Lecture 5 [0.3cm] Linear Income Taxes - CREST

40

Lecture 5 Linear Income Taxes St´ ephane Gauthier 25 mars 2008

Transcript of Lecture 5 [0.3cm] Linear Income Taxes - CREST

![Page 1: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/1.jpg)

Lecture 5

Linear Income Taxes

Stephane Gauthier

25 mars 2008

![Page 2: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/2.jpg)

Introduction

![Page 3: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/3.jpg)

The framework

Individuals are indexed by a parameter θ, θ ≥ 0.

This parameter will be later interpreted as individual ’productivity’.

We let θ ∼ F (·), with F : R→ [0, 1], F in C1.

By assumption, θ is given, i.e. it cannot be changed.

Individual θ has before-tax income y(θ).

If the social planner can observe θ, then the tax t(θ) is allowed.

It is a lump-sum tax.

The net income of individual θ is y(θ)− t(θ).

In this illustration, preferences are identical across individuals (they only

differ according to productivity θ) : individual θ gets u(y(θ)− t(θ)).

![Page 4: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/4.jpg)

The planner problem

The planner problem is to maximize a (unweighted) ’utilitarian’ social

welfare function ∫ ∞0

u(y(θ)− t(θ))dF (θ)

subject to ∫ ∞0

t(θ)dF (θ) ≥ R.

The FOC with respect to t(θ) writes u′(y(θ)− t(θ)) = λ, where the

marginal social cost of public funds λ is independent of θ.

If u′′ < 0, then net incomes y(θ)− t(θ) are all equalized. This fits the

’equal sacrifice’ principle according to which ’sacrifices [. . .] should be

made to bear as nearly as possible with the same pressure upon all.’ (J.S.

Mill, 1848, Principles of Political Economy, Book V, Ch. II, §2).

![Page 5: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/5.jpg)

Labor supply and disincentive effects of taxation

Let preferences be represented by u(c)− v(l), with y = θl and

c = θl − t(θ). Again, this tax has only income effects.

When such effects only bear on consumption, labor supply becomes

independent of taxes. This is the case if utility is quasi-linear in

consumption, u(c) = c . Then, individual θ chooses l(θ) which maximizes

θl − t(θ)− v(l), i.e. such that v ′(l(θ)) = θ, and there is no disincentive

effects of taxation.

For u(c)− v(l), with u′′ < 0 and v ′′ > 0, it is readily verified that

u′(c(θ)) = λ and v ′(l(θ)) = λθ at social optimum. Thus, after-tax

incomes are equalized and labor increases with productivity (and so, the

t(θ) increases with θ). If leisure is normal, labor increases with the tax !

![Page 6: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/6.jpg)

Information and disincentive effects of taxation

Disincentive effects of taxation arise when the planner is constrained to

rely on income, θl , instead of productivity itself, because e.g. the planner

cannot directly observe productivity θ and uses income as a signal of

productivity.

This is the starting point of Mirrlees (1971) : the tax now bears on

income and no longer on productivity, i.e. t = t(θl).

Then, indeed, c = θl − t(θl), which shows that taxation has both

I a substitution effect (the ’price’ of labor is θ(1− t ′(θl)) for individual

θ who already works l hours), through which individuals may

influence the amount of taxes they pay (if t ′ > 0, by working less),

I and an income effect (even in the quasi-linear case).

![Page 7: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/7.jpg)

Some limits to redistribution

What happens if the first-best income tax schedule (which leads to

c(θ) = c and l ′(θ) ≥ 0 ) is proposed to individuals ?

To grasp some intuition, consider the two-productivity case, with θ1 < θ2.

Given the observability hypothesis, the planner is only able to assign a

pair (c1, y1) to individual θ1 and (c2, y2) to individual θ2, with

c1 = c2 ≡ c and y1/θ2 < l1 = y1/θ1 < l2 = y2/θ2.

Then, the more productive individual does prefer to claim to have the

lowest productivity :

u(c)− v

(y1

θ2

)> u(c)− v

(y2

θ2

),

thus highlighting some limits to redistribution due to informational

constraints : the first-best optimum is no longer achievable.

![Page 8: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/8.jpg)

Le principe de taxation

Ce n’est qu’une illustration (dans le cas quasi-lineaire) d’un principe plus

general du a Guesnerie (1981) et Rochet (1979).

Soit θ ∈ Θ et (c(·), y(·),Θ) un mecanisme direct.

Il est revelateur si :

θ ∈ Θ→ (c(θ), y(θ)) ∈ Θ2

c(θ)− v

(y(θ)

θ

)≥ c(θ′)− v

(y(θ′)

θ

)∀(θ, θ′).

Et l’on a :

Principe de taxation (Partie 1). Tout mecanisme direct revelateur peut

etre decentralise par une fonction de taxe.

![Page 9: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/9.jpg)

Si y(θ) = y(θ′) pour une paire (θ, θ′), alors on doit avoir c(θ) = c(θ′).

En effet, le mecanisme etant revelateur,

c(θ)− v

(y(θ)

θ

)≥ c(θ′)−v

(y(θ′)

θ

)= c(θ′)− v

(y(θ)

θ

)⇒ c(θ) ≥ c(θ′),

et

c(θ′)− v

(y(θ′)

θ′

)= c(θ′)−v

(y(θ)

θ′

)≥ c(θ)− v

(y(θ)

θ′

)⇒ c(θ) ≤ c(θ′),

ce qui implique que c(θ) = c(θ′).

![Page 10: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/10.jpg)

On se donne maintenant une fonction de taxe t(y) telle que

c = y − t(y). On la construit de la facon suivante :

t(y) = y(θ)− c(θ) si y = y(θ), θ ∈ Θ,

t(y) = +∞ sinon.

On veut montrer que l’agent θ choisit y(θ) = θl(θ) et consomme c(θ) s’il

se trouve confronte au bareme t. C’est-a-dire :

y(θ) = arg maxy

{y − t(y)− v

(y

θ

)}.

Par construction, on aura alors c = c(θ) = y(θ)− t(y(θ)).

![Page 11: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/11.jpg)

Par contradiction, supposons qu’il existe y tel que :

y − t(y)− v

(y

θ

)> y(θ)− t(y(θ))− v

(y(θ)

θ

).

I Si y ∈ supp{y(θ), θ ∈ Θ}, alors on a une contradiction puisque le

mecanisme initial est revelateur.

I Si y /∈ supp{y(θ), θ ∈ Θ}, alors t(y) = +∞, de sorte que l’on a

aussi une contradiction.

Il existe donc un bareme t qui implique que tout agent θ choisit

l’allocation (c(θ), y(θ)) prevue par le mecanisme direct revelateur

(c(·), y(·),Θ).

![Page 12: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/12.jpg)

Principe de taxation (Partie 2). Toute allocation obtenue au terme

d’un processus decentralise associe a un bareme t(y) est ’revelatrice’.

Soit

y(θ) = arg maxy

{y − t(y)− v

(y

θ

)}, θ ∈ Θ,

et c(θ) = y(θ)− t(y(θ)).

Alors, par definition de y(θ), il n’existe aucun y(θ′) tel que

y(θ′)− t(y(θ′))− v

(y(θ′)

θ

)> y(θ)− t(y(θ))− v

(y(θ)

θ

),

ce qui montre que le resultat recherche.

![Page 13: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/13.jpg)

The general problem will be solved in Lecture 6 (Amedeo Spadaro).

Here, we restrict our attention to a linear income tax schedule.

By the ’taxation principle’, one can consider the following two-stage

problem :

1. At stage 1, the planner choose an linear income tax schedule.

2. At stage 2, all individuals maximize their welfare given the income

tax.

![Page 14: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/14.jpg)

Preferences individuelles

Le cadre de reference est : Sheshinski, E., 1972, The optimal linear

income tax, Review of Economic Studies 39, 297-302.

Les individus ont des preferences identiques, representees par u(c , l), avec

u concave.

Le revenu avant impot est y = θl .

Le bareme de l’imposition sur le revenu est lineaire : t(y) = ty − G .

La contrainte de budget individuelle donne c = y − t(y) = (1− t)θl + G .

Ainsi, G represente un ’revenu minimum’ (lorsque G ≥ 0).

![Page 15: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/15.jpg)

Le probleme du menage

Le menage θ choisit l ≥ 0 qui maximise u((1− t)θl + G , l).

La CPO s’ecrit (1− t)θuc + ul ≤ 0, avec egalite si l > 0. Pour θ = 0,

ul((1− t)θl + G , l) < 0, et donc l = 0.

Soient l((1− t)θ,G ) l’offre de travail et c((1− t)θ,G ) la consommation

choisies.

On ecrira parfois w ≡ (1− t)θ le ’salaire net’.

![Page 16: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/16.jpg)

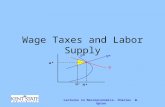

La condition de Spence-Mirrlees

Le TMS entre la consommation et le revenu (avant impot) est tel que

du(

c ,y

θ

)= 0⇔ dc

dy= − ul (c , y/θ)

θuc (c , y/θ).

S’il est decroissant avec θ, alors, si l’on impose a l’agent θ de travailler

pour gagner 1 euro supplementaire, il faudra compenser sa perte d’utilite

en lui donnant TMS unites de consommation supplementaires, et cette

compensation sera moins importante pour les plus productifs.

C’est le cas represente sur la figure ci-apres.

![Page 17: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/17.jpg)

c

G

Gytc +−= )1(

y

1θ 12 θθ >

1y2y

2c

1c

0

![Page 18: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/18.jpg)

Lorsque le TMS entre la consommation et le revenu est decroissant avec

θ,

1. les plus productifs ont un revenu avant impot plus eleve que les

moins productifs,

2. leur revenu apres impot (leur consommation) est aussi plus grand

que celui des moins productifs.

![Page 19: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/19.jpg)

Le sens de la redistribution

Avec la condition de Spence-Mirrlees,

∂

∂θ

(− ul (c , y/θ)

θuc (c , y/θ)

)< 0

pour tout (c , y), les plus productifs ont des revenus plus eleves ; un

revenu plus eleve signale une productivite plus elevee.

Cette condition suggere aussi que les plus productifs sont aussi ceux qui

’souffriront’ le moins lorsqu’on ampute leur revenu.

→ On va donc sans doute rechercher a redistribuer des ’riches’ vers les

’pauvres’ a partir de t = G = 0 (’laissez-faire’).

![Page 20: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/20.jpg)

Marginal utility of income decreases with productivity

The indirect utility of individual θ is v(w ,G ), where w stands for the net

wage, (1− t)θ.

By Roy’s identity, vw (w ,G ) = vG (w ,G )l(w ,G ) for every G , and so

vwG (w ,G ) = vGG (w ,G )l + vG (w ,G )lG

If leisure is normal, then lG < 0.

If u is concave, then v is concave, i.e. vGG < 0 (Mas Colell et al., Prop.

3D3).

Since vwG (w ,G ) = vGw (w ,G ), we have

vGw (w ,G )< 0.

![Page 21: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/21.jpg)

To summarize, thanks to the Spence-Mirrlees condition, consumption and

after-tax income increase with productivity, as well as before-tax income

and labor supply.

A higher income does reveal a higher productivity.

Moreover, richer individuals have lower marginal utility of income than

the less well-off.

Together, such properties suggest that a social planner may try to

redistribute income from rich to poor individuals in order to maximize

’welfare’.

![Page 22: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/22.jpg)

L’impot optimal

Le probleme de l’autorite fiscale est de choisir (t,G ) qui maximise∫ ∞0

Ψ (v((1− t)θ,G )) dF (θ)

sous la contrainte

t

∫ ∞0

θl((1− t)θ,G ))dF (θ)− G ≥ R.

ou R ≥ 0.

→ On reconnaıt le probleme de Ramsey du cours precedent.

![Page 23: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/23.jpg)

Le Lagrangien associe a ce probleme est

L =

∫ ∞0

Ψ(v((1− t)θ,G ))dF (θ)

+ λ

(t

∫ ∞0

θl((1− t)θ,G ))dF (θ)− G − R

).

En utilisant∂v

∂G= α,

∂v

∂w= αl ,

∂w

∂t= −θ,

les deux CPO s’ecrivent :

∂L∂G

=

∫ ∞0

(α

λΨ′ + tθ

∂l

∂G

)dF (θ)− 1 = 0 (1)

∂L∂t

=

∫ ∞0

θl

(α

λΨ′ − t

l

∂l

∂t− 1

)dF (θ) = 0. (2)

![Page 24: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/24.jpg)

Le revenu minimum optimal

On interprete (1), ∫ ∞0

(Ψ′α

λ+ tθ

∂l

∂G

)dF (θ) = 1,

en supposant que l’autorite decide de reduire le ’revenu minimum’ G

d’une unite (dG = −1) sans ajuster le taux de prelevement t.

Elle gagne cette unite, et elle perd :

I Puisque l’individu θ perd α unites d’utilite, elle perd Ψ′α unites

d’utilite, ou bien encore, Ψ′α/λ unites de recettes fiscales.

I Si le loisir est ’normal’, l’offre de travail de l’individu θ augmente de

−∂l/∂G > 0, son revenu avant impot de −θ∂l/∂G > 0, et l’impot

preleve de −tθ∂l/∂G > 0.

![Page 25: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/25.jpg)

Sur l’individu θ, l’autorite evalue donc sa perte b(w ,G ) a

Ψ′α/λ+ tθ∂l/∂G . Le terme b((1− t)θ,G ) est une mesure du poids que

l’autorite accorde a l’individu θ (cf. cours precedent).

Sur l’ensemble des individus, le cout est∫ ∞0

(Ψ′α

λ+ tθ

∂l

∂G

)dF (θ) =

∫ ∞0

b(w ,G )dF (θ).

Ainsi, si ∫ ∞0

b(w ,G )dF (θ) 6= 1,

l’autorite est incitee a modifier le montant du ’revenu minimum’ G .

![Page 26: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/26.jpg)

Le taux optimal : la ’regle de Ramsey’

La CPO relative a t est∫ ∞0

θl

(Ψ′α

λ− t

l

∂l

∂t− 1

)dF (θ) = 0.

La decomposition de Slutsky s’ecrit

∂l

∂w=∂lcomp

∂w+ l

∂l

∂G.

On note

εcomp =w

lcomp

∂lcomp

∂w> 0.

Alors, la CPO devient∫ ∞0

y

(t

1− tεcomp + b(w ,G )− 1

)dF (θ) = 0.

![Page 27: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/27.jpg)

Dans quel sens aller ?

L’autorite observe y . Elle sait qu’un plus haut revenu revele une

productivite elevee et une utilite marginale du revenu plus faible.

Les individus θ que l’autorite souhaiterait taxer plus lourdement sont

ceux pour lesquels b est petit (eventuellement fortement negatif), ceux

dont elle ’valorise’ peu la perte (soit dans l’absolu, soit parce qu’ils

tolerent une reduction importante du ’revenu minimum’).

→ Si ces individus sont ceux qui ont des revenus eleves, alors le taux de

taxe t devrait etre plus important.

Introduisons donc

cov(b, y) ≡∫ +∞

0

(y(w ,G )− y) (b(w ,G )− 1) dF (θ)

= −∫ +∞

0

y(w ,G ) (1− b(w ,G )) dF (θ).

![Page 28: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/28.jpg)

La CPO s’ecritt

1− t= − cov(b, y)∫ ∞

0

yεcompdF (θ)

.

Le membre de gauche est croissant avec t.

Si cov(b, y) < 0, alors on taxe d’autant plus que :

1. |cov(b, y)| est grand, c’est-a-dire que l’on accorde un poids social

eleve aux plus defavorises (equite),

2. εcomp(θ, t,G ) est petit, c’est-a-dire que les agents reagissent peu a

la taxation (une hausse du taux t reduit le salaire reel apres impot

mais n’affecte pas trop leur offre compensee de travail) (efficacite).

![Page 29: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/29.jpg)

The optimal tax rate for a ’utilitarian’ planner

Social preferences are of the (unweighted) utilitarian type if

V (t,G ) =

∫ ∞0

v((1− t)θ,G )dF (θ).

It is obvious that t∗ < 1 :

1. For t ≥ 1, any increase in labor supply leads to a fall in individual

consumption. Thus, l((1− t)θ,G ) = 0 whatever θ is.

2. By the planner budget constraint, G = 0. This solution is achievable

under ’laissez-faire’, i.e. for t = G = 0.

3. Since v(θ, 0) ≥ v(0, 0) for any θ (recall that vw = αl ≥ 0), then the

’laissez-faire’ is socially better than t ≥ 1 and G = 0.

![Page 30: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/30.jpg)

With t < 0, the planner provides a subsidy proportional to labor income,

and taxes in a lump-sum fashion all the individuals to finance labor

subsidies. This is unlikely to be optimal : given that high productivity

workers have also high incomes and low marginal utilities of income, this

tax schedule seems to have quite ’counter-redistributive’ effects.

To show this (see Hellwig, 1986, JPubE), notice that

V (t,G ) ≤ V (0, 0)− tcov(vG , y). Since cov(vG , y) < 0, we have :

t < 0⇒ V (t,G ) < V (0, 0).

To conclude, verify that t = 0 is neither optimal : evaluated at point

t = 0 (and so G (t) = 0),

dV

dt(t,G (t)) = −cov(vG , y) > 0.

Thus, at the utilitarian optimum, t∗ > 0, G∗ > 0 (and G ′(t∗) > 0, as

illustrated in figure of the next slide)

![Page 31: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/31.jpg)

t*t

)(tG

),(),( ** GtVGtV =

G

1

![Page 32: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/32.jpg)

Impot lineaire optimal et prelevement maximal

La contrainte budgetaire de l’autorite s’ecrit :

t

∫ ∞0

θl ((1− t)θ,G ) dF (θ)− G = 0.

Par le theoreme des fonctions implicites, elle definit implicitement la

fonction G (t) (puisque t∫∞0θlG dF (θ)− 1 < −1).

Soit G∗∗ = maxt G (t) et t∗∗ = arg maxt G (t). On supposera que t∗∗ est

unique (sinon, tous les arguments qui suivent s’appliquent en prenant le

plus grand parmi les taux qui maximisent la recette).

Pour t ≥ 1, G (t) = 0 (puisque l = 0). Pour t ≤ 0, G (t) ≤ 0. Comme

G∗ > 0, on doit avoir 0 < t∗∗ < 1.

![Page 33: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/33.jpg)

Pour tout t > t∗∗, on a (par definition de t∗∗), G (t) < G∗∗.

Et donc, pour tout t > t∗∗, on a necessairement

v ((1− t)θ,G ) < v ((1− t∗∗)θ,G∗∗)

En effet, avec la politique (t,G ), on taxe plus et on transfere moins a

tout agent θ qu’avec (t∗∗,G∗∗) !

Il s’ensuit que t∗ ≤ t∗∗.

![Page 34: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/34.jpg)

Soit V (t,G (t)) l’utilite sociale, pour G = G (t). Au point t∗∗, on a :

dV

dt(t∗∗,G∗∗) =

∂V

∂t(t∗∗,G∗∗) +

∂V

∂G(t∗∗,G∗∗)G ′(t∗∗)

=∂V

∂t(t∗∗,G∗∗)

= −∫ ∞

0

θvw ((1− t∗∗)θ,G∗∗)dF (θ)

= −∫ ∞

0

θα((1− t∗∗)θ,G∗∗)l((1− t∗∗)θ,G∗∗)dF (θ).

On a α > 0, et l ≥ 0 pour tout θ ; comme G∗∗ > 0, on doit avoir l > 0

pour certains θ. Et donc :

dV

dt(t∗∗,G∗∗) < 0.

Il s’ensuit que t∗∗ 6= t∗.

On en deduit que t∗ < t∗∗ (et G∗ < G∗∗).

![Page 35: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/35.jpg)

Rawls criterion and the ’Leviathan’

There are close links between the linear income tax which maximizes the

welfare of the individual whose welfare is the lowest and the one which

maximizes tax revenue.

Indirect utility is increasing with respect to (before-tax) income, and

income is increasing with productivity θ. Thus the individual with the

lowest welfare has the lowest productivity θinf ≥ 0. In the sequel, we let

θinf > 0.

Let (tr ,G r ) be the ’Rawlsian’ linear income tax, i.e.

(tr ,G r ) = arg max(t,G)

{v ((1− t)θinf ,G ) |

∫ ∞0

tθl ((1− t)θ,G ) dF (θ) ≥ G

}.

Then, we have (this is proven in the next two slides) :

1. If l ((1− tr )θinf ,Gr ) = 0, then (tr ,G r ) = (t∗∗,G∗∗).

2. If l ((1− tr )θinf ,Gr ) > 0, then tr < t∗∗ and G r < G∗∗.

![Page 36: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/36.jpg)

The argument proceeds as follows.

Note first that G r ≤ G∗∗ by definition of G∗∗.

If tr > t∗∗, then it must be that

v ((1− tr )θinf ,Gr ) < v ((1− t∗∗)θinf ,G

∗∗), which contradicts the

definition of (tr ,G r ). So, tr ≤ t∗∗.

To prove Point 1, suppose that l ((1− tr )θinf ,Gr ) = 0.

Then, v ((1− tr )θinf ,Gr ) = u(G r , 0).

On the other hand, v ((1− tr )θinf ,Gr ) ≥ v ((1− t∗∗)θinf ,G

∗∗), which is

greater than u(G∗∗, 0) by definition of v .

Hence, u(G r , 0) ≥ u(G∗∗, 0), which implies G r ≥ G∗∗. By definition of

G∗∗, it must be that G r = G∗∗ ; thus, tr = t∗∗.

![Page 37: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/37.jpg)

Suppose now that l ((1− tr )θinf ,Gr ) > 0.

To see Point 2, that tr 6= t∗∗ (and so tr < t∗∗), simply observe that

dv

dt((1− t∗∗)θinf ,G (t∗∗)) =

∂v

∂t((1− t∗∗)θinf ,G (t∗∗))

= −θinfαinf l ((1− t∗∗)θinf ,G∗∗) .

By contradiction, suppose that tr = t∗∗. Then, G r = G∗∗. Thus,

dv

dt((1− tr )θinf ,G (tr )) = −θinfαinf l ((1− tr )θinf ,G

r ) > 0,

which is impossible by definition of (tr ,G r ).

It follows that tr < t∗∗ and G r < G∗∗.

![Page 38: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/38.jpg)

’Rawlsian’ and utilitarian linear income taxes

We have tr ≥ t∗ and G r ≥ G∗.

The intuition hinges on the following property : for any given linear

income tax (t,G ), feasible or not, the utilitarian planner puts relatively

less weight to the minimal income transfer G , and relatively more weight

to the tax rate t than the Rawlsian planner.

As a result, at point (t∗,G∗), the Rawlsian planner would find desirable

to increase G by a small amount dG > 0, and to increase the tax rate by

dt > 0 to finance this additional transfer (recall that t∗ < t∗∗, so that

the economy initially faces a upward sloping ’Laffer’ curve).

![Page 39: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/39.jpg)

Recall that

V (t,G ) ≡∫ ∞

0

v((1− t)θ,G )dF (θ).

Applying Roy’s identity,

dV (t,G ) = 0⇔(∫ ∞

0

−αθldF (θ)

)dt +

(∫ ∞0

αdF (θ)

)dG = 0.

Similarly, dv((1− t)θinf ,G ) = 0⇔ −αinfθinf linfdt + αinfdG = 0, with

αinf > 0.

By the Spence-Mirrlees condition, θl is an increasing function of θ. Thus,

provided that some individuals are working at (t,G ),∫ ∞0

αθldF (θ) > θinf linf

∫ ∞0

αdF (θ)

⇒ dG

dt

∣∣∣∣dV=0

=

∫ ∞0

αθldF (θ)∫ ∞0

αdF (θ)

> θinf linf =dG

dt

∣∣∣∣dvinf=0

.

→ The utilitarian planner is more reluctant to increase minimal income.

![Page 40: Lecture 5 [0.3cm] Linear Income Taxes - CREST](https://reader033.fdocument.org/reader033/viewer/2022060310/62943e40c310f80a5e2f288f/html5/thumbnails/40.jpg)

t*t **trt

)(tG

),(),(

** GtVGtV

=

),)1((

),)1((*

inf*

inf

Gtv

Gtv

θ

θ

−=

−

![Lecture 2 [0.3cm] Optimal Indirect Taxationecon.sciences-po.fr/sites/default/files/file/laroque/...Ramsey vs. Mirrlees Ramsey: constraints are put directly on the B function, i.e.](https://static.fdocument.org/doc/165x107/5aedd17e7f8b9ad73f91a413/lecture-2-03cm-optimal-indirect-vs-mirrlees-ramsey-constraints-are-put-directly.jpg)

![4. C [1]pmt.physicsandmathstutor.com/download/Physics/A-level/Topic-Qs... · OR measure several ... Add standing waves to diagrams Mark for each correct diagram (1)(1) 2 ... Crest](https://static.fdocument.org/doc/165x107/5ae9e6aa7f8b9a3b2e8be48c/4-c-1pmt-measure-several-add-standing-waves-to-diagrams-mark-for-each-correct.jpg)

![THE SCORPION - 100th Monkey PressLAYLAH. I had rather a scorpion stung me. RINALDO. My crest is a scorpion. [He points to the golden bejewelled crest upon his light helmet.] I am thirsty.](https://static.fdocument.org/doc/165x107/5f04404b7e708231d40d0de6/the-scorpion-100th-monkey-press-laylah-i-had-rather-a-scorpion-stung-me-rinaldo.jpg)