![UK Domain Average Windstorm Risk S] risk non-SJ risk Wind ...sws98slg/Downloads/RMetS-NCAS-2016-StingJet... · UK Domain Average Windstorm Risk S] risk non-SJ risk Wind speed threshold](https://static.fdocument.org/doc/165x107/5bfce26209d3f264188c4657/uk-domain-average-windstorm-risk-s-risk-non-sj-risk-wind-sws98slgdownloadsrmets-ncas-2016-stingjet.jpg)

γλώσσες

Σελίδες

Νομικός

CBOE Risk Management Conference March 2013

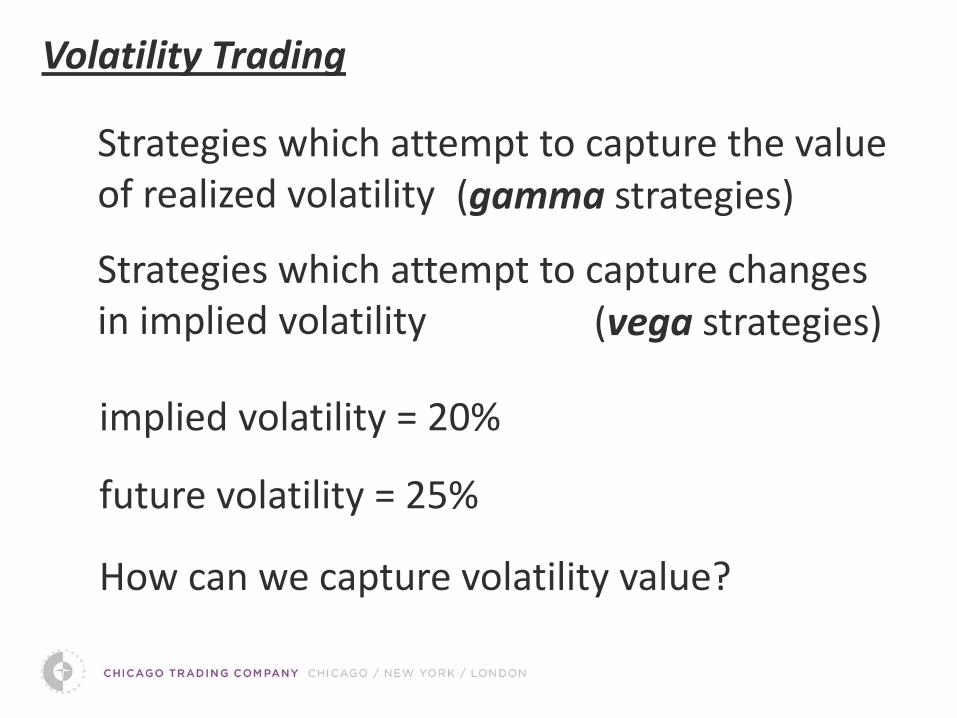

Volatility Trading

Sheldon Natenberg Chicago Trading Co.

440 South LaSalle St. Chicago, IL 60605 (312) 863-8004

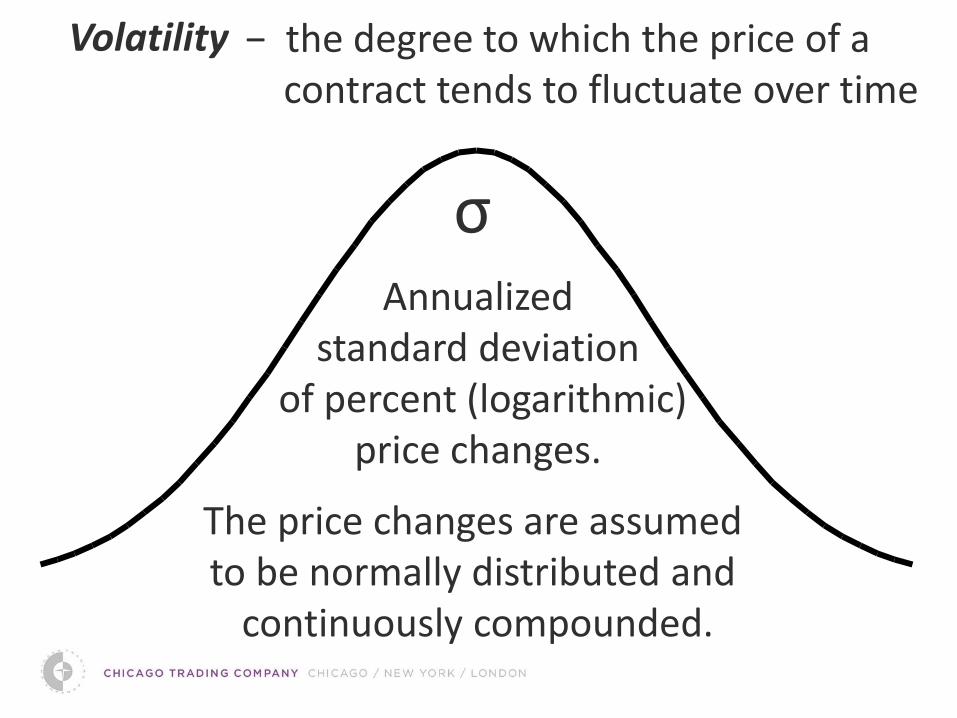

Volatility − the degree to which the price of a contract tends to fluctuate over time

Annualized standard deviation

of percent (logarithmic) price changes.

σ

The price changes are assumed to be normally distributed and

continuously compounded.

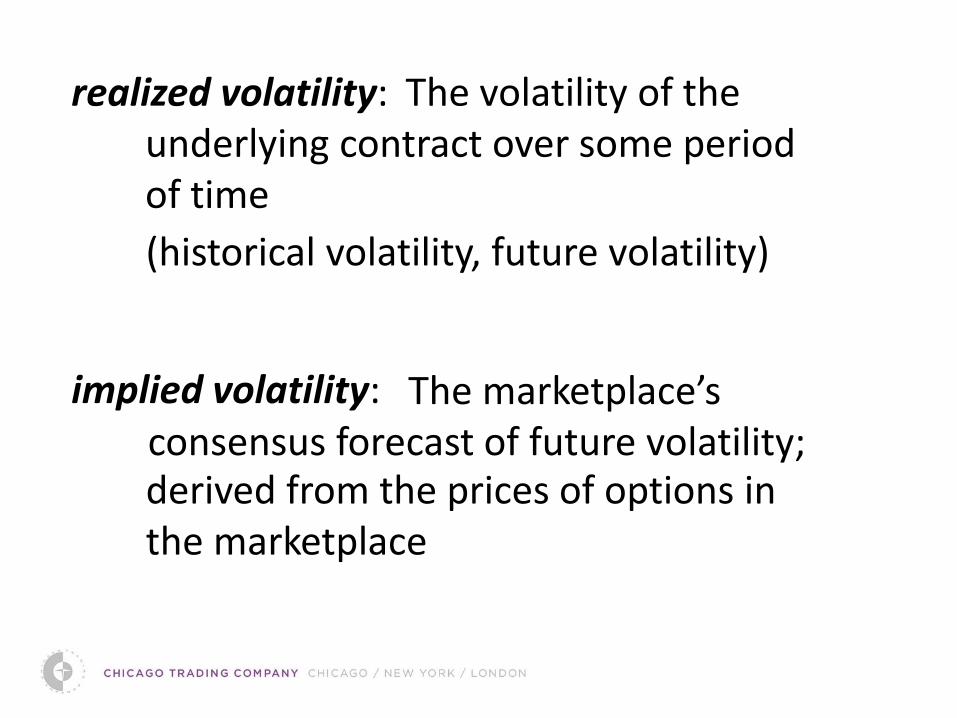

The volatility of the underlying contract over some period of time

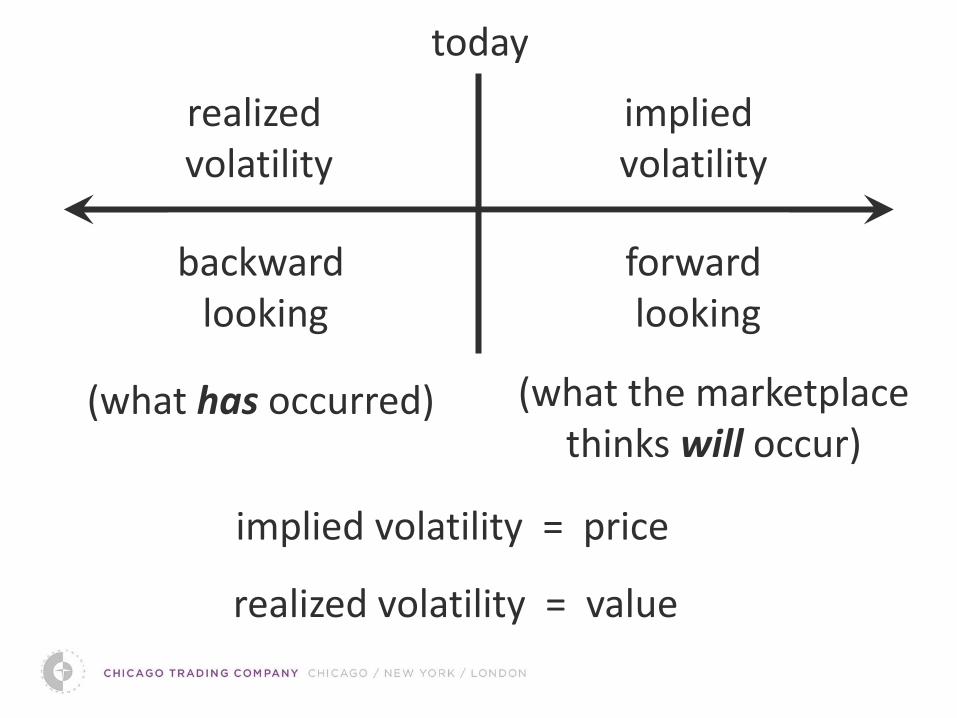

realized volatility:

derived from the prices of options in the marketplace

implied volatility: The marketplace’s consensus forecast of future volatility;

(historical volatility, future volatility)

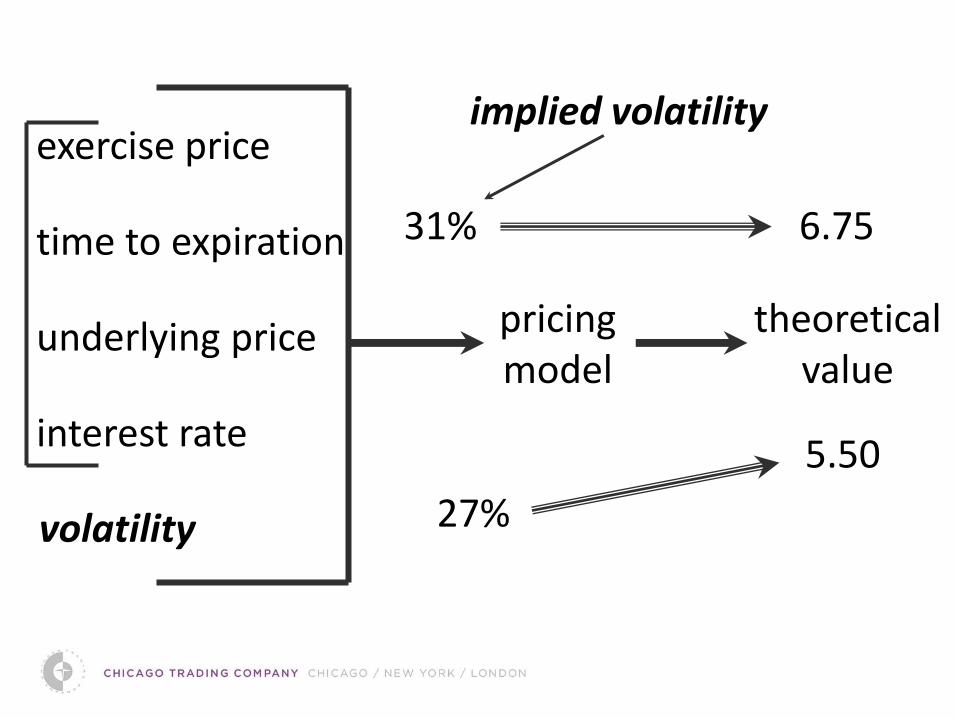

pricing model

theoretical value

5.50

6.75

exercise price

time to expiration

underlying price

interest rate

volatility 27% volatility

??? 31%

implied volatility

today

realized volatility

backward looking

(what has occurred)

implied volatility

forward looking

(what the marketplace thinks will occur)

implied volatility = price

realized volatility = value

Strategies which attempt to capture the value of realized volatility

Volatility Trading

Strategies which attempt to capture changes in implied volatility

How can we capture volatility value?

implied volatility = 20%

future volatility = 25%

(gamma strategies)

(vega strategies)

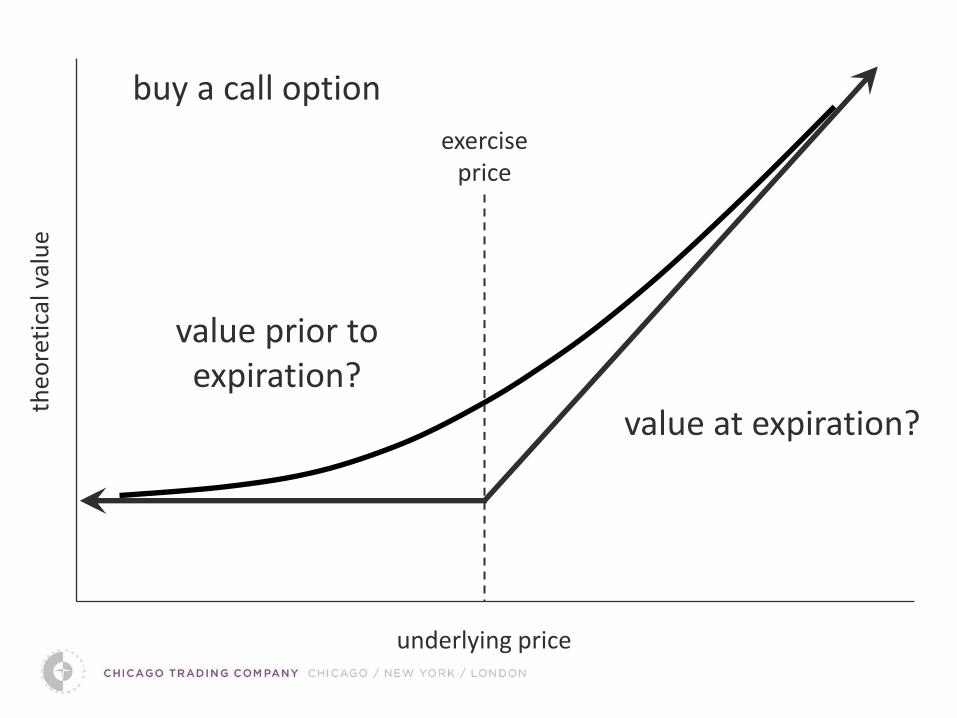

buy a call option

theo

reti

cal v

alu

e

underlying price

exercise price

value at expiration?

value prior to expiration?

theo

reti

cal v

alu

e

underlying price

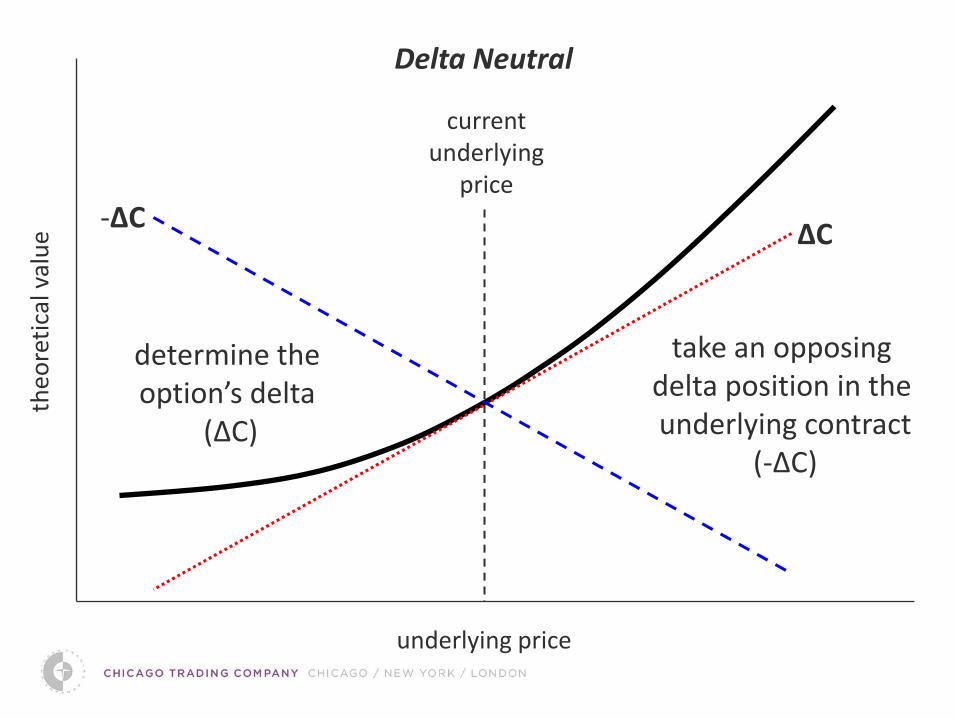

current underlying

price

determine the option’s delta

(ΔC)

ΔC

take an opposing delta position in the underlying contract

(-ΔC)

-ΔC

Delta Neutral

theo

reti

cal v

alu

e

underlying price

ΔC -ΔC

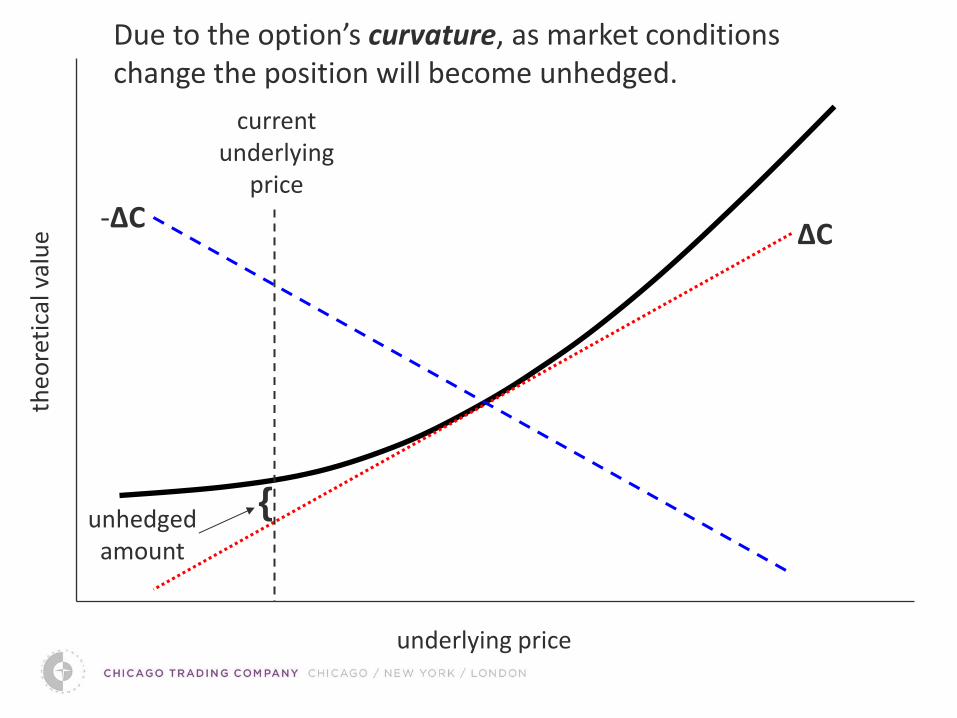

Due to the option’s curvature, as market conditions change the position will become unhedged.

current underlying

price

{ unhedged

amount

theo

reti

cal v

alu

e

underlying price

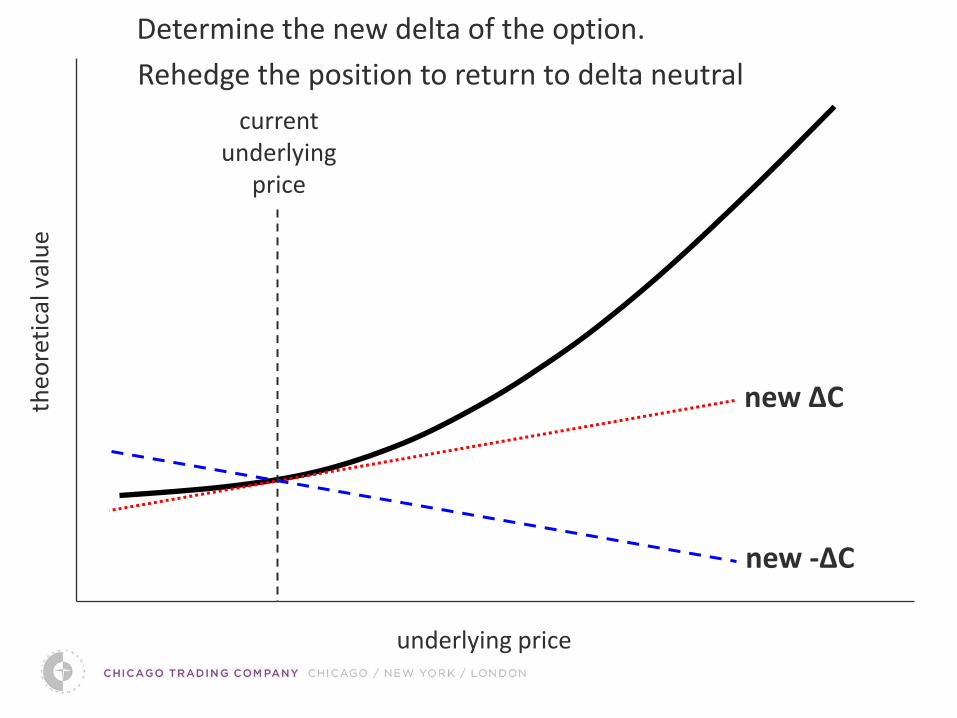

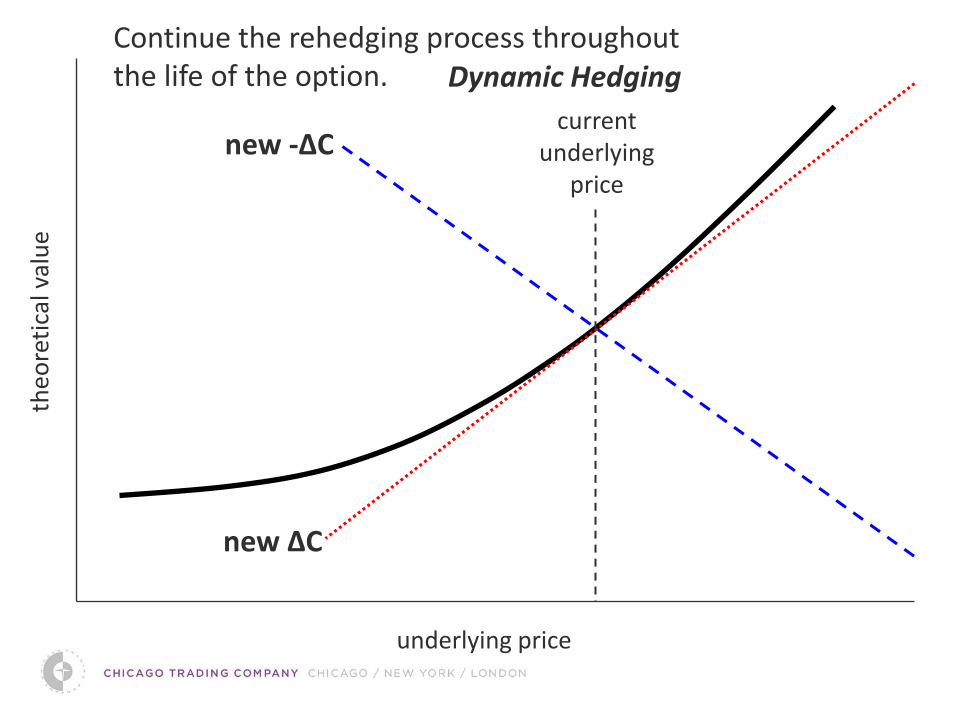

Determine the new delta of the option.

Rehedge the position to return to delta neutral

current underlying

price

new ΔC

new -ΔC

theo

reti

cal v

alu

e

underlying price

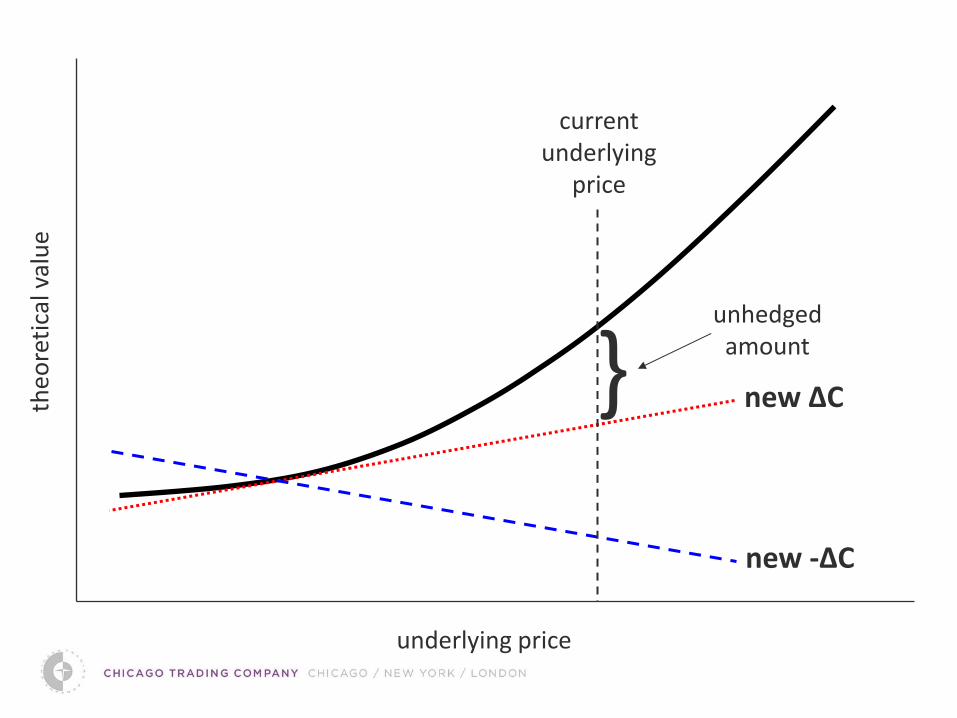

current underlying

price

} unhedged

amount

new ΔC

new -ΔC

theo

reti

cal v

alu

e

underlying price

current underlying

price

new ΔC

new -ΔC

Dynamic Hedging Continue the rehedging process throughout the life of the option.

Suppose we add up all the profit opportunities over the life of the option which result from the rehedging process.

the option’s theoretical value

The rehedging process is a type of statistical arbitrage.

What should this equal?

Each time the position becomes unhedged there is a potential profit opportunity. We can capture this profit by rehedging the position.

Volatility Trading

1. Compare implied volatility to an expected future realized volatility

2. If implied is lower, buy options; if implied is higher, sell options

3. Hedge the position, delta neutral, against the underlying contract

4. As the underlying price moves rehedge the position in order to remain delta neutral (dynamic hedging)

5. At expiration close out the entire position

It sounds good in theory, but …..

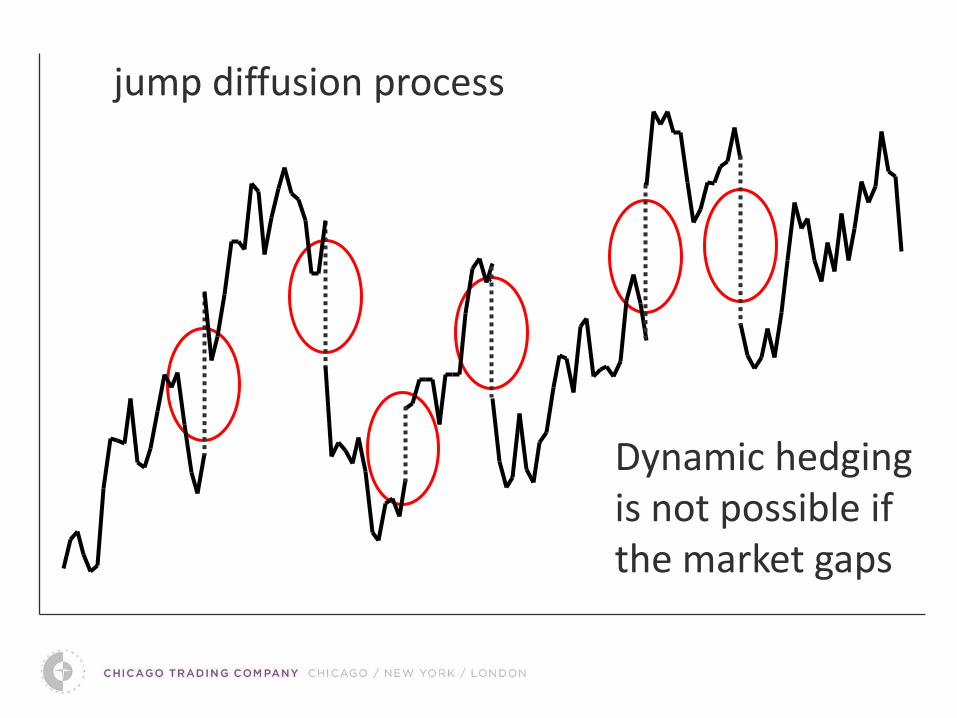

2. It may not always be possible to dynamically hedge an option position.

3. The volatility sensitivity of an option is not constant. As time passes, or as the underlying price changes in relation to the option’s exercise price, the option may become either more or less sensitive to changes in volatility.

4. Percent price changes in the real world may not be normally distributed.

1. The transaction costs of dynamically hedging a position may affect the expected results.

diffusion process

Dynamic hedging is not possible if the market gaps

jump diffusion process

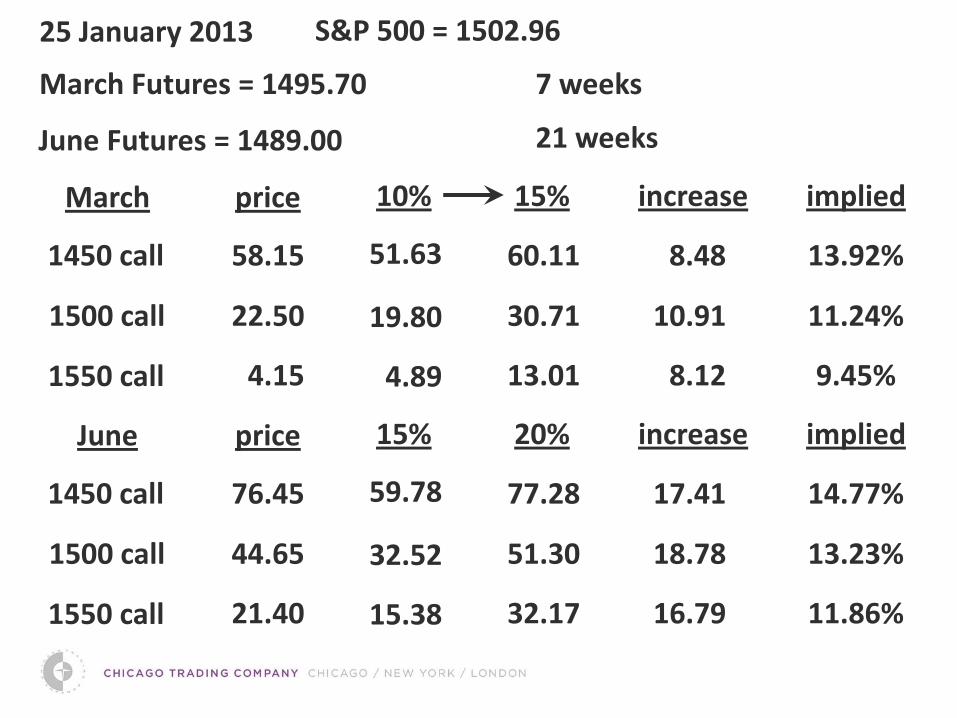

25 January 2013 S&P 500 = 1502.96

June Futures = 1489.00

1450 call

1500 call

1550 call

increase implied

13.92%

11.24%

9.45%

8.48

10.91

8.12

March

March Futures = 1495.70 7 weeks

21 weeks

price 10% 15%

58.15

22.50

4.15

51.63

19.80

4.89

60.11

30.71

13.01

1450 call

1500 call

1550 call

increase implied

14.77%

13.23%

11.86%

17.41

18.78

16.79

June price 15% 20%

76.45

44.65

21.40

59.78

32.52

15.38

77.28

51.30

32.17

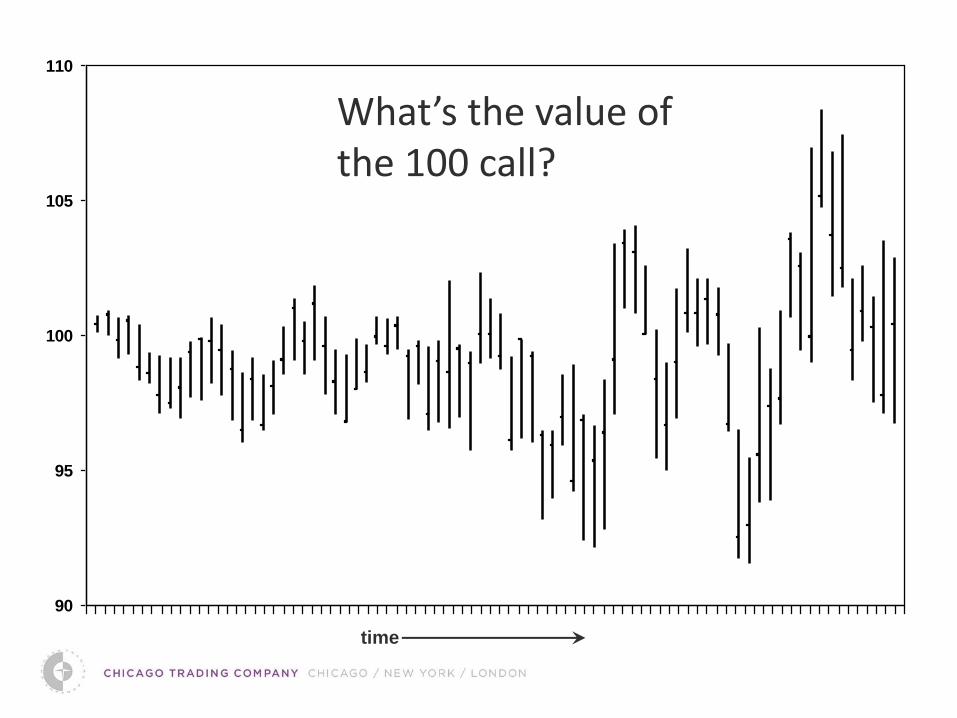

90

95

100

105

110

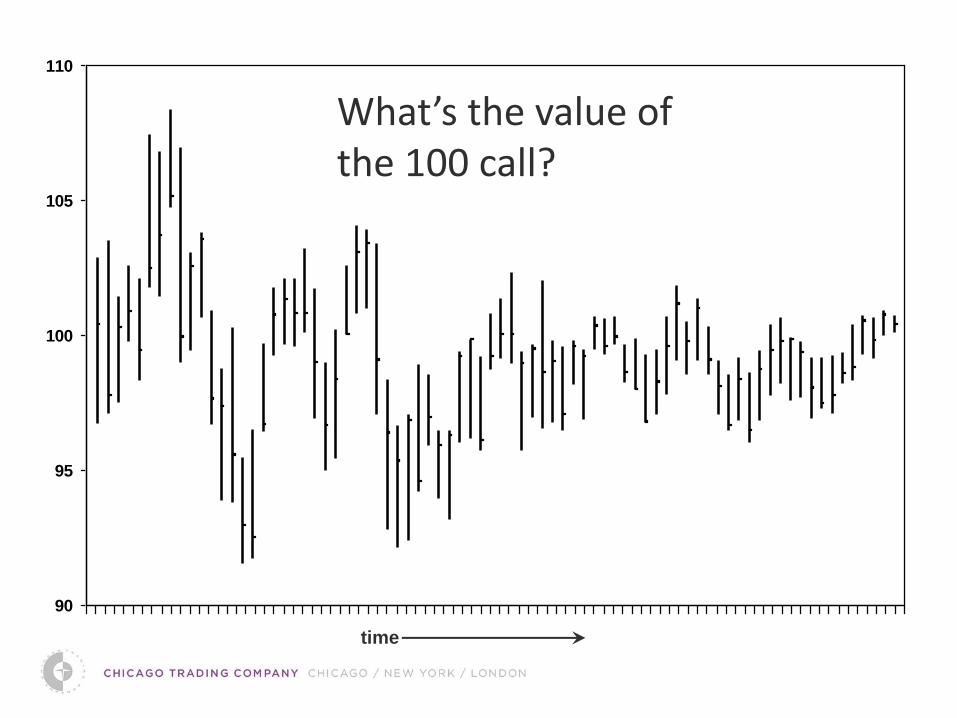

What’s the value of the 100 call?

time

90

95

100

105

110

What’s the value of the 100 call?

time

Time to expiration = 107 days Volatility = 32.00% Forward price = 100.00

100 C/P

constant volatility

rising volatility

falling volatility

6.90

4.93

8.10

80 P

.72

1.03

.43

120 C

1.43

1.89

.99

nu

mb

er o

f o

ccu

rren

ces

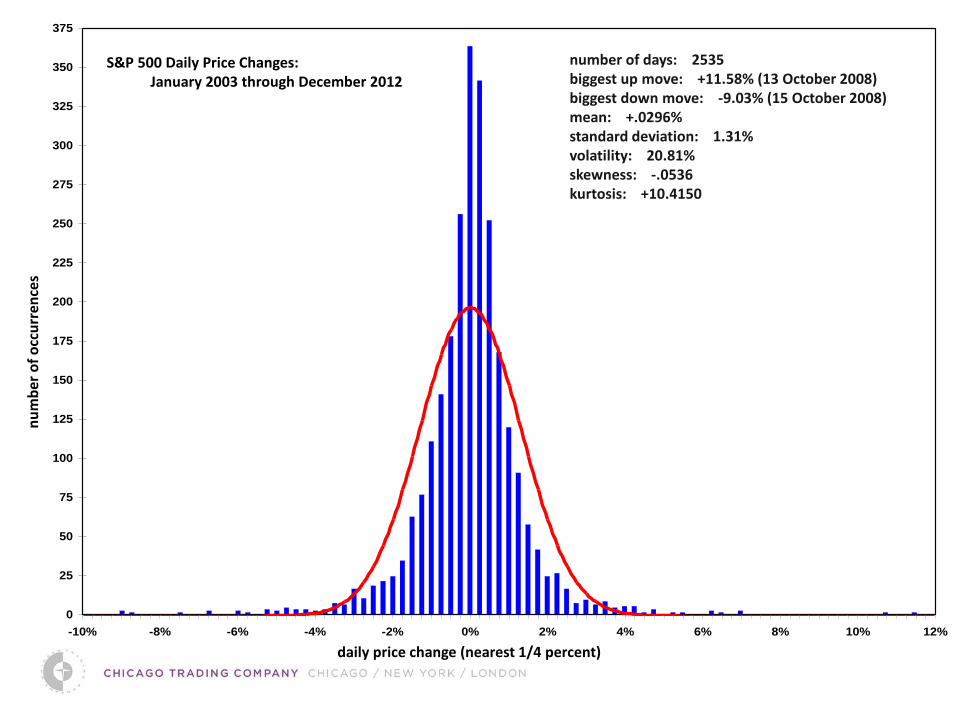

daily price change (nearest 1/4 percent)

S&P 500 Daily Price Changes: January 2003 through December 2012

number of days: 2535 biggest up move: +11.58% (13 October 2008) biggest down move: -9.03% (15 October 2008) mean: +.0296% standard deviation: 1.31% volatility: 20.81% skewness: -.0536 kurtosis: +10.4150

0

25

50

75

100

125

150

175

200

225

250

275

300

325

350

375

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10% 12%

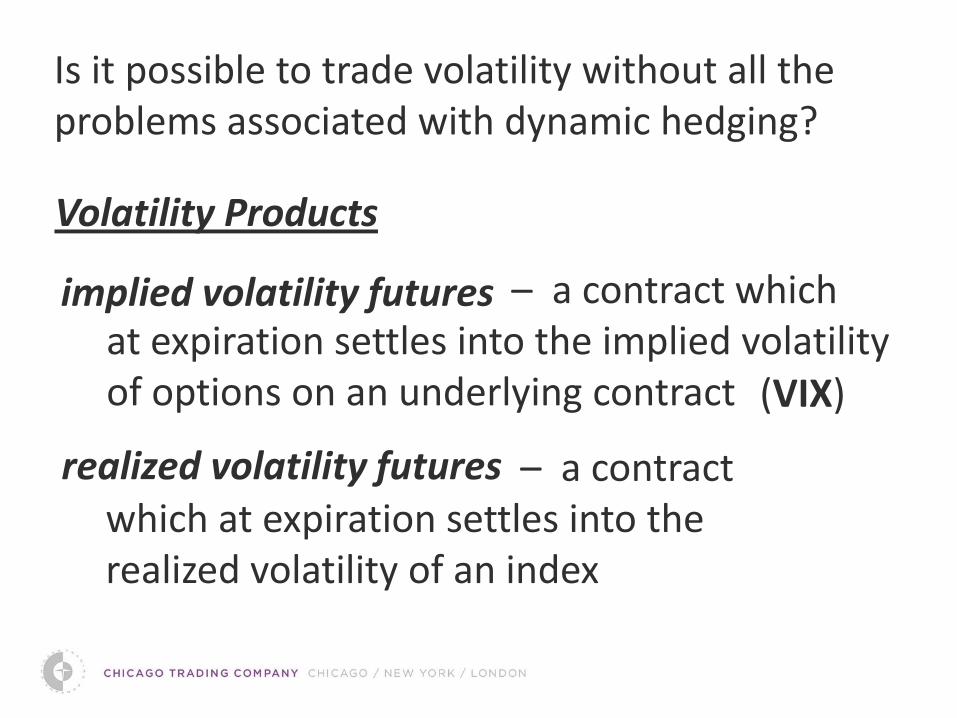

Volatility Products

implied volatility futures – a contract which at expiration settles into the implied volatility of options on an underlying contract

realized volatility futures – a contract which at expiration settles into the realized volatility of an index

Is it possible to trade volatility without all the problems associated with dynamic hedging?

(VIX)

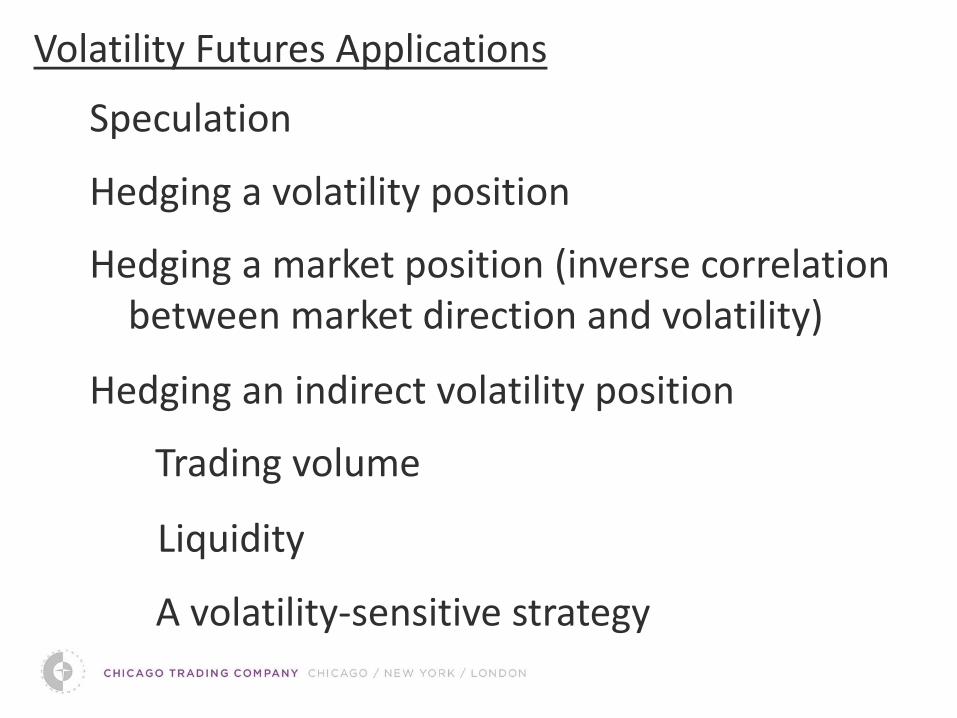

Volatility Futures Applications

Speculation

Hedging a volatility position

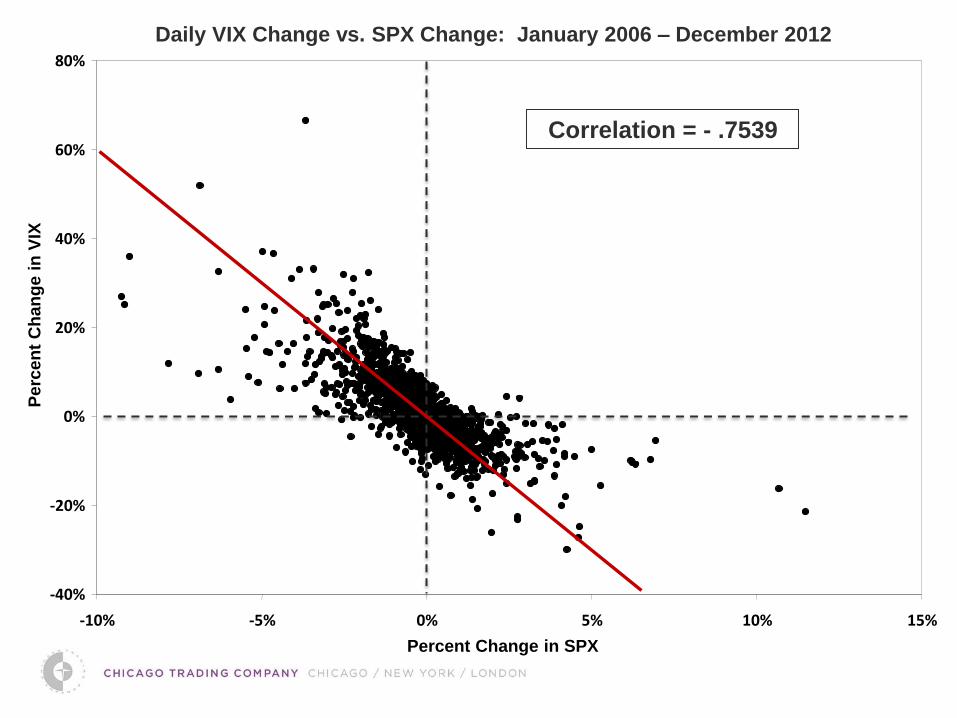

Hedging a market position (inverse correlation between market direction and volatility)

Hedging an indirect volatility position

Trading volume

Liquidity

A volatility-sensitive strategy

Daily VIX Change vs. SPX Change: January 2006 – December 2012

Correlation = - .7539

-40%

-20%

0%

20%

40%

60%

80%

-10% -5% 0% 5% 10% 15%

Percent Change in SPX

Perc

en

t C

han

ge i

n V

IX

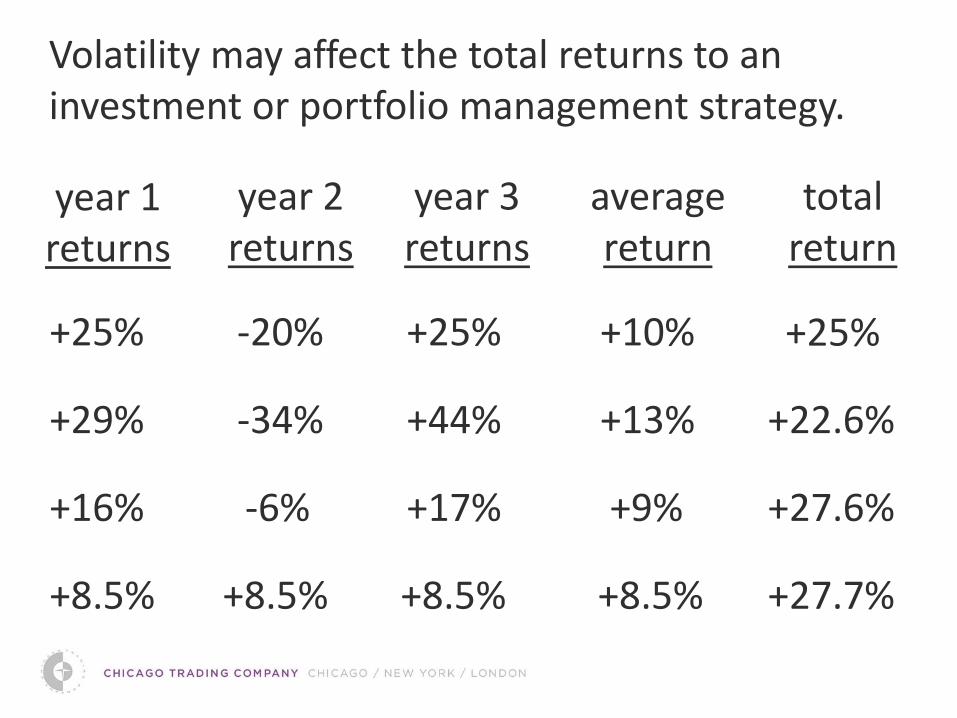

Volatility may affect the total returns to an investment or portfolio management strategy.

year 1 returns

year 2 returns

year 3 returns

average return

+25%

total return

-20% +10% +25%

+29% -34% +13% +44%

+25%

+22.6%

+16% -6% +9% +17% +27.6%

+8.5% +8.5% +8.5% +8.5% +27.7%

Top Related