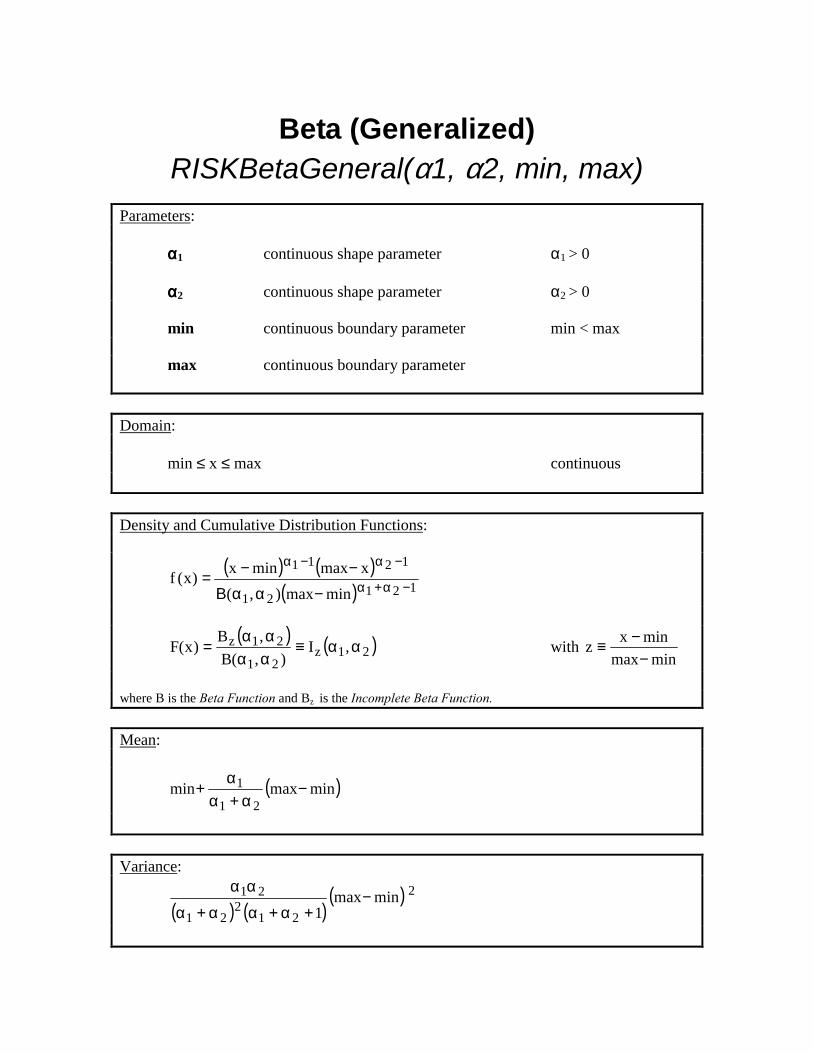

Beta (Generalized) RISKBetaGeneral(α1, α2, min, max)

Parameters: αααα1 continuous shape parameter α1 > 0 αααα2 continuous shape parameter α2 > 0 min continuous boundary parameter min < max max continuous boundary parameter

Domain: min ≤ x ≤ max continuous

Density and Cumulative Distribution Functions:

( ) ( )( ) 12121

1211

minmax),(xmaxminx)x(f −α+α

−α−α

−ααΒ−−=

( ) ( )21z21

21z ,I),(B

,B)x(F αα≡

αααα

= with minmax

minxz−

−≡

where B is the Beta Function and Bz is the Incomplete Beta Function. Mean:

( )minmaxmin21

1 −α+α

α+

Variance:

( ) ( )( ) 2

212

21

21 minmax1

−+α+αα+α

αα

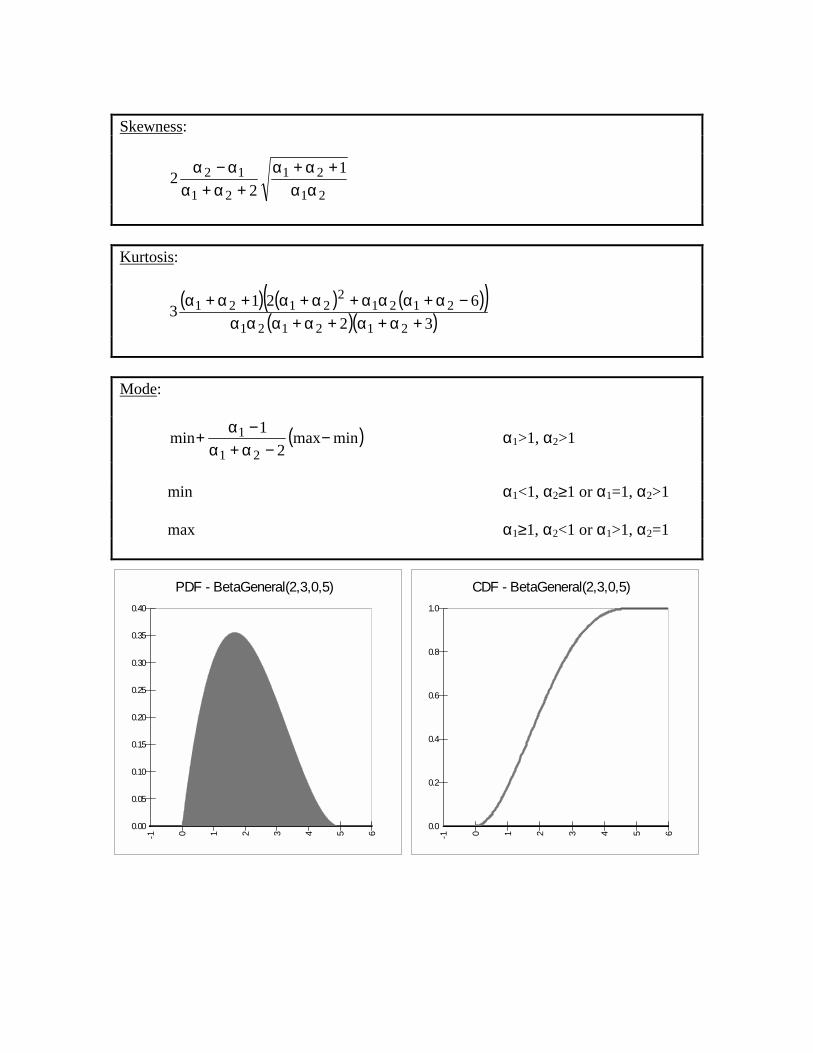

Skewness:

21

21

21

12 12

2αα

+α+α+α+α

α−α

Kurtosis:

( ) ( ) ( )( )

( )( )32621

3212121

21212

2121+α+α+α+ααα

−α+ααα+α+α+α+α

Mode:

( )minmax2

1min

21

1 −−α+α

−α+ α1>1, α2>1

min α1<1, α2≥1 or α1=1, α2>1 max α1≥1, α2<1 or α1>1, α2=1

PDF - BetaGeneral(2,3,0,5)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

-1 0 1 2 3 4 5 6

CDF - BetaGeneral(2,3,0,5)

0.0

0.2

0.4

0.6

0.8

1.0

-1 0 1 2 3 4 5 6

Beta (Subjective) RISKBetaSubj(min, m.likely, mean, max)

Definitions:

2maxminmid +≡

( )( )( )( )minmaxlikely.mmean

likely.mmidminmean21 −−−−≡α

minmeanmeanmax

12 −−α≡α

Parameters: min continuous boundary parameter min < max m.likely continuous parameter min < m.likely < max mean continuous parameter min < mean < max max continuous boundary parameter mean > mid if m.likely > mean mean < mid if m.likely < mean mean = mid if m.likely = mean Domain: min ≤ x ≤ max continuous Density and Cumulative Distribution Functions:

( ) ( )( ) 12121

1211

minmax),(xmaxminx)x(f −α+α

−α−α

−ααΒ−−=

( ) ( )21z21

21z ,I),(B

,B)x(F αα≡

αααα

= with minmax

minxz−

−≡

where B is the Beta Function and Bz is the Incomplete Beta Function.

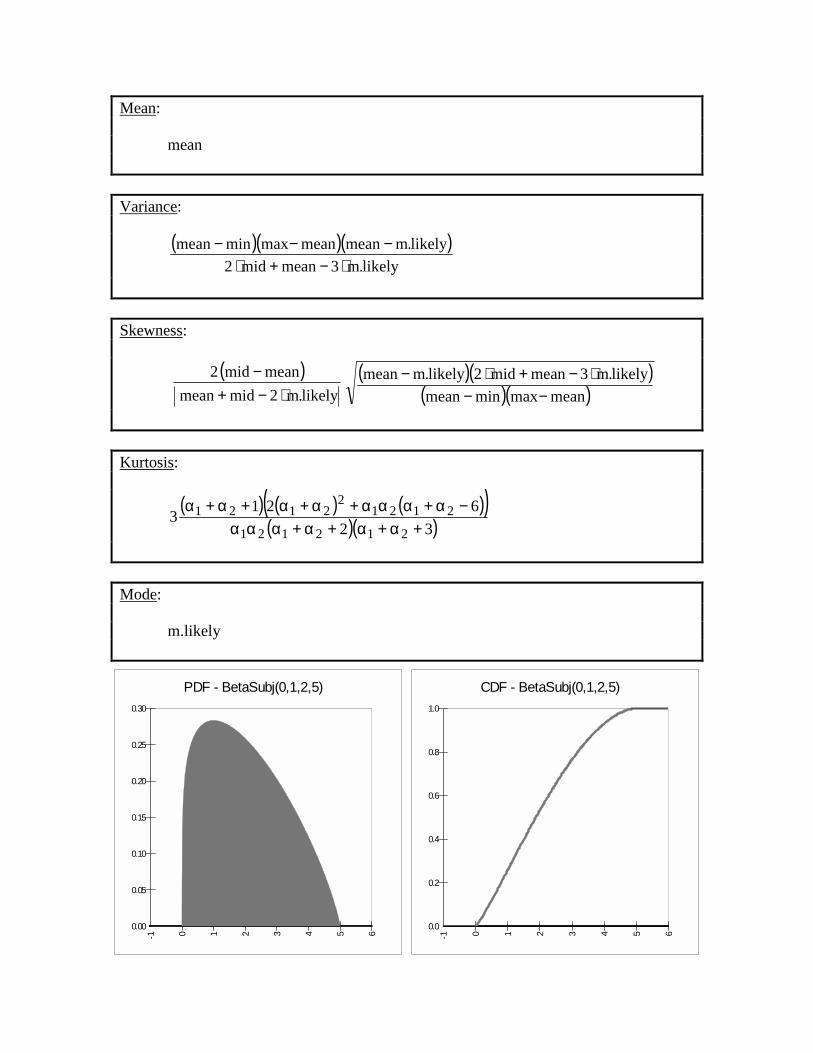

Mean:

mean Variance:

( )( )( )likely.m3meanmid2

likely.mmeanmeanmaxminmean⋅−+⋅

−−−

Skewness:

( ) ( )( )( )( )meanmaxminmean

likely.m3meanmid2likely.mmeanlikely.m2midmean

meanmid2−−

⋅−+⋅−⋅−+

−

Kurtosis:

( ) ( ) ( )( )

( )( )32621

3212121

21212

2121+α+α+α+ααα

−α+ααα+α+α+α+α

Mode: m.likely

PDF - BetaSubj(0,1,2,5)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

-1 0 1 2 3 4 5 6

CDF - BetaSubj(0,1,2,5)

0.0

0.2

0.4

0.6

0.8

1.0

-1 0 1 2 3 4 5 6

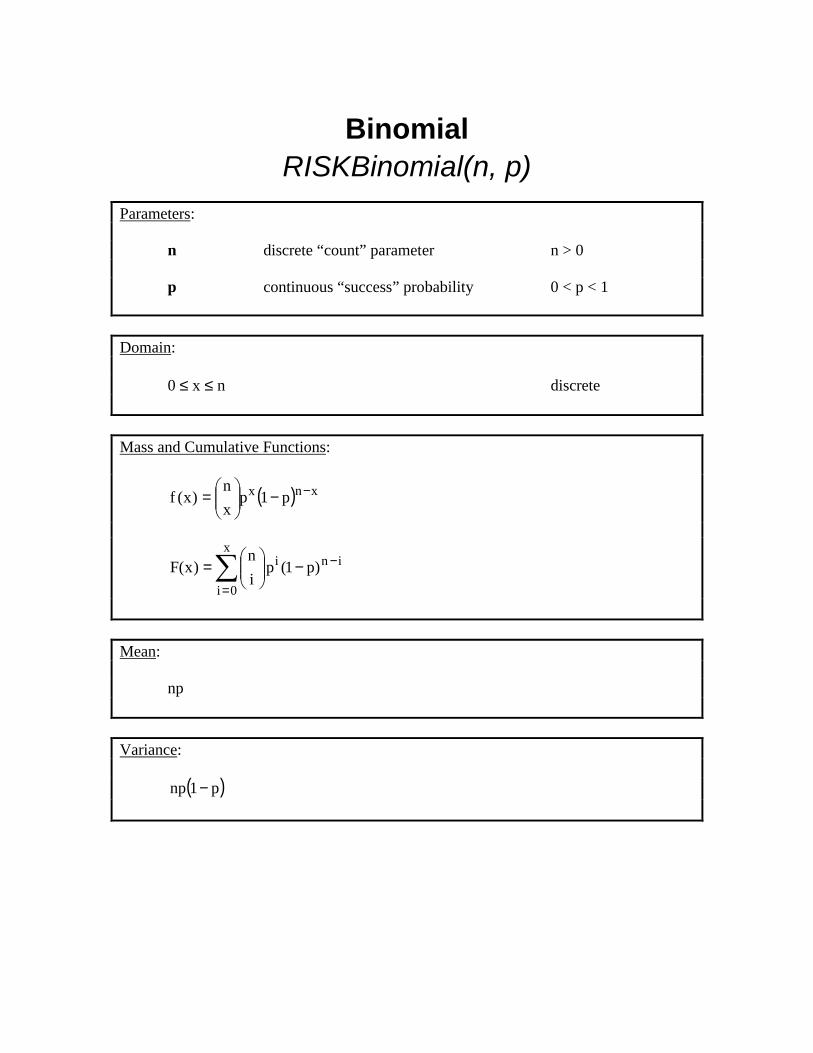

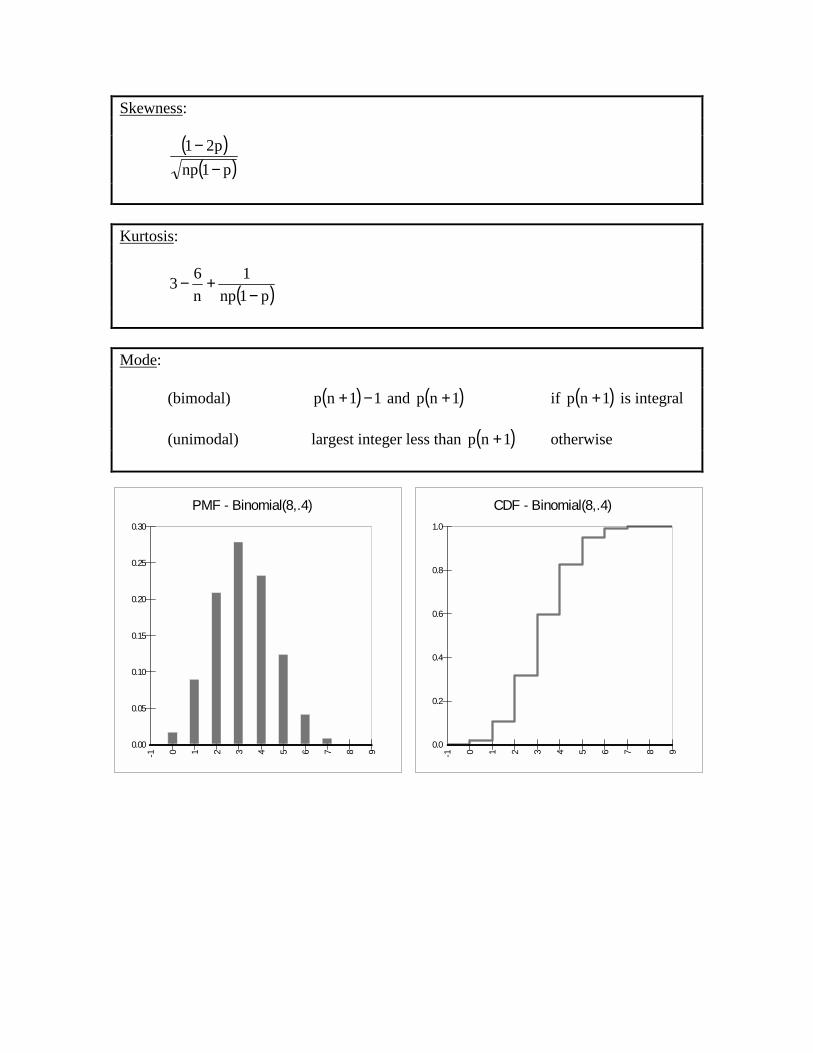

Binomial RISKBinomial(n, p)

Parameters: n discrete “count” parameter n > 0 p continuous “success” probability 0 < p < 1 Domain: 0 ≤ x ≤ n discrete

Mass and Cumulative Functions:

( ) xnx p1pxn

)x(f −−

=

inix

0i

)p1(pin

)x(F −

=

−

=∑

Mean:

np

Variance:

( )p1np −

Skewness:

( )( )p1np

p21−

−

Kurtosis:

( )p1np1

n63

−+−

Mode:

(bimodal) ( ) 11np −+ and ( )1np + if ( )1np + is integral (unimodal) largest integer less than ( )1np + otherwise

PMF - Binomial(8,.4)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

-1 0 1 2 3 4 5 6 7 8 9

CDF - Binomial(8,.4)

0.0

0.2

0.4

0.6

0.8

1.0

-1 0 1 2 3 4 5 6 7 8 9

Chi-Squared RISKChiSq(ν)

Parameters: νννν discrete shape parameter ν > 0 Domain: 0 ≤ x ≤ +∞ continuous

Density and Cumulative Functions:

( )

( ) 122x2 xe

221)x(f −ν−

ν νΓ=

( )

( )22

)x(F 2x

νΓ

νΓ=

where Γ is the Gamma Function, and Γx is the Incomplete Gamma Function. Mean:

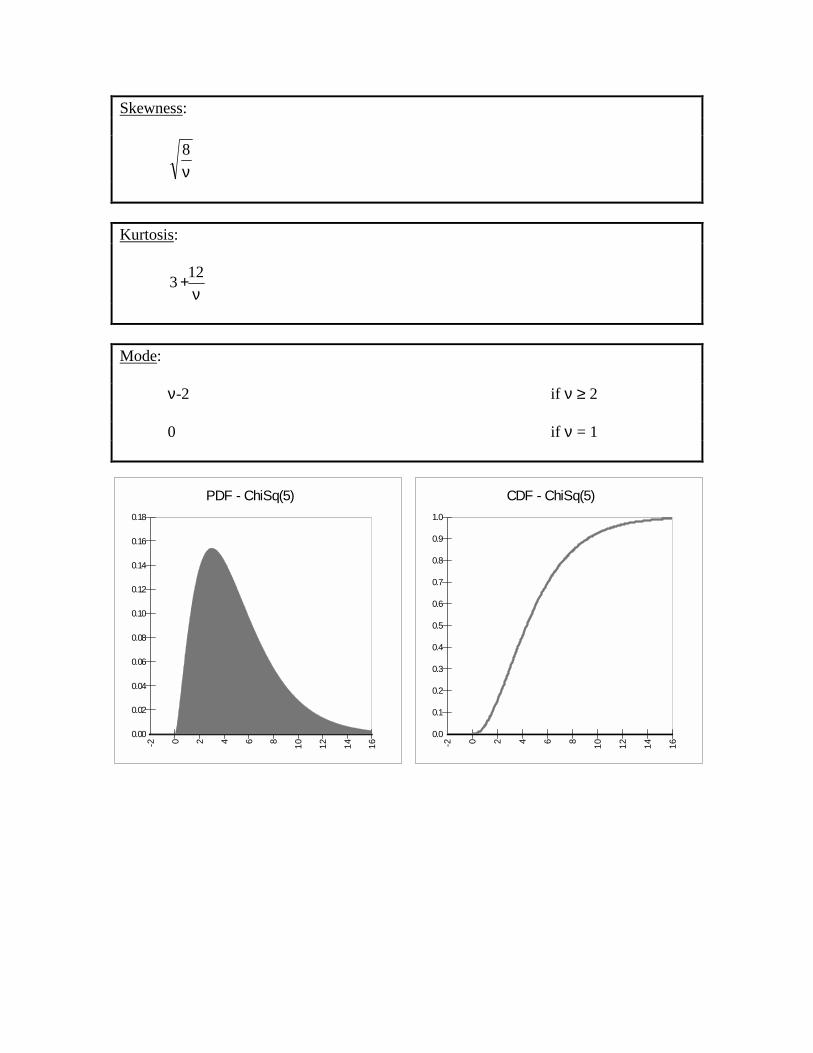

ν Variance:

2ν

Skewness:

ν8

Kurtosis:

ν+123

Mode:

ν-2 if ν ≥ 2 0 if ν = 1

PDF - ChiSq(5)

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

-2 0 2 4 6 8 10 12 14 16

CDF - ChiSq(5)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-2 0 2 4 6 8 10 12 14 16

Cumulative (Ascending) RISKCumul(min, max, {x}, {p})

Parameters: min continuous parameter min < max max continuous parameter {x} = {x1, x2, …, xN} array of continuous parameters min ≤ xi ≤ max {p} = {p1, p2, …, pN} array of continuous parameters 0 ≤ pi ≤ 1 Domain: min ≤ x ≤ max continuous

Density and Cumulative Functions:

i1i

i1ixxpp

)x(f−−

=+

+ for xi ≤ x < xi+1

( )

−

−−+=

++

i1i

ii1ii xx

xxppp)x(F for xi ≤ x ≤ xi+1

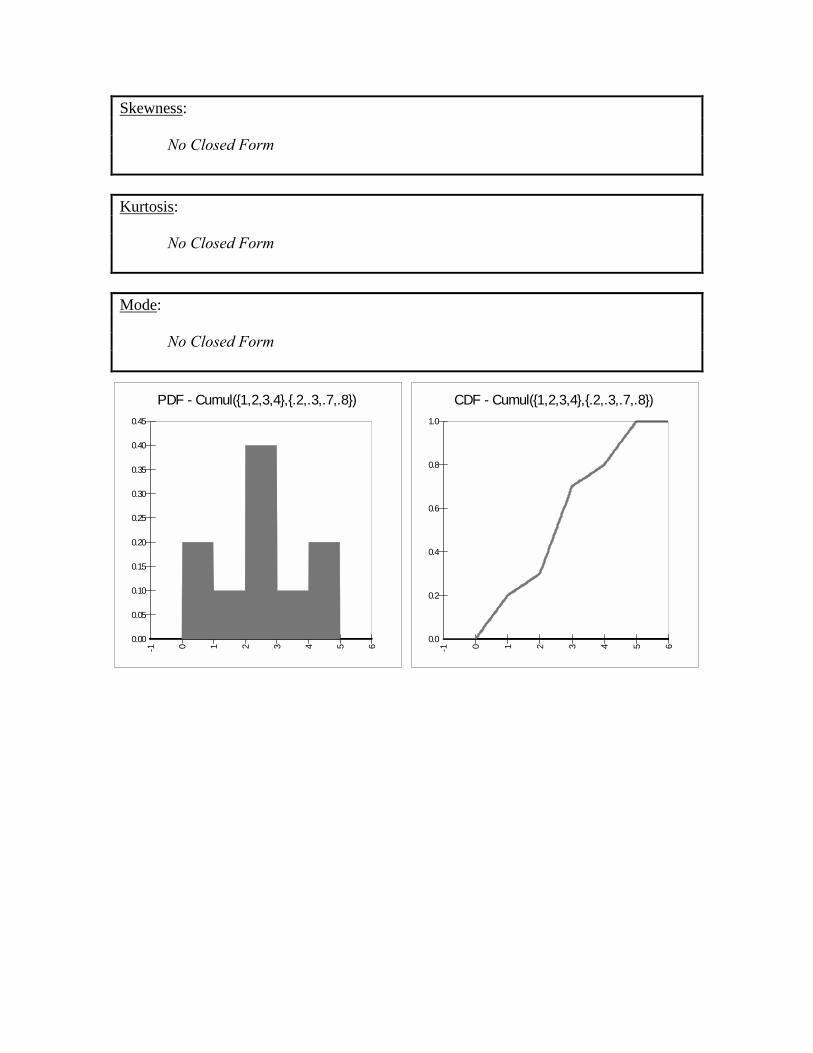

With the assumptions: 1. The arrays are ordered from left to right 2. The i index runs from 0 to N+1, with two extra elements : x0 ≡ min, p0 ≡ 0 and xN+1 ≡ max, pN+1 ≡ 1. Mean: No Closed Form Variance: No Closed Form

Skewness:

No Closed Form

Kurtosis:

No Closed Form Mode:

No Closed Form

CDF - Cumul({1,2,3,4},{.2,.3,.7,.8})

0.0

0.2

0.4

0.6

0.8

1.0

-1 0 1 2 3 4 5 6

PDF - Cumul({1,2,3,4},{.2,.3,.7,.8})

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

-1 0 1 2 3 4 5 6

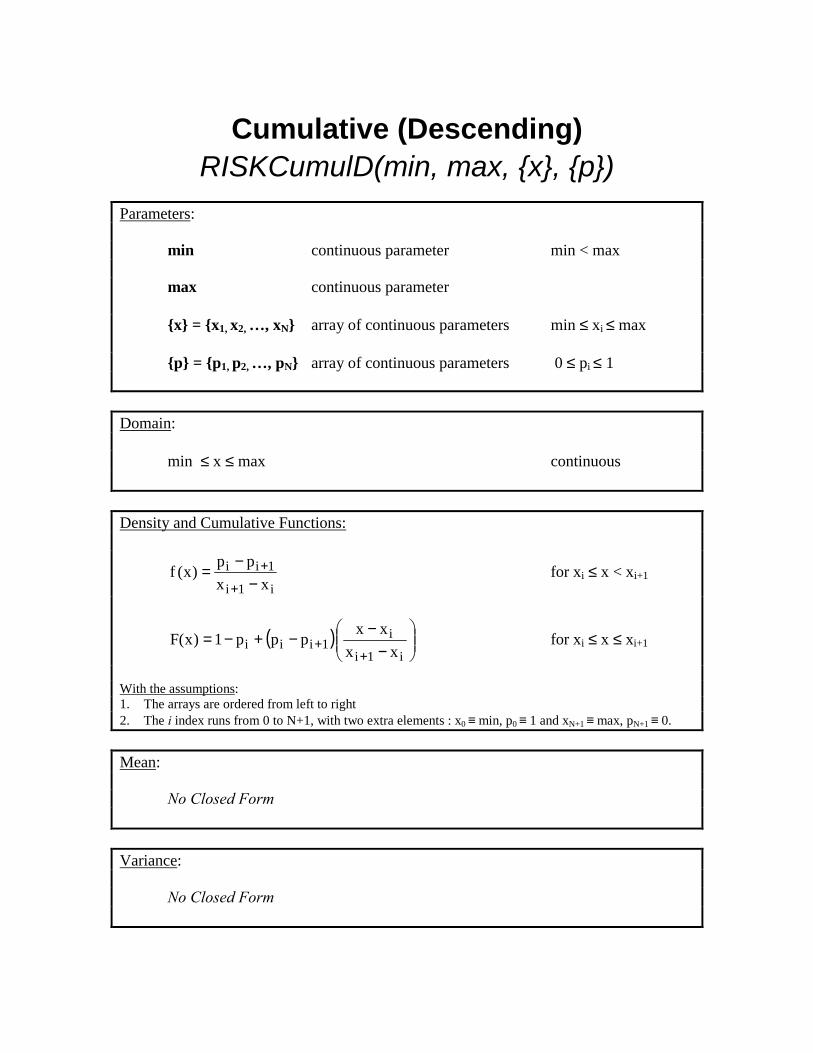

Cumulative (Descending) RISKCumulD(min, max, {x}, {p})

Parameters: min continuous parameter min < max max continuous parameter {x} = {x1, x2, …, xN} array of continuous parameters min ≤ xi ≤ max {p} = {p1, p2, …, pN} array of continuous parameters 0 ≤ pi ≤ 1 Domain: min ≤ x ≤ max continuous

Density and Cumulative Functions:

i1i

1iixx

pp)x(f

−−

=+

+ for xi ≤ x < xi+1

( )

−

−−+−=

++

i1i

i1iii xx

xxppp1)x(F for xi ≤ x ≤ xi+1

With the assumptions: 1. The arrays are ordered from left to right 2. The i index runs from 0 to N+1, with two extra elements : x0 ≡ min, p0 ≡ 1 and xN+1 ≡ max, pN+1 ≡ 0. Mean: No Closed Form Variance: No Closed Form

Skewness:

No Closed Form

Kurtosis:

No Closed Form Mode:

No Closed Form

PDF - CumulD({1,2,3,4},{.2,.3,.7,.8})

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

-1 0 1 2 3 4 5 6

CDF - CumulD({1,2,3,4},{.2,.3,.7,.8})

0.0

0.2

0.4

0.6

0.8

1.0

-1 0 1 2 3 4 5 6

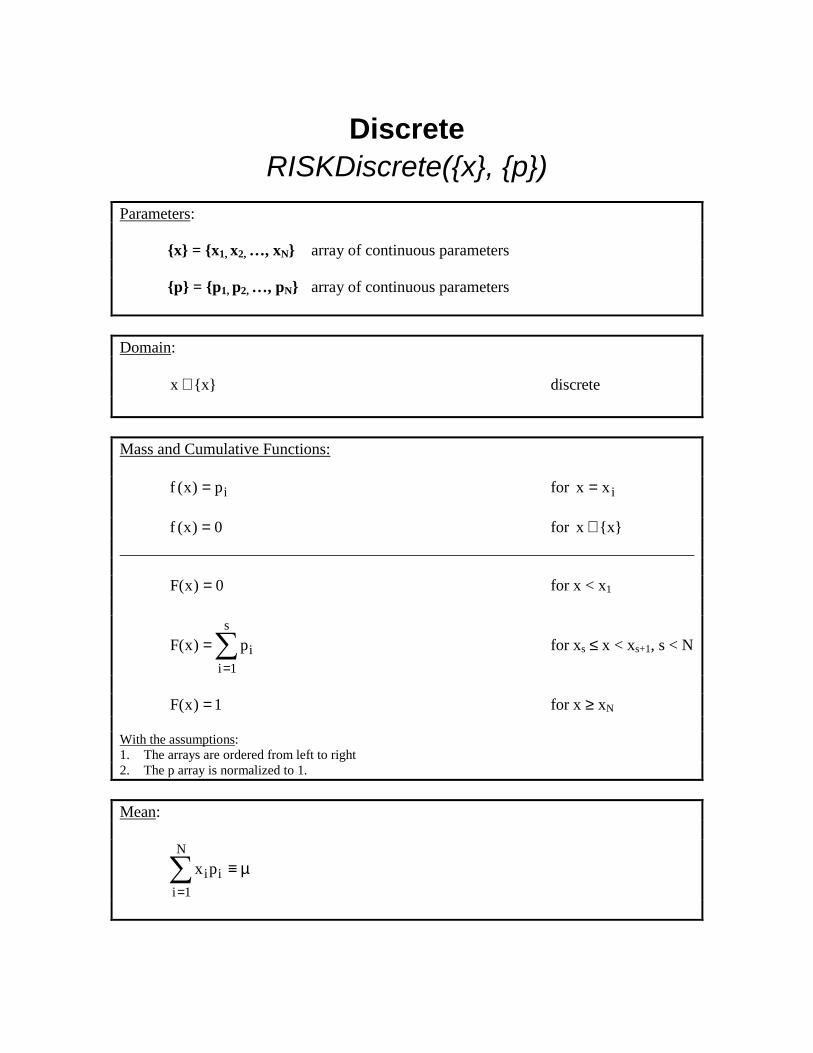

Discrete RISKDiscrete({x}, {p})

Parameters: {x} = {x1, x2, …, xN} array of continuous parameters {p} = {p1, p2, …, pN} array of continuous parameters Domain: }x{x ∈ discrete

Mass and Cumulative Functions: ip)x(f = for ixx = 0)x(f = for }x{x ∉

0)x(F = for x < x1

∑=

=s

1iip)x(F for xs ≤ x < xs+1, s < N

1)x(F = for x ≥ xN

With the assumptions: 1. The arrays are ordered from left to right 2. The p array is normalized to 1. Mean:

µ≡∑=

i

N

1iipx

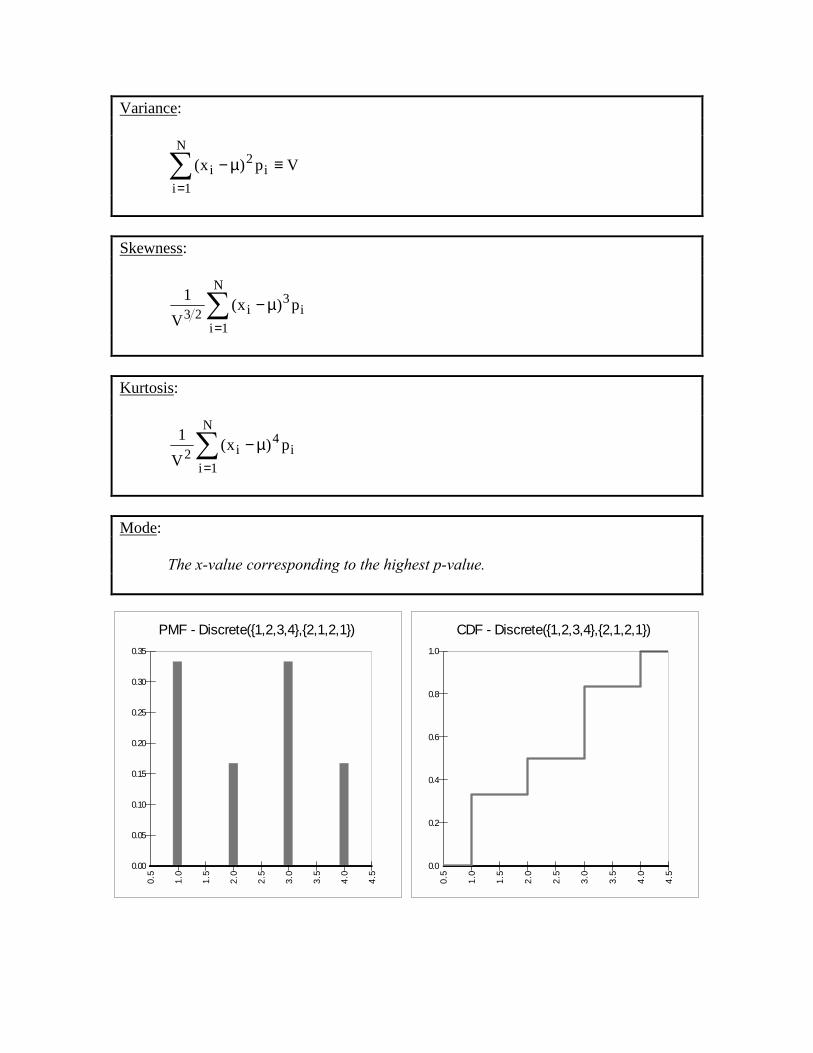

Variance:

Vp)x( i2

N

1ii ≡µ−∑

=

Skewness:

i3

N

1ii23 p)x(

V1 ∑

=

µ−

Kurtosis:

i4

N

1ii2 p)x(

V1 ∑

=

µ−

Mode: The x-value corresponding to the highest p-value.

CDF - Discrete({1,2,3,4},{2,1,2,1})

0.0

0.2

0.4

0.6

0.8

1.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

PMF - Discrete({1,2,3,4},{2,1,2,1})

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

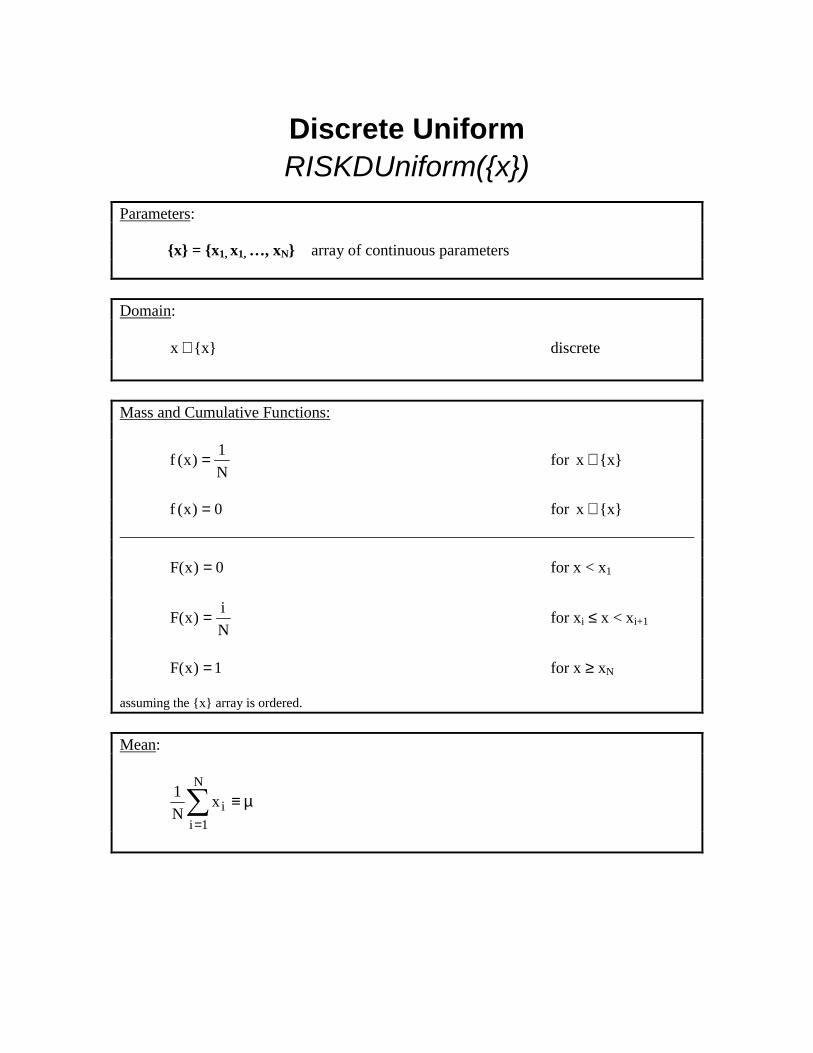

Discrete Uniform RISKDUniform({x})

Parameters: {x} = {x1, x1, …, xN} array of continuous parameters Domain: }x{x ∈ discrete

Mass and Cumulative Functions:

N1)x(f = for }x{x ∈

0)x(f = for }x{x ∉

0)x(F = for x < x1

Ni)x(F = for xi ≤ x < xi+1

1)x(F = for x ≥ xN

assuming the {x} array is ordered. Mean:

µ≡∑=

N

1iix

N1

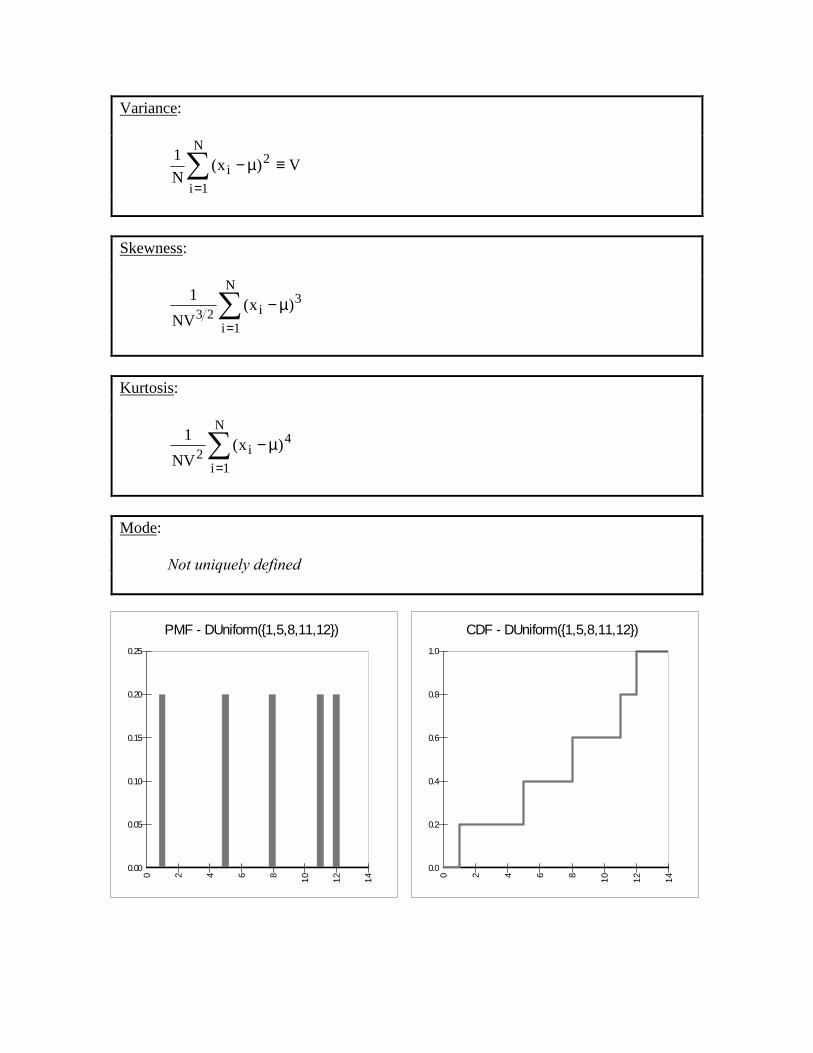

Variance:

V)x(N1 2

N

1ii ≡µ−∑

=

Skewness:

3N

1ii23 )x(

NV1 ∑

=

µ−

Kurtosis:

4N

1ii2 )x(

NV1 ∑

=

µ−

Mode: Not uniquely defined

PMF - DUniform({1,5,8,11,12})

0.00

0.05

0.10

0.15

0.20

0.25

0 2 4 6 8 10 12 14

CDF - DUniform({1,5,8,11,12})

0.0

0.2

0.4

0.6

0.8

1.0

0 2 4 6 8 10 12 14

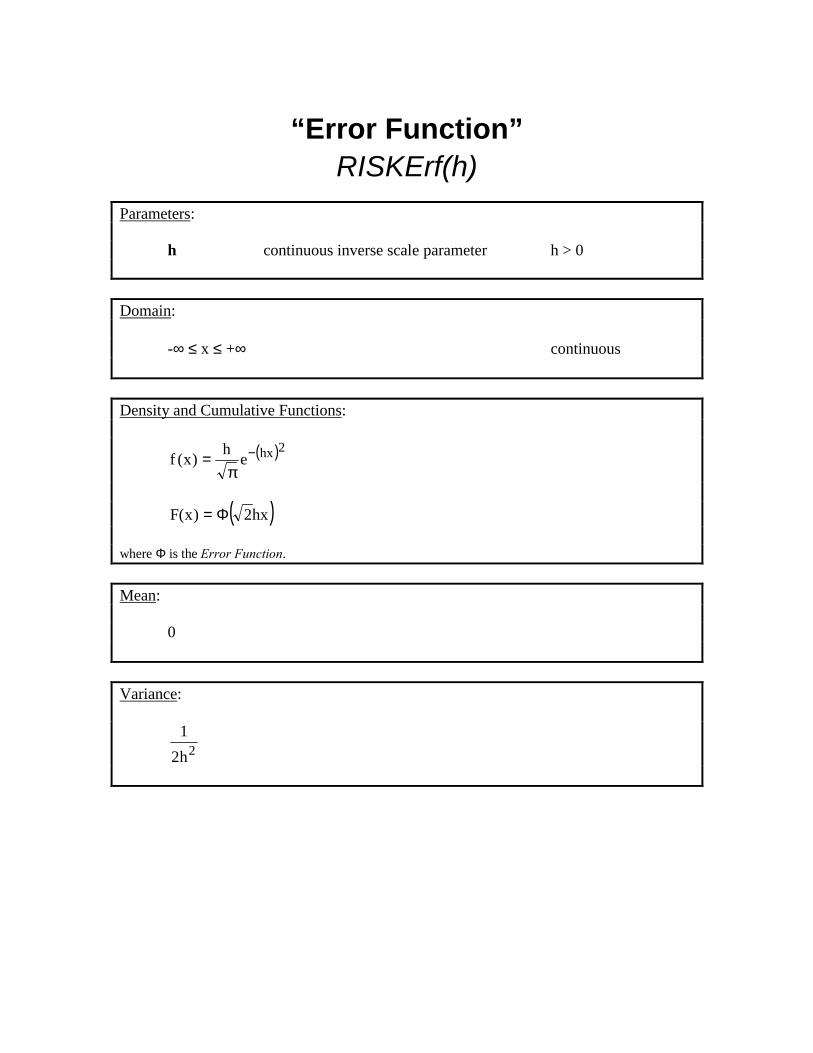

“Error Function” RISKErf(h)

Parameters: h continuous inverse scale parameter h > 0 Domain:

-∞ ≤ x ≤ +∞ continuous

Density and Cumulative Functions:

( )2hxeh)x(f −π

=

( )hx2)x(F Φ= where Φ is the Error Function. Mean:

0 Variance:

2h21

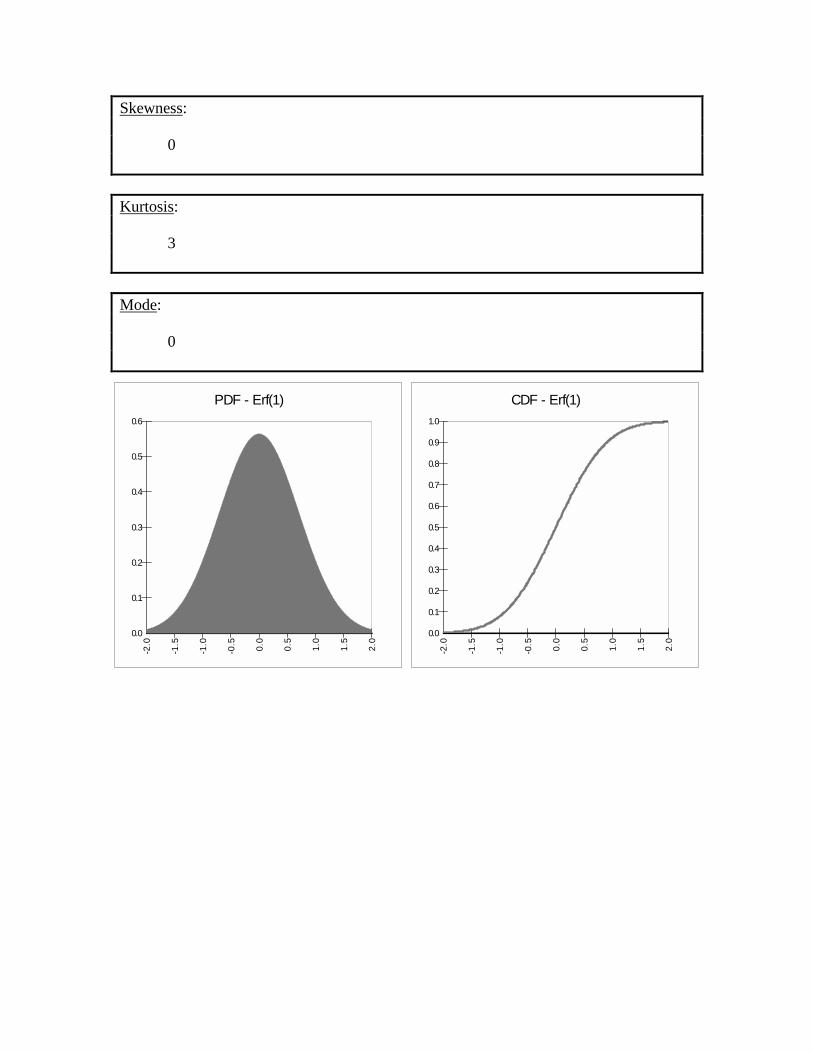

Skewness:

0 Kurtosis:

3 Mode:

0

PDF - Erf(1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

-2.0

-1.5

-1.0

-0.5 0.0

0.5

1.0

1.5

2.0

CDF - Erf(1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-2.0

-1.5

-1.0

-0.5 0.0

0.5

1.0

1.5

2.0

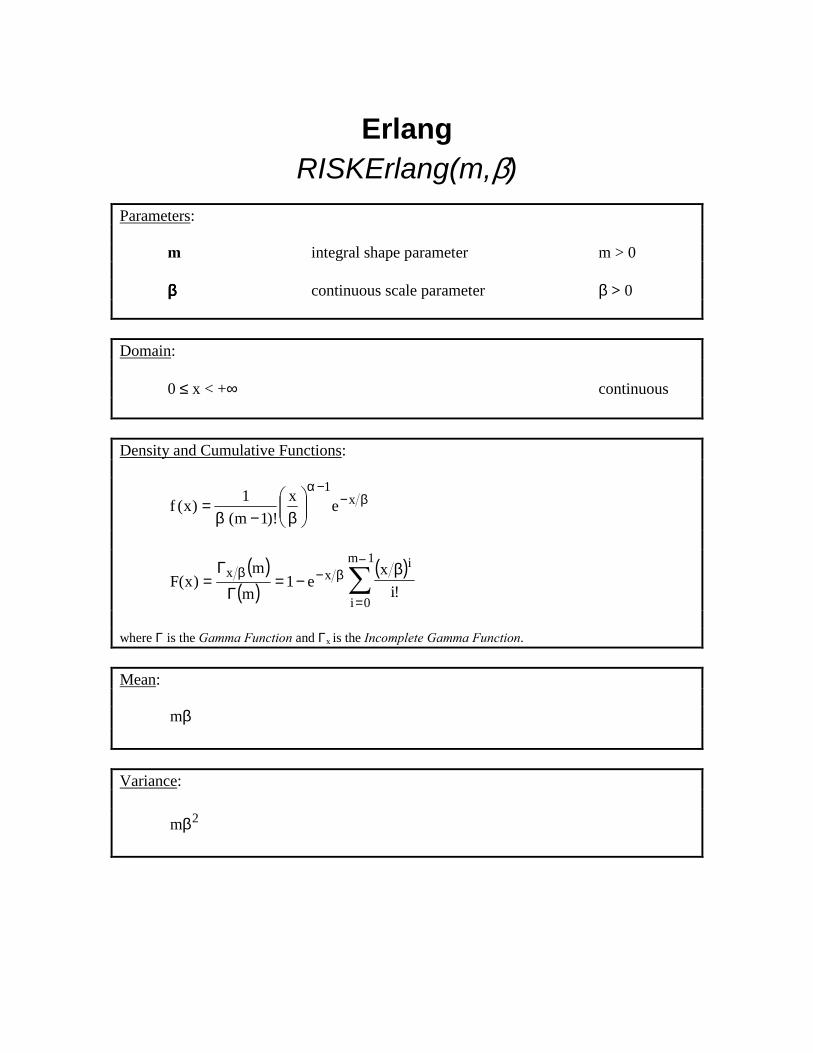

Erlang RISKErlang(m,β)

Parameters: m integral shape parameter m > 0

ββββ continuous scale parameter β > 0

Domain:

0 ≤ x < +∞ continuous Density and Cumulative Functions:

β−−α

β−β

= x1ex

)!1m(1)x(f

( )

( )( )∑

−

=

β−β β−=

Γ

Γ=

1m

0i

ixx

!ix

e1m

m)x(F

where Γ is the Gamma Function and Γx is the Incomplete Gamma Function. Mean: βm Variance:

2mβ

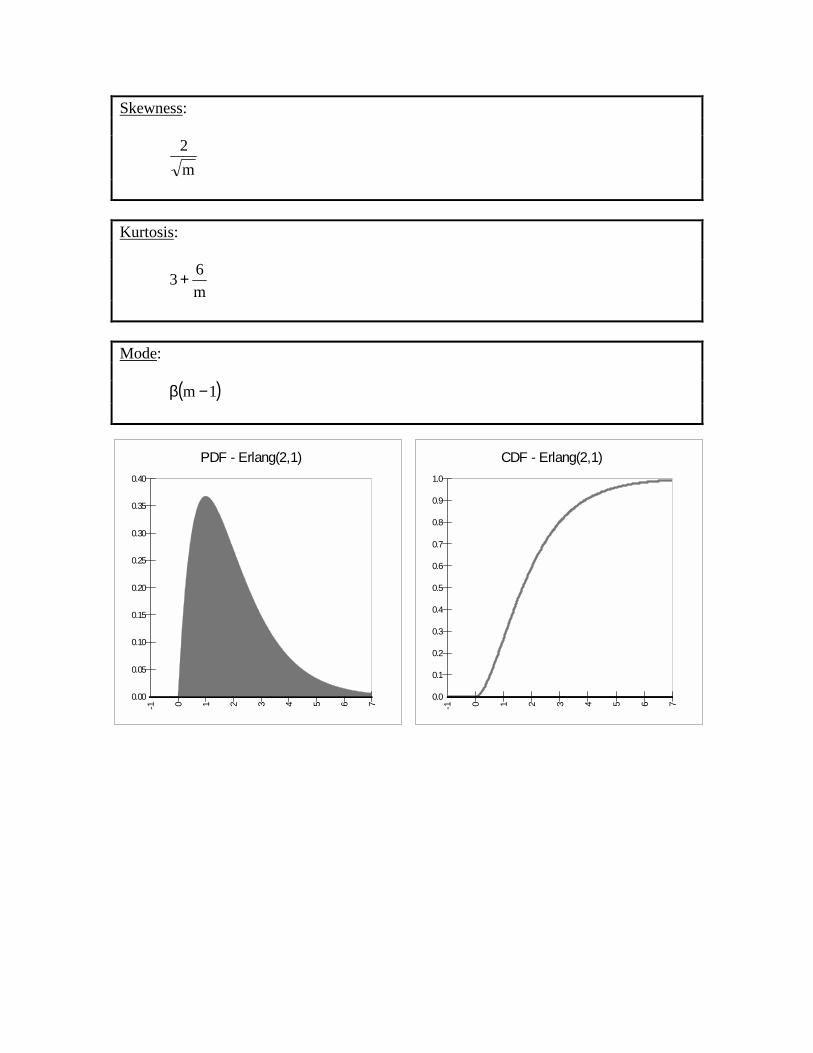

Skewness:

m2

Kurtosis:

m63 +

Mode: ( )1m −β

PDF - Erlang(2,1)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

-1 0 1 2 3 4 5 6 7

CDF - Erlang(2,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-1 0 1 2 3 4 5 6 7

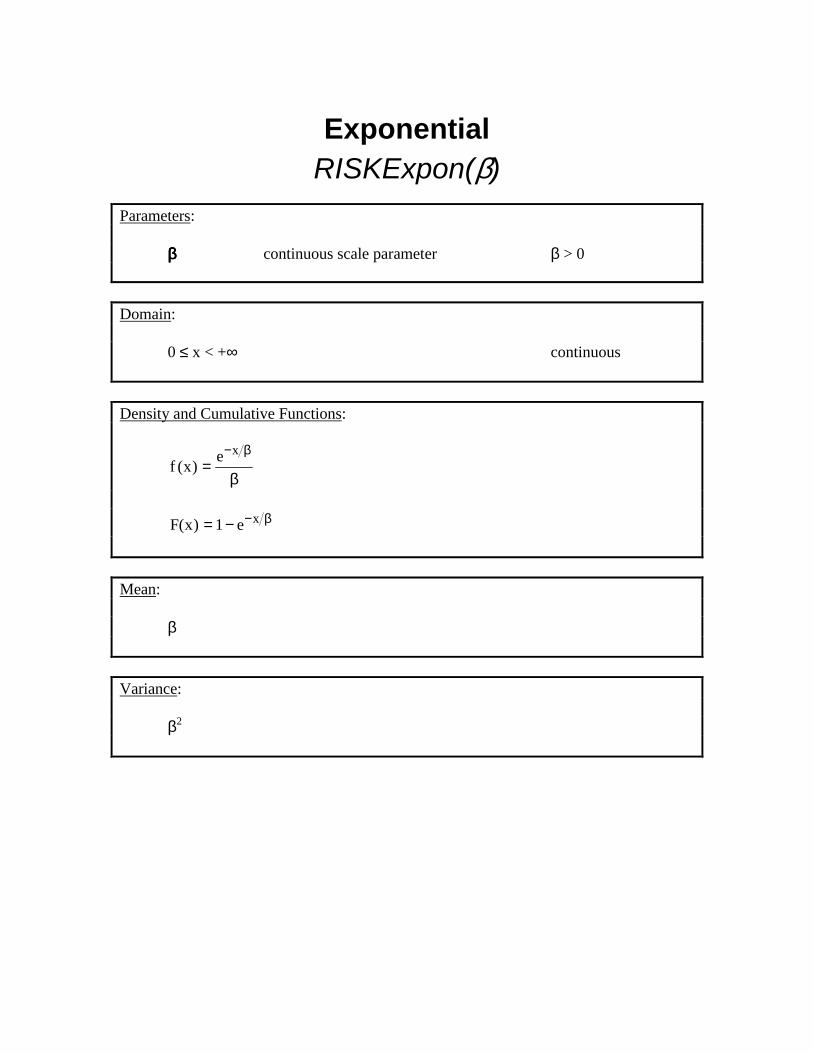

Exponential RISKExpon(β)

Parameters: ββββ continuous scale parameter β > 0

Domain: 0 ≤ x < +∞ continuous

Density and Cumulative Functions:

β

=β−xe)x(f

β−−= xe1)x(F

Mean:

β Variance:

β2

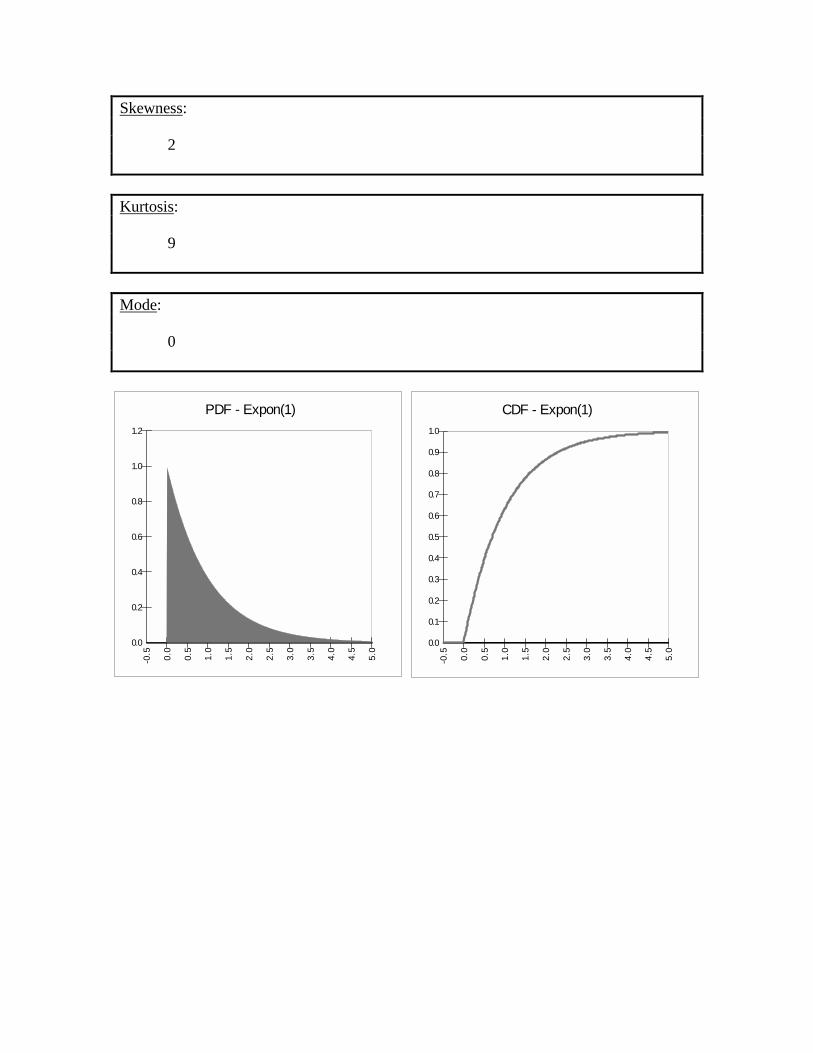

Skewness:

2 Kurtosis:

9 Mode:

0

PDF - Expon(1)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

CDF - Expon(1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0-0

.5 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

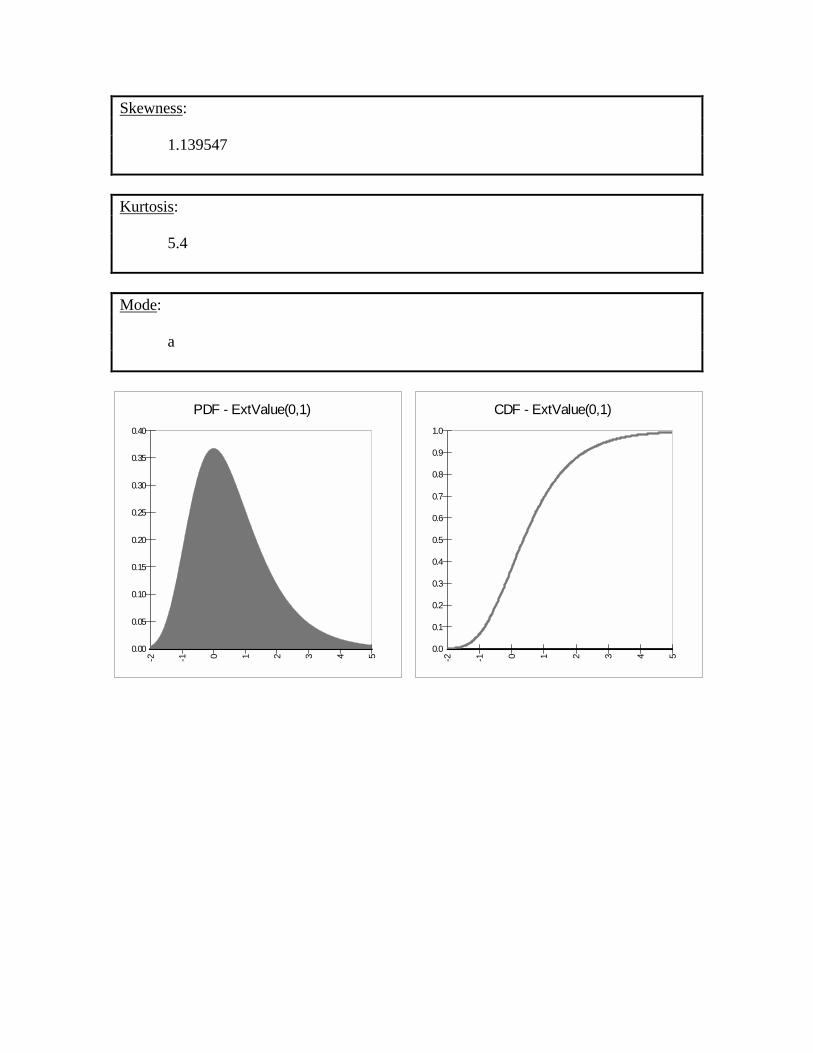

Extreme Value RISKExtValue(a, b)

Parameters: a continuous location parameter

b continuous scale parameter b > 0 Domain:

-∞ ≤ x ≤ +∞ continuous

Density and Cumulative Functions:

= −+ )zexp(ze

1b1)x(f

)zexp(e

1)x(F−

= where ( )b

axz −≡

Mean:

( ) b577.a1ba +≈Γ′− where Γ’(x) is the derivative of the Gamma Function. Variance:

6b22π

Skewness: 1.139547

Kurtosis:

5.4

Mode:

a

PDF - ExtValue(0,1)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

-2 -1 0 1 2 3 4 5

CDF - ExtValue(0,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-2 -1 0 1 2 3 4 5

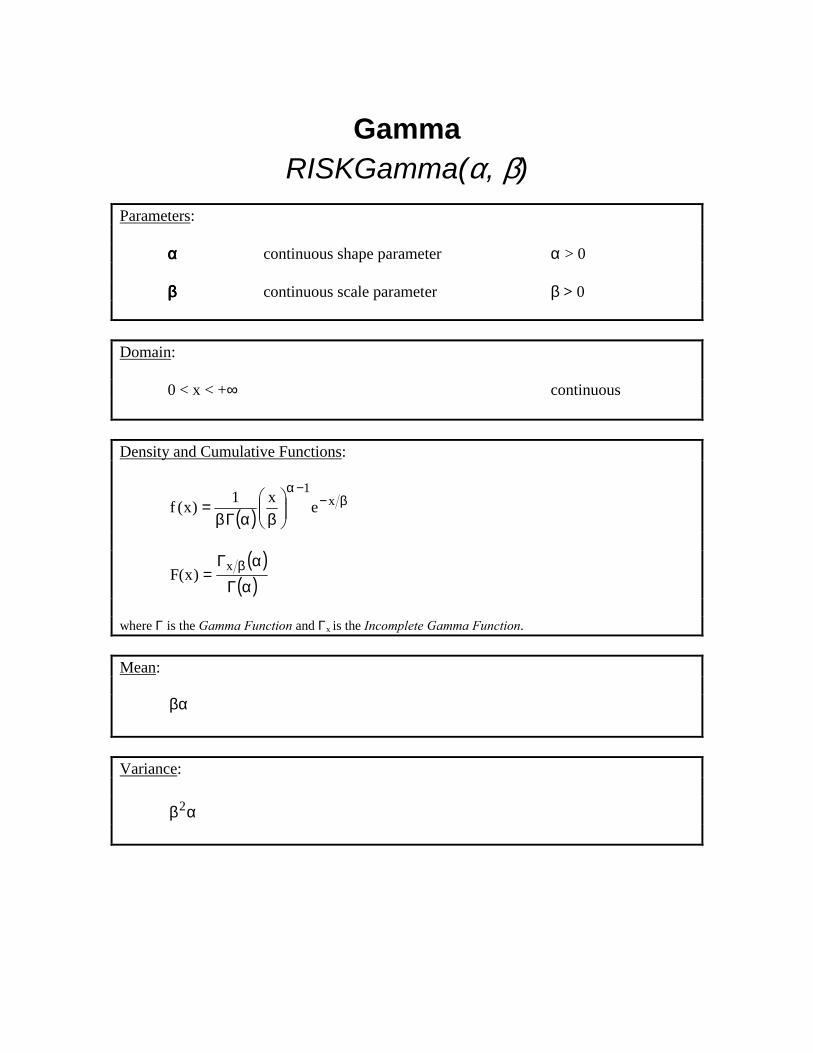

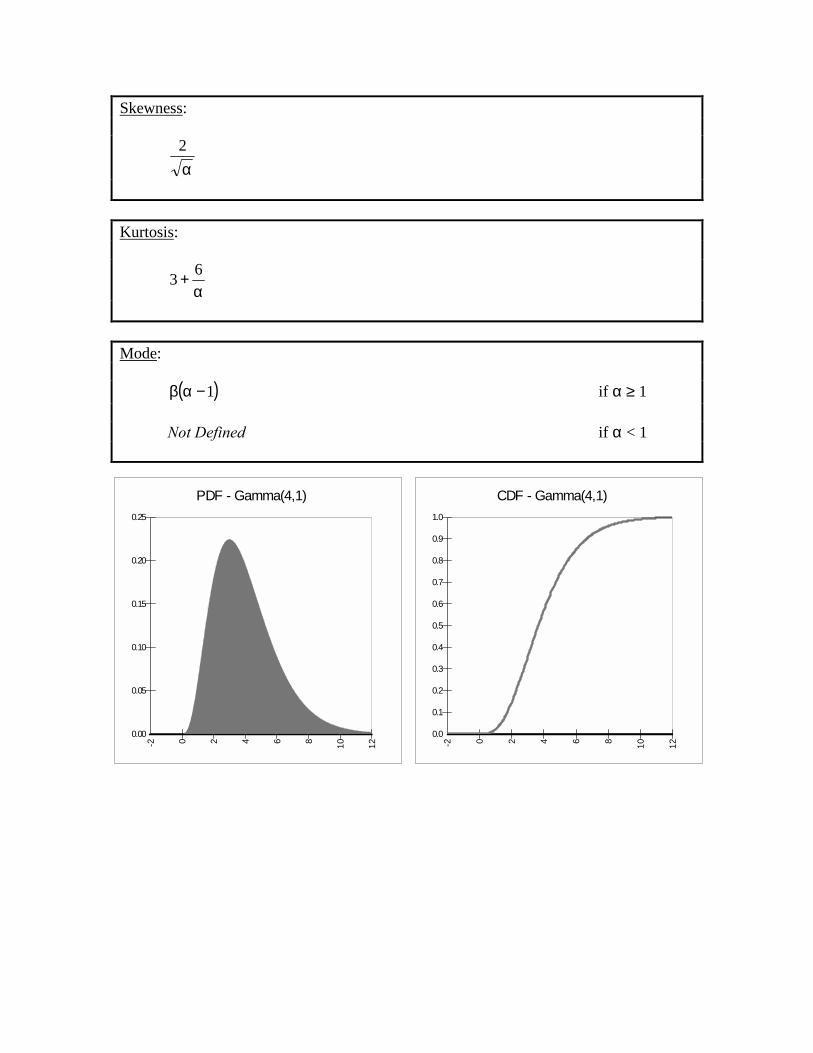

Gamma RISKGamma(α, β)

Parameters: αααα continuous shape parameter α > 0

ββββ continuous scale parameter β > 0

Domain:

0 < x < +∞ continuous

Density and Cumulative Functions:

( )β−

−α

βαΓβ

= x1ex1)x(f

( )

( )αΓαΓ

= βx)x(F

where Γ is the Gamma Function and Γx is the Incomplete Gamma Function. Mean: βα Variance:

αβ2

Skewness:

α2

Kurtosis:

α

+ 63

Mode: ( )1−αβ if α ≥ 1 Not Defined if α < 1

CDF - Gamma(4,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-2 0 2 4 6 8 10 12

PDF - Gamma(4,1)

0.00

0.05

0.10

0.15

0.20

0.25

-2 0 2 4 6 8 10 12

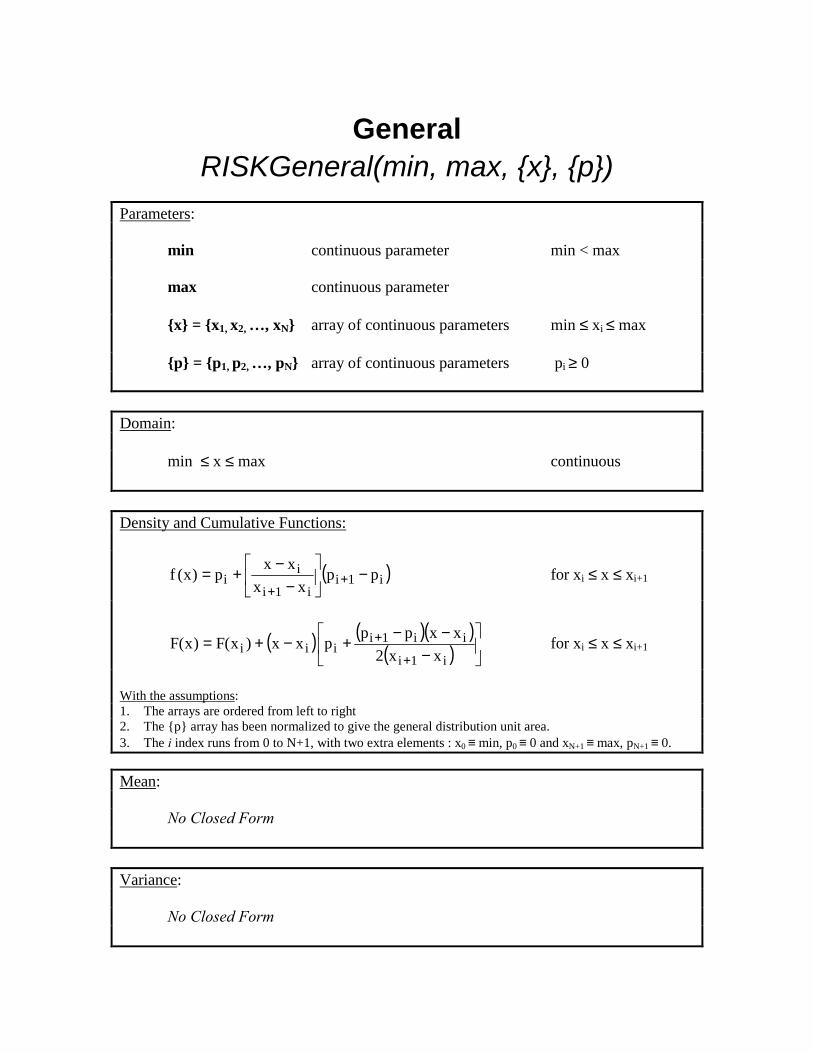

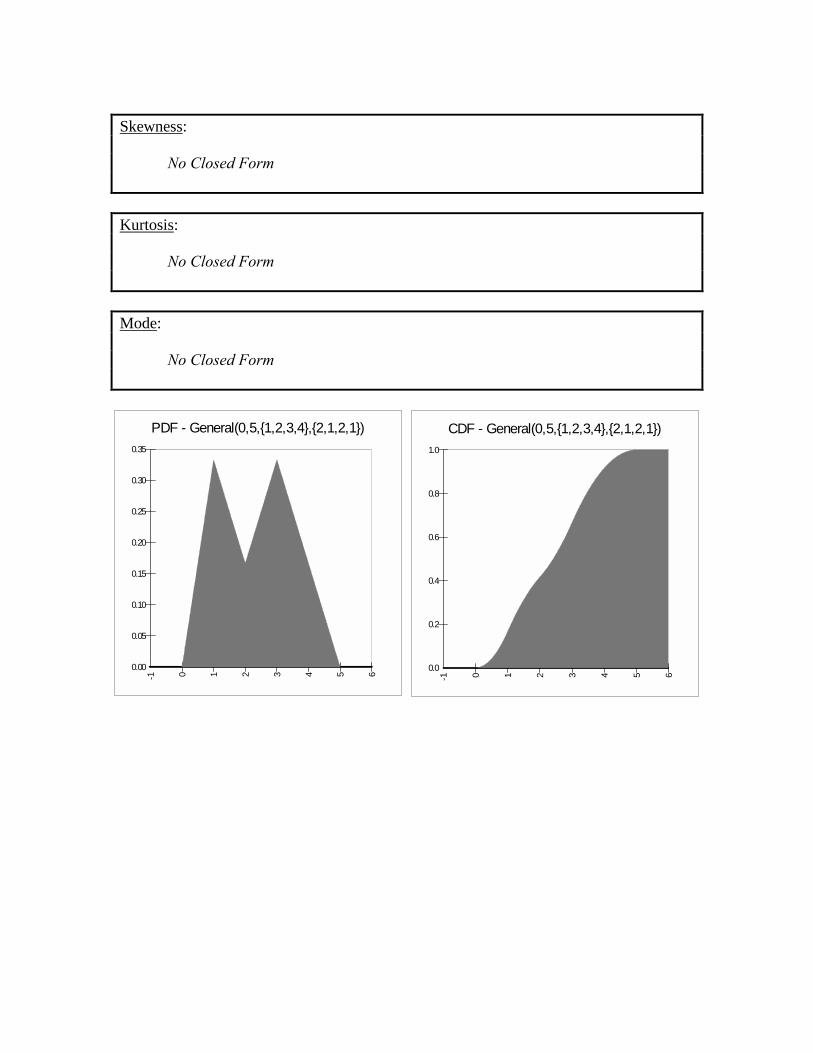

General RISKGeneral(min, max, {x}, {p})

Parameters: min continuous parameter min < max max continuous parameter {x} = {x1, x2, …, xN} array of continuous parameters min ≤ xi ≤ max {p} = {p1, p2, …, pN} array of continuous parameters pi ≥ 0 Domain: min ≤ x ≤ max continuous

Density and Cumulative Functions:

( )i1ii1i

ii pp

xxxx

p)x(f −

−

−+= +

+ for xi ≤ x ≤ xi+1

( ) ( )( )( )

−

−−+−+=

+

+

i1i

ii1iiii xx2

xxpppxx)x(F)x(F for xi ≤ x ≤ xi+1

With the assumptions: 1. The arrays are ordered from left to right 2. The {p} array has been normalized to give the general distribution unit area. 3. The i index runs from 0 to N+1, with two extra elements : x0 ≡ min, p0 ≡ 0 and xN+1 ≡ max, pN+1 ≡ 0. Mean: No Closed Form Variance: No Closed Form

Skewness:

No Closed Form

Kurtosis:

No Closed Form Mode:

No Closed Form

PDF - General(0,5,{1,2,3,4},{2,1,2,1})

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

-1 0 1 2 3 4 5 6

CDF - General(0,5,{1,2,3,4},{2,1,2,1})

0.0

0.2

0.4

0.6

0.8

1.0-1 0 1 2 3 4 5 6

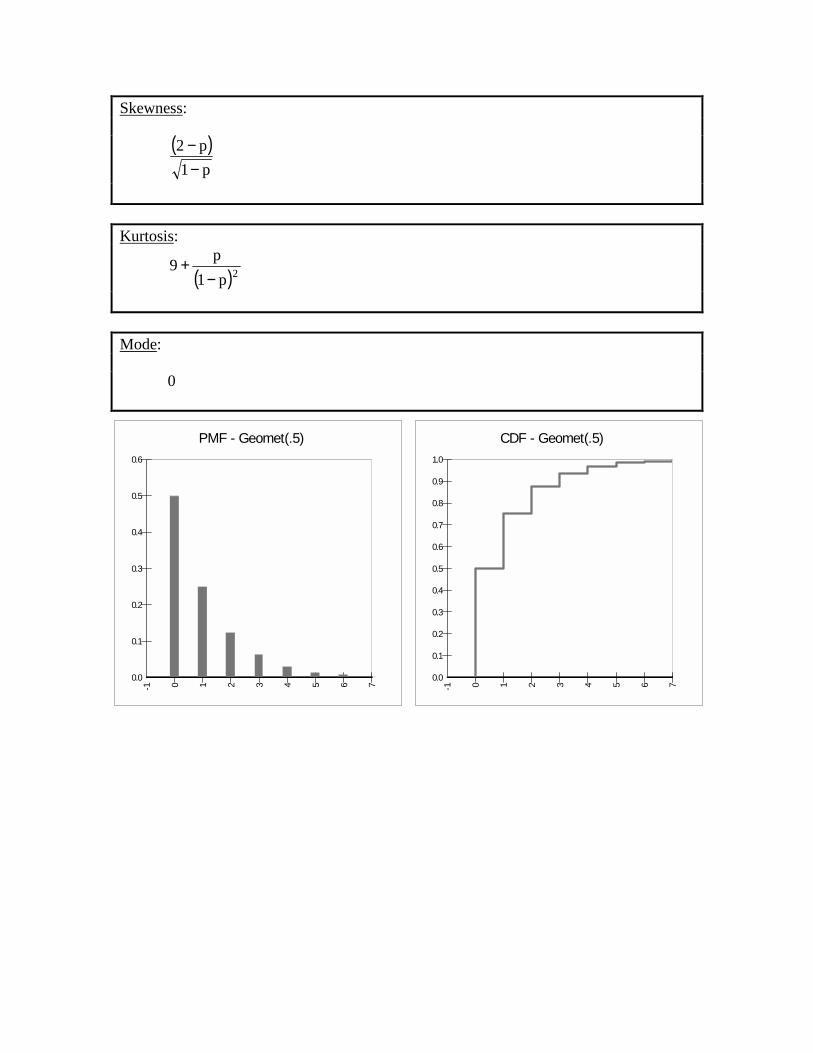

Geometric RISKGeomet(p)

Parameters: p continuous “success” probability 0< p < 1 Domain: 0 ≤ x < +∞ discrete

Mass and Cumulative Functions: ( )xp1p)x(f −=

1x)p1(1)x(F +−−=

Mean:

1p1 −

Variance:

2pp1−

Skewness:

( )p1p2

−−

Kurtosis:

( )2p1p9

−+

Mode:

0

PMF - Geomet(.5)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

-1 0 1 2 3 4 5 6 7

CDF - Geomet(.5)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0-1 0 1 2 3 4 5 6 7

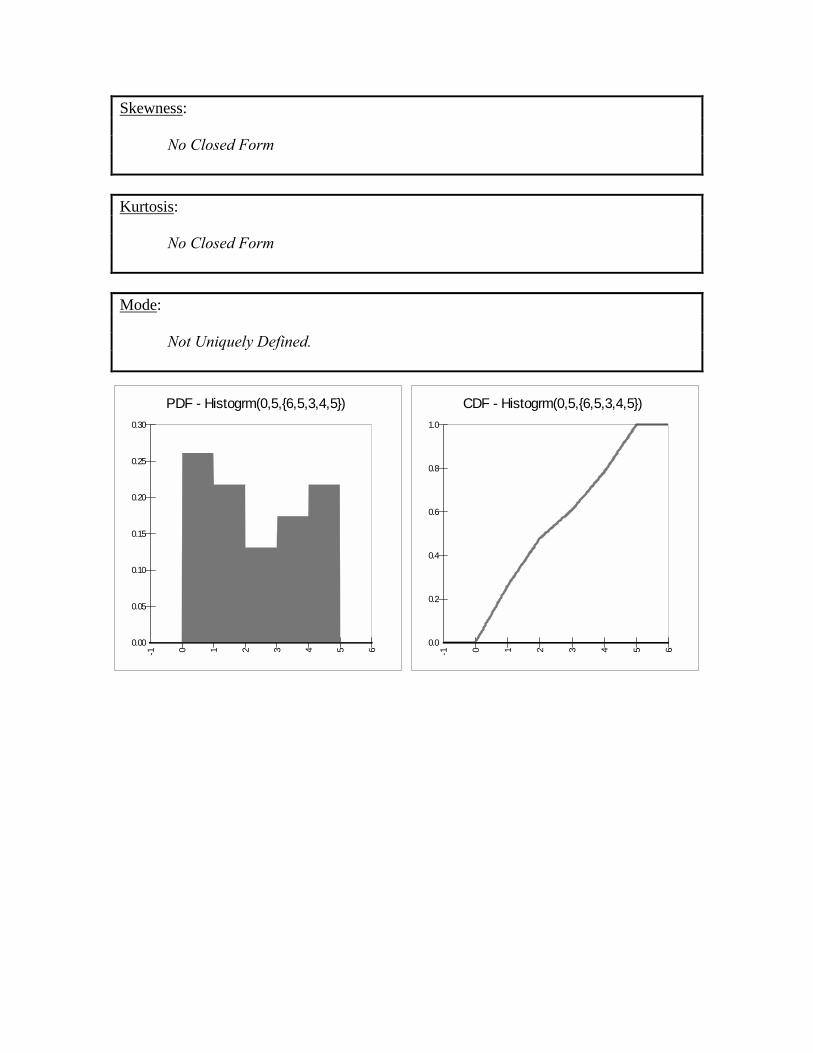

Histogram RISKHistogrm(min, max, {p})

Parameters: min continuous parameter min < max max continuous parameter {p} = {p1, p2, …, pN} array of continuous parameters pi ≥ 0 Domain: min ≤ x ≤ max continuous

Density and Cumulative Functions: ip)x(f = for xi ≤ x < xi+1

−

−+=

+ i1i

iii xx

xxp)x(F)x(F for xi ≤ x ≤ xi+1

where

−+≡

Nminmaximinxi

The {p} array has been normalized to give the histogram unit area. Mean: No Closed Form Variance: No Closed Form

Skewness:

No Closed Form

Kurtosis:

No Closed Form Mode:

Not Uniquely Defined.

PDF - Histogrm(0,5,{6,5,3,4,5})

0.00

0.05

0.10

0.15

0.20

0.25

0.30

-1 0 1 2 3 4 5 6

CDF - Histogrm(0,5,{6,5,3,4,5})

0.0

0.2

0.4

0.6

0.8

1.0

-1 0 1 2 3 4 5 6

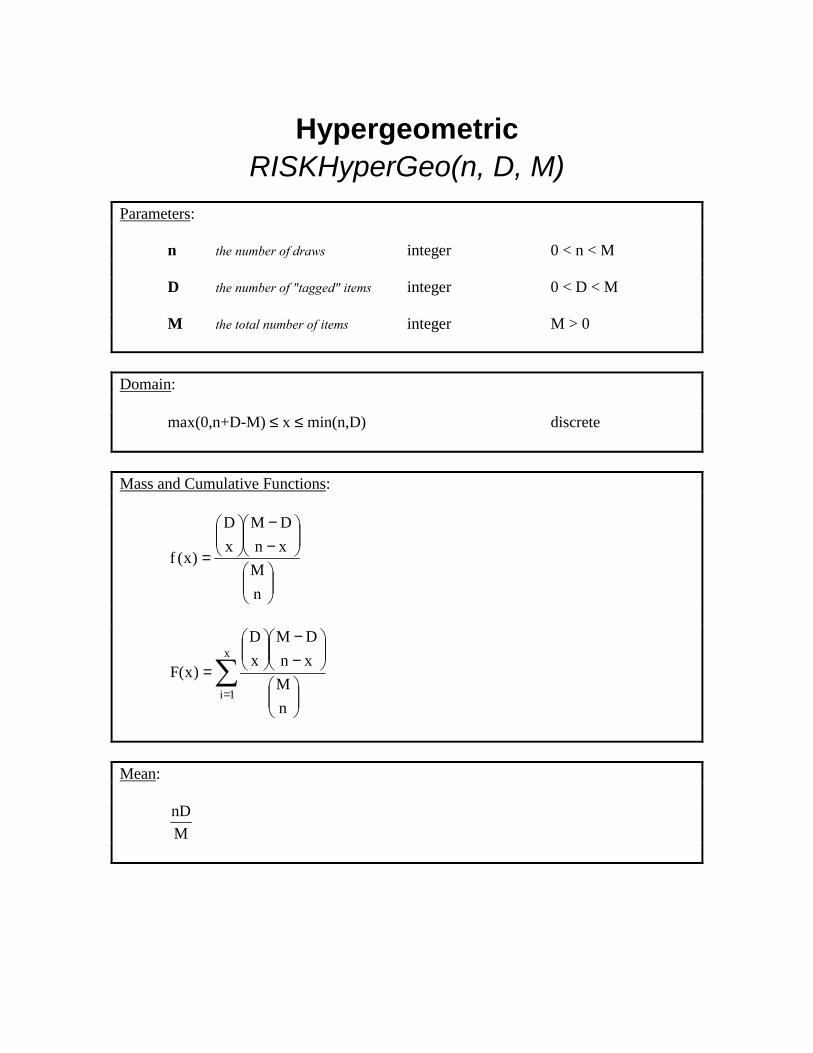

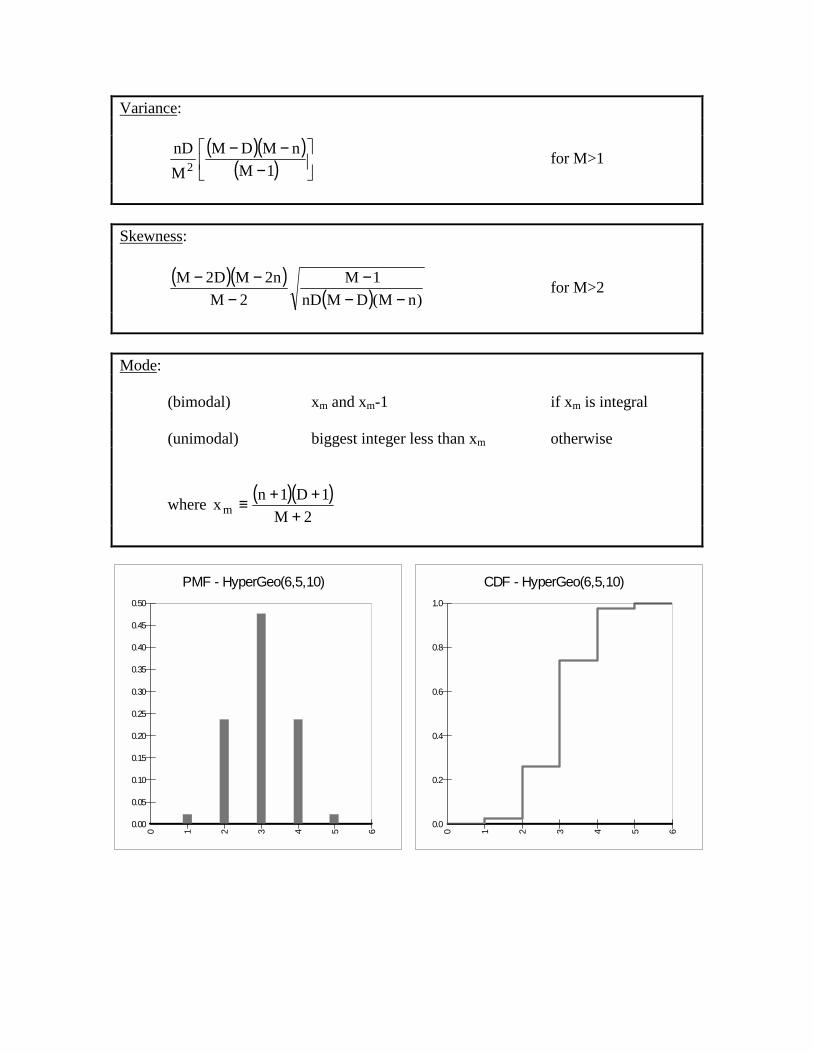

Hypergeometric RISKHyperGeo(n, D, M)

Parameters:

n the number of draws integer 0 < n < M D the number of "tagged" items integer 0 < D < M

M the total number of items integer M > 0 Domain: max(0,n+D-M) ≤ x ≤ min(n,D) discrete

Mass and Cumulative Functions:

−−

=

nM

xnDM

xD

)x(f

∑=

−−

=x

1inM

xnDM

xD

)x(F

Mean:

MnD

Variance:

( )( )( )

−

−−1M

nMDMMnD

2 for M>1

Skewness:

( )( )( ) )nM(DMnD

1M2M

n2MD2M−−

−−

−− for M>2

Mode:

(bimodal) xm and xm-1 if xm is integral

(unimodal) biggest integer less than xm otherwise

where ( )( )2M

1D1nx m +++≡

PMF - HyperGeo(6,5,10)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0 1 2 3 4 5 6

CDF - HyperGeo(6,5,10)

0.0

0.2

0.4

0.6

0.8

1.0

0 1 2 3 4 5 6

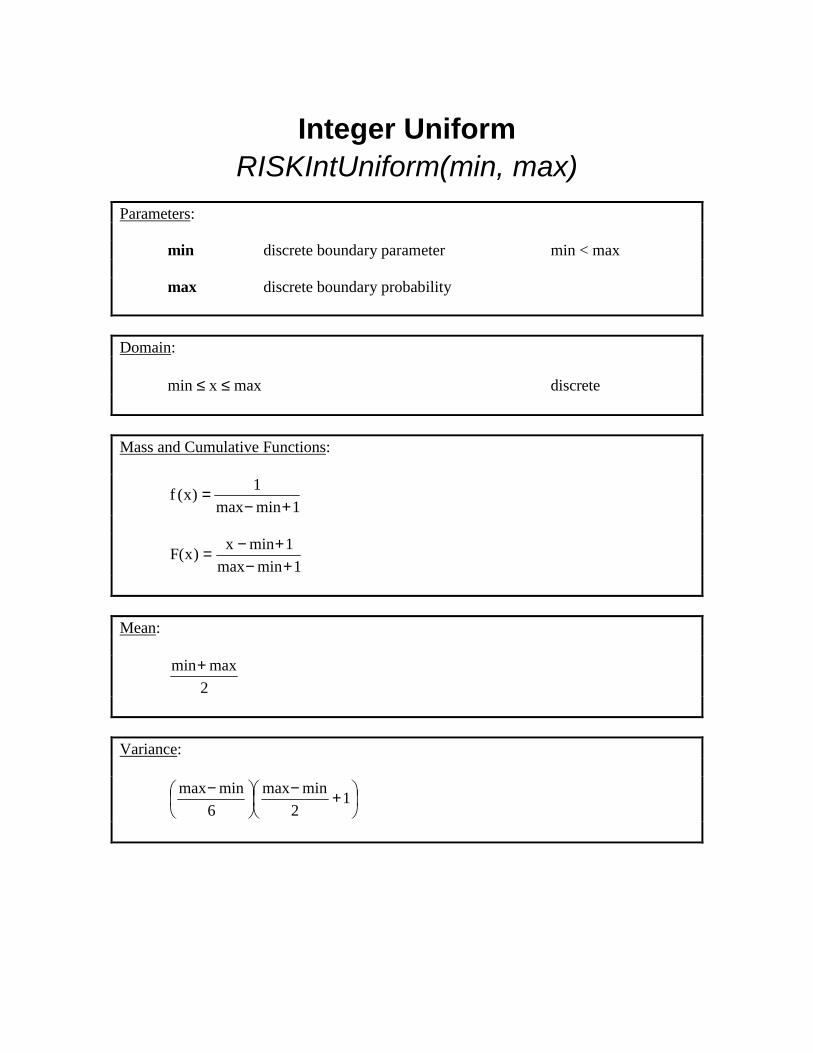

Integer Uniform RISKIntUniform(min, max)

Parameters: min discrete boundary parameter min < max max discrete boundary probability Domain: min ≤ x ≤ max discrete

Mass and Cumulative Functions:

1minmax

1)x(f+−

=

1minmax1minx)x(F+−

+−=

Mean:

2maxmin+

Variance:

+−

− 1

2minmax

6minmax

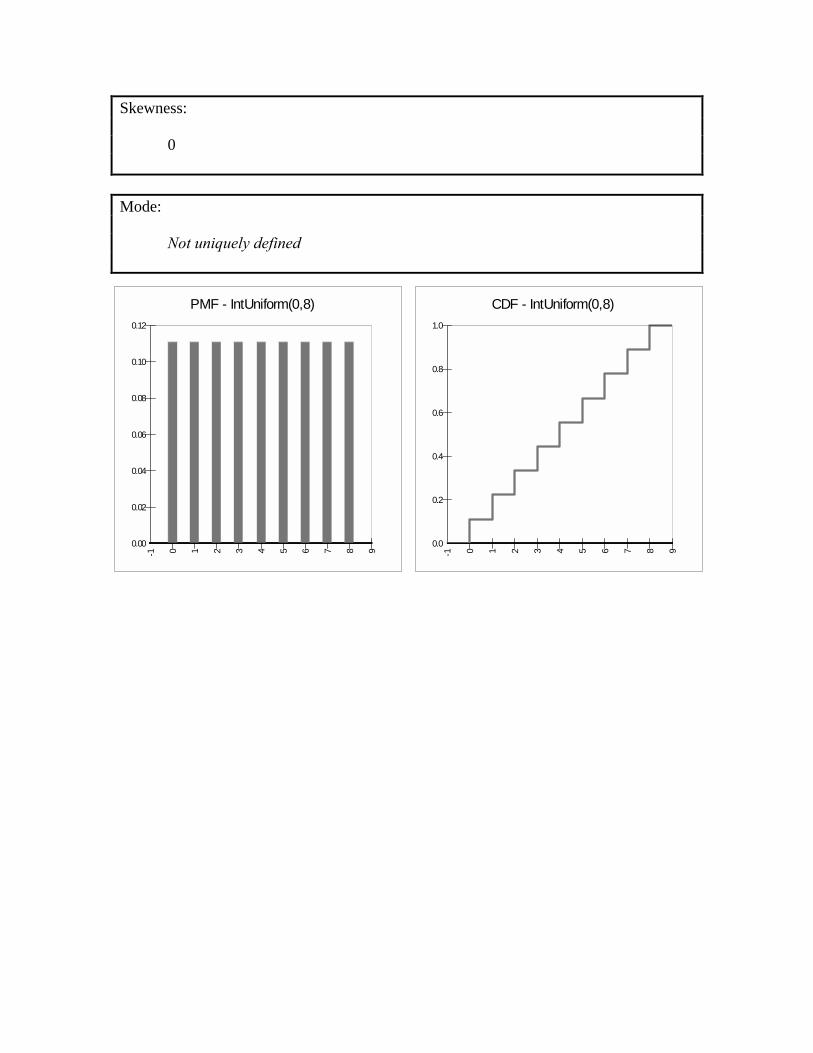

Skewness:

0 Mode:

Not uniquely defined

CDF - IntUniform(0,8)

0.0

0.2

0.4

0.6

0.8

1.0

-1 0 1 2 3 4 5 6 7 8 9

PMF - IntUniform(0,8)

0.00

0.02

0.04

0.06

0.08

0.10

0.12

-1 0 1 2 3 4 5 6 7 8 9

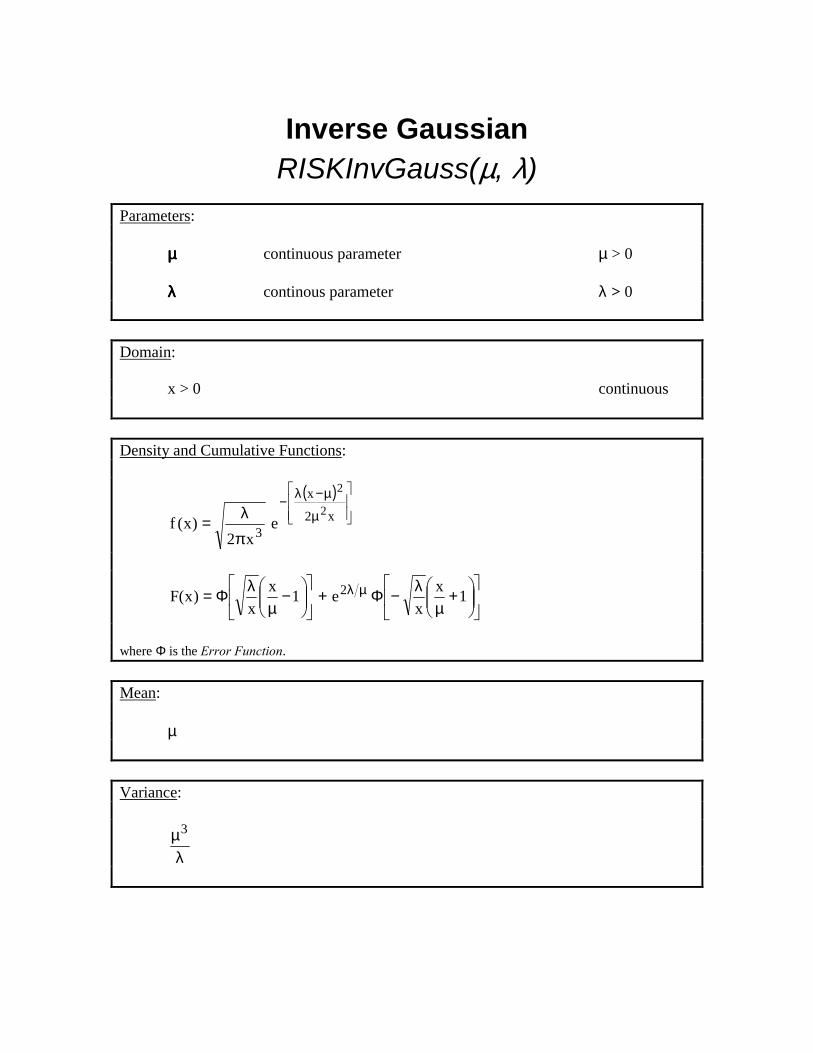

Inverse Gaussian RISKInvGauss(µ, λ)

Parameters:

µµµµ continuous parameter µ > 0

λλλλ continous parameter λ > 0 Domain:

x > 0 continuous

Density and Cumulative Functions:

( )

µ

µ−λ−

πλ= x2

x

3

2

2

ex2

)x(f

+µ

λ−Φ+

−µ

λΦ= µλ 1xx

e1xx

)x(F 2

where Φ is the Error Function. Mean: µ Variance:

λ

µ3

Skewness:

λµ3

Kurtosis:

λµ+153

Mode:

λµ−

λµ+µ

23

491 2

2

PDF - InvGauss(1,2)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

CDF - InvGauss(1,2)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

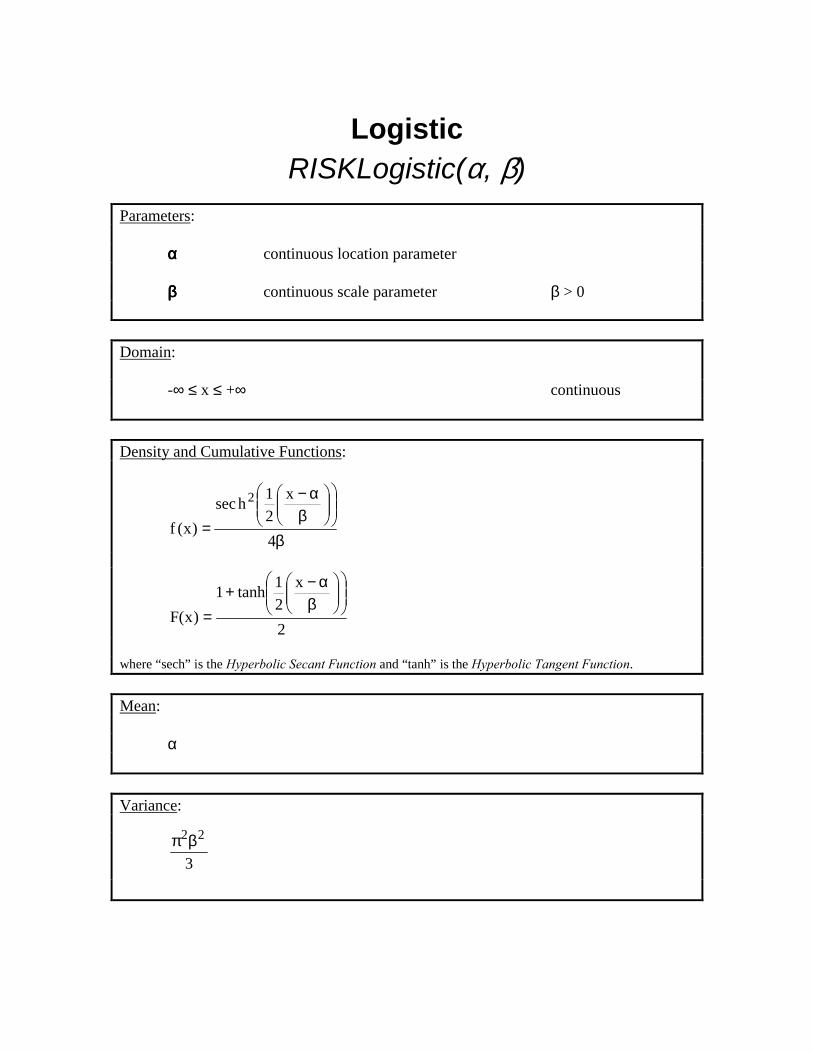

Logistic RISKLogistic(α, β)

Parameters: αααα continuous location parameter

ββββ continuous scale parameter β > 0

Domain: -∞ ≤ x ≤ +∞ continuous

Density and Cumulative Functions:

β

β

α−

=4

x21hsec

)x(f

2

2

x21tanh1

)x(F

β

α−+=

where “sech” is the Hyperbolic Secant Function and “tanh” is the Hyperbolic Tangent Function. Mean:

α Variance:

3

22βπ

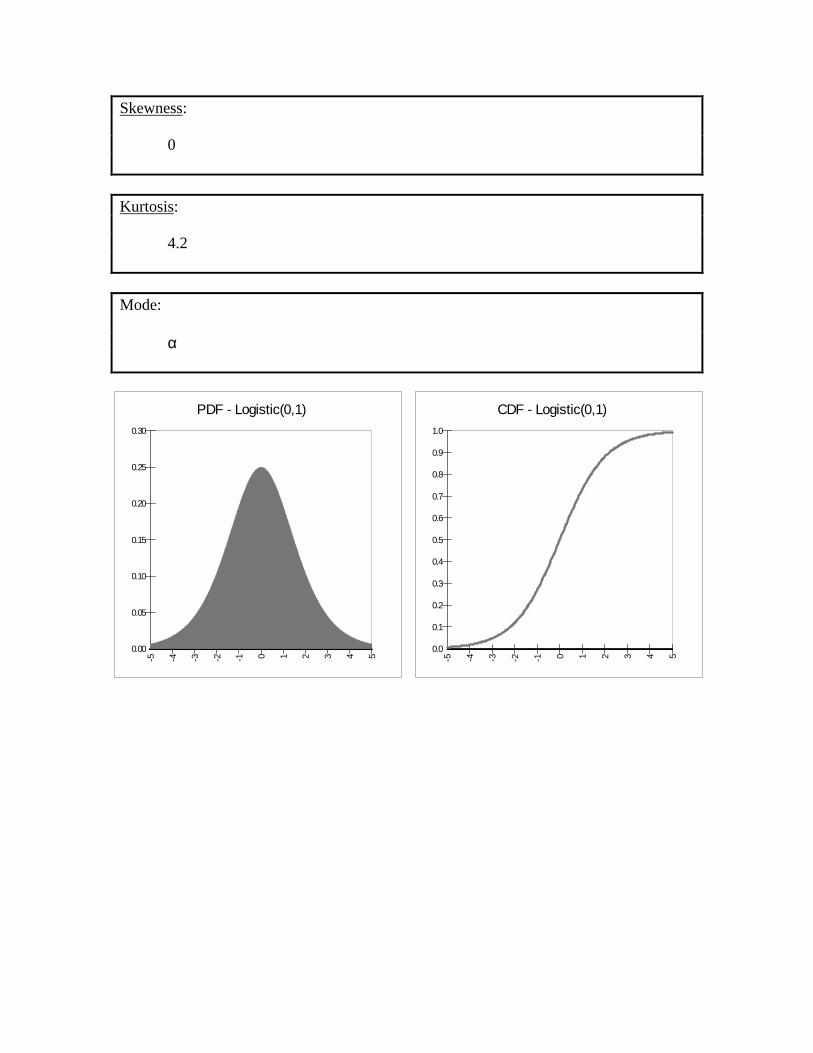

Skewness:

0 Kurtosis:

4.2 Mode:

α

PDF - Logistic(0,1)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

-5 -4 -3 -2 -1 0 1 2 3 4 5

CDF - Logistic(0,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-5 -4 -3 -2 -1 0 1 2 3 4 5

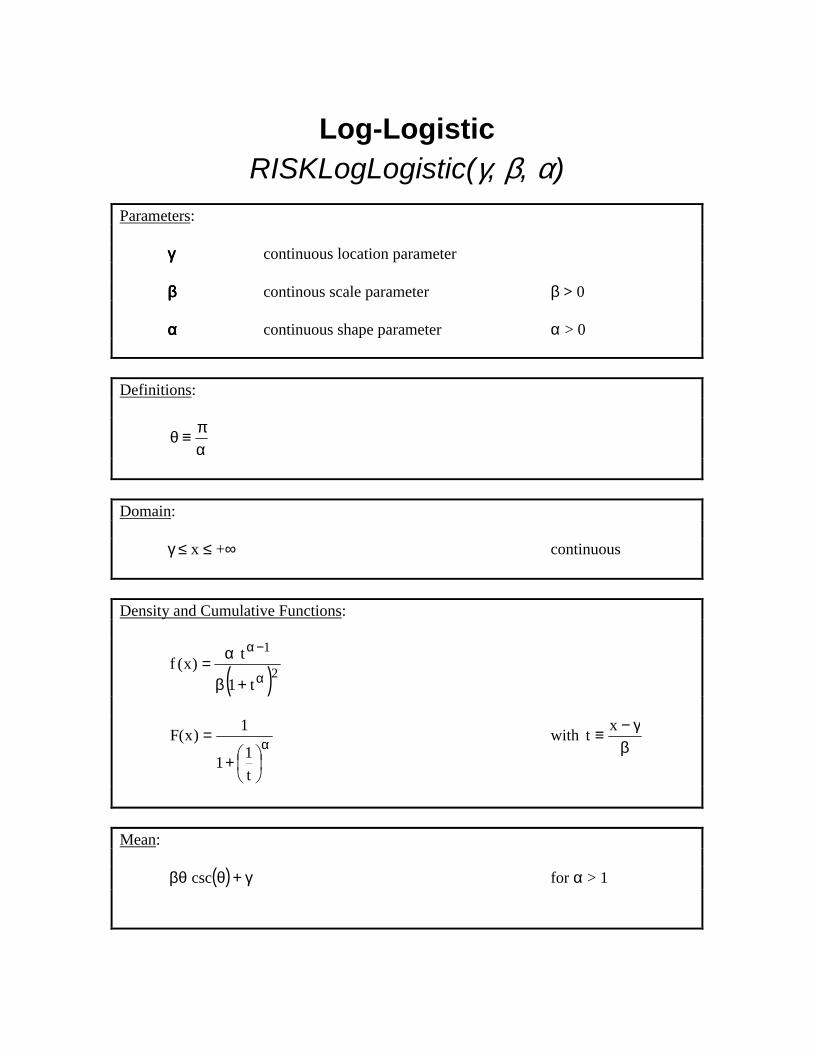

Log-Logistic RISKLogLogistic(γ, β, α)

Parameters:

γγγγ continuous location parameter

ββββ continous scale parameter β > 0 αααα continuous shape parameter α > 0

Definitions:

απ≡θ

Domain:

γ ≤ x ≤ +∞ continuous

Density and Cumulative Functions:

( )21

t1

t)x(fα

−α

+β

α=

α

+

=

t11

1)x(F with β

γ−≡ xt

Mean:

( ) γ+θβθ csc for α > 1

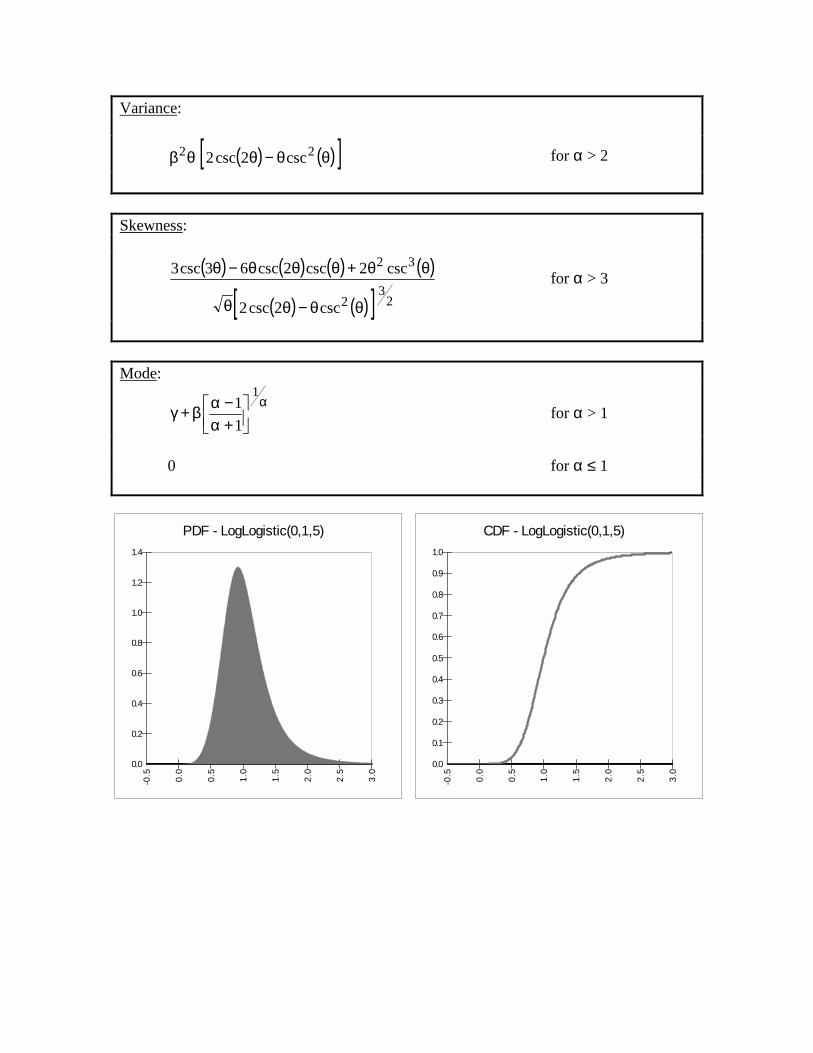

Variance:

( ) ( )[ ]θθ−θθβ 22 csc2csc2 for α > 2

Skewness:

( ) ( ) ( ) ( )

( ) ( )[ ] 23

2

32

csc2csc2

csc2csc2csc63csc3

θθ−θθ

θθ+θθθ−θ for α > 3

Mode:

α

+α−αβ+γ

1

11 for α > 1

0 for α ≤ 1

PDF - LogLogistic(0,1,5)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

3.0

CDF - LogLogistic(0,1,5)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

3.0

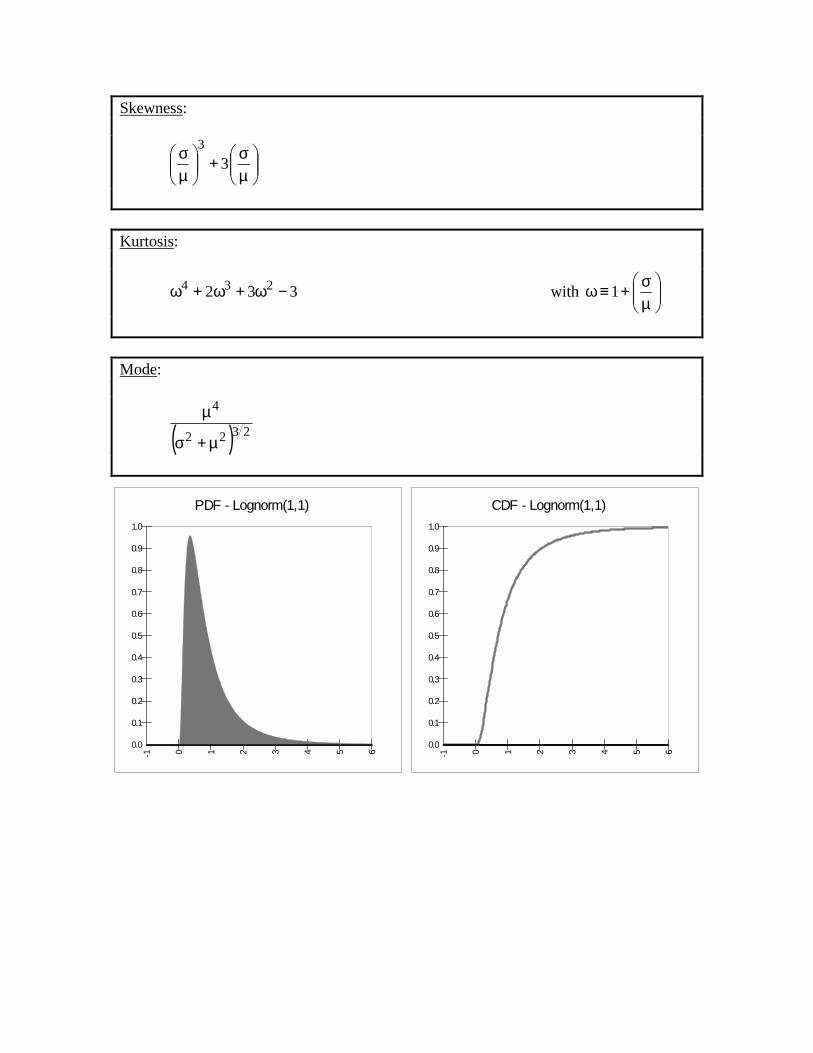

Lognormal (Format 1) RISKLognorm(µ, σ)

Parameters:

µµµµ continuous parameter µ > 0

σσσσ continous parameter σ > 0

Domain:

0 ≤ x ≤ +∞ continuous

Density and Cumulative Functions:

2xln

21

e2x1)x(f

σ′µ′−−

σ′π=

σ′µ′−Φ= xln)x(F

with

µ+σ

µ≡µ′22

2ln and

+≡′

2

1lnµσσ

where Φ is the Error Function. Mean: µ Variance:

2σ

Skewness:

µσ+

µσ 3

3

Kurtosis:

332 234 −ω+ω+ω with

µσ+≡ω 1

Mode:

( ) 2322

4

µ+σ

µ

PDF - Lognorm(1,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-1 0 1 2 3 4 5 6

CDF - Lognorm(1,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-1 0 1 2 3 4 5 6

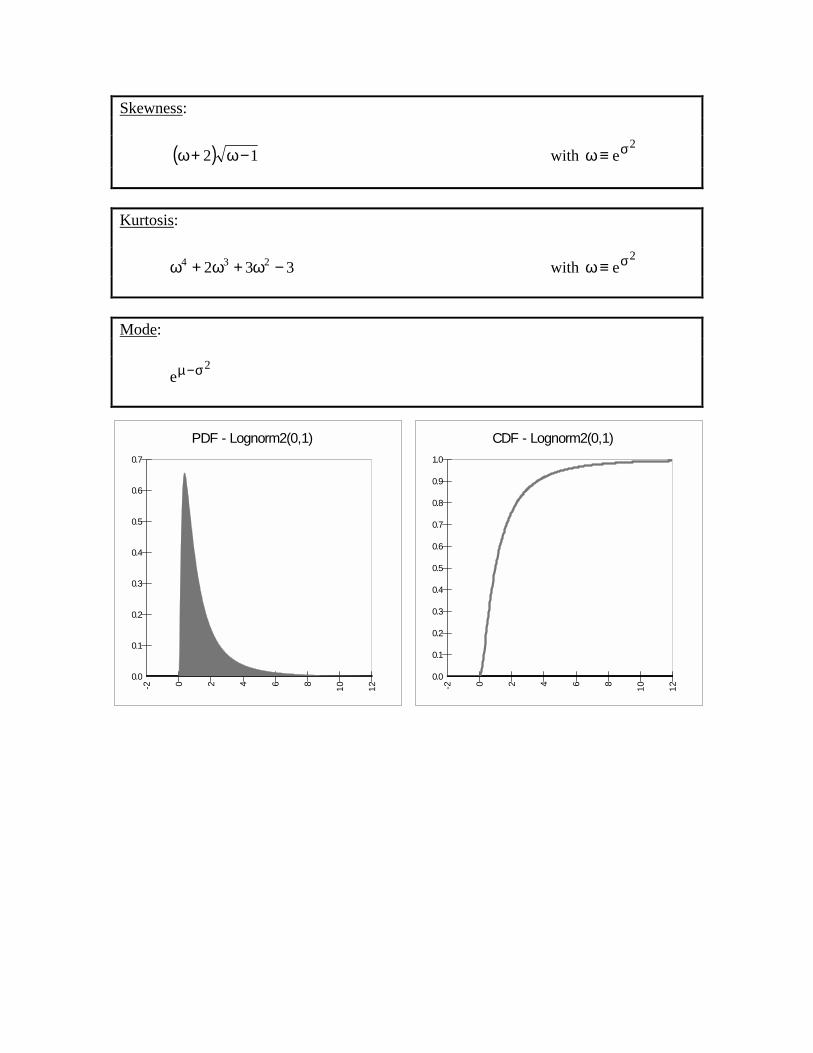

Lognormal (Format 2) RISKLognorm2(µ, σ)

Parameters:

µµµµ continuous parameter

σσσσ continous parameter σ > 0

Domain:

0 ≤ x ≤ +∞ continuous

Density and Cumulative Functions:

2xln21

e2x1)x(f

σµ−−

σπ=

σµ−Φ= xln)x(F

where Φ is the Error Function. Mean:

2

2

eσ+µ

Variance:

( )1e2 −ωωµ with 2

eσ≡ω

Skewness:

( ) 12 −ω+ω with 2

eσ≡ω Kurtosis:

332 234 −ω+ω+ω with 2

eσ≡ω Mode:

2

e σ−µ

PDF - Lognorm2(0,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

-2 0 2 4 6 8 10 12

CDF - Lognorm2(0,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0-2 0 2 4 6 8 10 12

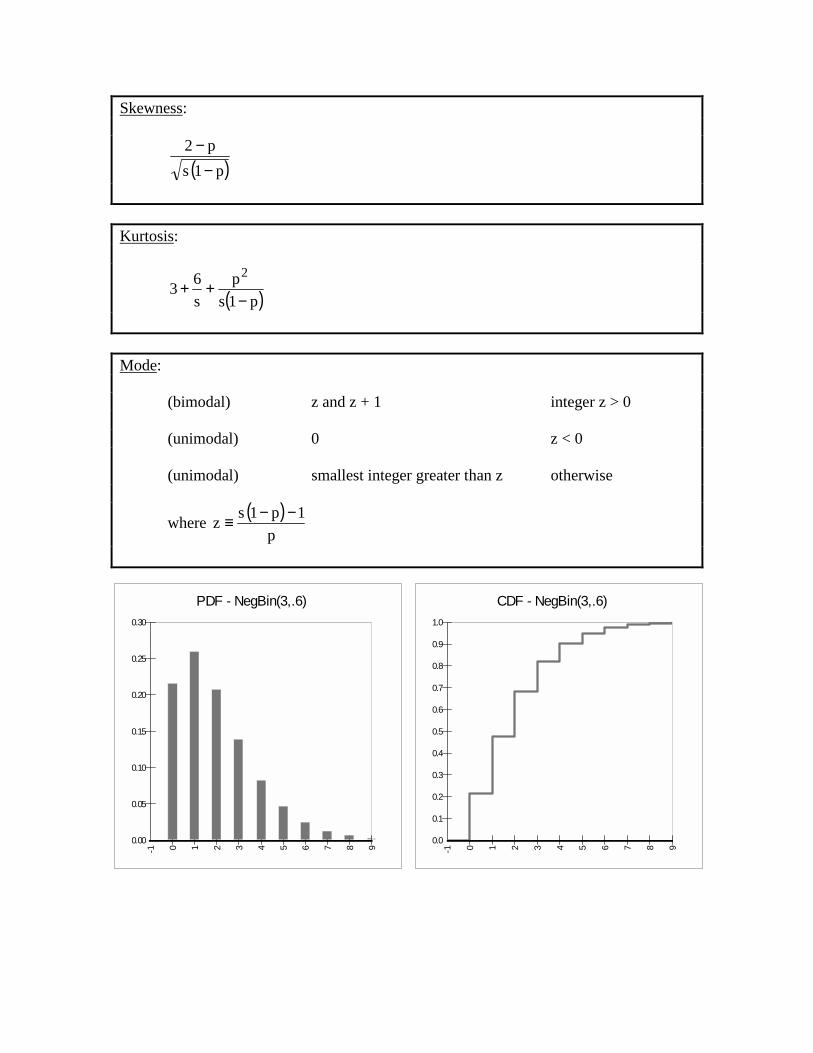

Negative Binomial RISKNegBin(s, p)

Parameters: s the number of successes discrete parameter s > 0 p probability of a single success continuous parameter 0 < p < 1 Domain: 0 ≤ x ≤ n discrete

Density and Cumulative Functions:

( )xs p1px

1xs)x(f −

−+=

ix

0i

s )p1(i

1isp)x(F −

−+= ∑

=

Where ( ) is the Binomial Coefficient. Mean:

( )p

p1s −

Variance:

( )2p

p1s −

Skewness:

( )p1sp2−

−

Kurtosis:

( )p1sp

s63

2

−++

Mode:

(bimodal) z and z + 1 integer z > 0

(unimodal) 0 z < 0 (unimodal) smallest integer greater than z otherwise

where ( )p

1p1sz −−≡

PDF - NegBin(3,.6)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

-1 0 1 2 3 4 5 6 7 8 9

CDF - NegBin(3,.6)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-1 0 1 2 3 4 5 6 7 8 9

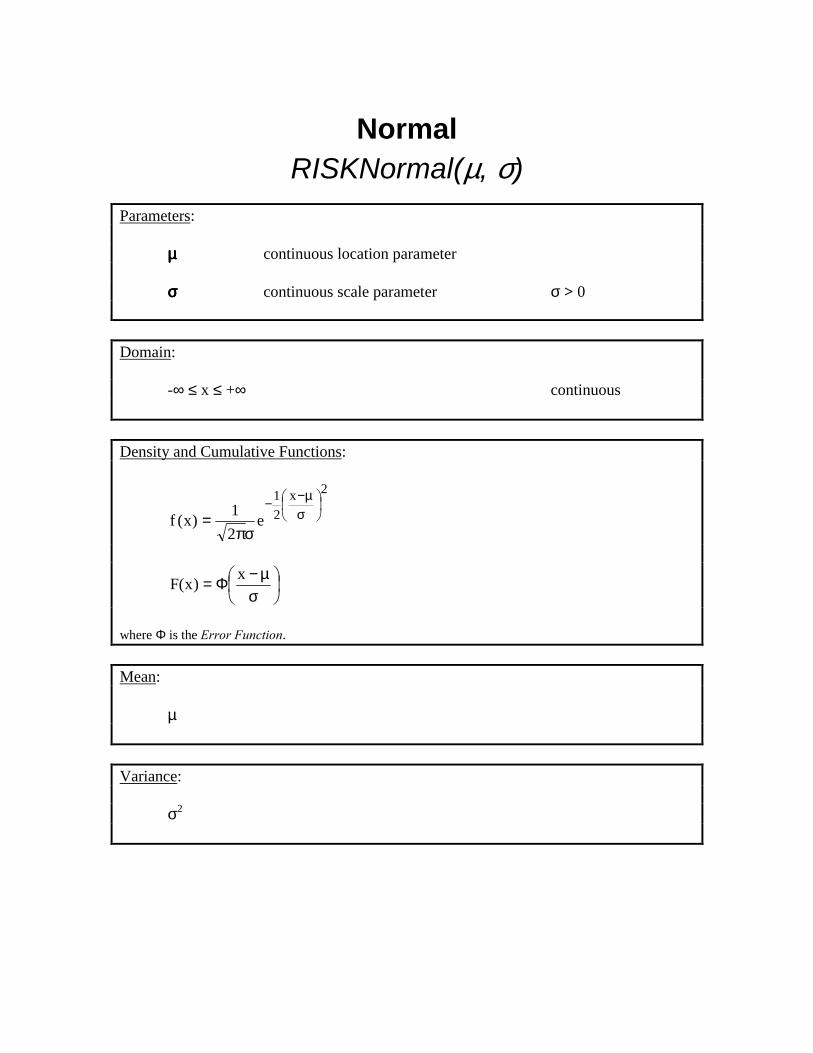

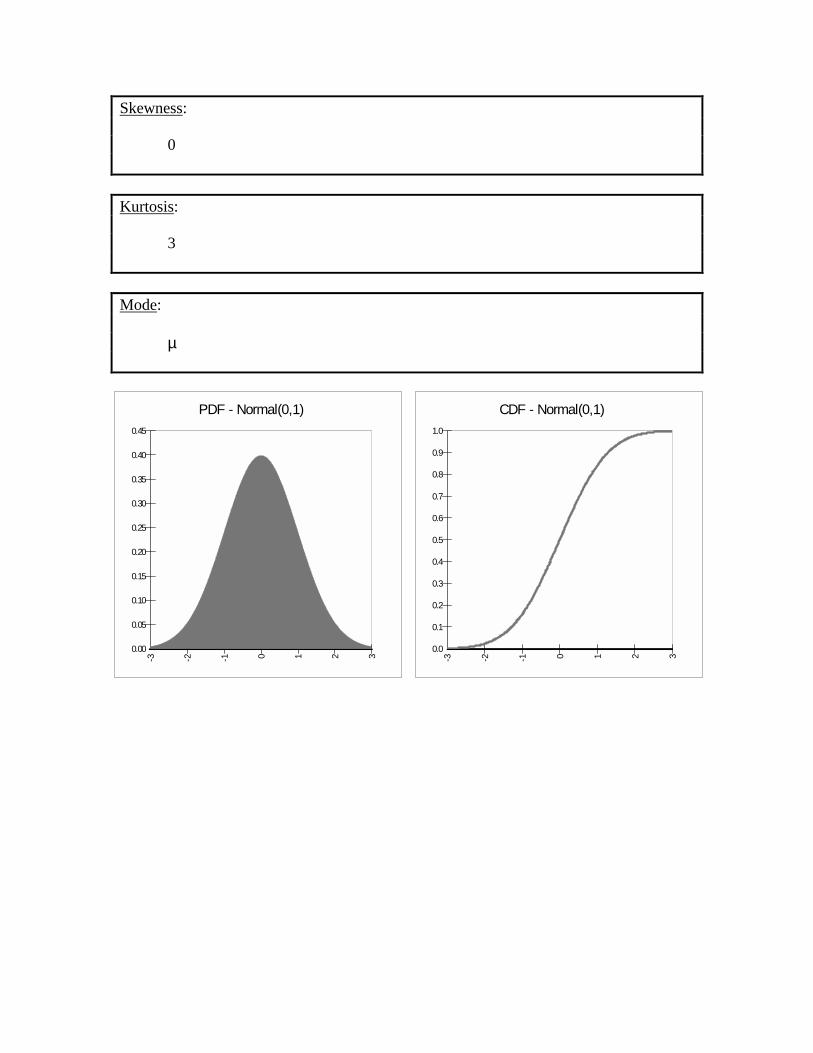

Normal RISKNormal(µ, σ)

Parameters: µµµµ continuous location parameter

σσσσ continuous scale parameter σ > 0

Domain:

-∞ ≤ x ≤ +∞ continuous

Density and Cumulative Functions:

2x21

e21)x(f

σµ−−

σπ=

σµ−Φ= x)x(F

where Φ is the Error Function. Mean:

µ Variance:

σ2

Skewness:

0 Kurtosis:

3 Mode:

µ

PDF - Normal(0,1)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

-3 -2 -1 0 1 2 3

CDF - Normal(0,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-3 -2 -1 0 1 2 3

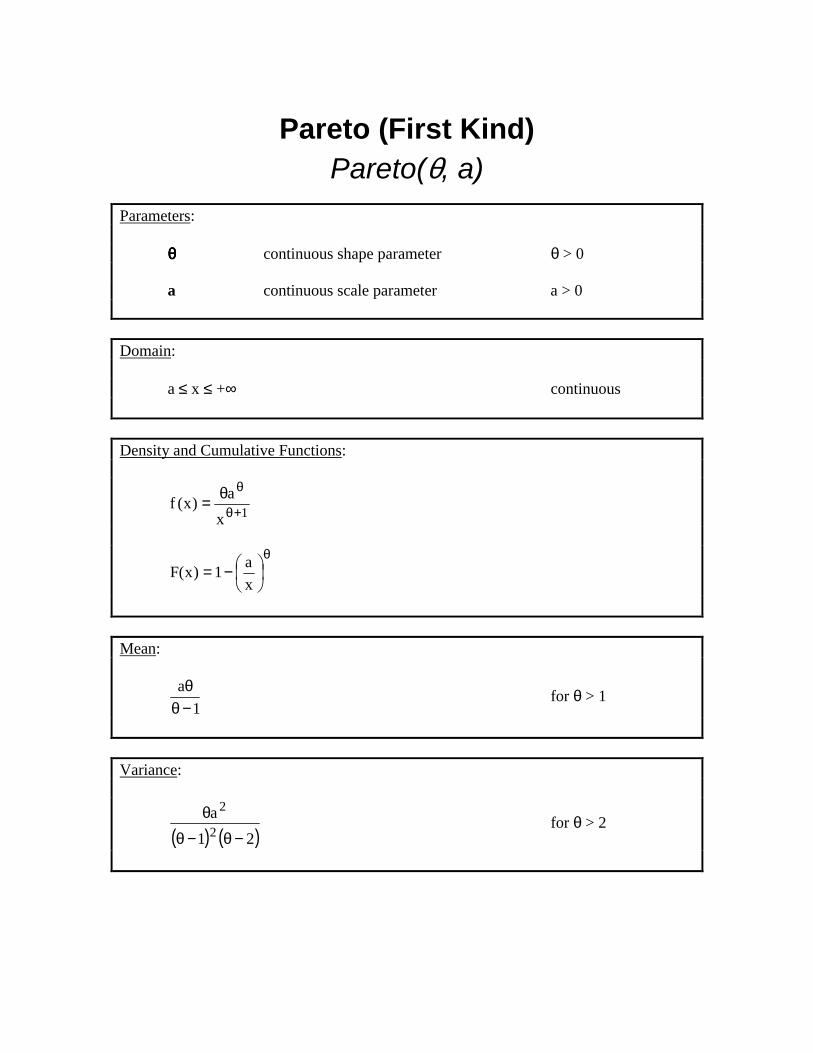

Pareto (First Kind) Pareto(θ, a)

Parameters: θθθθ continuous shape parameter θ > 0 a continuous scale parameter a > 0

Domain: a ≤ x ≤ +∞ continuous

Density and Cumulative Functions:

1x

a)x(f+θ

θθ=

θ

−=

xa1)x(F

Mean:

1a−θθ for θ > 1

Variance:

( ) ( )21

a2

2

−θ−θ

θ for θ > 2

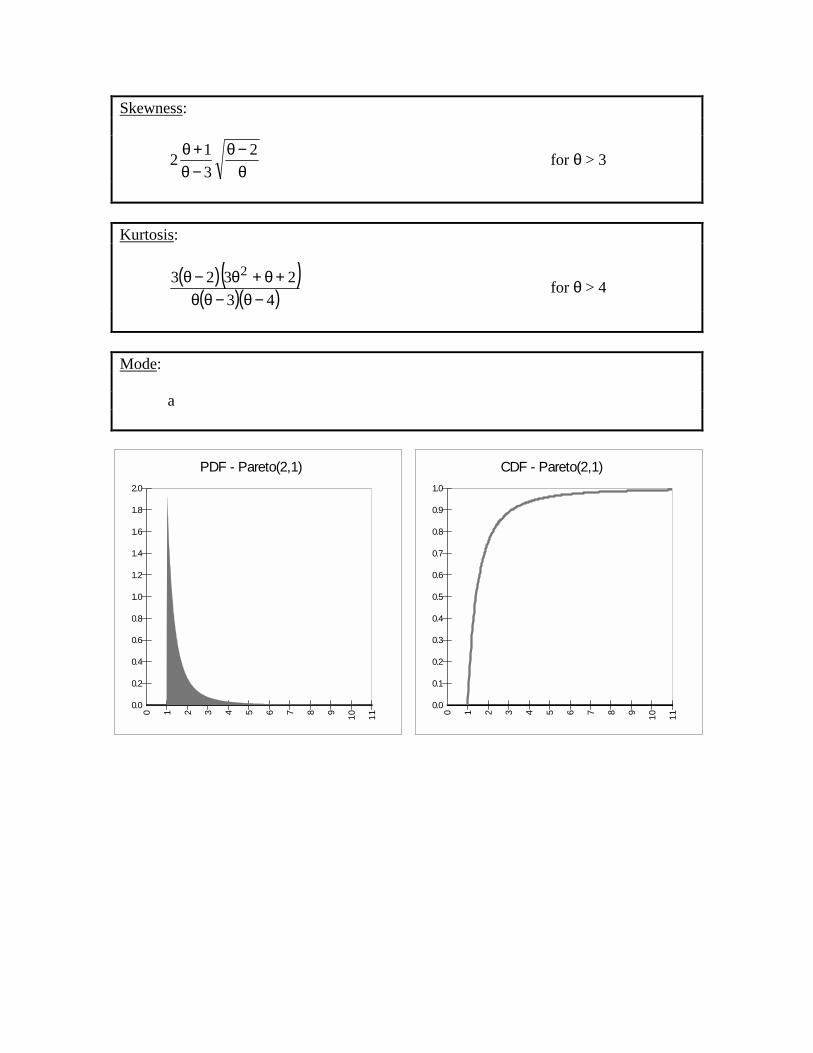

Skewness:

θ−θ

−θ+θ 2

312 for θ > 3

Kurtosis:

( )( )( )( )43

2323 2

−θ−θθ+θ+θ−θ for θ > 4

Mode:

a

PDF - Pareto(2,1)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

0 1 2 3 4 5 6 7 8 9 10 11

CDF - Pareto(2,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0 1 2 3 4 5 6 7 8 9 10 11

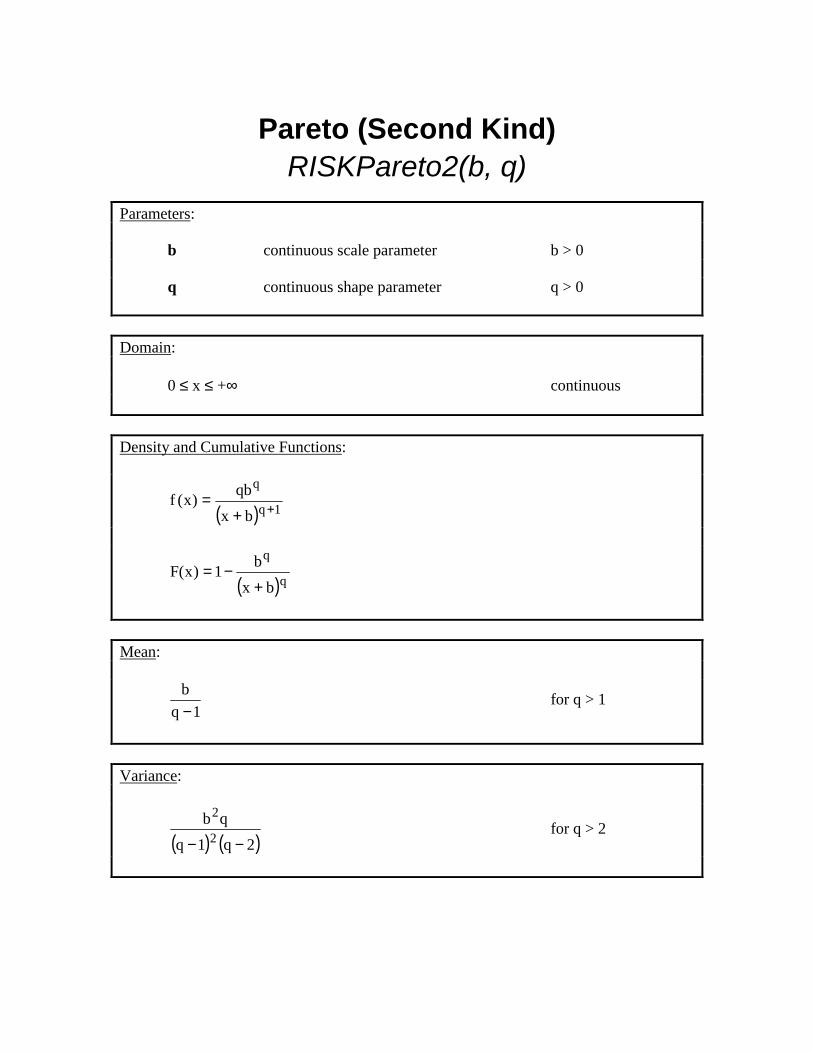

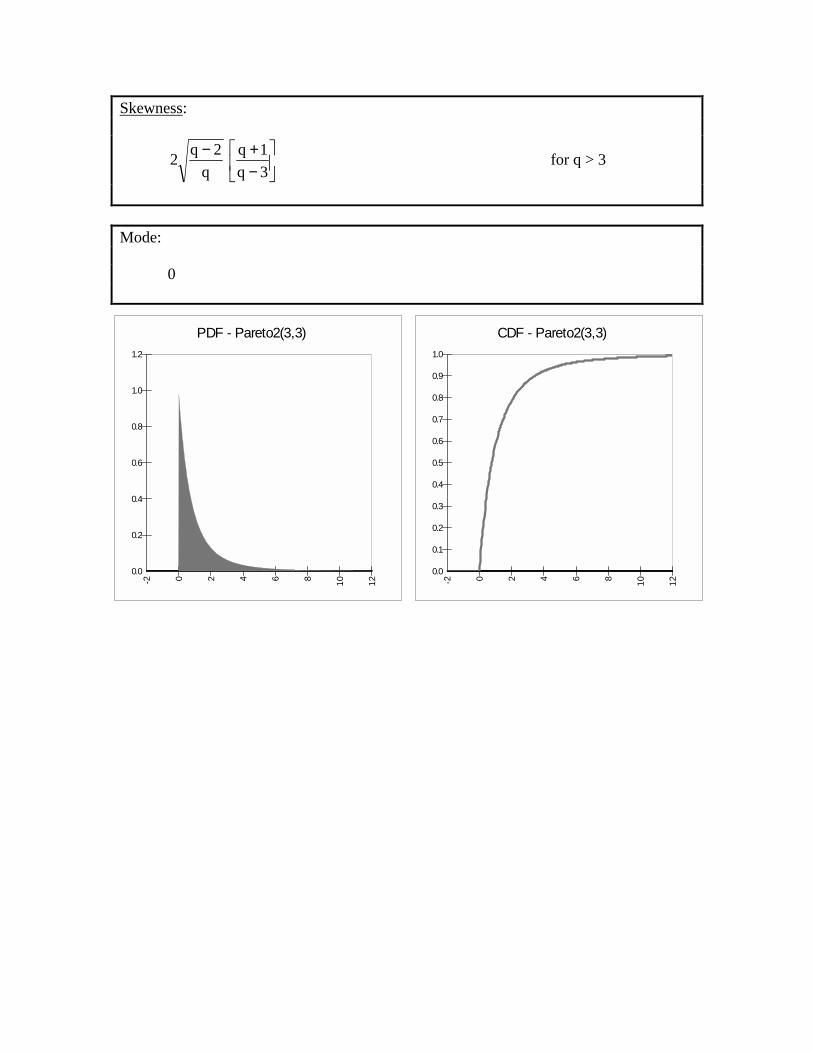

Pareto (Second Kind) RISKPareto2(b, q)

Parameters: b continuous scale parameter b > 0 q continuous shape parameter q > 0

Domain: 0 ≤ x ≤ +∞ continuous

Density and Cumulative Functions:

( ) 1q

q

bxqb)x(f ++

=

bxb1)x(F+

−=

Mean:

1qb−

for q > 1

Variance:

( ) ( )2q1q

qb2

2

−− for q > 2

Skewness:

−+−

3q1q

q2q2 for q > 3

Mode: 0

PDF - Pareto2(3,3)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

-2 0 2 4 6 8 10 12

CDF - Pareto2(3,3)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-2 0 2 4 6 8 10 12

Pearson Type V RISKPearson5(α, β)

Parameters:

αααα continuous shape parameter α > 0

ββββ continous scale parameter β > 0

Domain:

0 ≤ x < +∞ continuous

Density and Cumulative Functions:

( ) ( ) 1

x

xe1)x(f +α

β−

β⋅

αΓβ=

F(x) Has No Closed Form Mean:

1−α

β for α > 1

Variance:

( ) ( )21 2

2

−α−α

β for α > 2

Skewness:

3

24−α−α for α > 3

Kurtosis:

( )( )( )( )43

253−α−α−α+α for α > 4

Mode:

1+α

β

PDF - Pearson5(3,1)

0.0

0.5

1.0

1.5

2.0

2.5

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

CDF - Pearson5(3,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

Pearson Type VI RISKPearson6(α1, α2, β)

Parameters:

αααα1 continuous shape parameter α1 > 0 αααα2 continuous shape parameter α2 > 0

ββββ continuous scale parameter β > 0

Domain:

0 ≤ x < +∞ continuous

Density and Cumulative Functions:

( )( )

21

1

x1

x,B

1)x(f1

21α+α

−α

β

+

β×ααβ

=

F(x) Has No Closed Form.

where B is the Beta Function. Mean:

12

1

−αβα

for α2 > 1

Variance:

( )( ) ( )21

1

22

2

2112

−α−α−α+ααβ

for α2 > 2

Skewness:

( )

−α

−α+α−α+αα

−α3

121

22

2

21

211

2 for α2 > 3

Kurtosis:

( )( )( )

( )( ) ( )

+α+

−α+αα−α

−α−α−α

51

1243

232

211

22

22

2 for α2 > 4

Mode:

( )11

2

1

+α−αβ

for α1 > 1

0 otherwise

PDF - Pearson6(3,3,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

-1 0 1 2 3 4 5 6 7 8 9

CDF - Pearson6(3,3,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-1 0 1 2 3 4 5 6 7 8 9

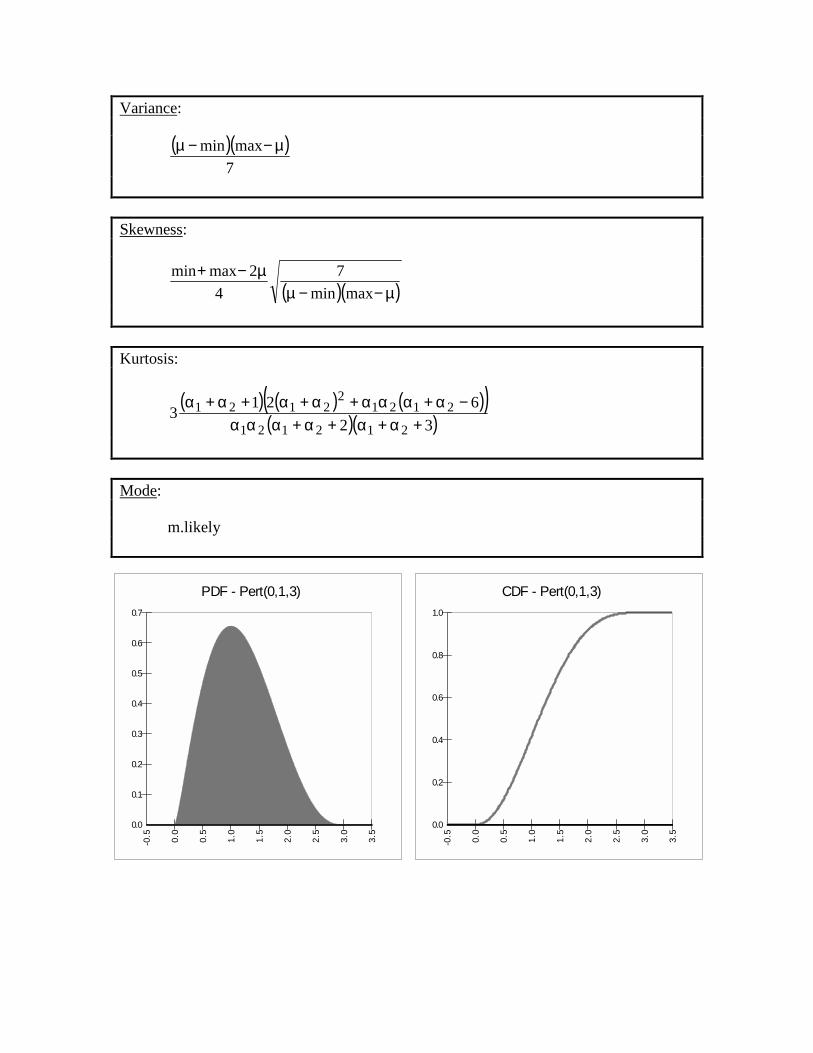

Pert (Beta) RISKPert(min, m.likely, max)

Definitions:

6maxlikely.m4min +⋅+≡µ

−−µ≡α

minmaxmin61

−µ−≡α

minmaxmax62

Parameters: min continuous boundary parameter min < max m.likely continuous parameter min < m.likely < max max continuous boundary parameter Domain: min ≤ x ≤ max continuous

Density and Cumulative Functions:

( ) ( )( ) 12121

1211

minmax),(xmaxminx)x(f −α+α

−α−α

−ααΒ−−=

( ) ( )21z21

21z ,I),(B

,B)x(F αα≡

αααα

= with minmax

minxz−

−≡

where B is the Beta Function and Bz is the Incomplete Beta Function. Mean:

6maxlikely.m4min +⋅+≡µ

Variance:

( )( )7

maxmin µ−−µ

Skewness:

( )( )µ−−µµ−+

maxmin7

42maxmin

Kurtosis:

( ) ( ) ( )( )( )( )32

6213

212121

21212

2121+α+α+α+ααα

−α+ααα+α+α+α+α

Mode: m.likely

PDF - Pert(0,1,3)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

CDF - Pert(0,1,3)

0.0

0.2

0.4

0.6

0.8

1.0

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

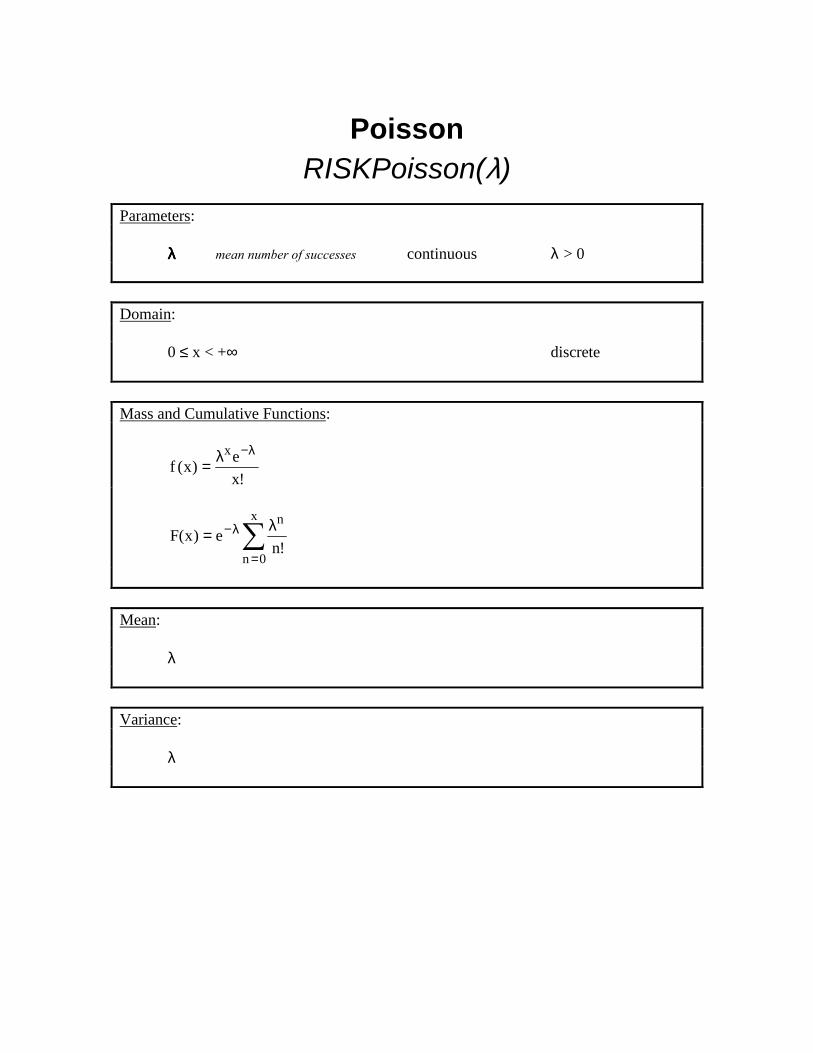

Poisson RISKPoisson(λ)

Parameters: λλλλ mean number of successes continuous λ > 0 Domain: 0 ≤ x < +∞ discrete

Mass and Cumulative Functions:

!xe)x(f

x λ−λ=

∑=

λ− λ=x

0n

n

!ne)x(F

Mean:

λ Variance:

λ

Skewness:

λ1

Kurtosis:

λ+ 13

Mode:

(bimodal) λ and λ+1 (bimodal) if λ is an integer

(unimodal) largest integer less than λ otherwise

PMF - Poisson(3)

0.00

0.05

0.10

0.15

0.20

0.25

-1 0 1 2 3 4 5 6 7 8 9

CDF - Poisson(3)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-1 0 1 2 3 4 5 6 7 8 9

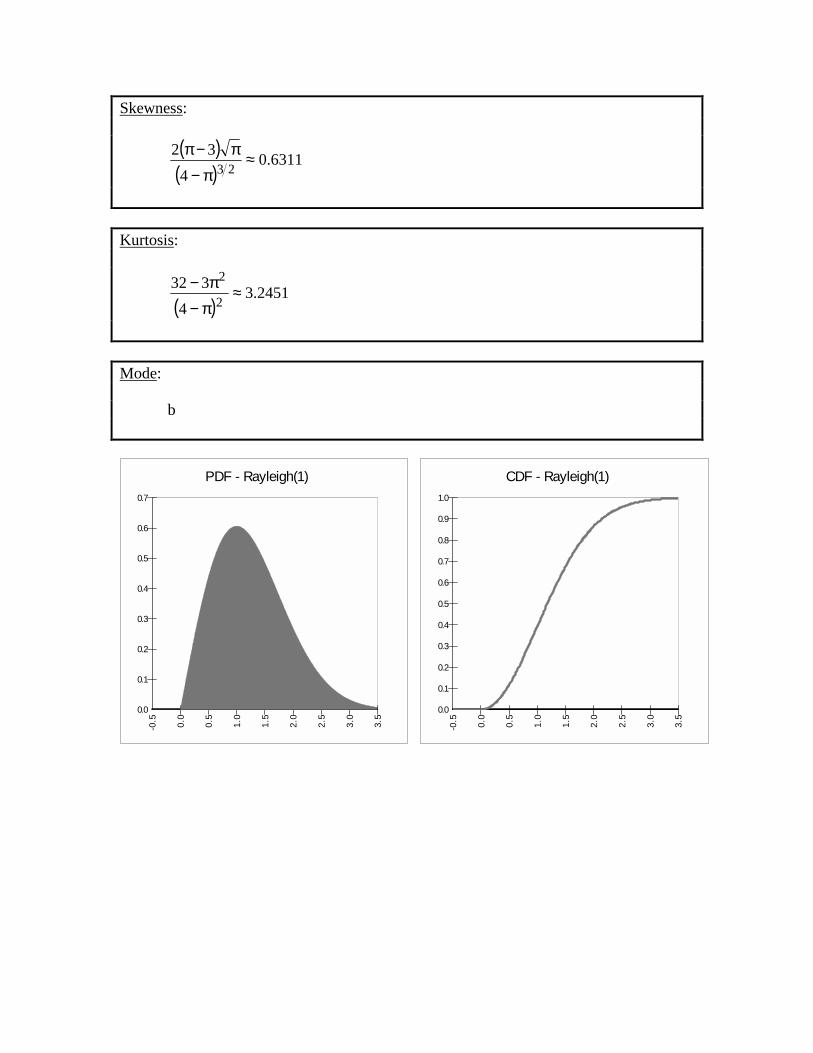

Rayleigh RISKRayleigh(b)

Parameters: b continuous scale parameter b > 0 Domain:

0 ≤ x < +∞ continuous

Density and Cumulative Functions:

2

bx

21

2e

bx)x(f

−

=

2

bx

21

e1)x(F

−

−= Mean:

2b π

Variance:

π−

22b2

Skewness:

( )( )

6311.04

3223

≈π−

π−π

Kurtosis:

( )2451.3

4332

2

2≈

π−

π−

Mode:

b

PDF - Rayleigh(1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

CDF - Rayleigh(1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

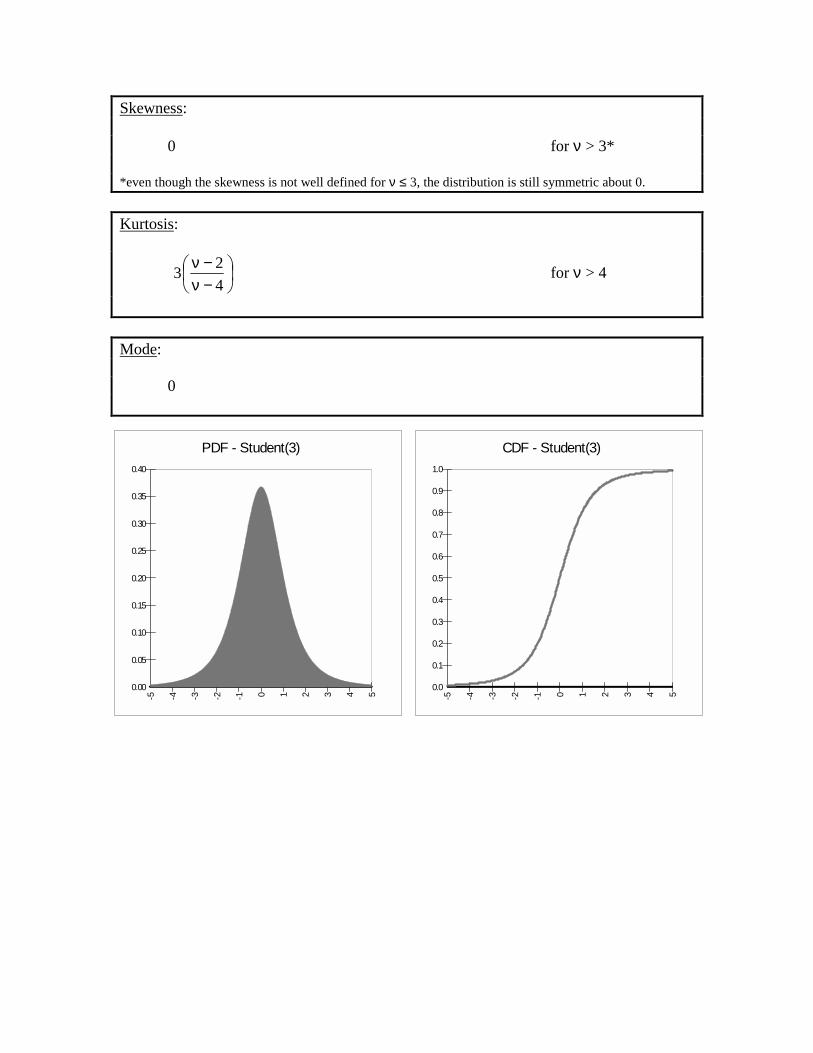

Student’s “t” RISKStudent(ν)

Parameters: νννν the degrees of freedom integer ν > 0

Domain:

-∞ ≤ x ≤ +∞ continuous

Density and Cumulative Functions:

21

2x2

21

1)x(f

+ν

+νν

νΓ

+νΓ

πν=

ν+=

2,

21I1

21)x(F s with 2

2

xxs+ν

≡

where Γ is the Gamma Function and Ix is the Incomplete Beta Function. Mean:

0 for ν > 1* *even though the mean is not well defined for ν = 1, the distribution is still symmetrical about 0. Variance:

2−νν for ν > 2

Skewness:

0 for ν > 3* *even though the skewness is not well defined for ν ≤ 3, the distribution is still symmetric about 0. Kurtosis:

−ν−ν

423 for ν > 4

Mode:

0

PDF - Student(3)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

-5 -4 -3 -2 -1 0 1 2 3 4 5

CDF - Student(3)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-5 -4 -3 -2 -1 0 1 2 3 4 5

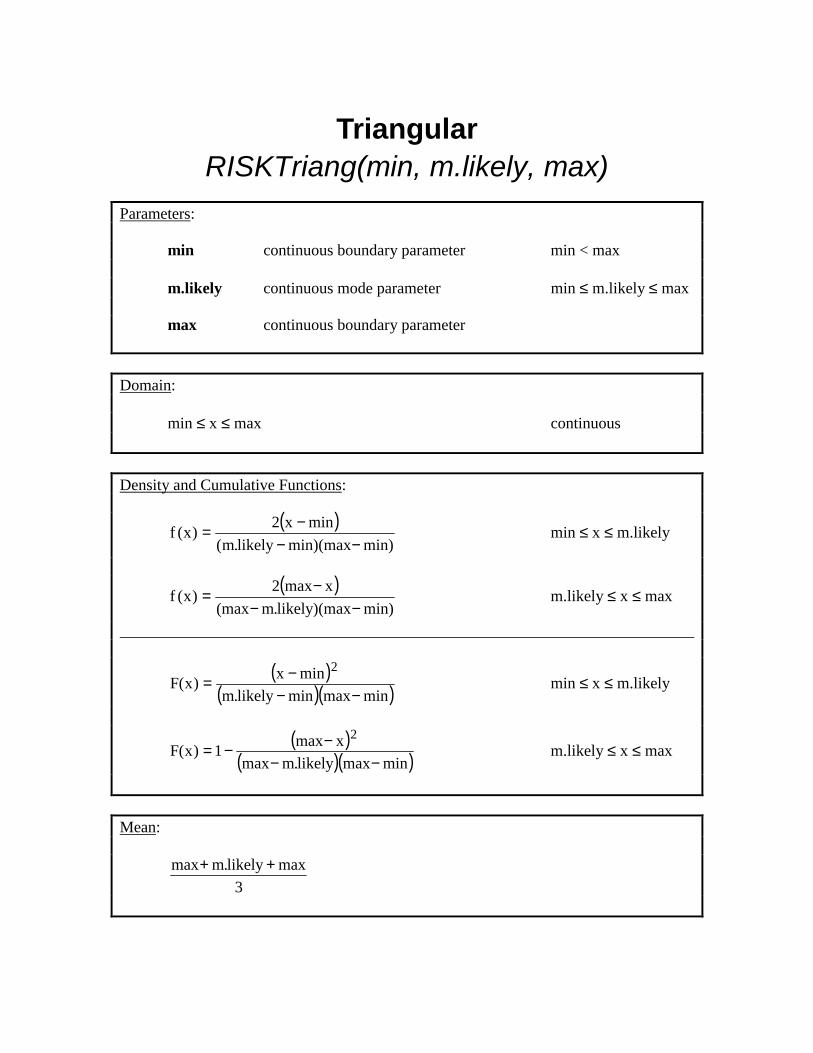

Triangular RISKTriang(min, m.likely, max)

Parameters: min continuous boundary parameter min < max m.likely continuous mode parameter min ≤ m.likely ≤ max max continuous boundary parameter Domain: min ≤ x ≤ max continuous

Density and Cumulative Functions:

( )min)min)(maxlikely.m(

minx2)x(f−−

−= min ≤ x ≤ m.likely

( )

min))(maxlikely.m(maxxmax2)x(f

−−−= m.likely ≤ x ≤ max

( )( )( )minmaxminlikely.m

minx)x(F2

−−−= min ≤ x ≤ m.likely

( )( )( )minmaxlikely.mmax

xmax1)x(F2

−−−−= m.likely ≤ x ≤ max

Mean:

3maxlikely.mmax ++

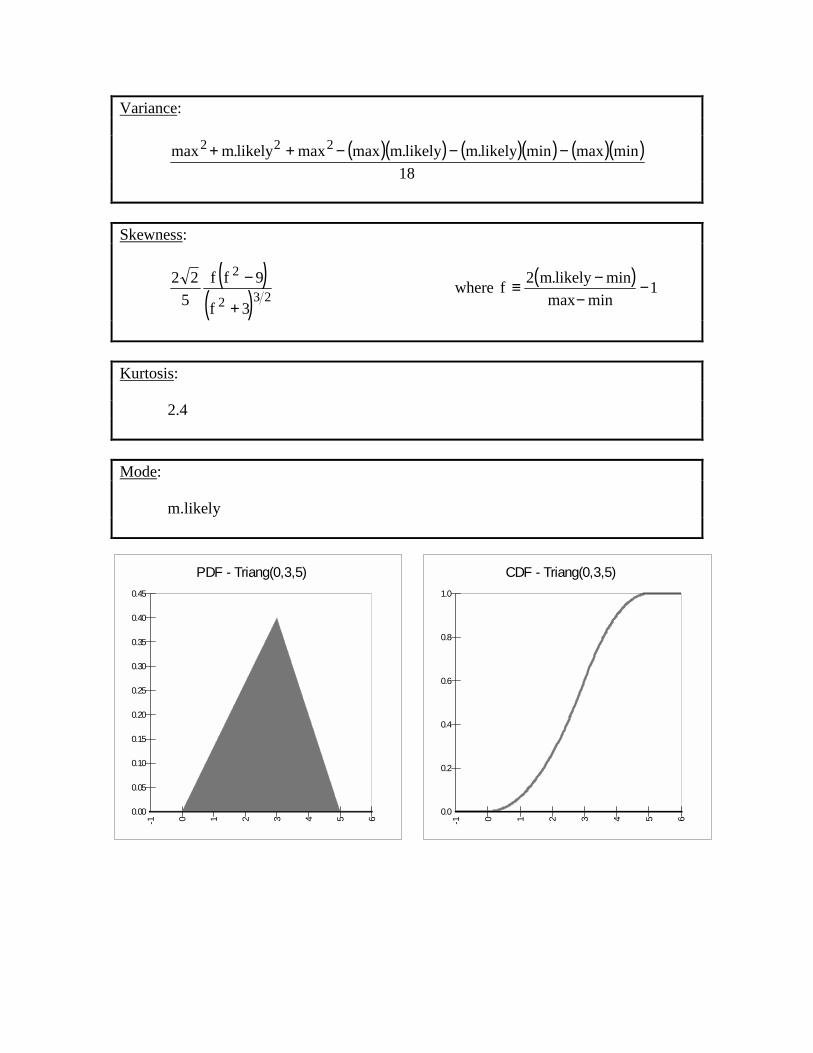

Variance:

( )( ) ( )( ) ( )( )18

minmaxminlikely.mlikely.mmaxmaxlikely.mmax 222 −−−++

Skewness:

( )( ) 232

2

3f

9ff5

22

+

− where ( ) 1minmax

minlikely.m2f −−

−≡

Kurtosis: 2.4 Mode:

m.likely

PDF - Triang(0,3,5)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

-1 0 1 2 3 4 5 6

CDF - Triang(0,3,5)

0.0

0.2

0.4

0.6

0.8

1.0

-1 0 1 2 3 4 5 6

Uniform RISKUniform(min, max)

Parameters: min continuous boundary parameter min < max max continuous boundary parameter Domain: min ≤ x ≤ max continuous

Density and Cumulative Functions:

minmax

1)x(f−

=

minmaxminx)x(F−

−=

Mean:

2minmax−

Variance:

( )12

minmax 2−

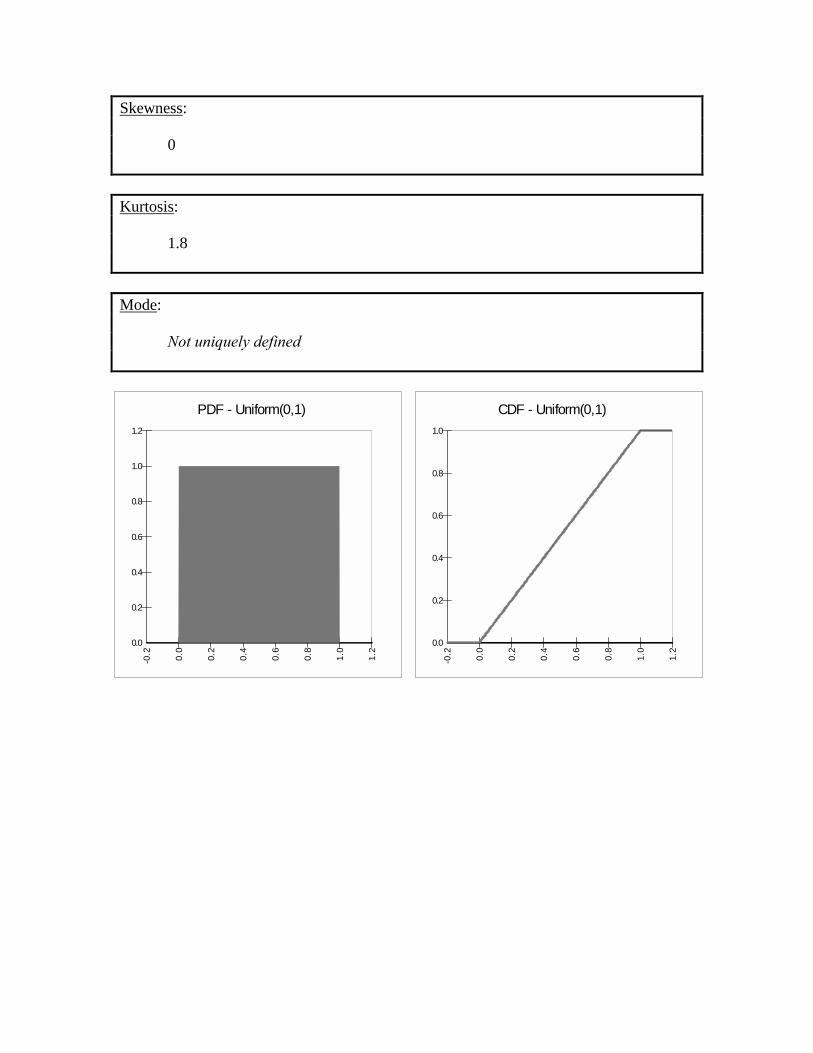

Skewness:

0 Kurtosis:

1.8 Mode:

Not uniquely defined

CDF - Uniform(0,1)

0.0

0.2

0.4

0.6

0.8

1.0

-0.2 0.0

0.2

0.4

0.6

0.8

1.0

1.2

PDF - Uniform(0,1)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

-0.2 0.0

0.2

0.4

0.6

0.8

1.0

1.2

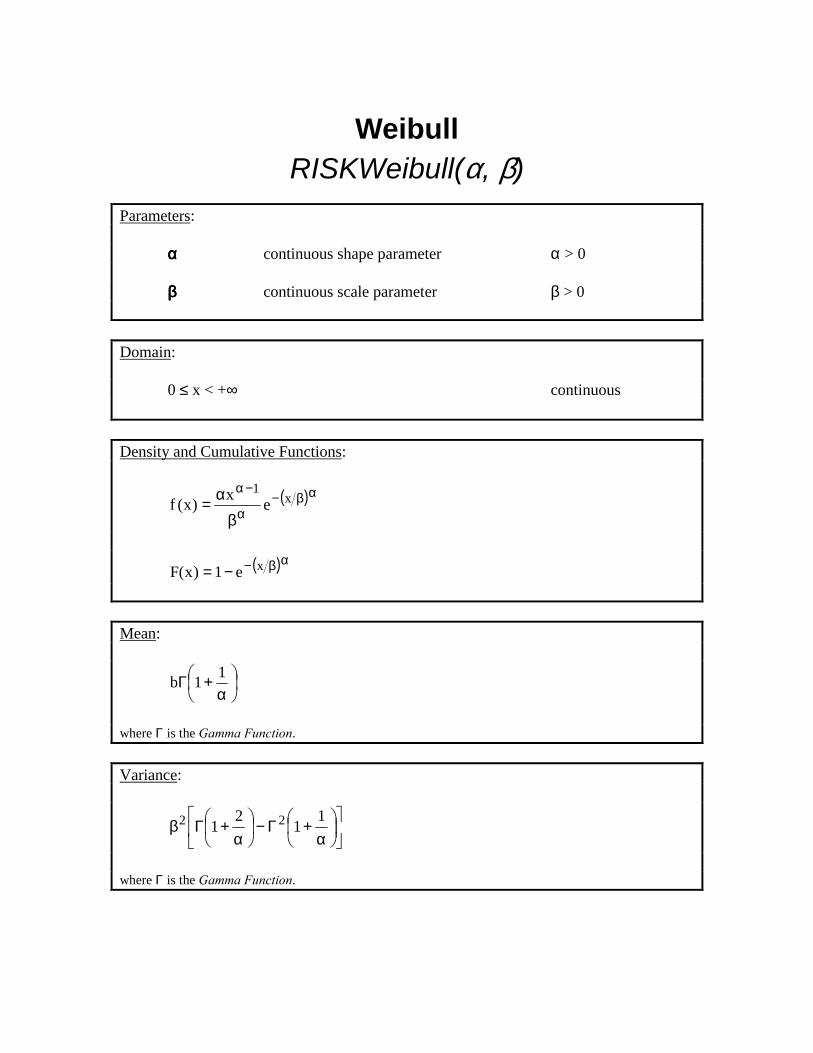

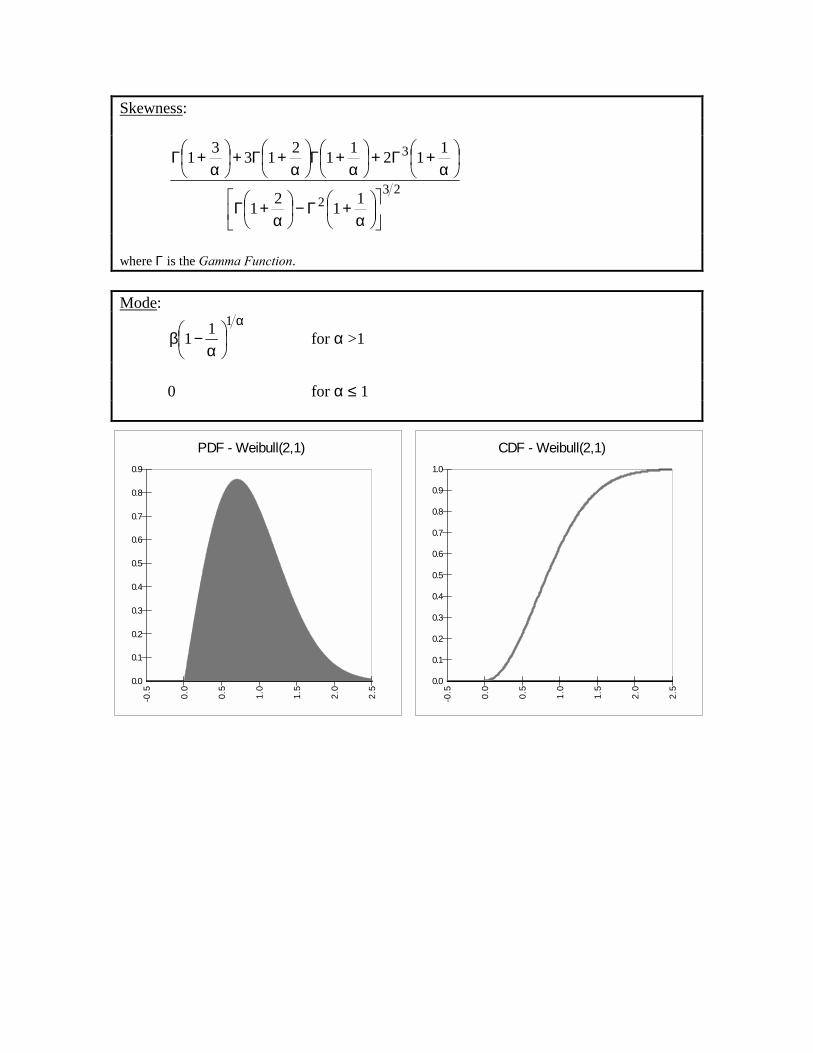

Weibull RISKWeibull(α, β)

Parameters: αααα continuous shape parameter α > 0

ββββ continuous scale parameter β > 0

Domain:

0 ≤ x < +∞ continuous

Density and Cumulative Functions:

( )αβ−α

−α

βα= x

1ex)x(f

( )αβ−−= xe1)x(F Mean:

α+Γ 11b

where Γ is the Gamma Function. Variance:

α+Γ−

α+Γβ

11

21 22

where Γ is the Gamma Function.

Skewness:

232

3

1121

1121121331

α+Γ−

α+Γ

α+Γ+

α+Γ

α+Γ+

α+Γ

where Γ is the Gamma Function. Mode:

α

α−β

111 for α >1

0 for α ≤ 1

PDF - Weibull(2,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

CDF - Weibull(2,1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-0.5 0.0

0.5

1.0

1.5

2.0

2.5

![UK Domain Average Windstorm Risk S] risk non-SJ risk Wind ...sws98slg/Downloads/RMetS-NCAS-2016-StingJet... · UK Domain Average Windstorm Risk S] risk non-SJ risk Wind speed threshold](https://static.fdocument.org/doc/165x107/5bfce26209d3f264188c4657/uk-domain-average-windstorm-risk-s-risk-non-sj-risk-wind-sws98slgdownloadsrmets-ncas-2016-stingjet.jpg)