Steven E. Pav steven@cerebellumcapital - R in...

38

Portfolio inference with this one weird trick Steven E. Pav [email protected] Cerebellum Capital May 16, 2014 Steven Pav (Cerebellum Capital) Portfolio Inference ... May 16, 2014 1 / 36

Transcript of Steven E. Pav steven@cerebellumcapital - R in...

Portfolio inference with this one weird trick

Steven E Pavstevencerebellumcapitalcom

Cerebellum Capital

May 16 2014

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 1 36

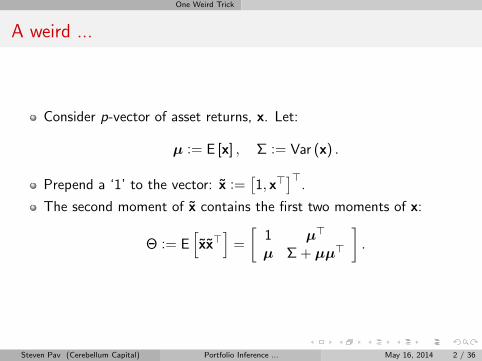

One Weird Trick

A weird

Consider p-vector of asset returns x Let

micro = E [x] Σ = Var (x)

Prepend a lsquo1rsquo to the vector x =[1 xgt

]gt

The second moment of x contains the first two moments of x

Θ = E[xxgt

]=

[1 microgt

micro Σ + micromicrogt

]

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 2 36

One Weird Trick

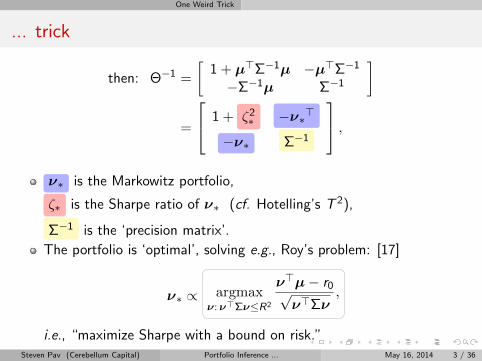

trick

then Θminus1 =

[1 + microgtΣminus1micro minusmicrogtΣminus1

minusΣminus1micro Σminus1

]

=

1 + ζ2lowast minusνlowastgt

minusνlowast Σminus1

νlowast is the Markowitz portfolio

ζlowast is the Sharpe ratio of νlowast (cf Hotellingrsquos T 2)

Σminus1 is the lsquoprecision matrixrsquo

The portfolio is lsquooptimalrsquo solving eg Royrsquos problem [17]

νlowast prop argmaxννgtΣνleR2

νgtmicrominus r0radicνgtΣν

ie ldquomaximize Sharpe with a bound on riskrdquoSteven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 3 36

One Weird Trick

But is it useful

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 4 36

Portfolio Inference

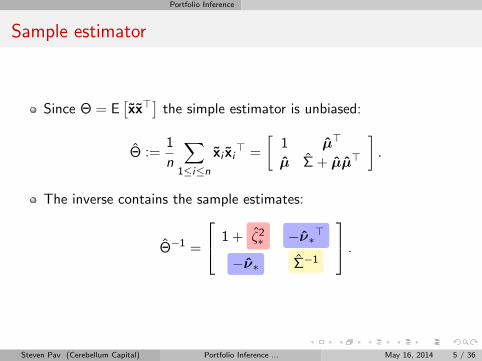

Sample estimator

Since Θ = E[xxgt

]the simple estimator is unbiased

Θ =1

n

sum1leilen

xi xigt =

[1 microgt

micro Σ + micromicrogt

]

The inverse contains the sample estimates

Θminus1 =

1 + ζ2lowast minusνlowastgt

minusνlowast Σminus1

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 5 36

Portfolio Inference

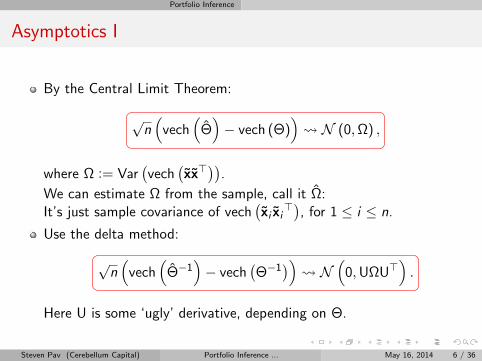

Asymptotics I

By the Central Limit Theorem

radicn(

vech(

Θ)minus vech (Θ)

) N (0Ω)

where Ω = Var(vech

(xxgt

))

We can estimate Ω from the sample call it ΩItrsquos just sample covariance of vech

(xi xi

gt) for 1 le i le n

Use the delta method

radicn(

vech(

Θminus1)minus vech

(Θminus1

)) N

(0UΩUgt

)

Here U is some lsquouglyrsquo derivative depending on Θ

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 6 36

Portfolio Inference

Asymptotics II

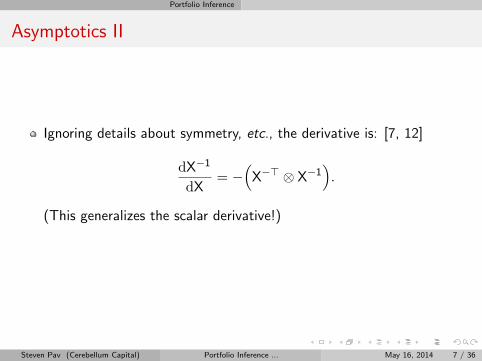

Ignoring details about symmetry etc the derivative is [7 12]

dXminus1

dX= minus

(Xminusgt otimes Xminus1

)

(This generalizes the scalar derivative)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 7 36

Portfolio Inference

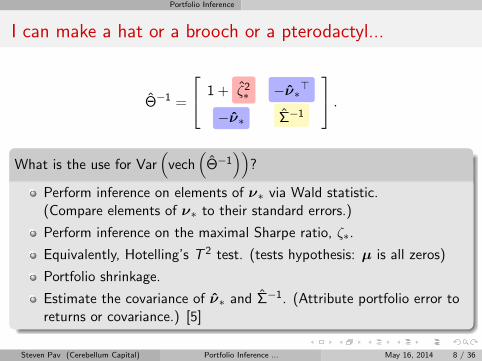

I can make a hat or a brooch or a pterodactyl

Θminus1 =

1 + ζ2lowast minusνlowastgt

minusνlowast Σminus1

What is the use for Var

(vech

(Θminus1

))

Perform inference on elements of νlowast via Wald statistic(Compare elements of νlowast to their standard errors)

Perform inference on the maximal Sharpe ratio ζlowast

Equivalently Hotellingrsquos T 2 test (tests hypothesis micro is all zeros)

Portfolio shrinkage

Estimate the covariance of νlowast and Σminus1 (Attribute portfolio error toreturns or covariance) [5]

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 8 36

Portfolio Inference

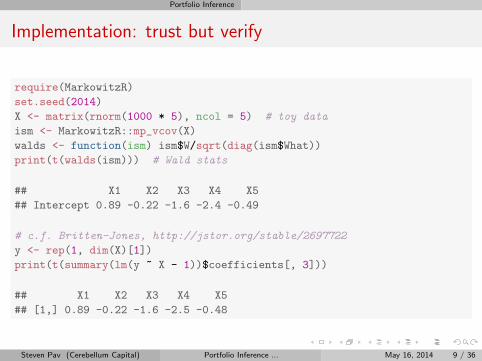

Implementation trust but verify

require(MarkowitzR)

setseed(2014)

X lt- matrix(rnorm(1000 5) ncol = 5) toy data

ism lt- MarkowitzRmp_vcov(X)

walds lt- function(ism) ism$Wsqrt(diag(ism$What))

print(t(walds(ism))) Wald stats

X1 X2 X3 X4 X5

Intercept 089 -022 -16 -24 -049

cf Britten-Jones httpjstororgstable2697722

y lt- rep(1 dim(X)[1])

print(t(summary(lm(y ~ X - 1))$coefficients[ 3]))

X1 X2 X3 X4 X5

[1] 089 -022 -16 -25 -048

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 9 36

Portfolio Inference

Game over

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 10 36

Portfolio Inference

Selling this weird trick

Why weird trick not Britten-Jones or Okhrin et al [4 2 14]

Fewer assumptions fourth moments exist vs normality of returns

Straightforward to use HAC estimator for Ω

Models covariance between return and volatility (At a cost)

Solves a larger problem eg can use for inference on ζ2lowast

Real question whatrsquos wrong with vanilla Markowitz

This trick can be adapted to deal with

Hedged portfolios

Heteroskedasticity

Conditional expected returns

Perhaps more

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 11 36

Portfolio Inference

Selling this weird trick

Why weird trick not Britten-Jones or Okhrin et al [4 2 14]

Fewer assumptions fourth moments exist vs normality of returns

Straightforward to use HAC estimator for Ω

Models covariance between return and volatility (At a cost)

Solves a larger problem eg can use for inference on ζ2lowast

Real question whatrsquos wrong with vanilla Markowitz

This trick can be adapted to deal with

Hedged portfolios

Heteroskedasticity

Conditional expected returns

Perhaps more

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 11 36

Extensions

Hedged portfolios I

Hedging the goal

Returns which are statistically independent from some random variables

Hedging a more realistic goal

A portfolio with zero covariance to some random variables

Hedging an achievable goal

A portfolio with zero sample covariance to some other portfolios oftradeable assets(eg you may have to hold some Mkt to hedge out the Mkt)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 12 36

Extensions

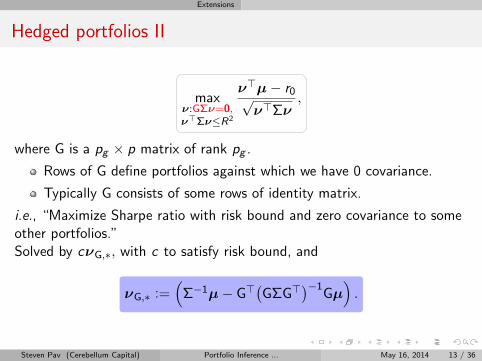

Hedged portfolios II

maxνGΣν=0νgtΣνleR2

νgtmicrominus r0radicνgtΣν

where G is a pg times p matrix of rank pg

Rows of G define portfolios against which we have 0 covariance

Typically G consists of some rows of identity matrix

ie ldquoMaximize Sharpe ratio with risk bound and zero covariance to someother portfoliosrdquoSolved by cνGlowast with c to satisfy risk bound and

νGlowast =(

Σminus1microminus Ggt(GΣGgt

)minus1Gmicro)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 13 36

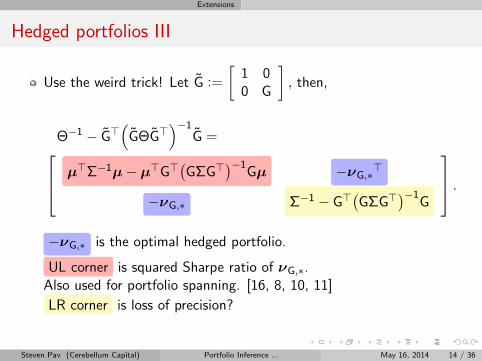

Extensions

Hedged portfolios III

Use the weird trick Let G =

[1 00 G

] then

Θminus1 minus Ggt(

GΘGgt)minus1

G = microgtΣminus1microminus microgtGgt(GΣGgt

)minus1Gmicro minusνGlowast

gt

minusνGlowast Σminus1 minus Ggt(GΣGgt

)minus1G

minusνGlowast is the optimal hedged portfolio

UL corner is squared Sharpe ratio of νGlowastAlso used for portfolio spanning [16 8 10 11]

LR corner is loss of precision

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 14 36

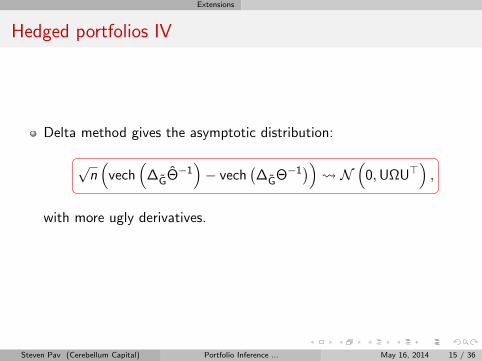

Extensions

Hedged portfolios IV

Delta method gives the asymptotic distribution

radicn(

vech(

∆GΘminus1)minus vech

(∆GΘminus1

)) N

(0UΩUgt

)

with more ugly derivatives

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 15 36

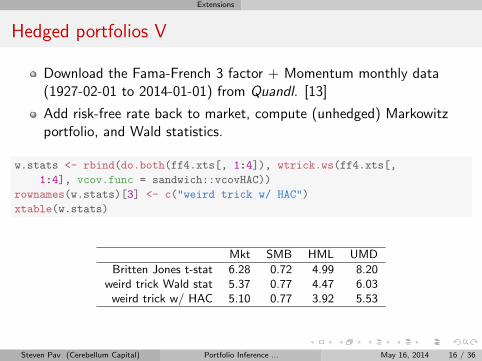

Extensions

Hedged portfolios V

Download the Fama-French 3 factor + Momentum monthly data(1927-02-01 to 2014-01-01) from Quandl [13]

Add risk-free rate back to market compute (unhedged) Markowitzportfolio and Wald statistics

wstats lt- rbind(doboth(ff4xts[ 14]) wtrickws(ff4xts[

14] vcovfunc = sandwichvcovHAC))

rownames(wstats)[3] lt- c(weird trick w HAC)

xtable(wstats)

Mkt SMB HML UMD

Britten Jones t-stat 628 072 499 820weird trick Wald stat 537 077 447 603weird trick w HAC 510 077 392 553

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 16 36

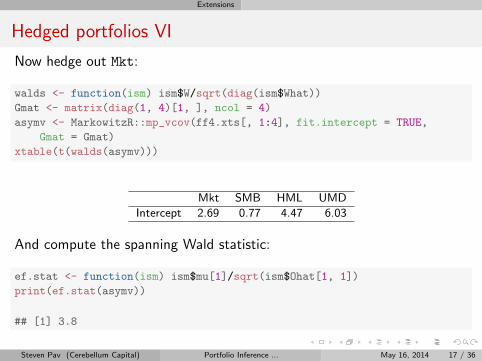

Extensions

Hedged portfolios VI

Now hedge out Mkt

walds lt- function(ism) ism$Wsqrt(diag(ism$What))

Gmat lt- matrix(diag(1 4)[1 ] ncol = 4)

asymv lt- MarkowitzRmp_vcov(ff4xts[ 14] fitintercept = TRUE

Gmat = Gmat)

xtable(t(walds(asymv)))

Mkt SMB HML UMD

Intercept 269 077 447 603

And compute the spanning Wald statistic

efstat lt- function(ism) ism$mu[1]sqrt(ism$Ohat[1 1])

print(efstat(asymv))

[1] 38

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 17 36

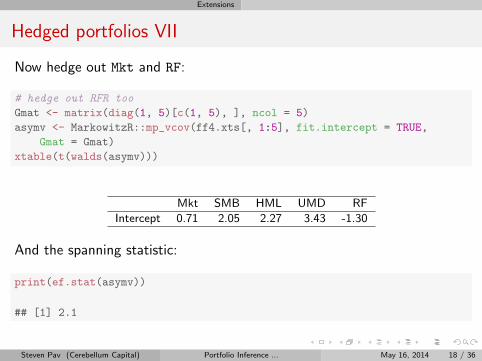

Extensions

Hedged portfolios VII

Now hedge out Mkt and RF

hedge out RFR too

Gmat lt- matrix(diag(1 5)[c(1 5) ] ncol = 5)

asymv lt- MarkowitzRmp_vcov(ff4xts[ 15] fitintercept = TRUE

Gmat = Gmat)

xtable(t(walds(asymv)))

Mkt SMB HML UMD RF

Intercept 071 205 227 343 -130

And the spanning statistic

print(efstat(asymv))

[1] 21

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 18 36

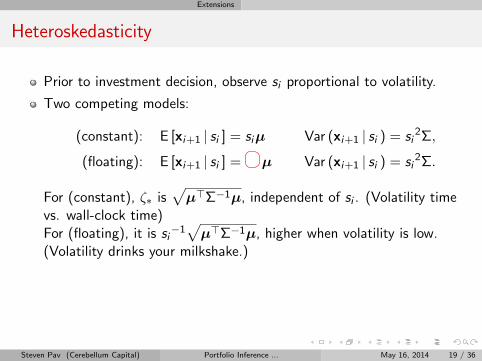

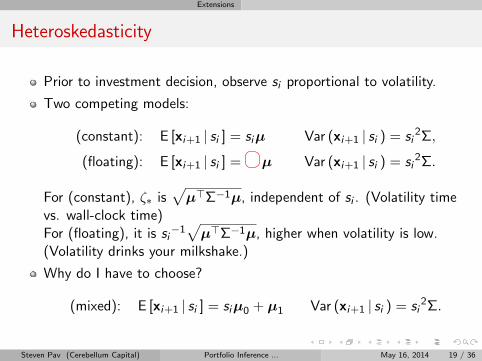

Extensions

Heteroskedasticity

Prior to investment decision observe si proportional to volatility

Two competing models

(constant) E [xi+1 | si ] = simicro Var (xi+1 | si ) = si2Σ

(floating) E [xi+1 | si ] = micro Var (xi+1 | si ) = si2Σ

For (constant) ζlowast isradicmicrogtΣminus1micro independent of si (Volatility time

vs wall-clock time)For (floating) it is si

minus1radicmicrogtΣminus1micro higher when volatility is low

(Volatility drinks your milkshake)

Why do I have to choose

(mixed) E [xi+1 | si ] = simicro0 + micro1 Var (xi+1 | si ) = si2Σ

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 19 36

Extensions

Heteroskedasticity

Prior to investment decision observe si proportional to volatility

Two competing models

(constant) E [xi+1 | si ] = simicro Var (xi+1 | si ) = si2Σ

(floating) E [xi+1 | si ] = micro Var (xi+1 | si ) = si2Σ

For (constant) ζlowast isradicmicrogtΣminus1micro independent of si (Volatility time

vs wall-clock time)For (floating) it is si

minus1radicmicrogtΣminus1micro higher when volatility is low

(Volatility drinks your milkshake)

Why do I have to choose

(mixed) E [xi+1 | si ] = simicro0 + micro1 Var (xi+1 | si ) = si2Σ

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 19 36

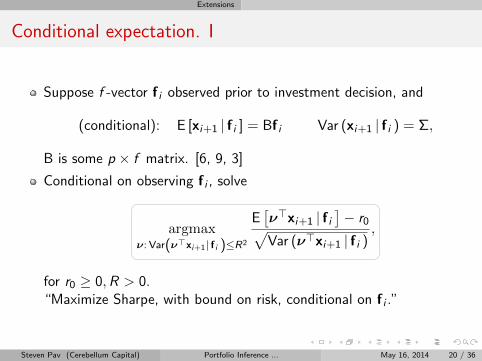

Extensions

Conditional expectation I

Suppose f -vector f i observed prior to investment decision and

(conditional) E [xi+1 | f i ] = Bf i Var (xi+1 | f i ) = Σ

B is some p times f matrix [6 9 3]

Conditional on observing f i solve

argmaxν Var(νgtxi+1| f i )leR2

E[νgtxi+1 | f i

]minus r0radic

Var (νgtxi+1 | f i )

for r0 ge 0R gt 0ldquoMaximize Sharpe with bound on risk conditional on f i rdquo

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 20 36

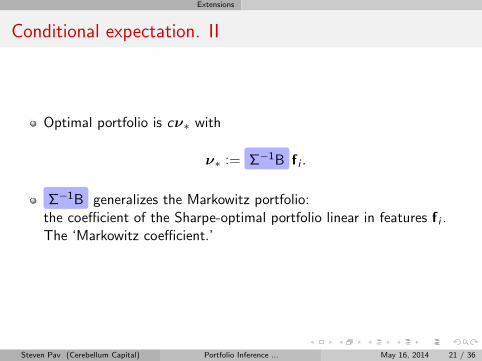

Extensions

Conditional expectation II

Optimal portfolio is cνlowast with

νlowast = Σminus1B f i

Σminus1B generalizes the Markowitz portfoliothe coefficient of the Sharpe-optimal portfolio linear in features f i The lsquoMarkowitz coefficientrsquo

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 21 36

Extensions

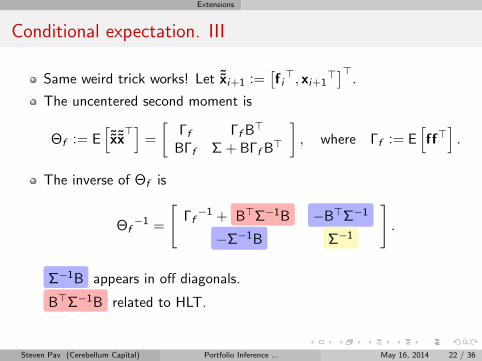

Conditional expectation III

Same weird trick works Let ˜xi+1 =[f igt xi+1

gt]gtThe uncentered second moment is

Θf = E[˜x˜xgt]

=

[Γf Γf Bgt

BΓf Σ + BΓf Bgt

] where Γf = E

[ffgt]

The inverse of Θf is

Θfminus1 =

[Γfminus1 + BgtΣminus1B minusBgtΣminus1

minusΣminus1B Σminus1

]

Σminus1B appears in off diagonals

BgtΣminus1B related to HLT

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 22 36

Extensions

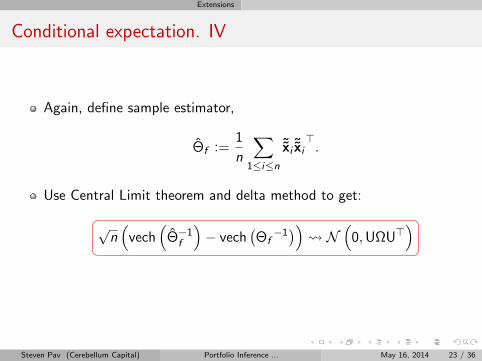

Conditional expectation IV

Again define sample estimator

Θf =1

n

sum1leilen

˜xi˜xigt

Use Central Limit theorem and delta method to get

radicn(

vech(

Θminus1f

)minus vech

(Θfminus1)) N

(0UΩUgt

)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 23 36

Examples

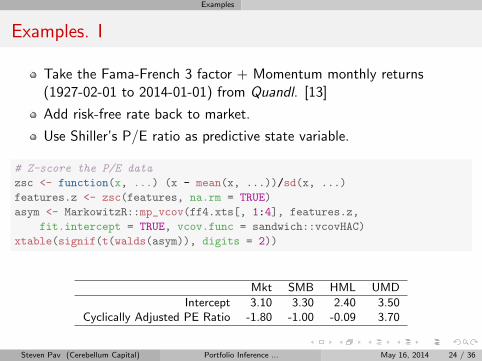

Examples I

Take the Fama-French 3 factor + Momentum monthly returns(1927-02-01 to 2014-01-01) from Quandl [13]

Add risk-free rate back to market

Use Shillerrsquos PE ratio as predictive state variable

Z-score the PE data

zsc lt- function(x ) (x - mean(x ))sd(x )

featuresz lt- zsc(features narm = TRUE)

asym lt- MarkowitzRmp_vcov(ff4xts[ 14] featuresz

fitintercept = TRUE vcovfunc = sandwichvcovHAC)

xtable(signif(t(walds(asym)) digits = 2))

Mkt SMB HML UMD

Intercept 310 330 240 350Cyclically Adjusted PE Ratio -180 -100 -009 370

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 24 36

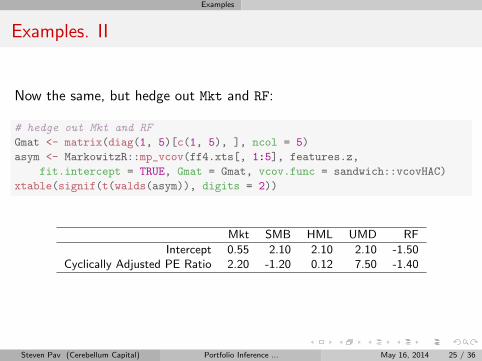

Examples

Examples II

Now the same but hedge out Mkt and RF

hedge out Mkt and RF

Gmat lt- matrix(diag(1 5)[c(1 5) ] ncol = 5)

asym lt- MarkowitzRmp_vcov(ff4xts[ 15] featuresz

fitintercept = TRUE Gmat = Gmat vcovfunc = sandwichvcovHAC)

xtable(signif(t(walds(asym)) digits = 2))

Mkt SMB HML UMD RF

Intercept 055 210 210 210 -150Cyclically Adjusted PE Ratio 220 -120 012 750 -140

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 25 36

Examples

Whatrsquos next

Constrained estimation of Θ (Linear constraints rank constraints)

Generalize to higher dimensions

Fancier hedging model

Conditional covariance models

Jakrsquos Tap

Thank You

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 26 36

Appendix

Bibliography I

[1] Clifford S Asness Andrea Frazzini Ronen Israel and Tobias J Moskowitz Fact fiction and momentum investingPrivately Published May 2014 URL httpssrncomabstract=2435323

[2] Taras Bodnar and Yarema Okhrin On the product of inverse Wishart and normal distributions with applications todiscriminant analysis and portfolio theory Scandinavian Journal of Statistics 38(2)311ndash331 2011 ISSN 1467-9469 doi101111j1467-9469201100729x URL httpdxdoiorg101111j1467-9469201100729x

[3] Michael W Brandt Portfolio choice problems Handbook of financial econometrics 1269ndash336 2009 URLhttpshrreceptidocsrudocs54748conv_1file1pdfpage=298

[4] Mark Britten-Jones The sampling error in estimates of mean-variance efficient portfolio weights The Journal of Finance54(2)655ndash671 1999 URL httpwwwjstororgstable2697722

[5] Vijay Kumar Chopra and William T Ziemba The effect of errors in means variances and covariances on optimal portfoliochoice The Journal of Portfolio Management 19(2)6ndash11 1993 URLhttpfacultyfuquadukeedu~charveyTeachingBA453_2006Chopra_The_effect_of_1993pdf

[6] Gregory Connor Sensible return forecasting for portfolio management Financial Analysts Journal 53(5)pp 44ndash51 1997ISSN 0015198X URL https

facultyfuquadukeedu~charveyTeachingBA453_2006Connor_Sensible_Return_Forecasting_1997pdf

[7] Paul L Fackler Notes on matrix calculus Privately Published 2005 URLhttpwww4ncsuedu~pfacklerMatCalcpdf

[8] Narayan C Giri On the likelihood ratio test of a normal multivariate testing problem The Annals of MathematicalStatistics 35(1)181ndash189 1964 doi 101214aoms1177703740 URLhttpprojecteuclidorgeuclidaoms1177703740

[9] Ulf Herold and Raimond Maurer Tactical asset allocation and estimation risk Financial Markets and PortfolioManagement 18(1)39ndash57 2004 ISSN 1555-4961 doi 101007s11408-004-0104-2 URLhttpdxdoiorg101007s11408-004-0104-2

[10] Gur Huberman and Shmuel Kandel Mean-variance spanning The Journal of Finance 42(4)pp 873ndash888 1987 ISSN00221082 URL httpwwwjstororgstable2328296

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 27 36

Appendix

Bibliography II

[11] Raymond Kan and GuoFu Zhou Tests of mean-variance spanning Annals of Economics and Finance 13(1) 2012 URLhttpwwwaeconfnetArticlesMay2012aef130105pdf

[12] Jan R Magnus and H Neudecker Matrix Differential Calculus with Applications in Statistics and Econometrics WileySeries in Probability and Statistics Texts and References Section Wiley 3rd edition 2007 ISBN 9780471986331 URLhttpwwwjanmagnusnlmiscmdc2007-3rdedition

[13] Raymond McTaggart and Gergely Daroczi Quandl Quandl Data Connection 2014 URLhttpCRANR-projectorgpackage=Quandl R package version 232

[14] Yarema Okhrin and Wolfgang Schmid Distributional properties of portfolio weights Journal of Econometrics 134(1)235ndash256 2006 URL httpwwwsciencedirectcomsciencearticlepiiS0304407605001442

[15] Steven E Pav MarkowitzR Statistical significance of the Markowitz portfolio 2014 URLhttpwwwr-projectorghttpsgithubcomshabbychefMarkowitzR R package version 01403

[16] C Radhakrishna Rao Advanced Statistical Methods in Biometric Research John Wiley and Sons 1952 URLhttpbooksgooglecombooksid=HvFLAAAAMAAJ

[17] A D Roy Safety first and the holding of assets Econometrica 20(3)pp 431ndash449 1952 ISSN 00129682 URLhttpwwwjstororgstable1907413

[18] Mervyn J Silvapulle and Pranab Kumar Sen Constrained statistical inference inequality order and shape restrictionsWiley-Interscience Hoboken NJ 2005 ISBN 0471208272 URL httpbooksgooglecombooksisbn=0471208272

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 28 36

Appendix

Common Questions I

Doesnrsquot this require fourth order moments

I always use relative (or lsquopercentrsquo) returns These are bounded Allmoments exist Identical distribution is a much more questionableassumption

Isnrsquot the complexity Ω(p4)

Portfolio optimization for large p (bigger than 20) is not typicallyrecommended

Wonrsquot estimating a large number of parameters hurt performance

The covariance Var(vech

(xxgt

))has Ω

(p4)

elements but the portfolio isconstructed only from Ω

(p2)

elements as with vanilla Markowitz

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 29 36

Appendix

Common Questions II

I want to hedge out exposure to a non-asset

I want that as well It does not appear to be a simple modification of theweird trick but it may be one discovery away

I want to maximize Sharpe ratio with a time-dependent risk-free rate

I suspect that the lsquorightrsquo way to do this is to include the RFR as an assetthen hedge out exposure to it This effectively allows each asset to have anon-unit lsquobetarsquo to the risk-free which seems like a higher bar than justhedging a constant unit of the risk-free

What was the quote about the pterodactyl

It was from the movie Airplane

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 30 36

Appendix

Common Questions III

I want to hedge out an asset but I do not want the mean of that asset tobe estimated

I believe this can be done with constrained estimation of Θ Briefly if thereare linear constraints one believes Θ satisfies you can solve a least-squaresproblem to get a sample estimate which satisfies the constraints and is nottoo lsquofarrsquo from the unconstrained estimator I have not done the analysisbut believe it is another simple application of the delta method

The conditional expectation model is many-to-many How do I sparseify it

Similar to the above but I believe one would want to specify linearconstraints on the Cholesky factor of Θ This might be more complicatedOr maybe not

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 31 36

Appendix

Common Questions IV

I donrsquot want to deal with the headaches of symmetry

The Cholesky factor of Θ is

[1 0

micro Σ12

] This is a lower triangular

matrix and completely determines Θ I suspect much of the analysis canbe re-couched in terms of this square root but I do not know the matrixderivative of the Cholesky factorization

What about a mashup with Kalman Filters

Sure This should probably be expressed as an update on the Choleskyfactor Θ12

Which portfolio managers are using the weird trick

All of them except you

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 32 36

Appendix

Common Questions V

I am not comforted by the fact that ζ2lowast ζ2

lowast since the portfolio νlowast mayachieve a much lower Sharpe ratio than optimal

Because νlowast is the optimal population Sharpe ratio of any portfolio it is anupper bound on the Sharpe ratio of νlowast To estimate the lsquogaprsquo requires Ibelieve the second-order multivariate delta method I have not done theanalysis

Can you shoehorn a short-sale constraint into the model

I doubt it is feasible It is known for example that Hotellingrsquos statisticunder a positivity constraint is not a similar statistic indicating Sharperatio is an imperfect yardstick for sign-constrained portfolio problems [18]

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 33 36

Appendix

Common Questions VI

Why maximize Sharpe ratio Everyone else maximizes lsquoutilityrsquo

No investor has ever told us their lsquorisk aversion parameterrsquo but they askabout our Sharpe ratio all the time Also read Roy for the connectionbetween Sharpe ratio and probability of a loss [17]

How do you deal with trade costs

It is not clear One hack would be to assume trade costs quadratic in thetarget portfolio I believe this merely leads to an inflation of the Σ butthere are likely complications

Isnrsquot independence of ˜xi suspicious

If the state variables wi depend on the previous period returns xi independence will be violated However the CLT may apply if thesequence is weakly dependent or lsquostrongly mixingrsquo

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 34 36

Appendix

Common Questions VII

How do you detect outliers

This probably requires one to impose a likelihood on ˜xi

Does the math simplify if you assume normal returns

In this case nΘ takes a conditional Wishart distribution

But does it do big data

Computation of Θ is very simple since it is just an uncentered moment

How should a Bayesian approach estimation of Θ

I donrsquot know Ask one I suspect they would assume normal returns thenassume some kind of conditional Wishart prior

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 35 36

Appendix

Common Questions VIII

Does the hedged portfolio involve a projection

It does The hedged portfolio is the optimal portfolio minus a projectionunder the metric induced by Σ

It seems that when I hedge out a single asset only the holdings in thatasset change in the portfolio

If you look at the projection operation the change can only occur in thecolumn space of Ggt which in this case means only the holdings in thesingle asset will change (This is all modulo adjustments to overall grossleverage to meet the risk budget)

Can you back out the traditional significance tests from the asymptoticdistribution of Θ

Possibly but probably a bit uglier than I can stomach

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 36 36

- One Weird Trick

- Portfolio Inference

- Extensions

- Examples

- Appendix

-

One Weird Trick

A weird

Consider p-vector of asset returns x Let

micro = E [x] Σ = Var (x)

Prepend a lsquo1rsquo to the vector x =[1 xgt

]gt

The second moment of x contains the first two moments of x

Θ = E[xxgt

]=

[1 microgt

micro Σ + micromicrogt

]

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 2 36

One Weird Trick

trick

then Θminus1 =

[1 + microgtΣminus1micro minusmicrogtΣminus1

minusΣminus1micro Σminus1

]

=

1 + ζ2lowast minusνlowastgt

minusνlowast Σminus1

νlowast is the Markowitz portfolio

ζlowast is the Sharpe ratio of νlowast (cf Hotellingrsquos T 2)

Σminus1 is the lsquoprecision matrixrsquo

The portfolio is lsquooptimalrsquo solving eg Royrsquos problem [17]

νlowast prop argmaxννgtΣνleR2

νgtmicrominus r0radicνgtΣν

ie ldquomaximize Sharpe with a bound on riskrdquoSteven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 3 36

One Weird Trick

But is it useful

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 4 36

Portfolio Inference

Sample estimator

Since Θ = E[xxgt

]the simple estimator is unbiased

Θ =1

n

sum1leilen

xi xigt =

[1 microgt

micro Σ + micromicrogt

]

The inverse contains the sample estimates

Θminus1 =

1 + ζ2lowast minusνlowastgt

minusνlowast Σminus1

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 5 36

Portfolio Inference

Asymptotics I

By the Central Limit Theorem

radicn(

vech(

Θ)minus vech (Θ)

) N (0Ω)

where Ω = Var(vech

(xxgt

))

We can estimate Ω from the sample call it ΩItrsquos just sample covariance of vech

(xi xi

gt) for 1 le i le n

Use the delta method

radicn(

vech(

Θminus1)minus vech

(Θminus1

)) N

(0UΩUgt

)

Here U is some lsquouglyrsquo derivative depending on Θ

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 6 36

Portfolio Inference

Asymptotics II

Ignoring details about symmetry etc the derivative is [7 12]

dXminus1

dX= minus

(Xminusgt otimes Xminus1

)

(This generalizes the scalar derivative)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 7 36

Portfolio Inference

I can make a hat or a brooch or a pterodactyl

Θminus1 =

1 + ζ2lowast minusνlowastgt

minusνlowast Σminus1

What is the use for Var

(vech

(Θminus1

))

Perform inference on elements of νlowast via Wald statistic(Compare elements of νlowast to their standard errors)

Perform inference on the maximal Sharpe ratio ζlowast

Equivalently Hotellingrsquos T 2 test (tests hypothesis micro is all zeros)

Portfolio shrinkage

Estimate the covariance of νlowast and Σminus1 (Attribute portfolio error toreturns or covariance) [5]

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 8 36

Portfolio Inference

Implementation trust but verify

require(MarkowitzR)

setseed(2014)

X lt- matrix(rnorm(1000 5) ncol = 5) toy data

ism lt- MarkowitzRmp_vcov(X)

walds lt- function(ism) ism$Wsqrt(diag(ism$What))

print(t(walds(ism))) Wald stats

X1 X2 X3 X4 X5

Intercept 089 -022 -16 -24 -049

cf Britten-Jones httpjstororgstable2697722

y lt- rep(1 dim(X)[1])

print(t(summary(lm(y ~ X - 1))$coefficients[ 3]))

X1 X2 X3 X4 X5

[1] 089 -022 -16 -25 -048

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 9 36

Portfolio Inference

Game over

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 10 36

Portfolio Inference

Selling this weird trick

Why weird trick not Britten-Jones or Okhrin et al [4 2 14]

Fewer assumptions fourth moments exist vs normality of returns

Straightforward to use HAC estimator for Ω

Models covariance between return and volatility (At a cost)

Solves a larger problem eg can use for inference on ζ2lowast

Real question whatrsquos wrong with vanilla Markowitz

This trick can be adapted to deal with

Hedged portfolios

Heteroskedasticity

Conditional expected returns

Perhaps more

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 11 36

Portfolio Inference

Selling this weird trick

Why weird trick not Britten-Jones or Okhrin et al [4 2 14]

Fewer assumptions fourth moments exist vs normality of returns

Straightforward to use HAC estimator for Ω

Models covariance between return and volatility (At a cost)

Solves a larger problem eg can use for inference on ζ2lowast

Real question whatrsquos wrong with vanilla Markowitz

This trick can be adapted to deal with

Hedged portfolios

Heteroskedasticity

Conditional expected returns

Perhaps more

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 11 36

Extensions

Hedged portfolios I

Hedging the goal

Returns which are statistically independent from some random variables

Hedging a more realistic goal

A portfolio with zero covariance to some random variables

Hedging an achievable goal

A portfolio with zero sample covariance to some other portfolios oftradeable assets(eg you may have to hold some Mkt to hedge out the Mkt)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 12 36

Extensions

Hedged portfolios II

maxνGΣν=0νgtΣνleR2

νgtmicrominus r0radicνgtΣν

where G is a pg times p matrix of rank pg

Rows of G define portfolios against which we have 0 covariance

Typically G consists of some rows of identity matrix

ie ldquoMaximize Sharpe ratio with risk bound and zero covariance to someother portfoliosrdquoSolved by cνGlowast with c to satisfy risk bound and

νGlowast =(

Σminus1microminus Ggt(GΣGgt

)minus1Gmicro)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 13 36

Extensions

Hedged portfolios III

Use the weird trick Let G =

[1 00 G

] then

Θminus1 minus Ggt(

GΘGgt)minus1

G = microgtΣminus1microminus microgtGgt(GΣGgt

)minus1Gmicro minusνGlowast

gt

minusνGlowast Σminus1 minus Ggt(GΣGgt

)minus1G

minusνGlowast is the optimal hedged portfolio

UL corner is squared Sharpe ratio of νGlowastAlso used for portfolio spanning [16 8 10 11]

LR corner is loss of precision

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 14 36

Extensions

Hedged portfolios IV

Delta method gives the asymptotic distribution

radicn(

vech(

∆GΘminus1)minus vech

(∆GΘminus1

)) N

(0UΩUgt

)

with more ugly derivatives

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 15 36

Extensions

Hedged portfolios V

Download the Fama-French 3 factor + Momentum monthly data(1927-02-01 to 2014-01-01) from Quandl [13]

Add risk-free rate back to market compute (unhedged) Markowitzportfolio and Wald statistics

wstats lt- rbind(doboth(ff4xts[ 14]) wtrickws(ff4xts[

14] vcovfunc = sandwichvcovHAC))

rownames(wstats)[3] lt- c(weird trick w HAC)

xtable(wstats)

Mkt SMB HML UMD

Britten Jones t-stat 628 072 499 820weird trick Wald stat 537 077 447 603weird trick w HAC 510 077 392 553

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 16 36

Extensions

Hedged portfolios VI

Now hedge out Mkt

walds lt- function(ism) ism$Wsqrt(diag(ism$What))

Gmat lt- matrix(diag(1 4)[1 ] ncol = 4)

asymv lt- MarkowitzRmp_vcov(ff4xts[ 14] fitintercept = TRUE

Gmat = Gmat)

xtable(t(walds(asymv)))

Mkt SMB HML UMD

Intercept 269 077 447 603

And compute the spanning Wald statistic

efstat lt- function(ism) ism$mu[1]sqrt(ism$Ohat[1 1])

print(efstat(asymv))

[1] 38

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 17 36

Extensions

Hedged portfolios VII

Now hedge out Mkt and RF

hedge out RFR too

Gmat lt- matrix(diag(1 5)[c(1 5) ] ncol = 5)

asymv lt- MarkowitzRmp_vcov(ff4xts[ 15] fitintercept = TRUE

Gmat = Gmat)

xtable(t(walds(asymv)))

Mkt SMB HML UMD RF

Intercept 071 205 227 343 -130

And the spanning statistic

print(efstat(asymv))

[1] 21

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 18 36

Extensions

Heteroskedasticity

Prior to investment decision observe si proportional to volatility

Two competing models

(constant) E [xi+1 | si ] = simicro Var (xi+1 | si ) = si2Σ

(floating) E [xi+1 | si ] = micro Var (xi+1 | si ) = si2Σ

For (constant) ζlowast isradicmicrogtΣminus1micro independent of si (Volatility time

vs wall-clock time)For (floating) it is si

minus1radicmicrogtΣminus1micro higher when volatility is low

(Volatility drinks your milkshake)

Why do I have to choose

(mixed) E [xi+1 | si ] = simicro0 + micro1 Var (xi+1 | si ) = si2Σ

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 19 36

Extensions

Heteroskedasticity

Prior to investment decision observe si proportional to volatility

Two competing models

(constant) E [xi+1 | si ] = simicro Var (xi+1 | si ) = si2Σ

(floating) E [xi+1 | si ] = micro Var (xi+1 | si ) = si2Σ

For (constant) ζlowast isradicmicrogtΣminus1micro independent of si (Volatility time

vs wall-clock time)For (floating) it is si

minus1radicmicrogtΣminus1micro higher when volatility is low

(Volatility drinks your milkshake)

Why do I have to choose

(mixed) E [xi+1 | si ] = simicro0 + micro1 Var (xi+1 | si ) = si2Σ

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 19 36

Extensions

Conditional expectation I

Suppose f -vector f i observed prior to investment decision and

(conditional) E [xi+1 | f i ] = Bf i Var (xi+1 | f i ) = Σ

B is some p times f matrix [6 9 3]

Conditional on observing f i solve

argmaxν Var(νgtxi+1| f i )leR2

E[νgtxi+1 | f i

]minus r0radic

Var (νgtxi+1 | f i )

for r0 ge 0R gt 0ldquoMaximize Sharpe with bound on risk conditional on f i rdquo

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 20 36

Extensions

Conditional expectation II

Optimal portfolio is cνlowast with

νlowast = Σminus1B f i

Σminus1B generalizes the Markowitz portfoliothe coefficient of the Sharpe-optimal portfolio linear in features f i The lsquoMarkowitz coefficientrsquo

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 21 36

Extensions

Conditional expectation III

Same weird trick works Let ˜xi+1 =[f igt xi+1

gt]gtThe uncentered second moment is

Θf = E[˜x˜xgt]

=

[Γf Γf Bgt

BΓf Σ + BΓf Bgt

] where Γf = E

[ffgt]

The inverse of Θf is

Θfminus1 =

[Γfminus1 + BgtΣminus1B minusBgtΣminus1

minusΣminus1B Σminus1

]

Σminus1B appears in off diagonals

BgtΣminus1B related to HLT

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 22 36

Extensions

Conditional expectation IV

Again define sample estimator

Θf =1

n

sum1leilen

˜xi˜xigt

Use Central Limit theorem and delta method to get

radicn(

vech(

Θminus1f

)minus vech

(Θfminus1)) N

(0UΩUgt

)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 23 36

Examples

Examples I

Take the Fama-French 3 factor + Momentum monthly returns(1927-02-01 to 2014-01-01) from Quandl [13]

Add risk-free rate back to market

Use Shillerrsquos PE ratio as predictive state variable

Z-score the PE data

zsc lt- function(x ) (x - mean(x ))sd(x )

featuresz lt- zsc(features narm = TRUE)

asym lt- MarkowitzRmp_vcov(ff4xts[ 14] featuresz

fitintercept = TRUE vcovfunc = sandwichvcovHAC)

xtable(signif(t(walds(asym)) digits = 2))

Mkt SMB HML UMD

Intercept 310 330 240 350Cyclically Adjusted PE Ratio -180 -100 -009 370

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 24 36

Examples

Examples II

Now the same but hedge out Mkt and RF

hedge out Mkt and RF

Gmat lt- matrix(diag(1 5)[c(1 5) ] ncol = 5)

asym lt- MarkowitzRmp_vcov(ff4xts[ 15] featuresz

fitintercept = TRUE Gmat = Gmat vcovfunc = sandwichvcovHAC)

xtable(signif(t(walds(asym)) digits = 2))

Mkt SMB HML UMD RF

Intercept 055 210 210 210 -150Cyclically Adjusted PE Ratio 220 -120 012 750 -140

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 25 36

Examples

Whatrsquos next

Constrained estimation of Θ (Linear constraints rank constraints)

Generalize to higher dimensions

Fancier hedging model

Conditional covariance models

Jakrsquos Tap

Thank You

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 26 36

Appendix

Bibliography I

[1] Clifford S Asness Andrea Frazzini Ronen Israel and Tobias J Moskowitz Fact fiction and momentum investingPrivately Published May 2014 URL httpssrncomabstract=2435323

[2] Taras Bodnar and Yarema Okhrin On the product of inverse Wishart and normal distributions with applications todiscriminant analysis and portfolio theory Scandinavian Journal of Statistics 38(2)311ndash331 2011 ISSN 1467-9469 doi101111j1467-9469201100729x URL httpdxdoiorg101111j1467-9469201100729x

[3] Michael W Brandt Portfolio choice problems Handbook of financial econometrics 1269ndash336 2009 URLhttpshrreceptidocsrudocs54748conv_1file1pdfpage=298

[4] Mark Britten-Jones The sampling error in estimates of mean-variance efficient portfolio weights The Journal of Finance54(2)655ndash671 1999 URL httpwwwjstororgstable2697722

[5] Vijay Kumar Chopra and William T Ziemba The effect of errors in means variances and covariances on optimal portfoliochoice The Journal of Portfolio Management 19(2)6ndash11 1993 URLhttpfacultyfuquadukeedu~charveyTeachingBA453_2006Chopra_The_effect_of_1993pdf

[6] Gregory Connor Sensible return forecasting for portfolio management Financial Analysts Journal 53(5)pp 44ndash51 1997ISSN 0015198X URL https

facultyfuquadukeedu~charveyTeachingBA453_2006Connor_Sensible_Return_Forecasting_1997pdf

[7] Paul L Fackler Notes on matrix calculus Privately Published 2005 URLhttpwww4ncsuedu~pfacklerMatCalcpdf

[8] Narayan C Giri On the likelihood ratio test of a normal multivariate testing problem The Annals of MathematicalStatistics 35(1)181ndash189 1964 doi 101214aoms1177703740 URLhttpprojecteuclidorgeuclidaoms1177703740

[9] Ulf Herold and Raimond Maurer Tactical asset allocation and estimation risk Financial Markets and PortfolioManagement 18(1)39ndash57 2004 ISSN 1555-4961 doi 101007s11408-004-0104-2 URLhttpdxdoiorg101007s11408-004-0104-2

[10] Gur Huberman and Shmuel Kandel Mean-variance spanning The Journal of Finance 42(4)pp 873ndash888 1987 ISSN00221082 URL httpwwwjstororgstable2328296

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 27 36

Appendix

Bibliography II

[11] Raymond Kan and GuoFu Zhou Tests of mean-variance spanning Annals of Economics and Finance 13(1) 2012 URLhttpwwwaeconfnetArticlesMay2012aef130105pdf

[12] Jan R Magnus and H Neudecker Matrix Differential Calculus with Applications in Statistics and Econometrics WileySeries in Probability and Statistics Texts and References Section Wiley 3rd edition 2007 ISBN 9780471986331 URLhttpwwwjanmagnusnlmiscmdc2007-3rdedition

[13] Raymond McTaggart and Gergely Daroczi Quandl Quandl Data Connection 2014 URLhttpCRANR-projectorgpackage=Quandl R package version 232

[14] Yarema Okhrin and Wolfgang Schmid Distributional properties of portfolio weights Journal of Econometrics 134(1)235ndash256 2006 URL httpwwwsciencedirectcomsciencearticlepiiS0304407605001442

[15] Steven E Pav MarkowitzR Statistical significance of the Markowitz portfolio 2014 URLhttpwwwr-projectorghttpsgithubcomshabbychefMarkowitzR R package version 01403

[16] C Radhakrishna Rao Advanced Statistical Methods in Biometric Research John Wiley and Sons 1952 URLhttpbooksgooglecombooksid=HvFLAAAAMAAJ

[17] A D Roy Safety first and the holding of assets Econometrica 20(3)pp 431ndash449 1952 ISSN 00129682 URLhttpwwwjstororgstable1907413

[18] Mervyn J Silvapulle and Pranab Kumar Sen Constrained statistical inference inequality order and shape restrictionsWiley-Interscience Hoboken NJ 2005 ISBN 0471208272 URL httpbooksgooglecombooksisbn=0471208272

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 28 36

Appendix

Common Questions I

Doesnrsquot this require fourth order moments

I always use relative (or lsquopercentrsquo) returns These are bounded Allmoments exist Identical distribution is a much more questionableassumption

Isnrsquot the complexity Ω(p4)

Portfolio optimization for large p (bigger than 20) is not typicallyrecommended

Wonrsquot estimating a large number of parameters hurt performance

The covariance Var(vech

(xxgt

))has Ω

(p4)

elements but the portfolio isconstructed only from Ω

(p2)

elements as with vanilla Markowitz

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 29 36

Appendix

Common Questions II

I want to hedge out exposure to a non-asset

I want that as well It does not appear to be a simple modification of theweird trick but it may be one discovery away

I want to maximize Sharpe ratio with a time-dependent risk-free rate

I suspect that the lsquorightrsquo way to do this is to include the RFR as an assetthen hedge out exposure to it This effectively allows each asset to have anon-unit lsquobetarsquo to the risk-free which seems like a higher bar than justhedging a constant unit of the risk-free

What was the quote about the pterodactyl

It was from the movie Airplane

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 30 36

Appendix

Common Questions III

I want to hedge out an asset but I do not want the mean of that asset tobe estimated

I believe this can be done with constrained estimation of Θ Briefly if thereare linear constraints one believes Θ satisfies you can solve a least-squaresproblem to get a sample estimate which satisfies the constraints and is nottoo lsquofarrsquo from the unconstrained estimator I have not done the analysisbut believe it is another simple application of the delta method

The conditional expectation model is many-to-many How do I sparseify it

Similar to the above but I believe one would want to specify linearconstraints on the Cholesky factor of Θ This might be more complicatedOr maybe not

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 31 36

Appendix

Common Questions IV

I donrsquot want to deal with the headaches of symmetry

The Cholesky factor of Θ is

[1 0

micro Σ12

] This is a lower triangular

matrix and completely determines Θ I suspect much of the analysis canbe re-couched in terms of this square root but I do not know the matrixderivative of the Cholesky factorization

What about a mashup with Kalman Filters

Sure This should probably be expressed as an update on the Choleskyfactor Θ12

Which portfolio managers are using the weird trick

All of them except you

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 32 36

Appendix

Common Questions V

I am not comforted by the fact that ζ2lowast ζ2

lowast since the portfolio νlowast mayachieve a much lower Sharpe ratio than optimal

Because νlowast is the optimal population Sharpe ratio of any portfolio it is anupper bound on the Sharpe ratio of νlowast To estimate the lsquogaprsquo requires Ibelieve the second-order multivariate delta method I have not done theanalysis

Can you shoehorn a short-sale constraint into the model

I doubt it is feasible It is known for example that Hotellingrsquos statisticunder a positivity constraint is not a similar statistic indicating Sharperatio is an imperfect yardstick for sign-constrained portfolio problems [18]

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 33 36

Appendix

Common Questions VI

Why maximize Sharpe ratio Everyone else maximizes lsquoutilityrsquo

No investor has ever told us their lsquorisk aversion parameterrsquo but they askabout our Sharpe ratio all the time Also read Roy for the connectionbetween Sharpe ratio and probability of a loss [17]

How do you deal with trade costs

It is not clear One hack would be to assume trade costs quadratic in thetarget portfolio I believe this merely leads to an inflation of the Σ butthere are likely complications

Isnrsquot independence of ˜xi suspicious

If the state variables wi depend on the previous period returns xi independence will be violated However the CLT may apply if thesequence is weakly dependent or lsquostrongly mixingrsquo

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 34 36

Appendix

Common Questions VII

How do you detect outliers

This probably requires one to impose a likelihood on ˜xi

Does the math simplify if you assume normal returns

In this case nΘ takes a conditional Wishart distribution

But does it do big data

Computation of Θ is very simple since it is just an uncentered moment

How should a Bayesian approach estimation of Θ

I donrsquot know Ask one I suspect they would assume normal returns thenassume some kind of conditional Wishart prior

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 35 36

Appendix

Common Questions VIII

Does the hedged portfolio involve a projection

It does The hedged portfolio is the optimal portfolio minus a projectionunder the metric induced by Σ

It seems that when I hedge out a single asset only the holdings in thatasset change in the portfolio

If you look at the projection operation the change can only occur in thecolumn space of Ggt which in this case means only the holdings in thesingle asset will change (This is all modulo adjustments to overall grossleverage to meet the risk budget)

Can you back out the traditional significance tests from the asymptoticdistribution of Θ

Possibly but probably a bit uglier than I can stomach

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 36 36

- One Weird Trick

- Portfolio Inference

- Extensions

- Examples

- Appendix

-

One Weird Trick

trick

then Θminus1 =

[1 + microgtΣminus1micro minusmicrogtΣminus1

minusΣminus1micro Σminus1

]

=

1 + ζ2lowast minusνlowastgt

minusνlowast Σminus1

νlowast is the Markowitz portfolio

ζlowast is the Sharpe ratio of νlowast (cf Hotellingrsquos T 2)

Σminus1 is the lsquoprecision matrixrsquo

The portfolio is lsquooptimalrsquo solving eg Royrsquos problem [17]

νlowast prop argmaxννgtΣνleR2

νgtmicrominus r0radicνgtΣν

ie ldquomaximize Sharpe with a bound on riskrdquoSteven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 3 36

One Weird Trick

But is it useful

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 4 36

Portfolio Inference

Sample estimator

Since Θ = E[xxgt

]the simple estimator is unbiased

Θ =1

n

sum1leilen

xi xigt =

[1 microgt

micro Σ + micromicrogt

]

The inverse contains the sample estimates

Θminus1 =

1 + ζ2lowast minusνlowastgt

minusνlowast Σminus1

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 5 36

Portfolio Inference

Asymptotics I

By the Central Limit Theorem

radicn(

vech(

Θ)minus vech (Θ)

) N (0Ω)

where Ω = Var(vech

(xxgt

))

We can estimate Ω from the sample call it ΩItrsquos just sample covariance of vech

(xi xi

gt) for 1 le i le n

Use the delta method

radicn(

vech(

Θminus1)minus vech

(Θminus1

)) N

(0UΩUgt

)

Here U is some lsquouglyrsquo derivative depending on Θ

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 6 36

Portfolio Inference

Asymptotics II

Ignoring details about symmetry etc the derivative is [7 12]

dXminus1

dX= minus

(Xminusgt otimes Xminus1

)

(This generalizes the scalar derivative)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 7 36

Portfolio Inference

I can make a hat or a brooch or a pterodactyl

Θminus1 =

1 + ζ2lowast minusνlowastgt

minusνlowast Σminus1

What is the use for Var

(vech

(Θminus1

))

Perform inference on elements of νlowast via Wald statistic(Compare elements of νlowast to their standard errors)

Perform inference on the maximal Sharpe ratio ζlowast

Equivalently Hotellingrsquos T 2 test (tests hypothesis micro is all zeros)

Portfolio shrinkage

Estimate the covariance of νlowast and Σminus1 (Attribute portfolio error toreturns or covariance) [5]

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 8 36

Portfolio Inference

Implementation trust but verify

require(MarkowitzR)

setseed(2014)

X lt- matrix(rnorm(1000 5) ncol = 5) toy data

ism lt- MarkowitzRmp_vcov(X)

walds lt- function(ism) ism$Wsqrt(diag(ism$What))

print(t(walds(ism))) Wald stats

X1 X2 X3 X4 X5

Intercept 089 -022 -16 -24 -049

cf Britten-Jones httpjstororgstable2697722

y lt- rep(1 dim(X)[1])

print(t(summary(lm(y ~ X - 1))$coefficients[ 3]))

X1 X2 X3 X4 X5

[1] 089 -022 -16 -25 -048

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 9 36

Portfolio Inference

Game over

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 10 36

Portfolio Inference

Selling this weird trick

Why weird trick not Britten-Jones or Okhrin et al [4 2 14]

Fewer assumptions fourth moments exist vs normality of returns

Straightforward to use HAC estimator for Ω

Models covariance between return and volatility (At a cost)

Solves a larger problem eg can use for inference on ζ2lowast

Real question whatrsquos wrong with vanilla Markowitz

This trick can be adapted to deal with

Hedged portfolios

Heteroskedasticity

Conditional expected returns

Perhaps more

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 11 36

Portfolio Inference

Selling this weird trick

Why weird trick not Britten-Jones or Okhrin et al [4 2 14]

Fewer assumptions fourth moments exist vs normality of returns

Straightforward to use HAC estimator for Ω

Models covariance between return and volatility (At a cost)

Solves a larger problem eg can use for inference on ζ2lowast

Real question whatrsquos wrong with vanilla Markowitz

This trick can be adapted to deal with

Hedged portfolios

Heteroskedasticity

Conditional expected returns

Perhaps more

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 11 36

Extensions

Hedged portfolios I

Hedging the goal

Returns which are statistically independent from some random variables

Hedging a more realistic goal

A portfolio with zero covariance to some random variables

Hedging an achievable goal

A portfolio with zero sample covariance to some other portfolios oftradeable assets(eg you may have to hold some Mkt to hedge out the Mkt)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 12 36

Extensions

Hedged portfolios II

maxνGΣν=0νgtΣνleR2

νgtmicrominus r0radicνgtΣν

where G is a pg times p matrix of rank pg

Rows of G define portfolios against which we have 0 covariance

Typically G consists of some rows of identity matrix

ie ldquoMaximize Sharpe ratio with risk bound and zero covariance to someother portfoliosrdquoSolved by cνGlowast with c to satisfy risk bound and

νGlowast =(

Σminus1microminus Ggt(GΣGgt

)minus1Gmicro)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 13 36

Extensions

Hedged portfolios III

Use the weird trick Let G =

[1 00 G

] then

Θminus1 minus Ggt(

GΘGgt)minus1

G = microgtΣminus1microminus microgtGgt(GΣGgt

)minus1Gmicro minusνGlowast

gt

minusνGlowast Σminus1 minus Ggt(GΣGgt

)minus1G

minusνGlowast is the optimal hedged portfolio

UL corner is squared Sharpe ratio of νGlowastAlso used for portfolio spanning [16 8 10 11]

LR corner is loss of precision

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 14 36

Extensions

Hedged portfolios IV

Delta method gives the asymptotic distribution

radicn(

vech(

∆GΘminus1)minus vech

(∆GΘminus1

)) N

(0UΩUgt

)

with more ugly derivatives

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 15 36

Extensions

Hedged portfolios V

Download the Fama-French 3 factor + Momentum monthly data(1927-02-01 to 2014-01-01) from Quandl [13]

Add risk-free rate back to market compute (unhedged) Markowitzportfolio and Wald statistics

wstats lt- rbind(doboth(ff4xts[ 14]) wtrickws(ff4xts[

14] vcovfunc = sandwichvcovHAC))

rownames(wstats)[3] lt- c(weird trick w HAC)

xtable(wstats)

Mkt SMB HML UMD

Britten Jones t-stat 628 072 499 820weird trick Wald stat 537 077 447 603weird trick w HAC 510 077 392 553

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 16 36

Extensions

Hedged portfolios VI

Now hedge out Mkt

walds lt- function(ism) ism$Wsqrt(diag(ism$What))

Gmat lt- matrix(diag(1 4)[1 ] ncol = 4)

asymv lt- MarkowitzRmp_vcov(ff4xts[ 14] fitintercept = TRUE

Gmat = Gmat)

xtable(t(walds(asymv)))

Mkt SMB HML UMD

Intercept 269 077 447 603

And compute the spanning Wald statistic

efstat lt- function(ism) ism$mu[1]sqrt(ism$Ohat[1 1])

print(efstat(asymv))

[1] 38

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 17 36

Extensions

Hedged portfolios VII

Now hedge out Mkt and RF

hedge out RFR too

Gmat lt- matrix(diag(1 5)[c(1 5) ] ncol = 5)

asymv lt- MarkowitzRmp_vcov(ff4xts[ 15] fitintercept = TRUE

Gmat = Gmat)

xtable(t(walds(asymv)))

Mkt SMB HML UMD RF

Intercept 071 205 227 343 -130

And the spanning statistic

print(efstat(asymv))

[1] 21

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 18 36

Extensions

Heteroskedasticity

Prior to investment decision observe si proportional to volatility

Two competing models

(constant) E [xi+1 | si ] = simicro Var (xi+1 | si ) = si2Σ

(floating) E [xi+1 | si ] = micro Var (xi+1 | si ) = si2Σ

For (constant) ζlowast isradicmicrogtΣminus1micro independent of si (Volatility time

vs wall-clock time)For (floating) it is si

minus1radicmicrogtΣminus1micro higher when volatility is low

(Volatility drinks your milkshake)

Why do I have to choose

(mixed) E [xi+1 | si ] = simicro0 + micro1 Var (xi+1 | si ) = si2Σ

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 19 36

Extensions

Heteroskedasticity

Prior to investment decision observe si proportional to volatility

Two competing models

(constant) E [xi+1 | si ] = simicro Var (xi+1 | si ) = si2Σ

(floating) E [xi+1 | si ] = micro Var (xi+1 | si ) = si2Σ

For (constant) ζlowast isradicmicrogtΣminus1micro independent of si (Volatility time

vs wall-clock time)For (floating) it is si

minus1radicmicrogtΣminus1micro higher when volatility is low

(Volatility drinks your milkshake)

Why do I have to choose

(mixed) E [xi+1 | si ] = simicro0 + micro1 Var (xi+1 | si ) = si2Σ

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 19 36

Extensions

Conditional expectation I

Suppose f -vector f i observed prior to investment decision and

(conditional) E [xi+1 | f i ] = Bf i Var (xi+1 | f i ) = Σ

B is some p times f matrix [6 9 3]

Conditional on observing f i solve

argmaxν Var(νgtxi+1| f i )leR2

E[νgtxi+1 | f i

]minus r0radic

Var (νgtxi+1 | f i )

for r0 ge 0R gt 0ldquoMaximize Sharpe with bound on risk conditional on f i rdquo

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 20 36

Extensions

Conditional expectation II

Optimal portfolio is cνlowast with

νlowast = Σminus1B f i

Σminus1B generalizes the Markowitz portfoliothe coefficient of the Sharpe-optimal portfolio linear in features f i The lsquoMarkowitz coefficientrsquo

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 21 36

Extensions

Conditional expectation III

Same weird trick works Let ˜xi+1 =[f igt xi+1

gt]gtThe uncentered second moment is

Θf = E[˜x˜xgt]

=

[Γf Γf Bgt

BΓf Σ + BΓf Bgt

] where Γf = E

[ffgt]

The inverse of Θf is

Θfminus1 =

[Γfminus1 + BgtΣminus1B minusBgtΣminus1

minusΣminus1B Σminus1

]

Σminus1B appears in off diagonals

BgtΣminus1B related to HLT

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 22 36

Extensions

Conditional expectation IV

Again define sample estimator

Θf =1

n

sum1leilen

˜xi˜xigt

Use Central Limit theorem and delta method to get

radicn(

vech(

Θminus1f

)minus vech

(Θfminus1)) N

(0UΩUgt

)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 23 36

Examples

Examples I

Take the Fama-French 3 factor + Momentum monthly returns(1927-02-01 to 2014-01-01) from Quandl [13]

Add risk-free rate back to market

Use Shillerrsquos PE ratio as predictive state variable

Z-score the PE data

zsc lt- function(x ) (x - mean(x ))sd(x )

featuresz lt- zsc(features narm = TRUE)

asym lt- MarkowitzRmp_vcov(ff4xts[ 14] featuresz

fitintercept = TRUE vcovfunc = sandwichvcovHAC)

xtable(signif(t(walds(asym)) digits = 2))

Mkt SMB HML UMD

Intercept 310 330 240 350Cyclically Adjusted PE Ratio -180 -100 -009 370

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 24 36

Examples

Examples II

Now the same but hedge out Mkt and RF

hedge out Mkt and RF

Gmat lt- matrix(diag(1 5)[c(1 5) ] ncol = 5)

asym lt- MarkowitzRmp_vcov(ff4xts[ 15] featuresz

fitintercept = TRUE Gmat = Gmat vcovfunc = sandwichvcovHAC)

xtable(signif(t(walds(asym)) digits = 2))

Mkt SMB HML UMD RF

Intercept 055 210 210 210 -150Cyclically Adjusted PE Ratio 220 -120 012 750 -140

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 25 36

Examples

Whatrsquos next

Constrained estimation of Θ (Linear constraints rank constraints)

Generalize to higher dimensions

Fancier hedging model

Conditional covariance models

Jakrsquos Tap

Thank You

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 26 36

Appendix

Bibliography I

[1] Clifford S Asness Andrea Frazzini Ronen Israel and Tobias J Moskowitz Fact fiction and momentum investingPrivately Published May 2014 URL httpssrncomabstract=2435323

[2] Taras Bodnar and Yarema Okhrin On the product of inverse Wishart and normal distributions with applications todiscriminant analysis and portfolio theory Scandinavian Journal of Statistics 38(2)311ndash331 2011 ISSN 1467-9469 doi101111j1467-9469201100729x URL httpdxdoiorg101111j1467-9469201100729x

[3] Michael W Brandt Portfolio choice problems Handbook of financial econometrics 1269ndash336 2009 URLhttpshrreceptidocsrudocs54748conv_1file1pdfpage=298

[4] Mark Britten-Jones The sampling error in estimates of mean-variance efficient portfolio weights The Journal of Finance54(2)655ndash671 1999 URL httpwwwjstororgstable2697722

[5] Vijay Kumar Chopra and William T Ziemba The effect of errors in means variances and covariances on optimal portfoliochoice The Journal of Portfolio Management 19(2)6ndash11 1993 URLhttpfacultyfuquadukeedu~charveyTeachingBA453_2006Chopra_The_effect_of_1993pdf

[6] Gregory Connor Sensible return forecasting for portfolio management Financial Analysts Journal 53(5)pp 44ndash51 1997ISSN 0015198X URL https

facultyfuquadukeedu~charveyTeachingBA453_2006Connor_Sensible_Return_Forecasting_1997pdf

[7] Paul L Fackler Notes on matrix calculus Privately Published 2005 URLhttpwww4ncsuedu~pfacklerMatCalcpdf

[8] Narayan C Giri On the likelihood ratio test of a normal multivariate testing problem The Annals of MathematicalStatistics 35(1)181ndash189 1964 doi 101214aoms1177703740 URLhttpprojecteuclidorgeuclidaoms1177703740

[9] Ulf Herold and Raimond Maurer Tactical asset allocation and estimation risk Financial Markets and PortfolioManagement 18(1)39ndash57 2004 ISSN 1555-4961 doi 101007s11408-004-0104-2 URLhttpdxdoiorg101007s11408-004-0104-2

[10] Gur Huberman and Shmuel Kandel Mean-variance spanning The Journal of Finance 42(4)pp 873ndash888 1987 ISSN00221082 URL httpwwwjstororgstable2328296

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 27 36

Appendix

Bibliography II

[11] Raymond Kan and GuoFu Zhou Tests of mean-variance spanning Annals of Economics and Finance 13(1) 2012 URLhttpwwwaeconfnetArticlesMay2012aef130105pdf

[12] Jan R Magnus and H Neudecker Matrix Differential Calculus with Applications in Statistics and Econometrics WileySeries in Probability and Statistics Texts and References Section Wiley 3rd edition 2007 ISBN 9780471986331 URLhttpwwwjanmagnusnlmiscmdc2007-3rdedition

[13] Raymond McTaggart and Gergely Daroczi Quandl Quandl Data Connection 2014 URLhttpCRANR-projectorgpackage=Quandl R package version 232

[14] Yarema Okhrin and Wolfgang Schmid Distributional properties of portfolio weights Journal of Econometrics 134(1)235ndash256 2006 URL httpwwwsciencedirectcomsciencearticlepiiS0304407605001442

[15] Steven E Pav MarkowitzR Statistical significance of the Markowitz portfolio 2014 URLhttpwwwr-projectorghttpsgithubcomshabbychefMarkowitzR R package version 01403

[16] C Radhakrishna Rao Advanced Statistical Methods in Biometric Research John Wiley and Sons 1952 URLhttpbooksgooglecombooksid=HvFLAAAAMAAJ

[17] A D Roy Safety first and the holding of assets Econometrica 20(3)pp 431ndash449 1952 ISSN 00129682 URLhttpwwwjstororgstable1907413

[18] Mervyn J Silvapulle and Pranab Kumar Sen Constrained statistical inference inequality order and shape restrictionsWiley-Interscience Hoboken NJ 2005 ISBN 0471208272 URL httpbooksgooglecombooksisbn=0471208272

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 28 36

Appendix

Common Questions I

Doesnrsquot this require fourth order moments

I always use relative (or lsquopercentrsquo) returns These are bounded Allmoments exist Identical distribution is a much more questionableassumption

Isnrsquot the complexity Ω(p4)

Portfolio optimization for large p (bigger than 20) is not typicallyrecommended

Wonrsquot estimating a large number of parameters hurt performance

The covariance Var(vech

(xxgt

))has Ω

(p4)

elements but the portfolio isconstructed only from Ω

(p2)

elements as with vanilla Markowitz

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 29 36

Appendix

Common Questions II

I want to hedge out exposure to a non-asset

I want that as well It does not appear to be a simple modification of theweird trick but it may be one discovery away

I want to maximize Sharpe ratio with a time-dependent risk-free rate

I suspect that the lsquorightrsquo way to do this is to include the RFR as an assetthen hedge out exposure to it This effectively allows each asset to have anon-unit lsquobetarsquo to the risk-free which seems like a higher bar than justhedging a constant unit of the risk-free

What was the quote about the pterodactyl

It was from the movie Airplane

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 30 36

Appendix

Common Questions III

I want to hedge out an asset but I do not want the mean of that asset tobe estimated

I believe this can be done with constrained estimation of Θ Briefly if thereare linear constraints one believes Θ satisfies you can solve a least-squaresproblem to get a sample estimate which satisfies the constraints and is nottoo lsquofarrsquo from the unconstrained estimator I have not done the analysisbut believe it is another simple application of the delta method

The conditional expectation model is many-to-many How do I sparseify it

Similar to the above but I believe one would want to specify linearconstraints on the Cholesky factor of Θ This might be more complicatedOr maybe not

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 31 36

Appendix

Common Questions IV

I donrsquot want to deal with the headaches of symmetry

The Cholesky factor of Θ is

[1 0

micro Σ12

] This is a lower triangular

matrix and completely determines Θ I suspect much of the analysis canbe re-couched in terms of this square root but I do not know the matrixderivative of the Cholesky factorization

What about a mashup with Kalman Filters

Sure This should probably be expressed as an update on the Choleskyfactor Θ12

Which portfolio managers are using the weird trick

All of them except you

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 32 36

Appendix

Common Questions V

I am not comforted by the fact that ζ2lowast ζ2

lowast since the portfolio νlowast mayachieve a much lower Sharpe ratio than optimal

Because νlowast is the optimal population Sharpe ratio of any portfolio it is anupper bound on the Sharpe ratio of νlowast To estimate the lsquogaprsquo requires Ibelieve the second-order multivariate delta method I have not done theanalysis

Can you shoehorn a short-sale constraint into the model

I doubt it is feasible It is known for example that Hotellingrsquos statisticunder a positivity constraint is not a similar statistic indicating Sharperatio is an imperfect yardstick for sign-constrained portfolio problems [18]

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 33 36

Appendix

Common Questions VI

Why maximize Sharpe ratio Everyone else maximizes lsquoutilityrsquo

No investor has ever told us their lsquorisk aversion parameterrsquo but they askabout our Sharpe ratio all the time Also read Roy for the connectionbetween Sharpe ratio and probability of a loss [17]

How do you deal with trade costs

It is not clear One hack would be to assume trade costs quadratic in thetarget portfolio I believe this merely leads to an inflation of the Σ butthere are likely complications

Isnrsquot independence of ˜xi suspicious

If the state variables wi depend on the previous period returns xi independence will be violated However the CLT may apply if thesequence is weakly dependent or lsquostrongly mixingrsquo

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 34 36

Appendix

Common Questions VII

How do you detect outliers

This probably requires one to impose a likelihood on ˜xi

Does the math simplify if you assume normal returns

In this case nΘ takes a conditional Wishart distribution

But does it do big data

Computation of Θ is very simple since it is just an uncentered moment

How should a Bayesian approach estimation of Θ

I donrsquot know Ask one I suspect they would assume normal returns thenassume some kind of conditional Wishart prior

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 35 36

Appendix

Common Questions VIII

Does the hedged portfolio involve a projection

It does The hedged portfolio is the optimal portfolio minus a projectionunder the metric induced by Σ

It seems that when I hedge out a single asset only the holdings in thatasset change in the portfolio

If you look at the projection operation the change can only occur in thecolumn space of Ggt which in this case means only the holdings in thesingle asset will change (This is all modulo adjustments to overall grossleverage to meet the risk budget)

Can you back out the traditional significance tests from the asymptoticdistribution of Θ

Possibly but probably a bit uglier than I can stomach

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 36 36

- One Weird Trick

- Portfolio Inference

- Extensions

- Examples

- Appendix

-

One Weird Trick

But is it useful

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 4 36

Portfolio Inference

Sample estimator

Since Θ = E[xxgt

]the simple estimator is unbiased

Θ =1

n

sum1leilen

xi xigt =

[1 microgt

micro Σ + micromicrogt

]

The inverse contains the sample estimates

Θminus1 =

1 + ζ2lowast minusνlowastgt

minusνlowast Σminus1

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 5 36

Portfolio Inference

Asymptotics I

By the Central Limit Theorem

radicn(

vech(

Θ)minus vech (Θ)

) N (0Ω)

where Ω = Var(vech

(xxgt

))

We can estimate Ω from the sample call it ΩItrsquos just sample covariance of vech

(xi xi

gt) for 1 le i le n

Use the delta method

radicn(

vech(

Θminus1)minus vech

(Θminus1

)) N

(0UΩUgt

)

Here U is some lsquouglyrsquo derivative depending on Θ

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 6 36

Portfolio Inference

Asymptotics II

Ignoring details about symmetry etc the derivative is [7 12]

dXminus1

dX= minus

(Xminusgt otimes Xminus1

)

(This generalizes the scalar derivative)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 7 36

Portfolio Inference

I can make a hat or a brooch or a pterodactyl

Θminus1 =

1 + ζ2lowast minusνlowastgt

minusνlowast Σminus1

What is the use for Var

(vech

(Θminus1

))

Perform inference on elements of νlowast via Wald statistic(Compare elements of νlowast to their standard errors)

Perform inference on the maximal Sharpe ratio ζlowast

Equivalently Hotellingrsquos T 2 test (tests hypothesis micro is all zeros)

Portfolio shrinkage

Estimate the covariance of νlowast and Σminus1 (Attribute portfolio error toreturns or covariance) [5]

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 8 36

Portfolio Inference

Implementation trust but verify

require(MarkowitzR)

setseed(2014)

X lt- matrix(rnorm(1000 5) ncol = 5) toy data

ism lt- MarkowitzRmp_vcov(X)

walds lt- function(ism) ism$Wsqrt(diag(ism$What))

print(t(walds(ism))) Wald stats

X1 X2 X3 X4 X5

Intercept 089 -022 -16 -24 -049

cf Britten-Jones httpjstororgstable2697722

y lt- rep(1 dim(X)[1])

print(t(summary(lm(y ~ X - 1))$coefficients[ 3]))

X1 X2 X3 X4 X5

[1] 089 -022 -16 -25 -048

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 9 36

Portfolio Inference

Game over

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 10 36

Portfolio Inference

Selling this weird trick

Why weird trick not Britten-Jones or Okhrin et al [4 2 14]

Fewer assumptions fourth moments exist vs normality of returns

Straightforward to use HAC estimator for Ω

Models covariance between return and volatility (At a cost)

Solves a larger problem eg can use for inference on ζ2lowast

Real question whatrsquos wrong with vanilla Markowitz

This trick can be adapted to deal with

Hedged portfolios

Heteroskedasticity

Conditional expected returns

Perhaps more

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 11 36

Portfolio Inference

Selling this weird trick

Why weird trick not Britten-Jones or Okhrin et al [4 2 14]

Fewer assumptions fourth moments exist vs normality of returns

Straightforward to use HAC estimator for Ω

Models covariance between return and volatility (At a cost)

Solves a larger problem eg can use for inference on ζ2lowast

Real question whatrsquos wrong with vanilla Markowitz

This trick can be adapted to deal with

Hedged portfolios

Heteroskedasticity

Conditional expected returns

Perhaps more

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 11 36

Extensions

Hedged portfolios I

Hedging the goal

Returns which are statistically independent from some random variables

Hedging a more realistic goal

A portfolio with zero covariance to some random variables

Hedging an achievable goal

A portfolio with zero sample covariance to some other portfolios oftradeable assets(eg you may have to hold some Mkt to hedge out the Mkt)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 12 36

Extensions

Hedged portfolios II

maxνGΣν=0νgtΣνleR2

νgtmicrominus r0radicνgtΣν

where G is a pg times p matrix of rank pg

Rows of G define portfolios against which we have 0 covariance

Typically G consists of some rows of identity matrix

ie ldquoMaximize Sharpe ratio with risk bound and zero covariance to someother portfoliosrdquoSolved by cνGlowast with c to satisfy risk bound and

νGlowast =(

Σminus1microminus Ggt(GΣGgt

)minus1Gmicro)

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 13 36

Extensions

Hedged portfolios III

Use the weird trick Let G =

[1 00 G

] then

Θminus1 minus Ggt(

GΘGgt)minus1

G = microgtΣminus1microminus microgtGgt(GΣGgt

)minus1Gmicro minusνGlowast

gt

minusνGlowast Σminus1 minus Ggt(GΣGgt

)minus1G

minusνGlowast is the optimal hedged portfolio

UL corner is squared Sharpe ratio of νGlowastAlso used for portfolio spanning [16 8 10 11]

LR corner is loss of precision

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 14 36

Extensions

Hedged portfolios IV

Delta method gives the asymptotic distribution

radicn(

vech(

∆GΘminus1)minus vech

(∆GΘminus1

)) N

(0UΩUgt

)

with more ugly derivatives

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 15 36

Extensions

Hedged portfolios V

Download the Fama-French 3 factor + Momentum monthly data(1927-02-01 to 2014-01-01) from Quandl [13]

Add risk-free rate back to market compute (unhedged) Markowitzportfolio and Wald statistics

wstats lt- rbind(doboth(ff4xts[ 14]) wtrickws(ff4xts[

14] vcovfunc = sandwichvcovHAC))

rownames(wstats)[3] lt- c(weird trick w HAC)

xtable(wstats)

Mkt SMB HML UMD

Britten Jones t-stat 628 072 499 820weird trick Wald stat 537 077 447 603weird trick w HAC 510 077 392 553

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 16 36

Extensions

Hedged portfolios VI

Now hedge out Mkt

walds lt- function(ism) ism$Wsqrt(diag(ism$What))

Gmat lt- matrix(diag(1 4)[1 ] ncol = 4)

asymv lt- MarkowitzRmp_vcov(ff4xts[ 14] fitintercept = TRUE

Gmat = Gmat)

xtable(t(walds(asymv)))

Mkt SMB HML UMD

Intercept 269 077 447 603

And compute the spanning Wald statistic

efstat lt- function(ism) ism$mu[1]sqrt(ism$Ohat[1 1])

print(efstat(asymv))

[1] 38

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 17 36

Extensions

Hedged portfolios VII

Now hedge out Mkt and RF

hedge out RFR too

Gmat lt- matrix(diag(1 5)[c(1 5) ] ncol = 5)

asymv lt- MarkowitzRmp_vcov(ff4xts[ 15] fitintercept = TRUE

Gmat = Gmat)

xtable(t(walds(asymv)))

Mkt SMB HML UMD RF

Intercept 071 205 227 343 -130

And the spanning statistic

print(efstat(asymv))

[1] 21

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 18 36

Extensions

Heteroskedasticity

Prior to investment decision observe si proportional to volatility

Two competing models

(constant) E [xi+1 | si ] = simicro Var (xi+1 | si ) = si2Σ

(floating) E [xi+1 | si ] = micro Var (xi+1 | si ) = si2Σ

For (constant) ζlowast isradicmicrogtΣminus1micro independent of si (Volatility time

vs wall-clock time)For (floating) it is si

minus1radicmicrogtΣminus1micro higher when volatility is low

(Volatility drinks your milkshake)

Why do I have to choose

(mixed) E [xi+1 | si ] = simicro0 + micro1 Var (xi+1 | si ) = si2Σ

Steven Pav (Cerebellum Capital) Portfolio Inference May 16 2014 19 36

Extensions

Heteroskedasticity

Prior to investment decision observe si proportional to volatility

Two competing models

(constant) E [xi+1 | si ] = simicro Var (xi+1 | si ) = si2Σ

(floating) E [xi+1 | si ] = micro Var (xi+1 | si ) = si2Σ

For (constant) ζlowast isradicmicrogtΣminus1micro independent of si (Volatility time

vs wall-clock time)For (floating) it is si

minus1radicmicrogtΣminus1micro higher when volatility is low

(Volatility drinks your milkshake)

Why do I have to choose

(mixed) E [xi+1 | si ] = simicro0 + micro1 Var (xi+1 | si ) = si2Σ