Σπύρος Νικολόπουλος & Παναγιώτης Τσαρχόπουλος - Βελτιώνω την πόλη μου – ολοκληρωμένη πλατφόρμα για

Upload

starttech-venturesCategory

view

198download

0

The better the question. The bet ter the answer �.The better the world works.

New IFRS 4 Phase II is on the way:Impact & challenges for insurers

23 June 2016

Κωνσταντίνος ΝικολόπουλοςExecutive Director, Actuarial Leader EY Greece

Page 2

Today’s Agenda

► From Solvency II to new IFRS

► IFRS 9

► IFRS 4.II

► Linkage of Solvency II with IFRS 4.II and IFRS 9

23 June 2016 New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 3

From Solvency II to new IFRS

23 June 2016 New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 4

From Solvency II to new IFRS – Introduction

23 June 2016

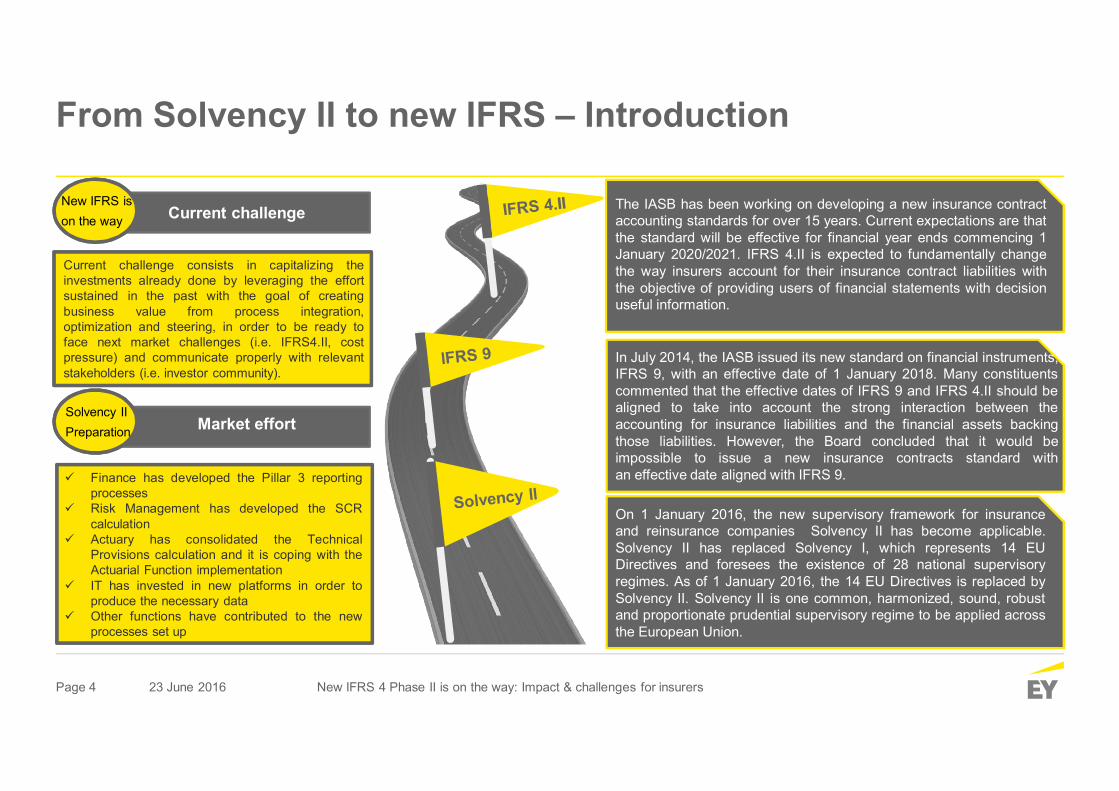

The IASB has been working on developing a new insurance contractaccounting standards for over 15 years. Current expectations are thatthe standard will be effective for financial year ends commencing 1January 2020/2021. IFRS 4.II is expected to fundamentally changethe way insurers account for their insurance contract liabilities withthe objective of providing users of financial statements with decisionuseful information.

In July 2014, the IASB issued its new standard on financial instruments,IFRS 9, with an effective date of 1 January 2018. Many constituentscommented that the effective dates of IFRS 9 and IFRS 4.II should bealigned to take into account the strong interaction between theaccounting for insurance liabilities and the financial assets backingthose liabilities. However, the Board concluded that it would beimpossible to issue a new insurance contracts standard withan effective date aligned with IFRS 9.

Solvency II

IFRS Phase II

IFRS 9

On 1 January 2016, the new supervisory framework for insuranceand reinsurance companies Solvency II has become applicable. Solvency II has replaced Solvency I, which represents 14 EUDirectives and foresees the existence of 28 national supervisoryregimes. As of 1 January 2016, the 14 EU Directives is replaced bySolvency II. Solvency II is one common, harmonized, sound, robustand proportionate prudential supervisory regime to be applied acrossthe European Union.

Current challenge

Current challenge consists in capitalizing theinvestments already done by leveraging the effortsustained in the past with the goal of creatingbusiness value from process integration,optimization and steering, in order to be ready toface next market challenges (i.e. IFRS4.II, costpressure) and communicate properly with relevantstakeholders (i.e. investor community).

New IFRS is New IFRS is on the way

Market effortSolvency II PreparationSolvency II Preparation

Finance has developed the Pillar 3 reportingprocesses

Risk Management has developed the SCRcalculation

Actuary has consolidated the TechnicalProvisions calculation and it is coping with theActuarial Function implementation

IT has invested in new platforms in order toproduce the necessary data

Other functions have contributed to the newprocesses set up

New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 5

From Solvency II to new IFRS – Roadmap

23 June 2016

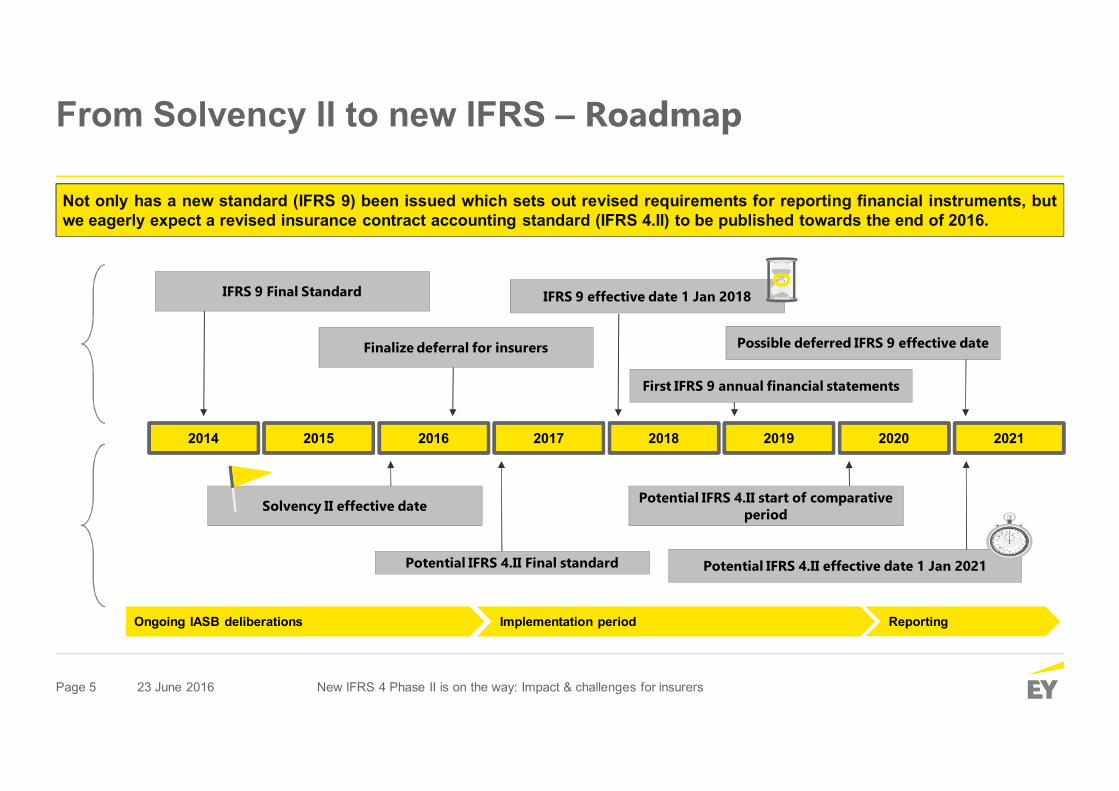

Not only has a new standard (IFRS 9) been issued which sets out revised requirements for reporting financial instruments, butwe eagerly expect a revised insurance contract accounting standard (IFRS 4.II) to be published towards the end of 2016.

Ongoing IASB deliberations Implementation period Reporting

IFRS 4.II

IFRS 9

2014 2015 2016 2017 2018 2019 2020 2021

IFRS 9 Final Standard

Potential IFRS 4.II Final standard

Finalize deferral for insurers

Potential IFRS 4.II start of comparative period

Possible deferred IFRS 9 effective date

IFRS 9 effective date 1 Jan 2018

Potential IFRS 4.II effective date 1 Jan 2021

Solvency II effective date

First IFRS 9 annual financial statements

New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 6

From Solvency II to new IFRS – Key Differences

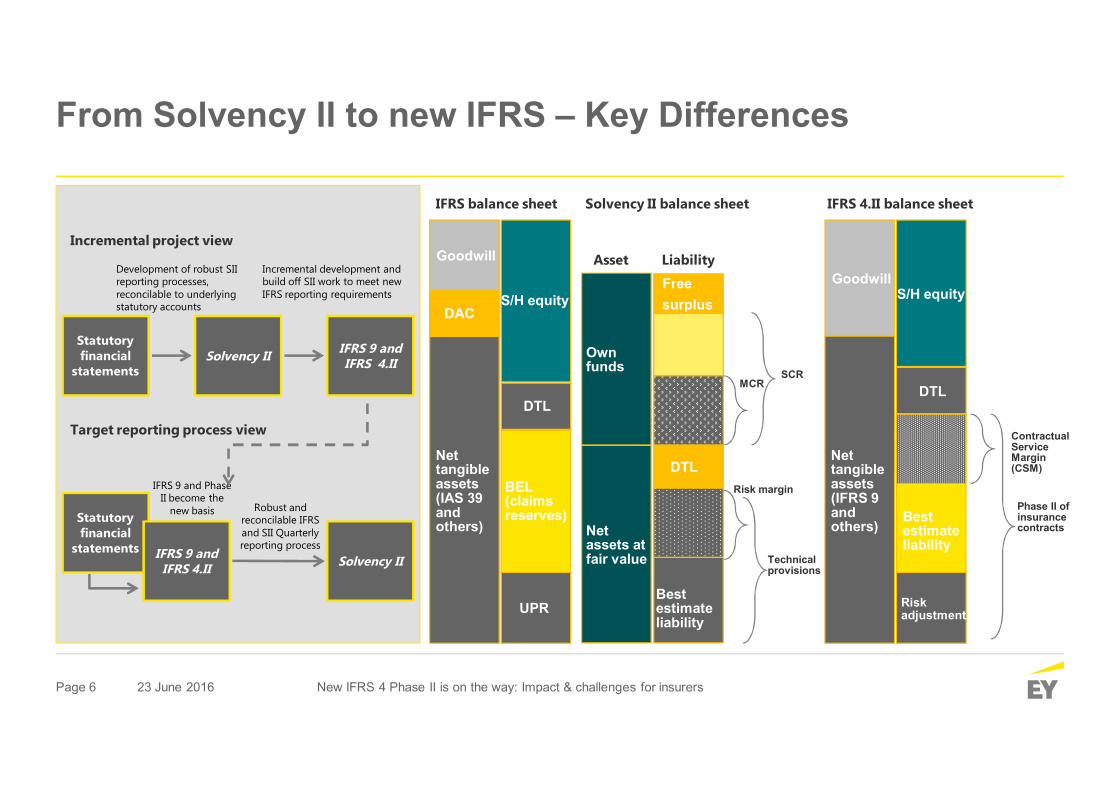

IFRS 9 and IFRS 4.II

Statutory financial

statementsSolvency II

Development of robust SII reporting processes, reconcilable to underlying statutory accounts

Incremental development and build off SII work to meet new IFRS reporting requirements

Statutory financial

statements IFRS 9 and IFRS 4.II Solvency II

IFRS 9 and Phase II become the

new basis Robust and reconcilable IFRS and SII Quarterly reporting process

Incremental project view

Target reporting process view

DAC

Net tangible assets (IAS 39 and others)

Goodwill

S/H equity

BEL (claims reserves)

UPR

DTL

IFRS balance sheet

Net assets at fair value

Own funds

Asset

Best estimate liability

Risk margin

DTL

Free surplus

MCRSCR

Technical provisions

Liability

Solvency II balance sheet

Net tangible assets (IFRS 9 and others)

Goodwill

Best estimate liability

DTL

IFRS 4.II balance sheet

Contractual Service Margin (CSM)

Phase II of insurance contracts

23 June 2016

S/H equity

Risk adjustment

New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 7

IFRS 9

23 June 2016 New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 8

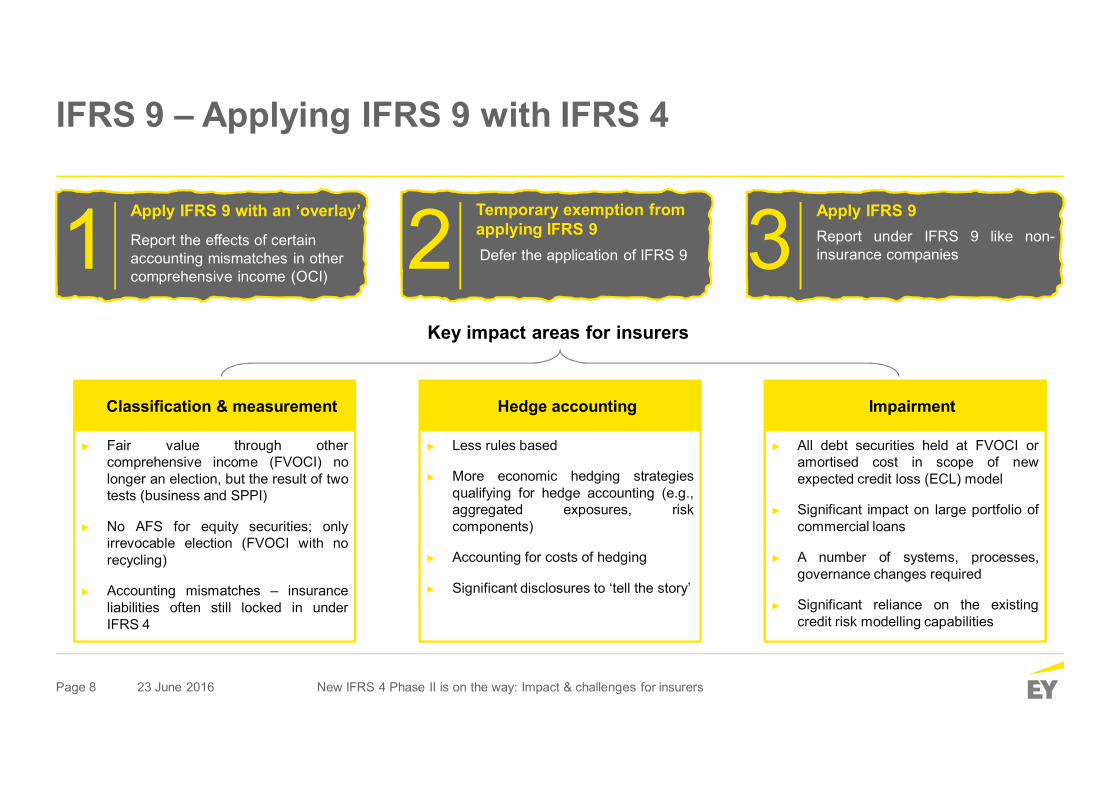

IFRS 9 – Applying IFRS 9 with IFRS 4

Classification & measurement

► Fair value through othercomprehensive income (FVOCI) nolonger an election, but the result of twotests (business and SPPI)

► No AFS for equity securities; onlyirrevocable election (FVOCI with norecycling)

► Accounting mismatches – insuranceliabilities often still locked in underIFRS 4

Impairment

► All debt securities held at FVOCI oramortised cost in scope of newexpected credit loss (ECL) model

► Significant impact on large portfolio ofcommercial loans

► A number of systems, processes,governance changes required

► Significant reliance on the existingcredit risk modelling capabilities

Hedge accounting

► Less rules based

► More economic hedging strategiesqualifying for hedge accounting (e.g.,aggregated exposures, riskcomponents)

► Accounting for costs of hedging

► Significant disclosures to ‘tell the story’

23 June 2016

Apply IFRS 9 with an ‘overlay’Report the effects of certain accounting mismatches in other comprehensive income (OCI)

1 Temporary exemption from applying IFRS 9 Defer the application of IFRS 9 2 Apply IFRS 9

Report under IFRS 9 like non-insurance companies3

Key impact areas for insurers

New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 9

IFRS 4.II

23 June 2016 New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 10

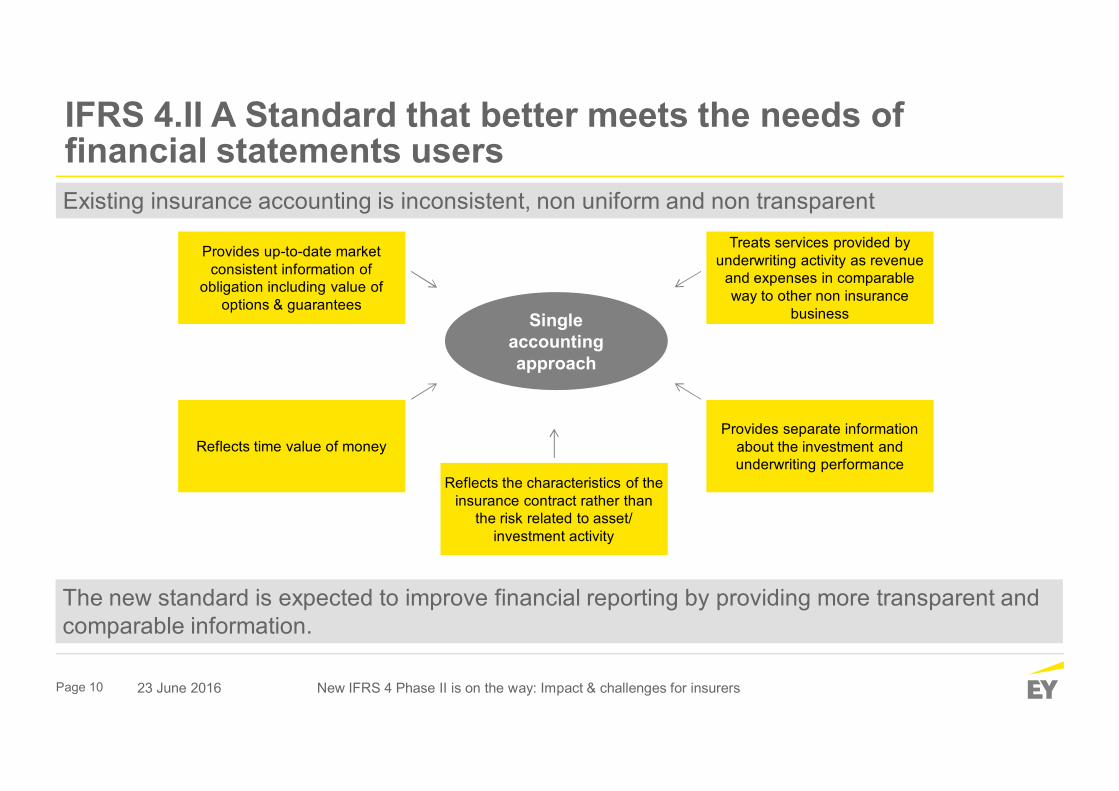

IFRS 4.II A Standard that better meets the needs of financial statements users

Single accounting approach

Provides up-to-date market consistent information of

obligation including value of options & guarantees

Reflects time value of money

Treats services provided by underwriting activity as revenue

and expenses in comparable way to other non insurance

business

Provides separate information about the investment and underwriting performance

Reflects the characteristics of the insurance contract rather than

the risk related to asset/ investment activity

Existing insurance accounting is inconsistent, non uniform and non transparent

23 June 2016 New IFRS 4 Phase II is on the way: Impact & challenges for insurers

The new standard is expected to improve financial reporting by providing more transparent and comparable information.

Page 11

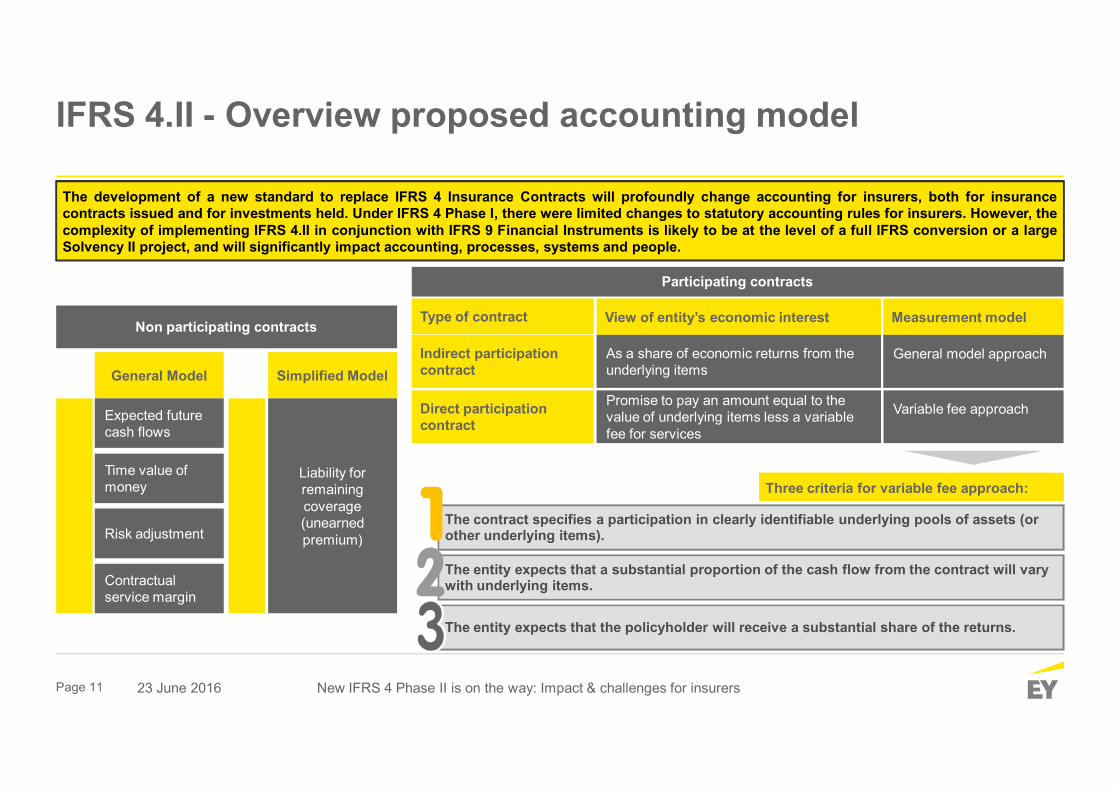

IFRS 4.II - Overview proposed accounting model

The development of a new standard to replace IFRS 4 Insurance Contracts will profoundly change accounting for insurers, both for insurancecontracts issued and for investments held. Under IFRS 4 Phase I, there were limited changes to statutory accounting rules for insurers. However, thecomplexity of implementing IFRS 4.II in conjunction with IFRS 9 Financial Instruments is likely to be at the level of a full IFRS conversion or a largeSolvency II project, and will significantly impact accounting, processes, systems and people.

General Model

Expected future cash flows

Time value of money

Risk adjustment

Contractual service marginBuilding block approach

Simplified Model

Liability for remaining coverage (unearned premium)Premium allocation approach

Non participating contracts

23 June 2016 New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Participating contracts

Direct participation contract

Indirect participation contract

View of entity’s economic interest Measurement model

As a share of economic returns from the underlying items

General model approach

Promise to pay an amount equal to the value of underlying items less a variable fee for services

Variable fee approach

Type of contract

Three criteria for variable fee approach:

The contract specifies a participation in clearly identifiable underlying pools of assets (or other underlying items).

The entity expects that the policyholder will receive a substantial share of the returns.

The entity expects that a substantial proportion of the cash flow from the contract will vary with underlying items.

Page 12

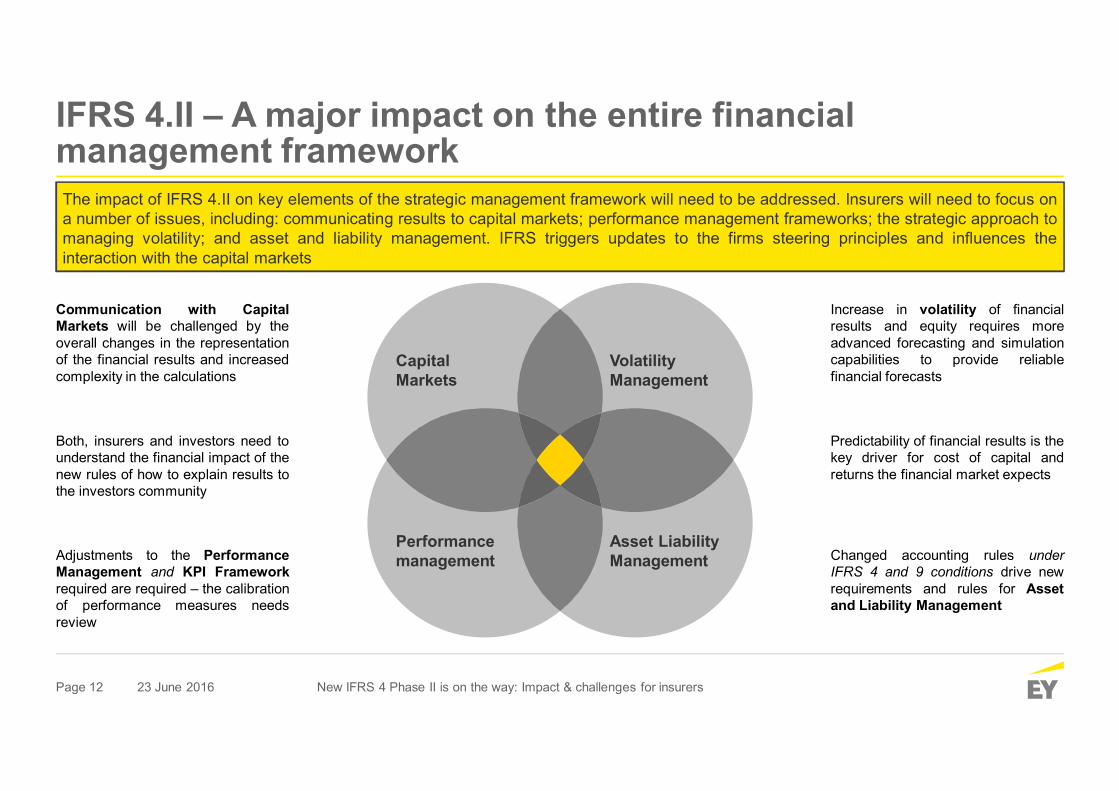

IFRS 4.II – A major impact on the entire financial management frameworkThe impact of IFRS 4.II on key elements of the strategic management framework will need to be addressed. Insurers will need to focus ona number of issues, including: communicating results to capital markets; performance management frameworks; the strategic approach tomanaging volatility; and asset and liability management. IFRS triggers updates to the firms steering principles and influences theinteraction with the capital markets

Capital Markets

Volatility Management

Performance management

Asset Liability Management

Communication with CapitalMarkets will be challenged by theoverall changes in the representationof the financial results and increasedcomplexity in the calculations

Both, insurers and investors need tounderstand the financial impact of thenew rules of how to explain results tothe investors community

Adjustments to the PerformanceManagement and KPI Frameworkrequired are required – the calibrationof performance measures needsreview

Increase in volatility of financialresults and equity requires moreadvanced forecasting and simulationcapabilities to provide reliablefinancial forecasts

Predictability of financial results is thekey driver for cost of capital andreturns the financial market expects

Changed accounting rules underIFRS 4 and 9 conditions drive newrequirements and rules for Assetand Liability Management

23 June 2016 New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 13

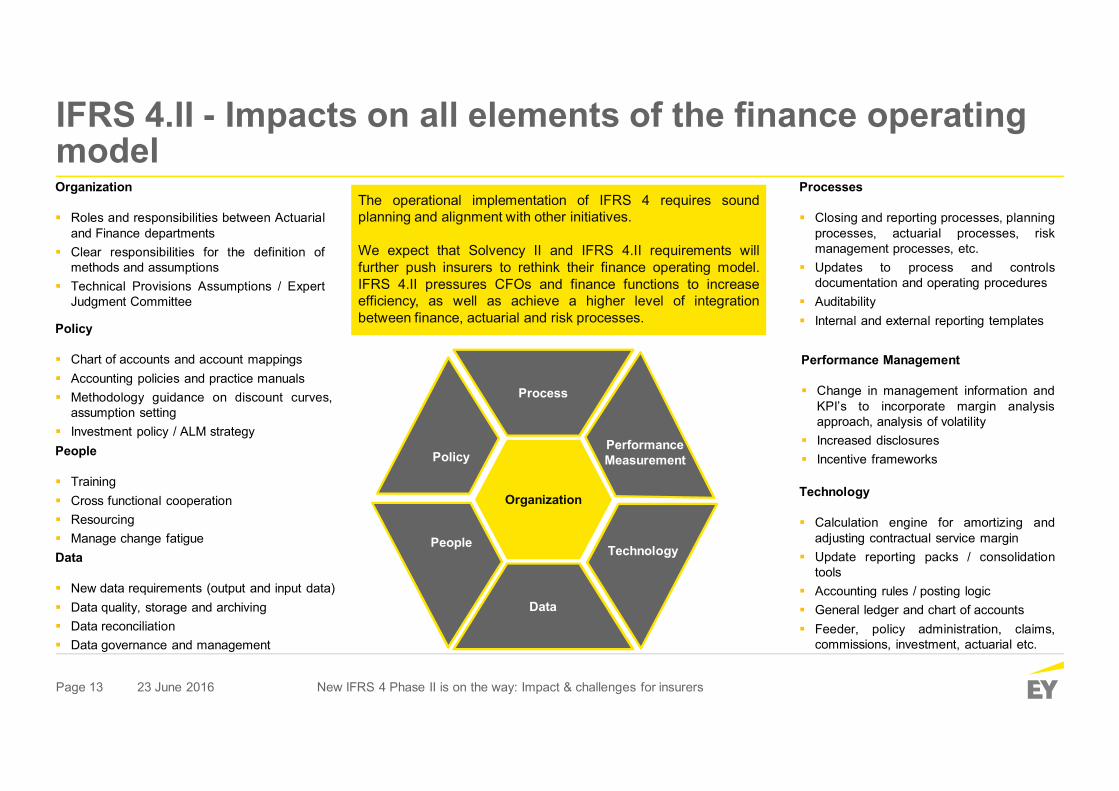

IFRS 4.II - Impacts on all elements of the finance operating model

Process

Organization

Data

Performance Measurement

Technology

Policy

People

Policy

Chart of accounts and account mappings Accounting policies and practice manuals Methodology guidance on discount curves,

assumption setting Investment policy / ALM strategy

Data

New data requirements (output and input data) Data quality, storage and archiving Data reconciliation Data governance and management

Performance Management

Change in management information andKPI’s to incorporate margin analysisapproach, analysis of volatility

Increased disclosures Incentive frameworks

Technology

Calculation engine for amortizing andadjusting contractual service margin

Update reporting packs / consolidationtools

Accounting rules / posting logic General ledger and chart of accounts Feeder, policy administration, claims,

commissions, investment, actuarial etc.

Processes

Closing and reporting processes, planningprocesses, actuarial processes, riskmanagement processes, etc.

Updates to process and controlsdocumentation and operating procedures

Auditability Internal and external reporting templates

People

Training Cross functional cooperation Resourcing Manage change fatigue

Organization

Roles and responsibilities between Actuarialand Finance departments

Clear responsibilities for the definition ofmethods and assumptions

Technical Provisions Assumptions / ExpertJudgment Committee

The operational implementation of IFRS 4 requires soundplanning and alignment with other initiatives.

We expect that Solvency II and IFRS 4.II requirements willfurther push insurers to rethink their finance operating model.IFRS 4.II pressures CFOs and finance functions to increaseefficiency, as well as achieve a higher level of integrationbetween finance, actuarial and risk processes.

The operational implementation of IFRS 4 requires soundplanning and alignment with other initiatives.

We expect that Solvency II and IFRS 4.II requirements willfurther push insurers to rethink their finance operating model.IFRS 4.II pressures CFOs and finance functions to increaseefficiency, as well as achieve a higher level of integrationbetween finance, actuarial and risk processes.

23 June 2016 New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 14

Linkage of Solvency II with IFRS 4.II and IFRS 9

23 June 2016 New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 15

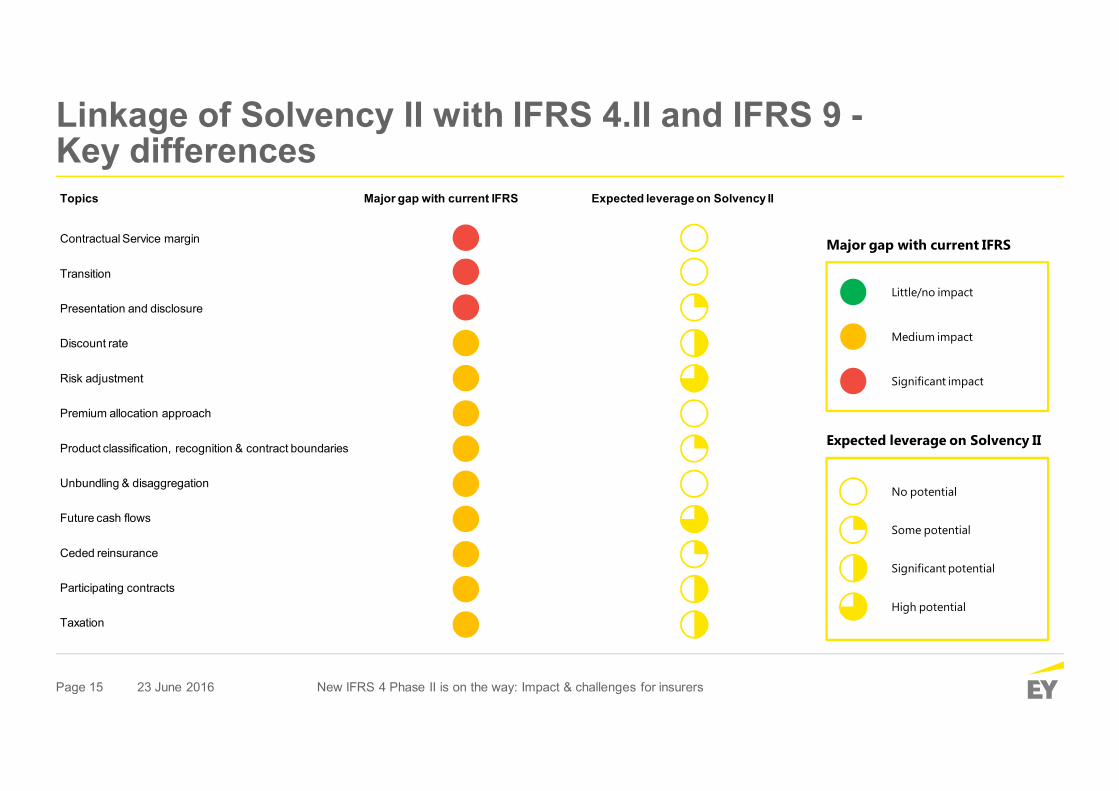

Linkage of Solvency II with IFRS 4.II and IFRS 9 -Key differencesTopics Major gap with current IFRS Expected leverage on Solvency II

Contractual Service margin

Transition

Presentation and disclosure

Discount rate

Risk adjustment

Premium allocation approach

Product classification, recognition & contract boundaries

Unbundling & disaggregation

Future cash flows

Ceded reinsurance

Participating contracts

Taxation

Major gap with current IFRS

Medium impact

Significant impact

Little/no impact

Expected leverage on Solvency II

Some potential

Significant potential

No potential

High potential

23 June 2016 New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Page 16

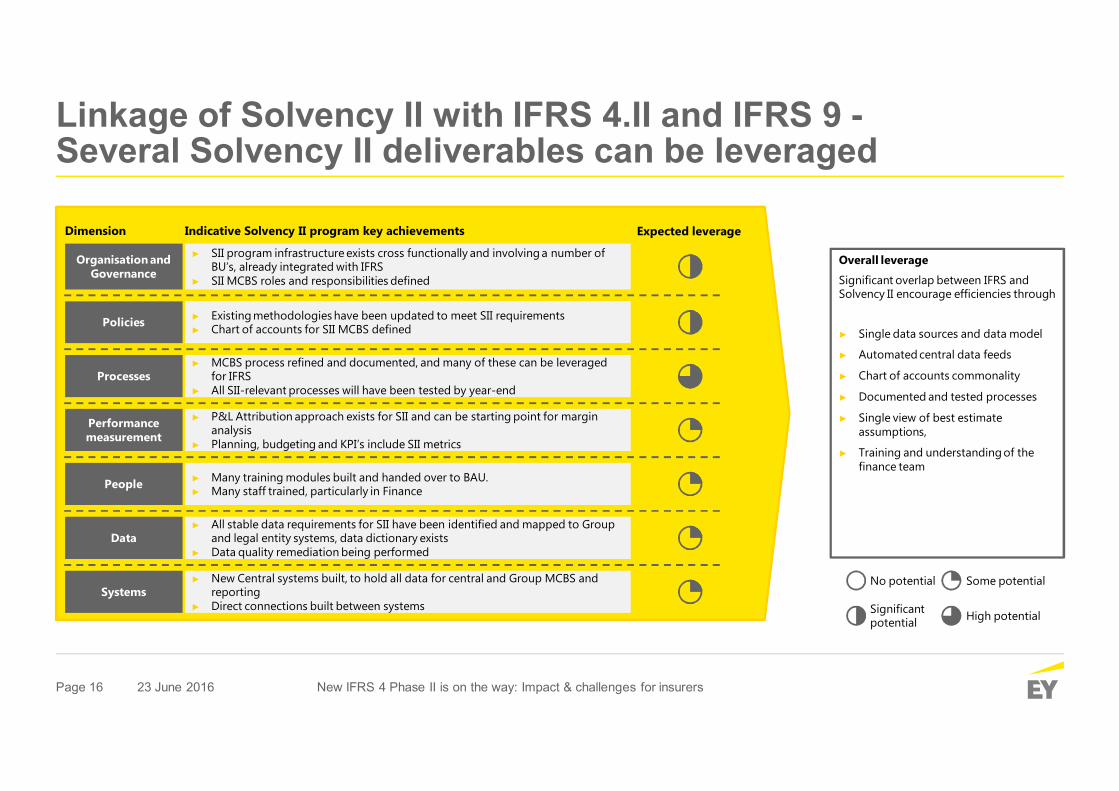

Linkage of Solvency II with IFRS 4.II and IFRS 9 -Several Solvency II deliverables can be leveraged

Overall leverageSignificant overlap between IFRS and Solvency II encourage efficiencies through

► Single data sources and data model

► Automated central data feeds

► Chart of accounts commonality

► Documented and tested processes

► Single view of best estimate assumptions,

► Training and understanding of the finance team

No potential Some potential

Significant potential High potential

Dimension

Organisation and Governance

► SII program infrastructure exists cross functionally and involving a number of BU’s, already integrated with IFRS

► SII MCBS roles and responsibilities defined

Policies ► Existing methodologies have been updated to meet SII requirements► Chart of accounts for SII MCBS defined

Processes► MCBS process refined and documented, and many of these can be leveraged

for IFRS► All SII-relevant processes will have been tested by year-end

Performance measurement

► P&L Attribution approach exists for SII and can be starting point for margin analysis

► Planning, budgeting and KPI’s include SII metrics

People ► Many training modules built and handed over to BAU.► Many staff trained, particularly in Finance

► New Central systems built, to hold all data for central and Group MCBS and reporting

► Direct connections built between systemsSystems

Data ► All stable data requirements for SII have been identified and mapped to Group

and legal entity systems, data dictionary exists► Data quality remediation being performed

Indicative Solvency II program key achievements Expected leverage

23 June 2016 New IFRS 4 Phase II is on the way: Impact & challenges for insurers

Thank you

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY's Advisory Services In a world of unprecedented change, EY Advisory believes a better working world means solving big, complex industry issues and capitalizing on opportunities to help deliver outcomes that grow, optimize and protect clients’ businesses. From C-suite and functional leaders of Fortune 100 multinationals to disruptive innovators and emerging market small and medium sized enterprises, EY Advisory teams with clients — from strategy through execution — to help them design better outcomes and deliver long-lasting results. A global mindset, diversity and collaborative culture inspires EY consultants to ask better questions. They work with the client, as well as an ecosystem of internal and external experts, to co-create more innovative answers. Together, EY helps clients’ businesses work better. The better the question. The better the answer. The better the world works.

© 2016 EYAll Rights Reserved.