September 2012 - delphiadvisors.com · 10 Yrs P3MA 2012:09 2012:12 2013:03 2013:06 2013:09 2013:12...

18

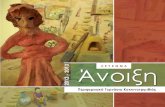

Confidential — Not For Reproduction Copyright 2012 Forest2Market ® A monthly publication of Forest2Market ® , 14045 Ballantyne Corporate Place, Suite 150, Charlotte, NC 28277 The Economic Outlook and macroeconomic forecasts are developed by Delphi Advisors ΤΜ LLC (www.delphiadvisors.com ), and used by Forest2Market with their permission. While the information cited and data used are deemed to be from reliable sources, and the quantitative methods utilized conform to industry standards, any projections are sub- ject to risk and uncertainty and are not guaranteed. Opinions expressed in the commentary are solely those of Delphi Advisors, and may not reflect Forest2Market’s viewpoints. Executive Summary* The fragile U.S. economy appears to be increasingly susceptible to the ongo- ing, synchronized global slowdown. Several classes of negative shocks, hav- ing the potential to throw the economy back into recession, are set to arrive by year’s end; they span the gamut of fiscal, monetary and regulatory poli- cies. Moreover, the polarized political climate seems to be pushing solutions further out of reach. There is little reason to expect a substantial pick-up in employment growth during the next 24 months, as slumping new orders for core capital goods suggest firms are “pulling in their horns” on hiring. Also, because most jobs being created are temporary and/or low-paying, domestic retail spending appears to have tipped over and is heading lower. Housing is one of the economy’s bright spots, although progress is excruciatingly slow. Congress and the Federal Reserve are both faced with unappealing choices that have low probabilities of averting a seemingly inevitable contraction and high likelihood of pushing tangible-asset prices higher. Oil will continue to be buffeted by competing effects of recession, declining supply and geopo- litical strife. ■ Economic Outlook U.S. gross domestic product. The modest upward revision to the Bureau of Economic Analysis’ estimate of 2Q2012 growth in real gross domestic prod- uct (GDP) – from 1.5 to 1.7 percent (Figures 2 and 3, next page) 1 – has done nothing to change our assessment that the U.S. economy remains stuck in low gear. The Federal Reserve’s August Beige Book – which presented eco- nomic anecdotes from around the country – reinforced that assessment by containing 43 instances of some variant of the word “weak,” the highest number since the end of last year. 2 In addition, although the Chicago Federal Reserve’s National Activity Index improved in July relative to June, the three-month moving average – generally considered a more accurate indica- tor than the volatile monthly series – registered a small decline between the two months. 3 “All in all, it’s still an anemic 2 percent economy,” wrote economic com- mentator Larry Kudlow, “the worst recovery…dating back to 1947.” 4 The Council on Foreign Relations’ (CFR) latest quarterly update, which includes a number of excellent charts, compared the current recovery to its post- A PUBLICATION OF FOREST2MARKET A PUBLICATION OF FOREST2MARKET A PUBLICATION OF FOREST2MARKET ® 0.00 0.25 0.50 0.75 1.00 Economic Activity Real GDP H. Starts Ind. Prod. Hist 4cast 0.00 0.25 0.50 0.75 1.00 Costs Prime Rate Oil Price PPI Hist 4cast © Delphi Advisors 0.00 0.25 0.50 0.75 1.00 10 Yrs P3MA 2012:09 2012:12 2013:03 2013:06 2013:09 2013:12 2014:03 2014:06 Exchange Rates Canadian $ Yen Euro Hist 4cast Strong U.S.$ ↑ Weak U.S.$ ↓ Figure 1. Indexed forecasts of macroeco- nomic variables relative to their historical 10-year min, max and average (lower and upper ends of the blue bars, and black dots, respectively), and prior three-month averages (“P3MA”); see Table 1, p. 2., for full variable labels. Source: Delphi Advi- sors September 2012 * Context for this forecast can be found in articles relating recent economic developments to the U.S. forest products sector, posted on Delphi Advi- sors’ website (http://delphiadvisorsmacropulse.blogspot.com/ ).

Transcript of September 2012 - delphiadvisors.com · 10 Yrs P3MA 2012:09 2012:12 2013:03 2013:06 2013:09 2013:12...

Confidential — Not For Reproduction Copyright 2012 Forest2Market®

A monthly publication of Forest2Market®, 14045 Ballantyne Corporate Place, Suite 150, Charlotte, NC 28277

The Economic Outlook and macroeconomic forecasts are developed by Delphi Advisors ΤΜ LLC (www.delphiadvisors.com), and used by Forest2Market with their permission. While the information cited and data used are deemed to be from reliable sources, and the quantitative methods utilized conform to industry standards, any projections are sub-ject to risk and uncertainty and are not guaranteed. Opinions expressed in the commentary are solely those of Delphi Advisors, and may not reflect Forest2Market’s viewpoints.

Executive Summary*

The fragile U.S. economy appears to be increasingly susceptible to the ongo-ing, synchronized global slowdown. Several classes of negative shocks, hav-ing the potential to throw the economy back into recession, are set to arrive by year’s end; they span the gamut of fiscal, monetary and regulatory poli-cies. Moreover, the polarized political climate seems to be pushing solutions further out of reach. There is little reason to expect a substantial pick-up in employment growth during the next 24 months, as slumping new orders for core capital goods suggest firms are “pulling in their horns” on hiring. Also, because most jobs being created are temporary and/or low-paying, domestic retail spending appears to have tipped over and is heading lower. Housing is one of the economy’s bright spots, although progress is excruciatingly slow. Congress and the Federal Reserve are both faced with unappealing choices that have low probabilities of averting a seemingly inevitable contraction and high likelihood of pushing tangible-asset prices higher. Oil will continue to be buffeted by competing effects of recession, declining supply and geopo-litical strife. ■

Economic Outlook

U.S. gross domestic product. The modest upward revision to the Bureau of Economic Analysis’ estimate of 2Q2012 growth in real gross domestic prod-uct (GDP) – from 1.5 to 1.7 percent (Figures 2 and 3, next page)1 – has done nothing to change our assessment that the U.S. economy remains stuck in low gear. The Federal Reserve’s August Beige Book – which presented eco-nomic anecdotes from around the country – reinforced that assessment by containing 43 instances of some variant of the word “weak,” the highest number since the end of last year.2 In addition, although the Chicago Federal Reserve’s National Activity Index improved in July relative to June, the three-month moving average – generally considered a more accurate indica-tor than the volatile monthly series – registered a small decline between the two months.3

“All in all, it’s still an anemic 2 percent economy,” wrote economic com-mentator Larry Kudlow, “the worst recovery…dating back to 1947.”4 The Council on Foreign Relations’ (CFR) latest quarterly update, which includes a number of excellent charts, compared the current recovery to its post-

A P U B L I C A T I O N O F F O R E S T 2 M A R K E TA P U B L I C A T I O N O F F O R E S T 2 M A R K E TA P U B L I C A T I O N O F F O R E S T 2 M A R K E T ®®®

0.00

0.25

0.50

0.75

1.00

Economic Activity

Real GDP H. Starts Ind. Prod.

Hist 4cast

0.00

0.25

0.50

0.75

1.00

Costs

Prime Rate Oil Price PPI

Hist 4cast

© Delphi Advisors

0.00

0.25

0.50

0.75

1.0010 Y

rs

P3M

A

2012:0

9

2012:1

2

2013:0

3

2013:0

6

2013:0

9

2013:1

2

2014:0

3

2014:0

6

Exchange Rates

Canadian $ Yen Euro

Hist 4cast Strong U.S.$↑

Weak U.S.$↓

Figure 1. Indexed forecasts of macroeco-nomic variables relative to their historical 10-year min, max and average (lower and upper ends of the blue bars, and black dots, respectively), and prior three-month averages (“P3MA”); see Table 1, p. 2., for full variable labels. Source: Delphi Advi-sors

September 2012

* Context for this forecast can be found in articles relating recent economic developments to the U.S. forest products sector, posted on Delphi Advi-sors’ website (http://delphiadvisorsmacropulse.blogspot.com/).

2

Table 1. Key economic 4cast statistics

Real

GDP

Housing

Starts

Industrial

Production

Prime

Rate

Oil

Price

CDN$ /

US$

Euro /

US$

Yen /

US$

PPI, Inter-

med Materials

2012:06 1.73 0.754 3.06 3.25 82.41 1.028 0.797 79.3 -0.64

2012:07 1.77 0.746 -1.97 3.25 87.93 1.015 0.815 79.0 -0.95

Estimated 2012:08 1.57 0.786 0.53 3.25 94.16 0.992 0.806 78.7 1.01

2012:09 -0.09 0.760 -0.66 3.25 92.17 0.988 0.810 78.8 -0.20

2012:10 -1.13 0.754 -1.17 3.25 99.16 0.991 0.807 79.9 -0.81

2012:11 -1.18 0.772 -0.58 3.25 100.91 0.993 0.816 81.5 0.902012:12 -1.17 0.732 0.18 3.25 97.07 0.998 0.814 81.6 1.20

2013:01 -2.40 0.717 -1.84 3.25 94.19 1.000 0.801 81.7 0.10

2013:02 -2.38 0.746 -1.43 3.25 95.67 1.006 0.783 82.7 0.14

2013:03 -2.37 0.693 0.49 3.25 103.11 0.996 0.782 82.0 -0.032013:04 -0.08 0.757 -2.36 3.25 102.37 0.982 0.786 81.2 0.76

2013:05 -0.08 0.726 0.06 3.25 101.97 0.971 0.811 79.2 0.74

2013:06 -0.13 0.779 2.32 3.25 96.26 0.983 0.805 81.3 0.172013:07 -1.00 0.787 -2.83 3.45 100.70 0.995 0.798 82.9 0.75

2013:08 -1.32 0.807 1.23 3.45 97.38 1.006 0.790 84.7 0.10

2013:09 -1.55 0.785 -0.32 3.45 96.08 1.005 0.797 84.1 -0.07

2013:10 -1.09 0.878 -0.72 3.65 94.57 1.005 0.784 83.2 -0.162013:11 -0.95 0.897 0.63 3.65 96.06 1.006 0.784 82.3 -0.02

2013:12 -0.94 0.850 0.24 3.65 95.39 0.998 0.794 82.6 0.53

2014:01 -0.38 0.841 -1.13 3.85 100.44 0.987 0.794 82.5 0.422014:02 -0.56 0.807 -0.38 3.85 95.43 0.982 0.792 83.1 0.08

2014:03 -0.56 0.852 0.84 3.85 99.39 0.987 0.779 84.6 0.01

2014:04 -0.89 0.866 -1.86 4.35 98.14 0.990 0.768 85.9 1.38

2014:05 -0.72 0.935 0.87 4.35 94.10 0.995 0.776 86.4 0.422014:06 -0.79 0.918 2.93 4.35 92.97 0.985 0.779 86.5 -0.19

2014:07 4.74 0.942 -1.92 4.75 93.18 0.977 0.774 86.2 0.93

2014:08 4.65 0.935 2.79 4.75 94.38 0.972 0.774 86.6 -0.05

Notes: All actual data from St Louis Federal Reserve Board's FRED database unless otherwise indicated:

Real GDP is annualized percentage change (chained 2000 US dollars)

Housing Starts are millions of units (seasonally adjusted, annualized rate) as reported by U.S. Census Bureau

Prime lending rate is monthly average of daily figures

Oil price is West Texas Intermediate crude, monthly average of daily $/barrel

Canadian dollar, euro and yen exchange rates are monthly averages of daily figures

Monthly percentage change in Producer Price Index, intermediate materials, as reported by Bureau of Labor Statistics

Projections developed by Delphi Advisors

Industrial Production is monthly percentage change in index (index not seasonally adjusted) as reported by the Federal Reserve's G-17 report

Actual

Projected

-3

-2

-1

0

1

2

3

4

5

2009Q

3

2010Q

1

2010Q

3

2011Q

1

2011Q

3

2012Q

1

Percent

PCE PDI NetX GCE GDP

© Delphi Advisors

Figure 2. Contributions -- from personal consumption ex-penditures (PCE), gross private domestic investment (PDI), net exports (NetX), and government consumption expenditures and gross investment (GCE) -- to percentage change in historical real GDP; data are seasonally ad-justed at annual rates. Source: Bureau of Economic Analysis

-0.5

0.0

0.5

1.0

1.5

2.0

Advance Preliminary Final

Estimate

Percent

PCE PDI NetX GCE GDP

© Delphi Advisors

2Q2012

Figure 3. Percentage change in most recent quarter’s real GDP, by estimate and component -- personal consump-tion expenditures (PCE), gross private domestic invest-ment (PDI), net exports (NetX), and government consump-tion expenditures and gross investment (GCE). Source: Bureau of Economic Analysis

3

World War II counterparts and concurred with Kud-low’s observation. “The current recovery remains an outlier among postwar recoveries,” the CFR said. More-over, “the global economic slowdown is beginning to manifest itself in world trade. After staging the strongest recovery of the post–World War II era, growth in world trade has begun to decelerate.”5

Looking forward, however, Kudlow is convinced “there is no recession in sight for now.” His view squares with a MarketWatch survey indicating the United States is projected to grow 2.0 percent in 3Q and 1.9 percent in 4Q2012.6 But there are a number of other gauges sup-porting analyst Gary Shilling’s contention that the world (including the United States) is either already in reces-sion or entering one.7 For example, the correlation be-tween global industrial production and Société Gé-nérale’s Global Economic Newsflow Indicator (or GENI, which captures sentiment regarding trends in the underlying economy from references to economic strength and weakness in newswire and newspaper arti-cles) is forecasting an additional drop-off in global in-dustrial production.8

The economy is entering a “stall speed” phase9 based on research published by the Philadelphia Federal Reserve last year.10 To be fair, the Fed cautioned that focusing on slowing economic growth alone resulted in a number of “false positives” when trying to predict the onset of an impending recession. Hence, views are mixed on what the slowdown means for the future path of the U.S. economy.

Results from the 2Q corporate earnings season also raise a number of worrying questions about the economy’s direction. The percentage of companies beating revenue forecasts during 2Q was the lowest since 2009. Also, for every company that gave a positive outlook, nearly five companies gave negative outlooks; 3Q earnings esti-mates are down sharply, and now show a year-over-year decline of 1.8 percent – that would be the first quarter of negative growth in three years. “What this is telling us is that the economy is slowing down,” said Pankaj Patel, quantitative research analyst at Credit Suisse.11

“If you look at the world, we have essentially Europe, we have the U.S., we have China and emerging econo-mies that depend heavily on China,” analyst Marc Faber said. “Europe is already in a recession and the German economy is still growing very, very slightly but will likely to go into recession soon. The other economies are in recession,” he added. “The U.S. has decelerated, and I don’t see much growth…in the next six to…12 months. If you would [factor in the true] cost of living increase, real GDP would be negative.”12

Mix in the impacts of running into the fiscal, monetary (both of which are expanded upon in subsequent sec-tions of this report) and regulatory “cliffs” set to loom in 2013, and it becomes even more difficult for us to imag-ine the U.S. economy will achieve sufficient velocity to avoid another recession. As for the regulatory cliff, the imposition of several multibillion-dollar regulations are being delayed until after the November elections. Among others, they include:13

* The Labor Department’s Fiduciary Rule, which will increase the cost of retirement planning for middle-class workers

* The Environmental Protection Agency’s (EPA) Ozone Rule, which could impose up to $90 billion in yearly costs on manufacturers and other employers

* The EPA’s rule targeting equipment that manufactur-ing facilities and power plants use to bring in water to prevent overheating, and whose enforcement would cost $1 for every three cents in benefits

* The Department of Transportation rule requiring all new cars and trucks be equipped with a rear-view camera and video display on the dashboard, at a cost of approximately $2.7 billion

* The 130 unfinished mandates under the 2010 Dodd-Frank financial law

Further, political discourse in the United States is be-coming more polarized; despite looming threats, the apparent inability to find common ground is putting so-lutions to fundamental economic problems further out of reach. Circumstances outside the United States are also exerting a drag here. The prospect of Germany entering a recession seems to have undercut the its citizens’ de-sire to bail out the rest of the Eurozone;14 U.S. exports could be adversely affected if the Eurozone weakens further. In addition, Middle East tensions are on the rise and geopolitical unrest there could have significant re-percussions on the global economy.

In light of the information presented above, and for rea-sons discussed below (which also provide the underpin-nings for our forecast shown in Figure 1 and Table 1), we continue to believe the U.S. economy will experi-ence a contraction during the next 24 months – very possibly beginning yet this year. Taken together, those factors have contributed to our becoming more pessi-mistic about the future during the past several months. Consequently, we have the U.S. economy contracting by the end of 3Q2012, experiencing a more severe re-cession than we forecast earlier in the year (although still much shallower than the 2008-2009 recession) and remaining in contraction into 2014.

4

Personal consumption expenditures

• Employment – Non-farm payroll employment rose by 96,000 in August and the unemployment rate dropped by 0.2 percentage point to 8.1 percent. Three-fourths of August’s job gains occurred in food services and drink-ing places (+28,000), in professional and technical ser-vices (+27,000), and in health care (+17,000). Govern-ment employment shrank by 7,000. The change in total non-farm payrolls for June was revised by -19,000 (from +64,000 to +45,000), and the change for July was revised by -22,000 (from +163,000 to +141,000). With-out revisions to July’s estimate, August’s increase would have been even smaller: 77,000 instead of 96,000 jobs.

Perhaps the most important element of the report was that the unemployment rate decreased because 386,000 people gave up looking for work in August (and thus were not included in the unemployment rate calculation) rather than because of the uptick in payrolls. Delphi Ad-visors’ website presents other details from the employ-ment report.15

U.S. manufacturing is one of the sectors “bearing the brunt of the slowdown in global growth.”16 Factory pay-rolls declined by 15,000 workers in August, the biggest drop in two years. The report also showed the work-week shrank and the share of industries that are hiring plunged to the lowest level in almost three years. A shrinking workweek is viewed as a leading indicator of decreasing economic activity. “There is a clear loss of momentum in manufacturing,” said Nigel Gault, chief U.S. economist at IHS Global Insight. “I don’t think manufacturing is going into reverse, but I think it’s stag-nating.”

While the drop in factory hiring was magnified by changes in the annual shutdowns at auto plants, the de-cline extended across multiple industries. Manufacturers of wood products, fabricated metals, electrical equip-ment and semiconductors also reduced headcount in August. Manufacturing is discussed in greater detail below.

“This was not a horrible [employment] report,” con-cluded Eric Green, economist at TD Securities. “It was, however, a weak one.” Scott Brown, chief economist at Raymond James, said the labor market is creating enough jobs to keep pace with the natural expansion of the labor force but far too weak to bring down the un-employment rate. Executives are too uncertain about three issues in particular – the debt crisis in Europe, U.S. fiscal policy and the looming November elections – to hire more workers, Brown added.17

While Brown had plenty of company in describing the report as “weak” others were not as restrained. Mike Shedlock, an investment advisor at Sitka Pacific Capital Management, described the report as “nothing short of a certified disaster.”18 Another analyst, Jim Fickett, commented with uncharacteristic candor, “By far the most important point in the jobs report…is that the overall rate of jobs growth is truly miserable and not getting better. First, three years into the recovery, jobs growth has never been more than just barely above the rate of population growth. This has never happened be-fore, in the whole history of the series. Second, the growth rate seems to have peaked, so the recovery looks unlikely, at this point, to ever gather any real mo-mentum.”19

Perhaps the longest-lasting impacts of the current em-ployment slowdown stems from its uneven effects across demographic groups. This is most readily seen in the labor force participation rate (LFPR). Although the overall LFPR fell to a 31-year low, the really bad news is that a disproportionate share of the workforce losses are occurring in the sub-55 year old age group. “The hope belief is that the younger members of the sub-55 group will have babies and buy houses. As they prosper, GDP will grow, tax revenues will rise,” analyst Bruce Krasting. However, as he pointed out, “The younger workers of today have a very big burden on them. In future years they must generate tax revenue for Wash-ington as D.C. has made very big promises on Social Security and Medicare that can’t be met unless this crop of workers succeeds.”20

“In order to have the unemployment rate go back down, we need significantly more than [July’s original payroll-growth estimate of] 163,000 a month,” said Diana Furchtgott-Roth, a senior fellow at the Manhattan Insti-tute. How many does she think would be needed? “I would say a good target number would be 400,000 jobs a month,” Furchtgott-Roth told Newsmax.TV.21 Unfor-tunately, she did not specify a timeframe over which job growth should average 400,000. If we assume it should extend over a 12-month period, history shows the U.S. economy has not achieved that goal anytime since 1936 (the earliest employment data available from the Labor Department). The closest it came was 392,000 jobs per month for the year ending in July 1941.

Frankly, we do not expect Furchtgott-Roth’s target to be achieved. One reason is that the Conference Board re-vealed new help-wanted ads plunged by 325,700 – the most since February 2009 – during the past two months.22, 23 Longer term, requirements contained in the Patient Protection and Affordable Care Act (a.k.a., Obamacare) will discourage businesses from adding to

5

their payrolls by penalizing companies with 50 or more employees that fail to provide health insurance. “[Pres. Obama] has pushed forward his signature achievement, the new healthcare law, which imposes a tax of $2,000 per worker if you are a firm of 49 or more people. If you have 49 people, your fiftieth worker will cost you $40,000 a year beginning in 2014 if you don’t have the right health insurance,” Furchtgott-Roth said. “These are policies that diminish…rather than expand employ-ment.”21

Figure 3 presents a variety of forecasts related to when employment might return to the January 2008 peak (dashed line) or converge with the number of jobs that likely would exist had the recession not occurred (gray line). At August’s rate of job gains, it would take an-other four years to return to January 2008’s employment level, without adjusting for population growth.

• Personal income and consumer spending – Despite increases since December 2011, in July real per-capita incomes remained almost 3 percent below the peak achieved during the last recession (Figure 5). Nonethe-less, rising incomes have tempted consumers to spend more – often in excess of their incomes. Such was the case in July, according to the BEA, as personal income increased $42.3 billion (0.3 percent) but disposable per-sonal income (DPI) increased only $39.9 billion (0.3 percent). Personal consumption expenditures (PCE) in-creased $46.0 billion (0.4 percent). Real DPI increased 0.3 percent while real PCE increased 0.4 percent.24

The jump in PCE during July was reflected in a corre-sponding rise in the seasonally adjusted retail and food service sales (Figure 6). The Census Bureau reported that consumers increased spending on retail goods by 0.8 percent. Coincidently, retail sales were up by an identical percentage across all (i.e., food service, vehi-cles and “other”) categories. Excluding gasoline sales, retail spending also rose 0.8 percent from June to July.24 Interestingly, the Census Bureau applied a positive July seasonal adjustment factor for the first time in a decade. Had the Census Bureau used (for example) the average of the past decade’s seasonal adjustment factors for July, retail sales would have declined by 1.3 percent.25 Granted, the unique characteristics of this business cycle compared to prior cycles complicate the derivation of appropriate seasonal adjustments; hence, we are reluc-tant to accuse the Census Bureau of anything nefarious.

Statistical mysteries aside, and despite the reported up-tick in July, retail sales may have reached a tipping point resulting from the types of jobs that have been created since the recession ended. While a majority of jobs lost during the downturn were in the middle range of wages, a study by the National Employment Law Project (NELP) revealed a majority of those added dur-ing the recovery have been low paying.26 The Labor Department’s August employment report discussed above followed that trend. “The overarching message here is we don’t just have a jobs deficit; we have a ‘good jobs’ deficit,” said Annette Bernhardt, a NELP policy co-director.

NELP looked at 366 occupations tracked by the Labor Department and aggregated them into three wage

125

130

135

140

145

150

155

160

165

170

2006:0

1

2010:0

1

2014:0

1

2018:0

1

2022:0

1

Total Non-Farm Employment (Million)

Actual

2006:01 jobs + pop growth @ 125K/mo

+400K/mo

+300K/mo

+200K/mo

© Delphi Advisors

+124K/mo (avg since 2010:01)

Figure 4. Length of time required for total non-farm em-ployment to converge with either the January 2008 peak (dashed line) or the January 2006 job level plus subse-quent population growth (gray line). Source of historical data: Bureau of Labor Statistics

6

8

10

12

14

2000:0

1

2002:0

1

2004:0

1

2006:0

1

2008:0

1

2010:0

1

2012:0

1

Personal Income (Trillion $)

33

35

37

39

41

Per-capita RPI (Thous. $)

Nominal Real (2005 $) Real Per-capita

© Delphi Advisors

Figure 5. Nominal personal income (PI), real PI (RPI), and per-capita RPI. Data are seasonally adjusted and annual-ized rates; “real” data expressed in 2005 dollars. Reces-sion shown in blue. Sources: Bureau of Economic Analy-sis and National Bureau of Economic Research

6

groups, each group representing a third of American employment in 2008. The middle third – occupations in fields like construction, manufacturing and information, with median hourly wages of $13.84 to $21.13 – ac-counted for 60 percent of job losses from the beginning of 2008 to early 2010 but only 22 percent of subsequent total job growth.

Higher-wage occupations – with a median wage of $21.14 to $54.55 – represented 19 percent of job losses when employment was falling, and 20 percent of job gains when employment began growing again. Lower-wage occupations, with median hourly wages of $7.69 to $13.83, accounted for 21 percent of job losses during the retraction but 58 percent of all job growth during the subsequent expansion. The fastest growth occurred in retail sales (median wage of $10.97 an hour) and food preparation workers ($9.04 an hour); each category has grown by more than 300,000 workers since June 2009.

Our conclusion is that unless and until the economy cre-ates more – and better-paying – jobs, consumer spend-ing will become progressively more depressed.27 This is something of a chicken-and-egg dilemma, however, as the economy will not create those jobs unless there ap-pears to be some justification for doing so.

Private domestic investment

• Manufacturing and service industry output – Last month we likened U.S. manufacturing to an aging fluo-rescent light bulb. Whereas the sector “burned brightly”

during the initial months of the recovery, it has begun to flicker – especially since late 1Q2012. In fact, the Fed-eral Reserve reported manufacturing industrial produc-tion increased by 0.5 percent in July (relative to June), but that increase was solely the result of seasonal adjust-ments (Figure 7). On a not-seasonally adjusted basis, manufacturing industrial production fell (as is typical between June and July) by 4.4 percent – the largest amount for comparable months since 2008.28

Looking forward, although the value of new orders for manufactured goods jumped by 2.0 percent July,29 the total did not push above the threshold set back in Febru-ary (Figure 8); hence the downward trend in place since March has yet to be reversed. Also, the relatively en-couraging headline number masked some less-optimistic details. Namely, all of the 4.2 percent increase in dura-ble goods orders originated with the transportation sec-tor. Commercial aircraft orders shot up almost 54 per-cent as Boeing signed tentative contracts last month to deliver more than 250 planes, its biggest batch of orders since Christmas. And orders for autos revved up nearly 13 percent after braking slightly in June. Without the volatile transportation category, however, the report’s complexion was dramatically different: Orders exclud-ing transportation actually fell 0.4 percent in July, the second decline in a row and the fourth in five months. Even worse, orders for core capital goods – used by businesses to manufacture their own products – dropped a much sharper 3.4 percent in July following a 2.7 per-cent decline in June.

“At first glance,” chief U.S. economist Paul Ashworth of Capital Economics said, “durable goods orders look

200

250

300

350

400

450

2000:0

1

2002:0

1

2004:0

1

2006:0

1

2008:0

1

2010:0

1

2012:0

1Retail & Food Service Sales (Billion $)

Nominal Real (2000 $)

© Delphi Advisors

Figure 6. Seasonally adjusted nominal and real (also re-indexed for population growth) retail and food service sales; recessions shown in blue. Sources: Census Bu-reau, Bureau of Economic Analysis, Bureau of Labor Sta-tistics and National Bureau of Economic Research

79

83

87

91

95

99

103

107

2000:0

1

2002:0

1

2004:0

1

2006:0

1

2008:0

1

2010:0

1

2012:0

1

Mfg Industrial Production Index

-20

-15

-10

-5

0

5

10

15

Annual % Change, NSA

Not Seas. Adj. Seas. Adj. Ann. Change

© Delphi Advisors

Figure 7. Seasonally and not-seasonally adjusted manu-facturing industrial production (IP) indices, and year-over-year percentage change in not-seasonally adjusted IP; recessions shown in blue. Sources: Federal Reserve Board and National Bureau of Economic Research

7

very impressive, but nothing could be fur-ther from the truth. This is a very weak report.” Much of the blame for flagging core capital goods orders is being laid on the threat of the so-called “fiscal cliff” – the slate of higher taxes and government spending cuts slated to kick in on 1 Janu-ary. “Firms are simply not willing to pull the trigger on big discretionary investment projects until they have more clarity on the policy backdrop for the next four years,” said chief economist Stephen Stanley of Pierpont Securities.30 This con-cern for what could be is one of the rea-sons we believe the U.S. economy will continue to downshift through this year in advance of the “fiscal cliff”.

Data for August indicated little change from July. Markit’s Flash U.S. Manufacturing PMI eked out a slight rise in the headline index, although it was the third-lowest reading in 35 months. “The U.S. manufac-turing sector continued to grow only modestly in Au-gust, with the overall expansion for 3Q set to be at a recovery-low,” commented Rob Dobson, Markit’s sen-ior economist. “Although [August’s] data pointed to a slightly better performance than that registered in July, it nonetheless suggested that manufacturing continued to take a hit from weak economic conditions in key ex-port markets. Higher domestic new orders, in part due to increased marketing and lower selling prices, was partly offset by a further reduction in new export work.”31

The report on manufacturing by the Institute for Supply Management (ISM), which followed Markit’s by a cou-

ple of weeks, communicated a gloomier message. Whereas Markit reported a modest expansion, ISM’s PMI ticked down to 49.6 percent, from 49.8 in July (50 percent is the breakpoint between contraction and ex-pansion). After reciting some report details, Bradley Holcomb, chair of ISM’s Manufacturing Business Sur-vey Committee, concluded with, “Comments from the [respondent] panel generally reflect a slowdown in or-ders and demand, with continuing concern over the un-certain state of global economies.” The mix among the sub-indices was also disheartening, as new orders, new export orders and order backlogs shrank in the face of rising producer inventories and input prices (Table 2).32 Interestingly, ISM reported expanding hiring for the manufacturing sector, whereas the Labor Department reported a contraction (see Employment section).

By contrast, the service sector grew at a faster clip in August, reflected by a 1.1 percentage point rise (to 53.7 percent) in the non-manufacturing index (now known simply as the “NMI”). Comments by Anthony Nieves, chair of ISM’s Non-manufacturing Business Survey Committee, were almost identical to Holcomb’s. “Respondents’ comments continue to be mixed,” said Nieves, “and for the most part reflect uncertainty about business conditions and the economy.” The mix of ser-vice sub-indices was somewhat more upbeat; at least new orders, order backlogs and new export orders in-creased (even if, as in some cases, only barely); how-ever, the proportion of firms facing higher input prices rose dramatically.

Wood Products remained unchanged in August, with the good news of shrinking customer inventories offset by rising imports. Paper Products expanded, but some clouds may be on the horizon from falling new orders, new export orders and order backlogs; some of that bad news may be mitigated by declining imports. Real Es-tate and Ag & Forestry both reported expansion in over-

100

200

300

400

500

2000:0

1

2002:0

1

2004:0

1

2006:0

1

2008:0

1

2010:0

1

2012:0

1

New Orders (Billion $)

Durables Non-durables Nom Total Real Total (2000 $)

© Delphi Advisors

Figure 8. Seasonally adjusted value of new orders for manufactured goods, by sector; recessions shown in blue. Sources: Census Bureau and National Bureau of Economic Research

Category

Manufac-

turing

Wood

Products

Paper

Products Services

Real

Estate

Construc-

tion

Ag. &

Forestry

Changes Reported for July 2012

Overall activity ▼▼ ▼ ▼ ▲▲ ▲ ▼ ▼New orders ▼▼ ▼ ▼ ▲▲ ▲ ▲ ▬Production ▲▲ ▼ ▬

Employment ▲▼ ▬ ▼ ▼ ▬ ▼ ▬

Pace of supplier deliveries ▲▲ ▬ ▼ ▲ ▬ ▲ ▲Inventories ▼▼ ▬ ▲ ▲▲ ▬ ▲ ▲Customers' inventories ▼▼ ▼ ▼Input prices ▼▼ ▬ ▼ ▲ ▬ ▼ ▼Backlog of orders ▼▲ ▼ ▼ ▼▲ ▬ ▲ ▲

New export orders ▼▲ ▬ ▼ ▲ ▬ ▼ ▼

Imports ▲▼ ▬ ▼ ▼ ▬ ▬ ▼

▲▲ = Growing/Increasing at a faster rate ▼ = Decrease, lower or slower

▲▼ = Growing/Increasing at a slower rate ▼▼ = Slowing/Decreasing at a slower rate

▲ = Increase, higher or faster ▼▲ = Slowing/Decreasing at a faster rate

▬ = No change © Delphi Advisors

Table 2. Performance overview of selected industries. Source: Institute for Supply Management

8

all activity, thanks primarily to new orders. Construc-tion, by contrast, is facing an uphill battle from falling new orders and shrinking order backlogs.

We are not alone in our opinion that manufacturing will struggle to expand going forward. “I don’t see any evi-dence that [manufacturing’s] weakness is truly feeding on itself at this point but at the same time, there’s no obvious spark for the economy to look a lot better in the next few months, either,” said Jim O’Sullivan, chief U.S. economist at High Frequency Economics in New York.33 “The softness in manufacturing indicators does not bode well for growth in the second half of the year,” added senior economist Jeremy Lawson of BNP Paribas.34 “The manufacturing sector overall looks like it softened quite sharply,” Bruce Kasman, chief econo-mist at JPMorgan Chase & Co.. “Manufacturing is go-ing through an adjustment that is going to give us – po-tentially for the next couple of months – flat to down readings on the production side.”16

• Construction – Overall construction spending retreated in July, breaking a three-month string of gains.35 Total spending decreased by 0.9 percent (the largest drop in a year), to a seasonally adjusted and annualized rate (SAAR) of $834.4 billion. All categories retreated, es-pecially private residential spending (-1.6 percent). As is often the case, total housing starts also fell, by 1.1 per-cent, to 746,000 units (SAAR). The fallback in starts was concentrated in the single-family category (-35,000 units or 6.5 percent relative to June, to 502,000 units) and could not be overcome by gains in the multi-family category (+27,000 or 12.4 percent, to 244,000 units).

Despite the drop in construction spending, building con-tractors provided a bit of encouragement to forest prod-ucts manufacturers via a fairly substantial boost in resi-dential permits (+51,000 or 6.7 percent relative to June) to a four-year high of 811,000 units. Both the single-family (+20,000 or 4.1 percent, to 511,000 units) and multi-family categories (+31,000 or 11.5 percent, to 300,000 units) contributed to the rise (Figure 9).

Debate continues among analysts as to whether the housing market is recovering. Bill McBride and Barry Ritholtz are perhaps the most prominent opponents in this argument. McBride drew almost immediate criti-cism36 when opining in February 2012 the U.S. housing market had bottomed.37 Ritholtz issued his treatise on the lack of housing recovery in April,38 which, predicta-bly, also spawned rebuttals.39

Although the number of news articles containing the phrase “housing recovery” has skyrocketed in recent

weeks,40 housing bears are on record forecasting no re-covery until anywhere between 201341 and 2020.42 They have marshaled a variety of metrics to buttress their ar-guments: foreclosure statistics,43 the Mortgage Bankers Association’s Mortgage Purchases Index, the American Institute of Architects’ Architecture Billing Index, and residential construction spending,44 among others.

So which is it? Is the housing market still in “purgatory”45 or is it slowly healing?46 To us, it seems difficult to deny the housing market has bottomed and is creeping higher ever so slowly. Housing starts fell to 554,000 units in 2009, down from 2008’s 900,000 units. Starts in 2010 bumped 5.7 percent higher relative to 2009, thanks largely to the homebuyer tax credit pro-gram. The growth rate slowed to 4.5 percent in 2011 (612,000 units). Year-to-date in 2012, starts are moving at a clip equal to an annualized 728,000 units; the per-centage gain over 2011 would be 19 percent if that pace holds.

Many analysts predicate their housing recovery calls on home prices instead of housing starts, however. Here too, though, the situation seems to be mending. The Census Bureau’s median new-home price is up nearly 10 percent from October 2010’s trough; the National Association of Realtors reported existing home prices up over 21 percent from January 2012’s low point.35 The S&P/Case-Shiller Home Price Index registered its first year-over-year gain since 2010, or since 2006 if one ignores the 2010 increase (since the latter was due to the homebuyer tax credit).47 Lender Processing Ser-vices,48 CoreLogic,49 Trulia,50 and the National Associa-tion of Home Builders (NAHB)51 are among other or-ganizations reporting improved home prices. So, while

0.0

0.5

1.0

1.5

2.0

2.5

2002:0

1

2004:0

1

2006:0

1

2008:0

1

2010:0

1

2012:0

1

Permits (Million)

-60

-40

-20

0

20

40

Annual Change, Total Permits (%)

Single-Family Multi-Family % Change

© Delphi Advisors

Figure 9. Components of total housing permits versus annual percentage change in total permits; data are sea-sonally adjusted and annualized. Source: Census Bureau

9

both new- and existing-home median prices remain 15 to 20 percent below their respective peaks, there can be little doubt progress is being made.

As for other indicators, the inventory of existing homes available for sale is down 23 percent from the same time last year.52 LPS reported delinquencies declined by 1.6 percent between June and July.53 Residential construc-tion employment is moving sideways instead of fal-ling.54 NAHB’s Housing Market Index showed im-proved builder confidence in August – the fourth con-secutive month of improvement and the highest reading since February 2007.55 Taken together, the picture that emerges is one of a market on the mend from a devastat-ing crash.

We recognize a number of obstacles remain to be re-solved before the market approaches its historical an-nual average of 1.5 million total starts. They include unsold existing home inventory, continuing replenish-ment of unsold inventory from foreclosed properties, elevated shadow inventories of delinquent homes that will be ultimately foreclosed on, high unemployment, and (as noted above) lasting demographic impacts and low income growth.56 However, presently we view these as obstacles to the pace of recovery, not obstacles that will derail the recovery. To sum up then, our view agrees with that of Michelle Girard, an economist at Royal Bank of Scotland, who said that recent data shows “the housing sector has turned a corner” but “underscores the fact that improvement will be grad-ual.”57

Looking forward, we think the pace of recovery will slow in 2013 relative to 2012 (Figure 10). First, the re-

cession will dampen economic activity, including household formation. Second, posting a 19 percent in-crease on a base of 600,000 units per year (2012’s in-crease relative to 2011) is much easier to accomplish than an increase of 19 percent on a base of 730,000 units per year (what 2013 would have to do to maintain 2012’s pace).

Finally, new homes are built where there is economic activity and limited existing inventory. Those conditions have thus far been met in less-populated areas. For the recovery to continue, however, construction will have to spread into more populated areas that frequently contain a larger unsold inventory. This will present a headwind to continuing increases in new home starts, which is why we see the rate of increase in starts moderating over the next two years.

Lumber futures prices (Figure 11) seem to indicate a mixed outlook among traders. Although price levels are higher for each subsequent contract delivery date (other than the November 2012 contract), signaling that traders expect lumber demand to escalate over the coming year, the price for each contract has declined quite noticeably since mid-August. We infer from those movements that traders became somewhat less bullish about the housing – and perhaps, especially, the lumber export – markets since that time.

0.0

0.4

0.8

1.2

1.6

2.0

2.4

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Total Starts (SAAR, Million)

2005 2009 2011 2012

2013 2014 Hist Avg

© Delphi Advisors

Figure 10. Comparison of recent historical and forecast total housing starts versus long-term (since 1959) histori-cal average starts, by month; data are seasonally adjusted and annualized. Source of historical data: Census Bureau

Contract Open Low Median High Close Trend

---------------------------------- $ / MBF ----------------------------------

2012:09 288.80 282.20 291.15 315.00 284.30 NEG

2012:11 284.10 275.00 291.45 305.90 275.00 NEG

2013:01 292.30 290.70 300.50 316.90 290.70 NEG2013:03 300.10 299.00 308.15 324.10 301.00 FLT

2013:05 302.10 302.10 312.00 324.90 304.20 FLT

2013:07 313.10 311.20 318.45 327.00 311.20 FLT

270

280

290

300

310

320

330

8/5 8/12 8/19 8/26 9/2

Date Observed

$ / MBF

2012:09 2012:11 2013:01

2013:03 2013:05 2013:07

© Delphi Advisors

Figure 11. Statistics of recent lumber futures prices, by contract delivery month. Source: Chicago Mercantile Ex-change

10

Government consumption expenditures

• Fiscal policy – As the total public debt outstanding held by the U.S. government soared past the $16 trillion mark ($16.016 trillion on 31 August58), Simon Black, of the Sovereign Man blog, provided the following per-spective (emphases in the original):59

“It took the U.S. government over 200 years to accu-mulate its first trillion dollars of debt. It took only 286 days to accumulate the most recent trillion dol-lars of debt. 200 years versus 286 days… To say that the trend is unsustainable is a massive understate-ment.

“At an average interest rate of 2.130 percent, Uncle Sam will shuffle $340 billion out the door just in interest payments this year...and it’s a number that’s only going up. To put it in context, China owns so much U.S. debt that the interest income they receive from the Treasury Department is nearly enough to fund their entire military budget.

“…[T]here is no sign of improvement anywhere on the horizon. Last year, the Treasury Department brought in about $2.3 trillion in tax revenue. They spent $2.9 trillion just on ‘mandatory’ programs like Social Security and Medicare, [and the] defense budget.

“In other words, the U.S. government was $600 bil-lion dollars in the hole before paying a dime of in-terest on the debt, or paying the light bill at the White House. In fact the government’s own num-bers reflect a budget deficit through the end of the decade; i.e., the debt level is only going to get higher. These are their own figures.”

Realistically, decision makers at the federal level are essentially boxed in. They can choose to crash into (or sail over) the “fiscal cliff” of letting the G.W. Bush-era tax rates expire at the end of 2012 and implementing the automatic spending cuts agreed to last year. Letting the tax rates expire would mean additional tax bills of up to $5,700 per year per taxpayer – the biggest tax hike since WWII – according to the Tax Foundation.60 Also, Congressional Budget Office (CBO) Director Doug Elmendorf estimated that failing to avoid the fis-cal cliff could cost two million jobs and cause the U.S. economy to contract by 2.9 percent in 1H2013 (-0.5 percent for all of 2013)61, 62 – granted, a far cry from the 8.9 percent dive during 1Q2008, but still very unpleas-ant.

The other alternative is to kick the proverbial debt “can” down the road by extending current tax rates and re-

scinding (or at least postponing) the spending cuts. That option avoids some of the short-term pain but allows the debt to balloon faster, conceivably hastening the United States’ own “Greek” moment.

So, which will it be? “I unfortunately think the most likely scenario is we actually go over the cliff, and then there’s a deal that’s cut in early or mid-January in which you combine a more progressive tax cut [similar in size to] what would have just expired, [along] with entitle-ment reform and simultaneously raise the debt limit,” said Peter Orszag, former director of the Office of Man-agement and Budget in the Obama administration. Or-szag dismissed the CBO’s warning of an impending re-cession. “What [the CBO is] saying is if you go over the cliff and stay there, that is such a fiscal constraint that it will cause a recession,” he said.63

Most analysts are worried about the fiscal cliff derailing the economy next year; but Hugh Johnson, chair of money-management firm Hugh Johnson Advisors, said concerns are already curbing growth. “It is clearly fear, or at least uncertainty, before the reality,” Johnson said. “Nobody knows if their taxes are going to go up, or if it’s going to be postponed and their taxes won’t go up. Anytime there’s uncertainty, it creates inaction, whether it’s on the part of individual investors or corporations.” That uncertainty is helping to keep the unemployment rate high, he noted. “There’s no question that this serves as a drag on corporate hiring and it shows up in the un-employment numbers.”64

Our current operating assumption is more pessimistic than Orszag’s. We believe Congress will take us over the cliff, but subsequently provide only window dress-ing-style temporary tax relief and spending cuts that do little to change the overall debt trajectory. Such a strat-egy both risks the economy sliding into recession near-term and keeps the country on track for a longer-term debt crisis.

• Monetary policy – The Federal Reserve’s tactic of using unconventional monetary policies – whether quantitative easing (QE), twisting the yield curve, or other approaches – to boost economic growth is “like morphine,” said former Assistant Treasury Secretary Neel Kashkari. While the tactic makes people feel bet-ter, generates good headlines and temporarily “gooses” asset prices, it does little to prompt real growth. “For 30 years, our economy borrowed to boost consumption, boost gross domestic product growth,” stated Kashkari, now managing director and head of global equities at PIMCO. “That illusion is over. We need to transition away from borrowing [for consumption] toward savings

11

and investment.”65 Kaskkari’s admonition seems par-ticularly apropos in light of the observation that the United States added an estimated $2.33 of debt for each additional dollar of GDP during 2Q2012.66

We believe the principal reason the Fed’s actions to stimulate the economy by lowering long-term interest rates have been ineffective is a fundamental lack of de-mand to drive economic growth. As Kashkari noted above, past consumption levels (i.e. demand) were am-plified or “leveraged” due to the use of debt. When con-sumers become over-leveraged, however, their capacity to take on debt shrinks and so demand falls from the amplified level to a level actually below what might be considered “normal” for the population. Not until con-sumers sufficiently de-leverage can meaningful growth occur again. Unfortunately, that de-leveraging induces considerable pain across the economy.

Another, related reason is that the short-term interest rates consumers are being charged remain stubbornly high. Since mid-2007 the effective federal funds rate (the interest rate banks charge each other for overnight loans made to fulfill reserve funding requirements) has dropped by 5 percentage points, nearly to zero; the prime rate (historically, the rate banks charged favored customers) has also fallen by 5 percentage points, or roughly 60 percent (Figure 12). Those rate drops have significantly reduced the financing costs of banks and large commercial customers. Other than mortgage rates, however, consumers face interest rates not dramatically different than before the recession. Average rates on 24-month personal loans during 2Q2012 were just 1.6 per-centage points (less than 13 percent) below mid-2007 levels; average credit card rates were 1.7 percentage points (roughly 16 percent) below their mid-2007 peak. Overleveraged consumers who have watched much of their net worth vaporize have rightfully shunned the prospect of taking on additional consumer debt that is associated with still-high interest rates.

On 13 September the Federal Open Market Committee (FOMC) finally dispelled questions of if, when and what it might do with respect to another round of quan-titative easing. Besides keeping the federal funds rate essentially at zero into 2015, the Fed announced its in-tentions to immediately begin an open-ended program of purchasing $40 billion per month of mortgage-backed securities (MBS). In addition, “If the outlook for the labor market does not improve substantially, the com-mittee will continue its purchases of agency mortgage-backed securities, undertake additional asset purchases and employ its other policy tools as appropriate,” the FOMC said in its post-meeting statement.

Although the stock market gapped up in approval of the Fed’s move, cooler heads had been warning – even be-fore the decision was announced – that the unconven-tional policies will cause problems. As we have ex-plained before, Operation Twist involved the Fed selling short-term Treasury bills and (up to three-year) bonds to finance purchases of 10-year and longer-dated Treasur-ies. In a couple of remarkable charts illustrating how the maturity distribution of marketable Treasury securities held by the Fed has changed over time, Stone & McCarthy Research Associates showed that not only is the Fed already monetizing all new issuance of 10- to 30-year Treasuries, but also that “the Fed owns all but $650 billion of 10- to 30-year nominal Treasuries.”67

“Does anyone outside of the Fed think that any new pol-icy news today, in the context of already historically low interest rates, will alter the behavior of any lender, corporate CEO, small business or large, or any individ-ual consumer?” asked Peter Boockvar, equity strategist at Miller Tabak in advance of the Federal Reserve’s an-nouncement. “Will the decision to build that plant, make that loan or buy that car or home be triggered by any new news by the Fed today? I think not.”68

Pragmatic Capitalism’s Cullen Roche offered the fol-lowing reflections on Fed Chair Bernanke’s 13 Septem-ber press conference (emphasis added below):

“‘The [monetary policy] tools we have involve af-fecting financial asset prices,’ Bernanke said. ‘There are a number of different channels [by which im-pacts of Fed policies may be transmitted]…. For example, the prices of homes. To the extent that

the prices of homes begin to rise, consumers will

0

2

4

6

8

10

12

14

16

2000:0

1

2002:0

1

2004:0

1

2006:0

1

2008:0

1

2010:0

1

2012:0

1

Interest Rate (%)

Credit Cards Personal Loans Prime Federal Funds

© Delphi Advisors

Figure 12. Comparison of various interest rates; reces-sions shown in blue. Sources: Federal Reserve Board and National Bureau of Economic Research

12

feel wealthier, they’ll begin to feel more disposed

to spend…. Stock prices – many people own stocks directly or indirectly. The issue here is whether

improving asset prices will make people more

willing to spend…. [I]f people feel their financial

position is better they’ll be more likely to

spend….’

“…[T]he idea that an economic recovery should be driven by consumers who spend out of today’s in-come based on the temporary increase in nominal wealth (which may or may not be higher in the fu-ture) is completely backwards,” Roche responded. “As I explained previously, this idea is similar to a CEO who thinks she/he can improve her/his busi-ness by buying back her/his stock ad infinitum. No, the CEO is there to generate growth in the underly-ing assets. Not to jam up the price of stock traded on a secondary market. The CEO who buys back stock and foregoes real investment in the firm is generat-ing a temporary boost in nominal wealth that may or may not be backed by real growth in the firm. What the US central bank is implementing is very similar. It is an intentional attempt to distort the price of

financial assets in order to generate a short-term

gain that may or may not be justified by im-

provement in the underlying assets. It is the very

definition of Ponzi finance.

“In my opinion,” concluded Roche, “the explicit de-fense of the Ponzi financial policies that got us into this mess is totally indefensible.”

We would add to Roche’s comments that the Federal Reserve, which operates under the dual mandate of maintaining stable prices and full employment, is inten-tionally pursuing a policy of causing prices to increase, and banking on the psychology that increased paper wealth will induce people to spend more – thereby pro-vide a justification for more hiring. Some commentators have described this as a bold move by the Federal Re-serve,69, 70 others as panic.71 Interestingly, even those supporting the Fed’s action are quick to point out it will fall short of addressing unemployment.72, 73

As for the Fed’s decision to also purchase MBS, Mi-chael Schumacher, an analyst at UBS, cautioned: 74

“[T]ilting purchases toward MBS implies that the QE program would need to be quite protracted. Monthly supply of conventional 15- and 30-year, and 30-year [Ginnie Mae] mortgages has averaged about $85-90 billion over the past year and the Fed is already buy-ing about $25 billion. The Fed might be able to buy another $40 billion without disrupting the market.

Assuming that the Fed does a $600 billion program with 75 percent in MBS, it would need to buy $450 billion in mortgages, so in our estimation the pro-gram would need to last nearly a year.”

As if to drive home Schumacher’s point, Walter Kurtz, author of the Sober Look economic blog, also observed that “[g]oing forward the Fed will be a buyer of more than half of all new agency MBS issued. At this point one might as well make [Fannie Mae, Freddie Mac and Ginnie Mae[ part of the Fed or give the central bank a mortgage origination capability.”75 George Mason Uni-versity economics professor responded to Kurtz’s post with “this scares me.”76

Time will tell whether these warnings are prescient. Much like our conclusion that Congress is boxed in on fiscal policy, so too is the Fed on monetary policy. It has options, but most are considered counterproductive,77 offer only limited flexibility with muted short-term benefits78 – particularly for helping avoid another reces-sion79, 80 and/or bringing down unemployment, and carry the risk of “pushing up the prices of…liquid assets”81 like commodities. We explore signs of ongoing price inflation (despite conventional inflation metrics to the contrary) in the following section.

Currency exchange rates. The U.S. dollar lost ground in August on a monthly average basis against all three currencies we track: 2.1 percent relative to Canada’s loonie, 1.0 percent against the euro and 0.3 percent against the yen. On a trade-weighted index basis, the dollar weakened by 0.9 percent against a basket of 26 currencies.82

Although we have used the term sparingly in past re-ports, the idea of “competitive devaluation” has been implicit in our exchange rate forecasts. By competitive devaluation, we mean that national governments and central banks around the world employ fiscal and mone-tary policies that result in their respective currencies temporarily depreciating against their peers. Most times those results are intentional – e.g., to support export-based domestic industries. Not all currencies can simul-taneously devalue against each other, however, thus the relative values of currencies ebb and flow. In the grand scheme of things, as Figure 13 illustrates, that ebb and flow has occurred within a fairly narrow range since 2000.

The green line in Figure 13 shows how the U.S. dollar has fared against the basket of 26 other currencies men-tioned in this section’s introduction.83 We re-indexed the broad trade-weighted U.S. dollar index such that the

13

value in January 2000 was set equal to 1.00 and all sub-sequent movements in the index were proportional changes relative to that initial value. Values below 1.00 mean the dollar depreciated against the other currencies; values above 1.00 mean the dollar appreciated. Since 2000 the dollar has moved inside a range between 0.89 and 1.22, meaning it has depreciated by as much as 11 percent and appreciated as much as 22 percent against the basket of other currencies.

So, how has the dollar (and, by extension, other curren-cies) fared in terms of purchasing tangible assets since January 2000? Not very well in the case of oil (the black line in Figure 13) and copper (red line). Here again, we re-indexed the oil and copper prices such that subse-quent changes were proportional to their respective January 2000 values. Values less than 1.00 mean the dollar’s purchasing power was greater than in January 2000, while values greater than 1.00 mean the dollar’s purchasing power was diminished. Prices for those com-modities have consistently been higher than their Janu-ary 2000 price since January 2003 (oil) and October 2003 (copper). In fact, oil’s June 2008 price was 4.93 times higher than in January 2000; copper’s peak oc-curred later (February 2011) but was also higher than oil’s (5.36 times its January 2000 price). I.e., the dollar has depreciated by as much as 80 percent in oil- and copper-value terms; despite little indication of “price inflation” in conventional metrics (e.g., consumer and producer price indices), the dollar’s purchasing power has declined.

Another inference from Figure 13 is that tangible assets are a better store of value than fiat currencies, including

the dollar. Notice the black line with black-and-red cir-cles in Figure 13. That series represents the metric tons of copper one could buy with a barrel of oil (once again, re-indexed relative to the January 2000 ratio). Although that line exhibits some volatility, it has stayed fairly close to 1.00 (implying stability in the copper-oil price ratio); also, its volatility is nowhere near the magnitude of either dollar-denominated price. Lest one think this relationship is unique between copper and oil, we have also confirmed similar results among gold, silver and iron ore.

Despite our expectation of central banks “opening the spigots” once again in an attempt to boost the flagging global economy, we do not expect currency exchange rates to change markedly as “the tide will raise and lower all ships.” However, all currencies will be losing purchasing power and the most noticeable changes are likely to be in commodity prices.

Canada: Real GDP grew at an annualized 1.8 percent in 2Q2012 (2.4 percent in June alone),84 leading Bank of Canada Governor Mark Carney to state that “some mod-est withdrawal of the present considerable monetary policy stimulus may become appropriate.”85 Ordinarily such action (assuming it is actually taken) would boost the loonie, but Canada’s auto workers are blaming the loonie’s strength for weak exports.86 Nonetheless, Can-ada is a commodity exporter. Thus, if commodity prices rise as explained above, the loonie will likely maintain its current stronger-than-parity position relative to the greenback.

There are some downside risks, however, include rising Canadian consumer indebtedness that could imperil do-mestic growth rates.87 There are also increasing signs of a housing bubble forming in Canada that could bode ill if allowed to continue increasing and then implode as has happened in Ireland, Spain, and the United States.88 However, Canadian mortgage lending practices may mitigate some of that perceived housing-sector risk.

Europe: Perhaps the most significant development in the Eurozone sovereign debt crisis involved European Cen-tral Bank (ECB) President Mario Draghi announcing the creation of yet another program that will be used to buy government bonds. The new Outright Market Transac-tions (OMT) program “will enable us to address severe distortions in government bond markets which originate from…unfounded fears [of the euro’s viability],” Draghi said. The OMT will allow the ECB to buy government bonds with maturities of one to three years in “unlimited” quantities, though purchases will be “sterilized” – or offset by draining an equivalent amount of money from elsewhere in the financial system – in

0

1

2

3

4

5

6

2000:0

1

2002:0

1

2004:0

1

2006:0

1

2008:0

1

2010:0

1

2012:0

1

Relative Index (2000:01 = 1.00)

Copper Oil Tons/Bbl $ Index

© Delphi Advisors

Figure 13. Relative indices of monthly copper and oil prices, metric tons of copper per barrel of oil, and broad, trade-weighted U.S. dollar index. Sources: Federal Re-serve Board and CME Group

14

order to avoid potential inflationary risks from a rise in the money supply.89

“The ECB move is helpful but is not a game-changer. The Eurozone is still in crisis,” said Nouriel Roubini, head of Roubini Global Economics. “Plenty of accidents can still occur. There is austerity fatigue in the periphery and bail-out fatigue in the core. Everybody is restless.”90 We are skeptical the OMT will be effective because – despite the “unlimited” promise – there is a limit to the other funds that can be drained in the sterilization proc-ess. Moreover, the ECB has also promised to not buy the bonds of troubled governments without the express consent of the other European Union countries. Several of the funding countries (especially Austria and the Netherlands) have essentially tied the ECB’s hands by stating quite clearly they will not hand over any more of their citizens’ money to any other country in Europe.91

Meanwhile, most economists see the Eurozone, which generates 16 percent of global economic output, shrink-ing by at least 0.3 percent this year. A recovery may only come in mid-2013. “Weakness is the name of the game,” said Joost Beaumont, a senior economist at ABN AMRO in Amsterdam. “We see another contrac-tion in the third quarter because domestic demand will be hit by fiscal consolidation, rising unemployment, tight credit conditions and the high uncertainty of the Eurozone crisis.”92

We expect the post-OMT euphoria to wear off in due time, but for the euro to remain around current levels until the U.S. fiscal cliff issues take center stage near the end of 2012. At that point, we think the euro could strengthen substantially until mid-year 2013 after which it essentially treads water against the dollar.

Japan: Despite the awful demographic and economic fundamentals that we have elaborated on repeatedly in previous editions of this report, Japan has confounded our (and many others’93) expectations of significant cur-rency depreciation for quite some time. Recent data were “more of the same,” with 2Q GDP growth at only about half the expected rate,94 industrial production and exports slumping in July,95, 96 and threats of a Japanese fiscal cliff stemming from opposition parties blocking a deficit financing bill.97

We continue to believe the yen will eventually begin depreciating against the dollar, but are unsure of the turnaround’s timing. Until we see concrete evidence it is occurring, we are keeping the yen on a roughly even keel against the greenback.

China: Evidence continues to mount that China’s econ-omy is cooling. For example, HSBC’s China manufac-

turing PMI fell to 47.6 in August, down from July’s 49.3, marking the tenth straight month-on-month dete-rioration. Meanwhile, China’s official PMI showed con-ditions at a nine-month low of 49.2 compared to 50.1 in July.98 Another indicator is that customers are taking longer to make payments and even defaulting on debt in a number of China’s industries, particularly machinery, coal and steel; and there is a risk of this spreading to other sectors, warned the state-run Economic Informa-tion Daily.99 Still another shows rail traffic is shrinking at almost 5.4 percent annually.100

Along with Chinese President Hu Jintao’s recent con-cession that China’s “economic growth is facing notable downward pressure,”101 perhaps the most crucial indica-tor is the Chinese government’s announcement of stimu-lus projects totaling 8 trillion yuan “in what appears to be a propaganda effort to reassure the public that the economy is still on track.” The roll call of announce-ments may be a signal that after half a year of fine-tuning monetary policy, the government is preparing to take more drastic measures. While the Communist party had penciled in slower growth of 7.5 percent for this year, in order to restructure and rebalance the economy, there are indications that China may suffer, or may al-ready have suffered, a “hard landing,” where growth would fall to below 7 percent. “A hard landing in China would look like 4Q2008 and 1Q2009 when exports col-lapsed, factories had no orders and migrant workers were laid off by the tens of millions,” said Wang Tao, an economist at UBS.102

Because the renminbi is still effectively pegged to the dollar, China’s glut of new stimulus spending is unlikely to have much impact on yuan-dollar exchange rates. It will, however, translate into more money units chasing the same number of physical goods. Beijing has admit-ted it already has a food inflation problem, and thus will release arguably token amounts of corn and rice from state reserves “to help tame inflation and reduce imports as the worst U.S. drought in half a century pushes corn prices to global records, creating fears of a world food crisis.”103 In our view, it seems as if decision makers there are pouring gasoline on fire with one hand while trying to extinguish the fire with the other.

Energy. The monthly average U.S.-dollar price of West Texas Intermediate (WTI) crude oil continued its ascent in August, advancing by $6.23 (7.1 percent) to $94.16 per barrel. That rise was concurrent with a weakening of the dollar, the lagged impacts of an increase in con-sumption of 208,000 barrels per day (BPD) – to 18.9 million BPD – during June, and a drawdown of still-plentiful crude stocks.104

15

With prospects for slower global economic growth, fu-tures traders apparently believe crude oil prices will stage a modest retreat to below current levels after a run-up ending in mid-2013 (Figure 14). Sustained higher crude oil prices have resulted in increased pro-duction from U.S. oil fields; oil production from these fields has amounted to nearly 1 million barrels of crude oil per day over the past year.105 While that trend has been in place since 2008 this source of incremental U.S. supply is very price sensitive and any price retrench-ment will see it dry up.106

Several crosscurrents are at work in crude oil markets. First, as mentioned above and discussed in previous sec-tions of this report, there is the growing acceptance of a global slowdown in growth.107 Should that continue, demand for crude oil will fall along with its price; Jeff Kennedy, chief commodity strategist at Elliott Wave International, has gone out on a limb with his prediction that oil will plummet to its December 2008 of $32.40 per barrel.108 A short-term price crash is certainly possi-ble if the global downturn is severe enough, but central bankers will almost certainly respond by increasing the amount of currency and credit in an attempt to stimulate demand; doing so will cause currency to lose purchasing power, however. Although currency exchange rates may not shift markedly (discussed in the exchange rate sec-tion above), global purchasing power is likely to ebb as commodity prices (including crude oil) increase.109

Another current is the increasing cost of extraction combined with the price national oil producers need to get in order to meet promised spending. Currently the latter is around $90 per barrel for WTI and $100 for Brent crude.110 We remain agnostic on the Peak Oil the-ory, but are convinced of the truthfulness of peak cheap oil. As Ambrose Evans-Pritchard observed recently, “some of Brazil’s non-shale fields are so far offshore in the Atlantic that helicopters have to be refueled in the air. The drilling is through layers of salt that blind the imaging technology. Extraction is even harder and more costly than the task that overwhelmed BP at Macondo.”111 Granted, Brazil is just one example, but it illustrates the ever more-common challenges facing oil producers.

Geopolitical risk is another current with the potential to send prices skyrocketing. While the events of the “Arab Spring” have largely slipped off media headlines, there has been no lack of action in the Middle East; in general tensions are tightening across the region. Whether it is Syria,112 Turkey,113, 114 or Israel,115 Iran is involved. Sanctions designed to shut in Iran’s oil exports are re-portedly wreaking havoc with the Iranian population,116 and could cause the country’s government to retaliate in

some way. E.g., if Iranian society is truly destabilizing, the prospect of Iran closing the Straits of Hormuz117 – generally regarded as a last resort action – becomes a more likely reality. A recent development that has re-ceived but scant news attention in the U.S. media is an apparently coordinated effort by the U.S. and Russia to reduce their direct support to front-line combatants Is-rael (U.S. withholding direct support) and Syria (Russia withholding direct support).118, 119 Whether such a gam-bit ultimately defuses the present conflict between Israel and Syria/Iran or results in heightened regional volatility is anyone’s guess.

A number of pundits have apparently concluded Iran would not blockade either the Strait of Hormuz and/or Suez Canal because doing so would prove destructive to its economy. To us, missing from such analyses is the possibility of a selective blockade in which Iranian ship-ments and those of its allies are allowed to pass. For example, all 20 of Iran’s major oil customers are cur-rently exempted from sanctions for six months.120 Just as oil sanctions are not really sanctions, it seems plausi-ble Iran would continue to find ways to sell its oil to global markets even if it blockades the Straits of Hor-muz to other oil traffic. In fact, there is some indication Iran is continuing to sell oil despite the sanctions. Bloomberg reports Iranian oil tankers, which have been stationary since February as sanctions began being im-posed, are suddenly on the move. Iranian Oil Minister Rostam Qasemi recently commented, “[t]he country’s oil exports will never be halted because oil consuming countries need Iranian crude. There are many ways to

90

93

96

99

102

105

2012:0

9

2012:1

2

2013:0

3

2013:0

6

2013:0

9

2013:1

2

2014:0

3

2014:0

6

Oil Price ($ per Barrel)

BAR(S) RED IF LAST < AVG

BAR(S) BLUE IF LAST > AVG

Data collected betw een 08/06/2012 and 09/07/2012

© Delphi Advisors

4cast

Figure 14. Futures and Delphi Advisors’ forecast prices for light crude oil by delivery month. The vertical black lines represent the range of futures closing prices during the data-collection period; the colored bars show the rela-tionship between the last observed and average closing prices. Source: New York Mercantile Exchange

16

easily sell oil, one of which is to take advantage of busi-nessmen and the private sector,”121

We conclude, then, that although a temporary correction is not out of the question, the relative risks of the com-peting crosscurrents favor higher oil prices.

Wrap-up.

The upward revisions to 2Q2012’s GDP growth are not enough to overcome the observation that economic ac-tivity continues to be anemic. Moreover, many of the

most recent data releases suggest there has been addi-tional “rot on the vine” or only modest improvement in specific sectors. Residential construction is one of those few bright spots, and even its glow is quite dim. With the combination of the synchronized global slowdown, prospects for higher oil prices, the fiscal, monetary and regulatory “cliffs” quickly coming into view, and the polarized political climate that frustrates problem solv-ing, we believe the risks of another economic downturn are multiplying. We expect that downturn to be shal-lower than the 2008-2009 recession, but the subsequent recovery will also be hampered by excessive sovereign and private debt. ■

1 http://delphiadvisorsmacropulse.blogspot.com/2012/08/2q2012-gross-domestic-product-second.html

2 http://www.marketwatch.com/story/us-economy-growing-gradually-fed-2012-08-29

3 http://www.chicagofed.org/digital_assets/publications/cfnai/2012/cfnai_august2012.pdf

4 http://www.moneynews.com/StreetTalk/Recession-Worst-Recovery-economy/2012/08/17/id/448889

5 http://www.cfr.org/geoeconomics/quarterly-update-economic-recovery-historical-context/p25774

6 http://www.marketwatch.com/story/us-grew-at-17-pace-in-second-quarter-2012-08-29

7 http://www.moneynews.com/StreetTalk/Shilling-US-global-recession/2012/08/14/id/448463

8 http://www.zerohedge.com/news/newsflow-sentiment-confirms-global-recession

9 http://blogs.wsj.com/economics/2011/07/29/has-the-economy-hit-stall-speed/

10 http://www.federalreserve.gov/pubs/feds/2011/201124/201124pap.pdf

11 http://www.reuters.com/article/2012/08/17/us-usa-earnings-idUSBRE87G0XV20120817

12 http://www.moneynews.com/StreetTalk/Faber-recession-Germany-100-/2012/08/24/id/449639

13 http://www.moneynews.com/StreetTalk/Portman-regulatory-fiscal-cliff/2012/08/17/id/448901

14 http://www.social-europe.eu/2012/09/the-euro-debate-in-germany-towards-political-union/

15 http://delphiadvisorsmacropulse.blogspot.com/2012/09/august-2012-employment-report.html

16 http://www.bloomberg.com/news/2012-09-07/jobs-data-show-u-s-factories-bearing-brunt-of-slowdown.html

17 http://www.marketwatch.com/story/us-hiring-weak-in-august-jobless-rate-drops-2012-09-07

18 http://globaleconomicanalysis.blogspot.com/2012/09/household-survey-number-of-employed.html