"The Checklist" - 9b Construction: Cross-sectional Strategies - Portfolio construction: "factors"

16

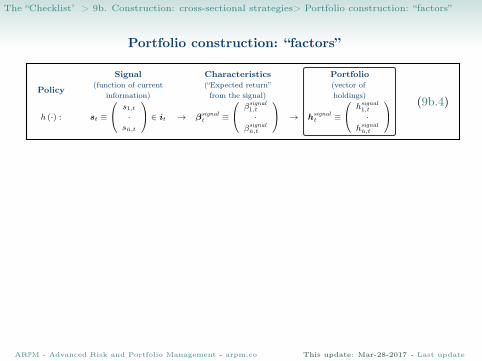

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors” Portfolio construction: “factors” Policy Signal (function of current information) Characteristics (“Expected return” from the signal) Portfolio (vector of holdings) h (·): st ≡ s1,t · s¯ n,t ∈ it → β signal t ≡ β signal 1,t · β signal ¯ n,t → h signal t ≡ h signal 1,t · h signal ¯ n,t (9b.4) ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

-

Upload

arpm-advanced-risk-and-portfolio-management -

Category

Economy & Finance

-

view

29 -

download

0

Transcript of "The Checklist" - 9b Construction: Cross-sectional Strategies - Portfolio construction: "factors"

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”

Portfolio construction: “factors”

Policy

Signal(function of current

information)

Characteristics(“Expected return”from the signal)

Portfolio(vector ofholdings)

h (·) : st ≡

s1,t

·sn̄,t

∈ it → βsignalt ≡

βsignal1,t

·βsignaln̄,t

→ hsignalt ≡

hsignal1,t

·hsignaln̄,t

(9b.4)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”

Exposures

Exposures

Policy

Signal(function of current

information)

Characteristics(“Expected return”from the signal)

Portfolio(vector ofholdings)

h (·) : st ≡

s1,t

·sn̄,t

∈ it → βsignalt ≡

βsignal1,t

·βsignaln̄,t

→ hsignalt ≡

hsignal1,t

·hsignaln̄,t

(9b.4)

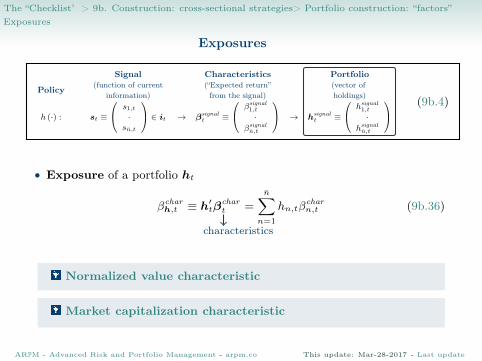

• Exposure of a portfolio ht

βcharh,t ≡ h′tβchar

t =

n̄∑n=1

hn,tβcharn,t (9b.36)

Normalized value characteristic

Market capitalization characteristic

characteristics

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”

Characteristic portfolio

Characteristic portfolio

Policy

Signal(function of current

information)

Characteristics(“Expected return”from the signal)

Portfolio(vector ofholdings)

h (·) : st ≡

s1,t

·sn̄,t

∈ it → βsignalt ≡

βsignal1,t

·βsignaln̄,t

→ hsignalt ≡

hsignal1,t

·hsignaln̄,t

(9b.4)

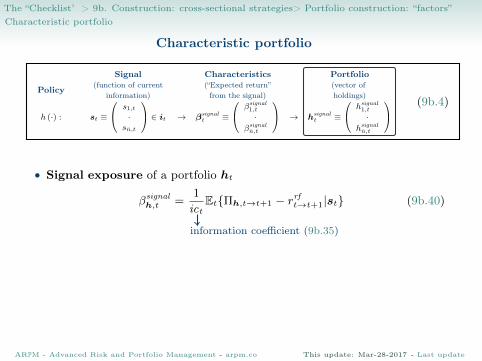

• Signal exposure of a portfolio ht

βsignalh,t =

1

ictEt{Πh,t→t+1 − rrft→t+1|st} (9b.40)

information coefficient (9b.35)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”

Characteristic portfolio

Characteristic portfolio

Policy

Signal(function of current

information)

Characteristics(“Expected return”from the signal)

Portfolio(vector ofholdings)

h (·) : st ≡

s1,t

·sn̄,t

∈ it → βsignalt ≡

βsignal1,t

·βsignaln̄,t

→ hsignalt ≡

hsignal1,t

·hsignaln̄,t

(9b.4)

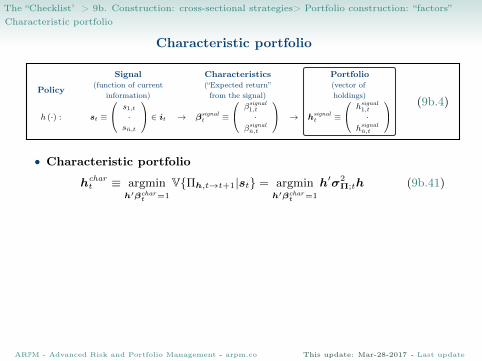

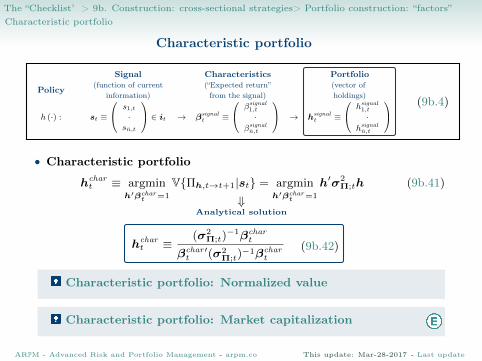

• Characteristic portfolio

hchart ≡ argmin

h′βchart =1

V{Πh,t→t+1|st} = argminh′βchar

t =1

h′σ2Π;th (9b.41)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”

Characteristic portfolio

Characteristic portfolio

Policy

Signal(function of current

information)

Characteristics(“Expected return”from the signal)

Portfolio(vector ofholdings)

h (·) : st ≡

s1,t

·sn̄,t

∈ it → βsignalt ≡

βsignal1,t

·βsignaln̄,t

→ hsignalt ≡

hsignal1,t

·hsignaln̄,t

(9b.4)

• Characteristic portfolio

hchart ≡ argmin

h′βchart =1

V{Πh,t→t+1|st} = argminh′βchar

t =1

h′σ2Π;th (9b.41)

⇓Analytical solution

hchart ≡

(σ2Π;t)

−1βchart

βchar′t (σ2

Π;t)−1βchar

t

(9b.42)

Characteristic portfolio: Normalized value

Characteristic portfolio: Market capitalization

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”

Characteristic portfolio

Characteristic portfolio

Policy

Signal(function of current

information)

Characteristics(“Expected return”from the signal)

Portfolio(vector ofholdings)

h (·) : st ≡

s1,t

·sn̄,t

∈ it → βsignalt ≡

βsignal1,t

·βsignaln̄,t

→ hsignalt ≡

hsignal1,t

·hsignaln̄,t

(9b.4)

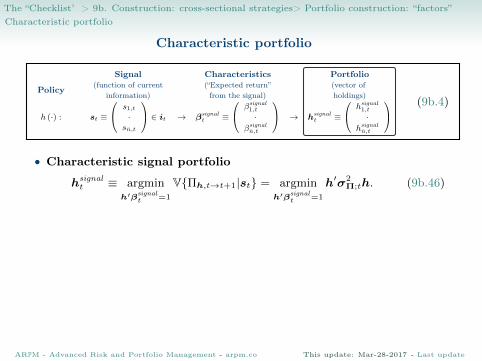

• Characteristic signal portfolio

hsignalt ≡ argmin

h′βsignalt =1

V{Πh,t→t+1|st} = argminh′βsignal

t =1

h′σ2Π;th. (9b.46)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”

Characteristic portfolio

Characteristic portfolio

Policy

Signal(function of current

information)

Characteristics(“Expected return”from the signal)

Portfolio(vector ofholdings)

h (·) : st ≡

s1,t

·sn̄,t

∈ it → βsignalt ≡

βsignal1,t

·βsignaln̄,t

→ hsignalt ≡

hsignal1,t

·hsignaln̄,t

(9b.4)

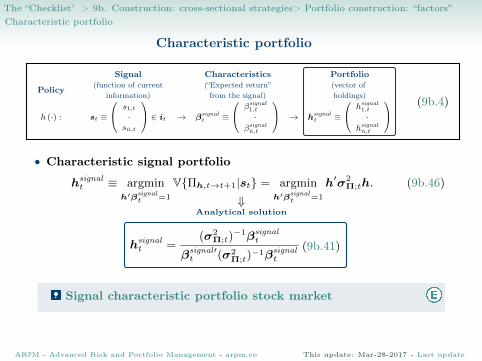

• Characteristic signal portfolio

hsignalt ≡ argmin

h′βsignalt =1

V{Πh,t→t+1|st} = argminh′βsignal

t =1

h′σ2Π;th. (9b.46)

⇓Analytical solution

hsignalt =

(σ2Π;t)

−1βsignalt

βsignal′t (σ2

Π;t)−1βsignal

t

(9b.41)

Signal characteristic portfolio stock market

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”

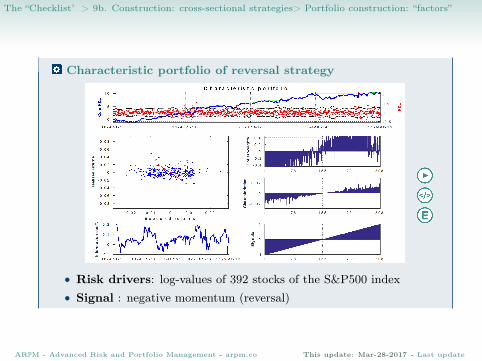

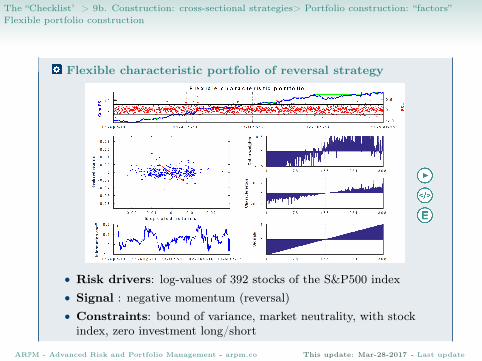

Characteristic portfolio of reversal strategy

• Risk drivers: log-values of 392 stocks of the S&P500 index• Signal : negative momentum (reversal)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

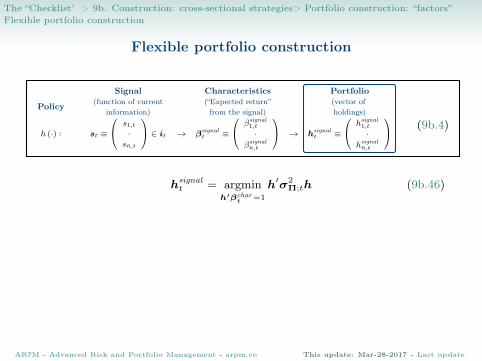

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”Flexible portfolio construction

Flexible portfolio construction

Policy

Signal(function of current

information)

Characteristics(“Expected return”from the signal)

Portfolio(vector ofholdings)

h (·) : st ≡

s1,t

·sn̄,t

∈ it → βsignalt ≡

βsignal1,t

·βsignaln̄,t

→ hsignalt ≡

hsignal1,t

·hsignaln̄,t

(9b.4)

hsignalt = argmin

h′βchart =1

h′σ2Π;th (9b.46)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”Flexible portfolio construction

Flexible portfolio construction

Policy

Signal(function of current

information)

Characteristics(“Expected return”from the signal)

Portfolio(vector ofholdings)

h (·) : st ≡

s1,t

·sn̄,t

∈ it → βsignalt ≡

βsignal1,t

·βsignaln̄,t

→ hsignalt ≡

hsignal1,t

·hsignaln̄,t

(9b.4)

hsignalt = argmin

h′βchart =1

h′σ2Π;th (9b.46)

hsignalt ≡ argmaxh∈Ct{h

′βsignalt }

Dual Problem:Ct ≡ {h′σ2

Π;th ≤ 1

βchar′t (σ2

Π;t)−1βchar

t}

m

(9b.54)

(9b.55)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

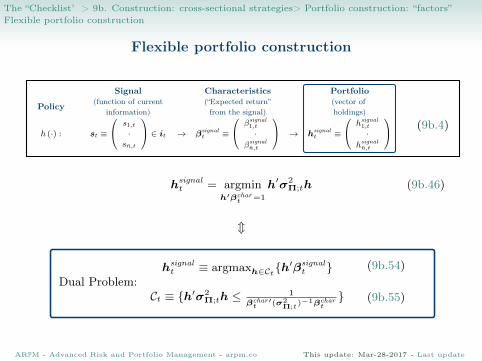

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”Flexible portfolio construction

Flexible characteristic portfolio of reversal strategy

• Risk drivers: log-values of 392 stocks of the S&P500 index• Signal : negative momentum (reversal)• Constraints: bound of variance, market neutrality, with stock

index, zero investment long/short

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

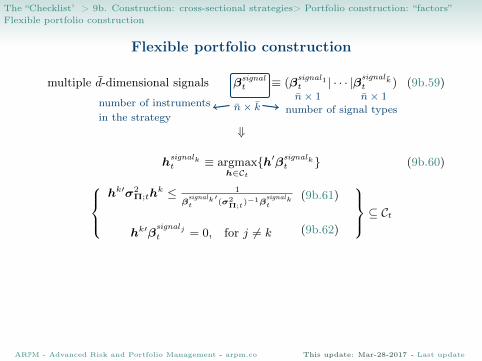

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”Flexible portfolio construction

Flexible portfolio construction

multiple d̄-dimensional signals βsignalt ≡ (β

signal1t | · · · |βsignalk̄

t ) (9b.59)

n̄× k̄number of instrumentsin the strategy

number of signal typesn̄× 1 n̄× 1

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”Flexible portfolio construction

Flexible portfolio construction

multiple d̄-dimensional signals βsignalt ≡ (β

signal1t | · · · |βsignalk̄

t ) (9b.59)

n̄× k̄number of instrumentsin the strategy

number of signal typesn̄× 1 n̄× 1

⇓

hsignalkt ≡ argmax

h∈Ct{h′βsignalk

t } (9b.60)

hk′σ2

Π;thk ≤ 1

βsignalk′t (σ2

Π;t)−1β

signalkt

hk′βsignaljt = 0, for j 6= k

⊆ Ct(9b.61)

(9b.62)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

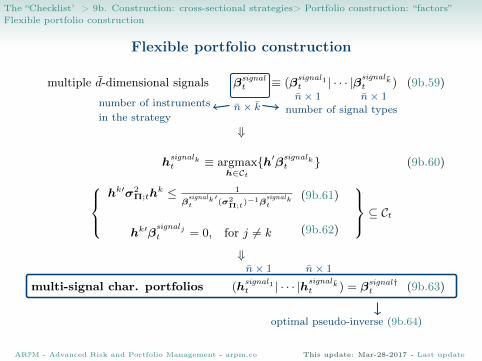

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”Flexible portfolio construction

Flexible portfolio construction

multiple d̄-dimensional signals βsignalt ≡ (β

signal1t | · · · |βsignalk̄

t ) (9b.59)

n̄× k̄number of instrumentsin the strategy

number of signal typesn̄× 1 n̄× 1

⇓

hsignalkt ≡ argmax

h∈Ct{h′βsignalk

t } (9b.60)

hk′σ2

Π;thk ≤ 1

βsignalk′t (σ2

Π;t)−1β

signalkt

hk′βsignaljt = 0, for j 6= k

⊆ Ct(9b.61)

(9b.62)

⇓

multi-signal char. portfolios (hsignal1t | · · · |hsignalk̄

t ) = βsignal†t (9b.63)

n̄× 1 n̄× 1

optimal pseudo-inverse (9b.64)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

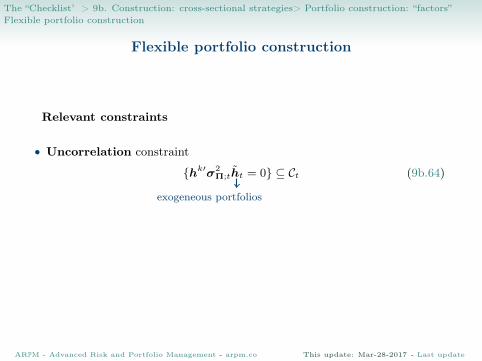

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”Flexible portfolio construction

Flexible portfolio construction

Relevant constraints

• Uncorrelation constraint

{hk′σ2Π;th̃t = 0} ⊆ Ct (9b.64)

exogeneous portfolios

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update

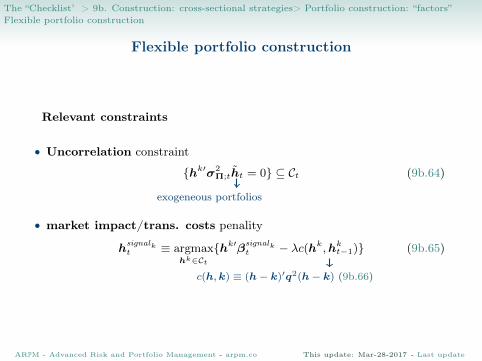

The “Checklist’’ > 9b. Construction: cross-sectional strategies> Portfolio construction: “factors”Flexible portfolio construction

Flexible portfolio construction

Relevant constraints

• Uncorrelation constraint

{hk′σ2Π;th̃t = 0} ⊆ Ct (9b.64)

exogeneous portfolios

• market impact/trans. costs penality

hsignalkt ≡ argmax

hk∈Ct{hk′β

signalkt − λc(hk,hk

t−1)} (9b.65)

c(h,k) ≡ (h− k)′q2(h− k) (9b.66)

ARPM - Advanced Risk and Portfolio Management - arpm.co This update: Mar-28-2017 - Last update