NAI Hellas Market Report_March 2014_for email

24

RE-DEFINING REAL ESTATE MARKET THE GREEK Commercial Real Estate Market Report 2013

-

Upload

eleni-makri -

Category

Documents

-

view

100 -

download

2

Transcript of NAI Hellas Market Report_March 2014_for email

RE-DEFINING

REAL ESTATE MARKET

THE GREEK

Commercial Real Estate Market Report 2013

E79

THESSALONIKI

ALEXANDROUPOLI

IGOUMENITSA

PATRAS

ΤRIPOLI

LAMIA

ΑTHENS

E79

CRETE

RHODES

ΚAVALA

VOLOS

KORINTHOS

KALAMATA

CHANIAHERACLION

IOANNINA

PREVEZA

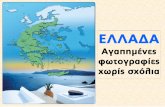

Capital: Athens

Official Language: Greek

Currency: Euro (€)

Population: 10,815,197 (2011 Cencus)

GDP (2012):193.7 bil €

AIRPORTS

PORTS

NATIONAL ROADS

UNDER CONSTRUCTION

EUROPEAN ROAD

03Executive Summary

After five consecutive years of recession, in 2013 there was a steady improvement

in two of the three main macroeconomic indicators for Greece, while the rise in

unemployment showed signs of slowing:

Similarly Real Estate values, having closely followed the financial market since

2008, decreased on average (all sectors) by c. 55%. The close of 2013 showed

stabilization in rental and capital values and a new normal being created.

Towards the end of 2013, the office, retail and hotels & leisure sectors seemed the

most likely candidates for recovery.

In the Athens office market, rents and yields for Grade A offices remained at

2012 levels, ranging from 12€ to 20€/ per month and from 8.25% to 11%

respectively. Kifissias Avenue and Athens City Centre are still the most popular office

locations. Demand for Grade A quality accommodation is increasing as is the supply

of Grade B accommodation.

Likewise, in the retail market, rents and yields for prime locations in Athens2remained steady compared to 2012 (ranging from 60€ to 140€/m /month for

Ermou Street, Kifissia, Glyfada & Kolonaki) and 20€ to 50€ for other retail markets,

with yields ranging between 7.25% to 8% respectively. Established prime retail

locations continue to be favored and enjoy low vacancy rates. Shopping centres

have been comparatively less affected by the credit crunch and on the

whole perform better in terms of rental values and vacancy rates. A notable trend

in the retail market has involved a large number of small retail units converting

into F&B establishments.

In hotels & leisure, the rapid increase in tourist arrivals since 2004, led to an

increase in hotel units by an average of 20% during the last 10 years. Greece is

still a favored tourist destination, showing in H1 of 2013 an increase of tourism

receipts by 15.4%. In 2013, RevPAR is estimated to exceed 30,000€ for 5* hotels and

20,000€ for 4* hotels, while the ADR is estimated to reach 150€ for 5* hotels and 90€

for 4* hotels.

In the logistics sector, a decrease of demand is noted, which resulted in a2decrease of rents and softening of yields (which ranged from 3€ to 4€/m and

10.5%-11.5% respectively) for Grade A logistics in prime locations.

2014 is expected to be a year of correction in capital and rental values. A new

normal is being created in the market and that has already started to show.

Opportunities are on offer for investors who buy now, at discount, and benefit

from the gradual increase of capital and rental values.

2m

GDP

CPI

Unemployment rate

04Greek Real EstateMarket Overview

During the last 15 years, the Greek real estate market went through a full property

cycle. Following closely the financial market, it fell dramatically in the beginning of

2000, only to start rising in 2001 and reached a peak in 2007. The boom period

was a result of historically low interest rates, aggressive bank lending, a rise in

income rates and high public spending on infrastructure due to the Olympic

Games of 2004. High LTV ratios and relaxation of lending terms led to high

construction and development rates. Commercial buildings in Greece increased

in capital value by almost 40% while rents grew over 20%.

After the credit crunch of 2008, Greek real estate experienced a severe downturn

characterized by falling market values. Market uncertainty, rising unemployment,

reduced income and rising taxes were the main reasons that resulted in falling

capital values and low rents; limited demand and minimum project financing also

led to frozen development and construction. Rental values are estimated to have

fallen by more than 30% in all sectors while capital values became increasingly

uncertain. It is estimated that the average decrease of real estate (all sectors)

capital values since 2008 has been c. 55%. Due to the prolonged economic

recession, oversupply of commercial space increased considerably offering

the opportunity for tenants to negotiate better terms.

The Real Estate industry appears to be less volatile than the other markets, where

the logistics industry has higher yields than the office market which has in turn higher

yields than the retail market.

Until 2009 the 10 year Greek Government bond was considered to be a risk free

investment, yet from 2010 the yield to maturity grew significantly, indicating the

economic uncertainty in the country.

The dividend yield of the FTSE/ATHEX Large Cap (top performing companies in the

Athens Stock Exchange) was considerably lower than the All Risks Yield (ARY) of the

property industry, demonstrating the low returns in the stock market.

On the whole, where the government bond's risk tripled and the return from the stock

market fell by 3% in the 5 year period after the crisis, the investment yield in real

estate increased only by 2% in all sectors to reflect risk. Property has historically

proven to be a stable investment.

Greek Investment Markets’ Yields post 2008 credit crunch Comparison

2008 2009 2010 2011 2012 2013

25%

20%

15%

10%

5%

0%

10Y Gov. Bond Yield to maturityARY - Grade A Offices Kifissias Av.ARY - Prime Retail Ermou Str.

FTSE/ATHEX Large CAP Divident YieldARY - Prime Grade A Logistics Aspropyrgos Area

Source: European Central Bank, Hellenic Exchanges Group, NAI Hellas

05Greek Real Estate

Market Overview

After 2008 capital values of real estate, bonds and stocks fell dramatically and

reached a bottom in 2011/2012. Capital values of stocks fell more than all other

markets while capital values of bonds during 2010-2012 fell less than capital

values of grade A offices and prime retail. On the whole real estate capital values

followed a similar trend as the values of stocks and bonds. However, bonds' and

stocks' capital values appear to be growing since 2011, while property capital values

follow with a slower rate. The year 2013 shows that the increase in capital values of

bonds and stocks continues while real estate values stabilize. Capital values in 2013

appear to be at a turning point given also the change in macroeconomic indices.

Taiped I

Taiped II

Pangaia REIC

Fairfax

Praktiker

Dolphino Capital

City Gate

Cosmote Headquarters

Asteras Vouliagmenis

Ermou 19

Q4

Q4

Q4

Q3

Q4

Q3

Q3

Q1

Q4

Q3

Project Name Period Type Vendor Buyer Price

Office Portfolio

Office Portfolio

66% capital share

41.2% capital share

4 DYI Stores

Office Building

Mall

Office Building

Long term Hotel Concession

Retail Shop

Greek State

Greek State

National Bank of Greece

Eurobank Properties REIC

Rockspring

BNP Bank

APN

DIMAND

Greek State & National Bank of Greece

Greek State

Pangaia REIC

Eurobank Properties REIC

Invel

Fairfax Financial Holdings LTD

Eurobank Properties REIC

Dolphino Capital

Marinopoulos Group

Pangaia REIC

Jermyn Street Real Estate Fund IV LP

Pangaia REIC

Major Transactions for 2013

115 mil €

145 mil €

653 mil €

146 mil €

50 mil €

10.3 mil €

6 mil €

120 mil €

493 mil €

5.9 mil €

As the real estate market began to stabilize in 2013, the last quarters of the year

presented a number of noteworthy transactions:

Greek Investment Markets’ Capital Values Comparison (2007=100)

2007 2009 2010 2011 2012 2013

120

100

80

60

40

20

0

OTE Stock PriceOffice Grade A Kifissias Av.Prime Retail Ermou Str.

Prime Grade A Logistics Aspropyrgos Area10 year Gov. Bond

2008

Source: European Central Bank, Hellenic Exchanges Group, NAI Hellas

Source: NAI Hellas

06MacroeconomicOutlook

The year 2013 shows a steady improvement of the main macroeconomic indicators

of Greece. This is reflected in the Economic Sentiment Indicator which continues to

rise from 80.0 units in 2012 to 91.2 units in 2013, the highest in the last five years.

CDP (% change)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014F

8%

6%

4%

2%

0%

-2%

-4%

-6%

-8%

The expected 2013 contraction of the GDP is c. 3.5%, lower than the 2012

expectation (-6.4%). GDP is expected to rise by 0.6% in 2014 and by 2.9% in 2015. In

total the GDP for the period 2007-2013 shrank by c. 27%.

Source: Eurostat, processed by NAI Hellas

Inflation (CPI) in 2011 was 3.1%, in 2012 was 1.00% and is expected to fall by 0.8%

in 2013 and by 0.4% in 2014. The Uniformed CPI in October 2013 reached a record

low of -1.9% (12 month change).

Inflation Rate (% change)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014F

5%

4%

3%

2%

1%

0%

-1%

-2%

Source: Eurostat, processed by NAI Hellas

The unemployment rate reached a high of 27% in 2013 and is expected to remain

at this level in 2014.

Unemployment Rate (% change)

2003 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014F

25%

20%

15%

10%

5%

0%

30%

2004

Source: Hellenic Statistical Authority, processed by NAI Hellas

Net disposable income fell in 2013 by 6.7% since 2011 and is expected to fall by

4.8% in 2013 as an outcome of stringent austerity measures that resulted in a decline

in salaries and social benefits while is estimated to rise by 0.63% in 2014.

Disposable Income (% change)

2003 2004 2005 2006 2007 2008 2010 2011 2012 2013E

10%8%6%4%2%0%

-2%-4%-6%-8%

-10%-12%

2014F2009

Source: Hellenic Statistical Authority, processed by NAI Hellas

07Macroeconomic

Outlook

GDP

CPI

Unemployment

Trade Balance

Disposable Income

2014 Forecast 2015 Forecast

Current Trade Balance showed a surplus of 1.5 bil.€ in 2013 compared to a 2.8 bil.€

deficit in 2012 as a result of improved performance in the food and drinks industry,

tourism and the non-metallic minerals industry.

Trade Balance (bil. €)

5

0

-5

-10

-15

-20

-25

-30

-352003 2004 2005 2006 2007 2008 2010 2011 2012 2013E 2014F2009

Source: Bank of Greece, processed by NAI Hellas

Source: NAI Hellas

The Automobile industry was one of the sectors in Greece that was hit by the

2008 recession. According to the Hellenic Association of Automobile Merchants &

Importers, in 2013 the number of new car licences rose by 0.4% since 2012.

Merchants and Importers are optimistic that the car market will slowly pick up and is

forecasted to further rise by 5% in 2014.

After a deficit in the Budget of 2.8 bil. € in 2012 the Greek Government achieved a

surplus of 0.6 bil.€ for 2013 and the forecast for 2014 is nearly 2.9 bil.€.

4

3

2

1

0

-1

-2

-3

-4 2012 2013E 2014F

Government Budget (bil. €)

Source: Hellenic Republic Ministry of Finance, processed by NAI Hellas

Source: Hellenic Association of Automobile Merchants & Importers, processed by NAI Hellas

New Car Licences350,000

300,000

250,000

200,000

150,000

100,000

50,000

02003 2004 2005 2006 2007 2008 2010 2011 2012 2013E 2014F2009

20%

10%

0%

-10%

-20%

-30%

-40%

-50%

-4.2%

-12.6%

-6.9% -0.8%-4.5% -4.5%

-17.5%

-35.8%-31.0% -40.1%

0.4%5.0%

08 Office Market

The Office Market in Athens since 2008 has witnessed an average fall in capital and

rental values of between 40% and 50% respectively. Occupiers' priority has shifted

to downsizing in space and achieving more affordable rents.

The Athenian Office Market is characterized by a large supply of Grade C or even

D offices and a much lesser offer of Grade A and B accommodation. This specificity

drives vacancy rates of offices to an average range of 3% to 6% for Grade A and from

5% to 10% for Grade B, much lower than the EU average. On the other hand,

vacancy rates for Grade C or D offices range between 20% to 30% while the stock of

ageing buildings continues to rise.

Athens Office Market

Athens Centre (C) Athens West (W) Athens North (N) Athens South (S)

City Centre

Alexandras Av.

Patision Av.

Piraeus Av.

Vas. Sofias Av.

Ampelokipi

National Rd

Petrou Rali

Iera Odos

Thivon Av.

Athinon Av.

Kifissias Av.

Mesogeion Av.

National Rd

Attiki Odos

Sygrou Av.

Faliron

Vouliagmenis Av.

Poseidonos Av.

Piraeus

W C

N

S

Source: NAI Hellas

30

25 €

20 €

15 €

10 €

5 €

0 €

€

2003 2004 2005 2006 2007 2008 2010 2011 2012 20132009

9%

8%

7%

6%

5%

4%

3%

2%

1%

0%

8.50% 8.25%

7.50%7.25%

7.00%6.50%

7.00%

7.50%8.00%

8.25% 8.25%

Rent ( /sq.m./month)€ Yield

Grade A Office Market - Historic Overview

Athens Office Market 2014 Forecast

Grade A

Grade B

Rents Yields Demand Supply

City Centre

West Athens

Kifissias Av.

Sygrou Av.

Vouliagmenis Av.

50%

15%

6%

19%

10%

Office stock Allocation per Area (Grades A & B)

09Office Market

Rental values and yields for Grade A office buildings in Athens in 2013 remained at

2012 levels. Athens City Centre is still expected to achieve higher rents than other

locations followed by Kifissias Av. (North Athens) which is the second preferred

office market in Athens.

On the whole, vacancy rates for Grade B buildings remain higher than Grade A as

demand for good quality accommodation is ongoing.

Athens CBD

Athens West

Kifissias Av.

Mesogeion Av.

National Rd

Sygrou Av.

Faliron

Surroundings

Vouliagmenis Av.

South Athens

8.25%

11.00%

8.25%

8.50%

9.00%

3%

n/a

3%

2%

0%

20.00

12.00 €

15.00 €

14.00 €

12.00 €

€

Grade A

Prime

Rent

Prime

Yield

Vacancy

Rate

9.50%

11.00%

9.50%

9.50%

10.00%

16%

n/a

3%

5%

6%

12.00

7.00 €

10.00 €

10.00 €

9.00 €

€

Grade B

Rent YieldVacancy

Rate

Source: NAI Hellas

Source: NAI Hellas, on-site inspections

10 Retail Market

The growing disposable income up to 2008 led to an increase in retail spending

which consequently pushed retail rental values significantly higher especially in

prime locations such as Ermou, Kifissia and Glyfada. Post 2008, a reduction in

disposable income, credit availability and unemployment reduced consumer

activity. The average reduction in 2013 retail sales has been lower than 35% since

2008. According to the National Confederation of Hellenic Commerce the

percentage of stores that closed down in the city centre of Athens in March 2012 was

29% higher than August 2011 and 27% higher in Piraeus.

Athens

Kifissia

Piraeus

Glyfada

Pagrati

ChalandriPeristeri

Aegaleo

Ermou Str.

Stadiou Str.

Patission Str.

Source: NAI Hellas

2003 2004 2005 2006 2007 2008 2010 2011 2012 20132009

8%

7%

6%

5%

4%

3%

2%

1%

0%

Rent ( /sq.m./month)€ Yield

Grade A Office Market - Historic Overview

300 €

250 €

200 €

150 €

100 €

50 €

- €

350 €

6.50% 6.50% 6.50%6.00%

5.00% 5.00%

5.75%6.25%

6.75%7.25% 7.25%

11Retail Market

High Street Retail Space (sq.m.)

6

50,000

40,000

30,000

20,000

10,000

0

0,000

Glyfada Kifissia Ermou Stadiou Patission Pagrati Aegaleo Piraeus Peristeri Kolonaki Chalandri

25%

20%

15%

10%

5%

0%

16%

9%

3%

17%

19%

22%

14%

9%10%

20%

6%

Retail space sq.m. Vacant space sq.m. Vacancy rate

Source: NAI Hellas on-site inspections

Retail rents in 2013 remained stable at 2012 levels while yields in prime locations

reached 7.50%. Throughout the years of the recession, established prime retail

locations continued to be favored and have enjoyed comparatively lower vacancy

rates whereas secondary locations have suffered high vacancy rates and falling

rental values.

New conditions in the market created an opportunity for big retailers to

consolidate their market positions, reduce occupational costs through negotiation

and continue their expansion program. The Food and Beverage sector has grown

significantly as the new trend in the retail market is to convert small retail units

into bars, cafes, and restaurants.

Athens High Street Retail Market 2013 Outlook

Rents Yields

Prime PrimeSecondary Secondary

Glyfada

Kifissia

Ermou

Stadiou

Patission

Pagrati

Aegaleo

Piraeus

Peristeri

Kolonaki

Chalandri

60 -80

70€-100€

90€-140€

80€-100€

20€-30€

25€-50€

30€-40€

25€-35€

30€-50€

60€-110€

30€-75€

€ € 30€-50€

30€-50€

45€-70€

50€

8€-15€

8€-15€

15€-20€

10€-15€

10€-15€

25€-50€

15€-25€

7.25% - 8.00% 8.00% - 9.00%

Source: NAI Hellas

12 Retail Market

Athens High Street Retail Market 2014 Forecast

Prime

Secondary

Rents Yields Demand Supply

Occupancy by Sector

Kifissia Ermou

Stadiou Patission

Pagrati Aegaleo Piraeus

Peristeri Kolonaki Chalandri

Glyfada

Food & Beverage

Clothing & Footwear

Household Goods

Books/Electronics/Toys/Mobile

Supermarket/Grocery/Butcher

Cosmetics

Cars/Moto/Heavy Equip.

Services

Vacant

Other

Source: NAI Hellas on-site inspections

13Shopping Centres

Shopping Centres in Greece appeared after 1990 and are typically multi-storey

buildings of 3 retail floors where normally one or more large anchor tenants generate

footfall. In Athens, Shopping Centres (Malls) followed the same trend whereas

bigger outlets commonly known as Retail Boxes or Retail Parks consist of a single

large floor space and are found in outer Athens. Shopping Centres compared to

High Street retail were less affected by the credit crunch and on the whole performed

better than high street retail, with lower vacancy rates, higher footfall and more stable

rates. The average leasable space per 1,000 inhabitants (for the greater Athens area) 2remains less than 100m /1,000 persons compared to the EU-27 average of

2246m /1,000 persons.

Shopping Centers - Key Figures

Maintenance (pa)

Property Management (% of GPI pa)

Allowance of risk of rental loss

Useful Life

No. of parking spaces requirred

No. of storeys

Fitout Specification

Building Costs (excl. site improvements)

Ancillary building costs

24 - 6 € / m

2 - 4%

> 5%

50 years

2guide: 1 space for 15-20 m of sales area

multi-storey, 2 - 3 retail floors

average to high

21,000 - 1,500 € / m GEA

7 - 15% of building costs

Source: International Council of Shopping Centers (ICSC), processed by NAI Hellas

Name Location

Athens Heart

Avenue

Golden Hall

Metro Mall

River West

The Mall Athens

Village Shopping & More

McArthurGlen Designer Outlet

Malls

Tavros

Kifissias Av., Maroussi

Kifissias Av., Maroussi

Agios Dimitrios

Kifissos Av., Tavros

Maroussi

Thivon Av., Rentis

Spata

Total sqm of retail space 2272,500 m approx.

Name Location

Airport Retail Rark

Jumbo

Media Markt

Leroy Merlin

Smart Park

IKEA

Boxes

Attica Rd

Pireos Str.

Spata

Kifissos Av.

Tavros

Total sqm of retail space 2175,000 m approx.

Source: NAI Hellas

2Mall - Anchor Tenant (2,000m +)

2Mall > 100 m

2Mall < 100 m

2Box (min. 5,000 m )

Athens Shopping Centres

Rents Yields

11 -15

35€-60€

50€-90€

8€-16€

€ €

7 -13

2%-7%

% %

Turnover Rent

8.25 -9.00

8.50%-9.50%

% %

Source: NAI Hellas

Athens Shopping Centres Market 2014 Forecast

Malls

Boxes

Rents Yields Demand Supply

Athens Malls’ Vacancy Rate

Occupancy Rate

Vacancy Rate

Athens Boxes’ Vacancy Rate

Source: NAI Hellas

14 Logistics

Athens Logistics Market 2014 Forecast

Prime

Secondary

Rents Yields Demand Supply

2 2Rents in 2013 varied from 3€/m /month to 4 /m /month for the best quality

buildings, while yields ranged from 10.50% to 11.50% depending on the location.

It is estimated that for 2014 rents and yields for prime logistics will remain

constant as the market appears to be stabilizing. Supply of logistics space is not

expected to increase as no new development plans are on the way, while existing

stock is ageing. Demand for prime logistics is expected to increase due to the

new development of the freight center in Thriassio (Athens West).

€

Investment and development interest for logistics from international players

remained low in 2013, with very few transactions to report and low business activity.

The market remains owner occupied and demand for logistics during 2013

decreased. Supply of newly constructed logistics buildings was very limited in 2012

and 2013, as developers only look to pre-let or pre-sell before commencing any new

development. Falling demand created an opportunity for occupiers to bargain rents

on Grade A logistics buildings in prime locations.

2003 2004 2005 2006 2007 2008 2010 2011 2012 20132009

Rent ( /sq.m./month)€ Yield

Prime Logistics Market - Historic Overview

6 €

5 €

4 €

3 €

2 €

1 €

0 €

7 € 12%

10%

8%

6%

4%

2%

0%

8.50% 7.00% 8.00%

9.00% 9.00%9.50%

10.50%10.75%

9.50% 9.50%9.00%

Source: NAI Hellas

Athens North (1)

Metamorfosi

Kifissia

Krioneri

Agios Stefanos

Attica Logistics Market

Athens East (2)

Koropi

Spata

Airport (El. Venizelos)

Peania

Athens West (3)

Aspropyrgos

Magoula

Elefsina

Inofita & Schimatari (4)

Koropi

Spata

Airport(El. Venizelos)

Peania

Elefsina

MagoulaAspropyrgos Metamorfosi

Kifissia 1 3

Inofita

Schimatari

4

Ag. StefanosKrioneri

2

15Infrastructure

Road Network

Ports

New Projects

The continuous upgrade of the E79 international road network will link Athenswith the rest of Central Europe. The construction of IONIA ODOS highway will connect the whole of Western Greece linking also three ports (Patra, Astakos, Igoumenitsa) and three airports (Araxos, Preveza, Ioannina). It will run from Antirrio and end on Egnatia Odos highway, which connects the whole of North Greece and E79. It also connects the industrial centres of Western Europe with Eastern Europe and acts as the main road axis for transportation in the Balkans and SE Europe.

Due to Greece's extensive coastline, there are several commercial ports locatedstrategically in the country; in Attika (Piraeus, Rafina, Lavrio), Crete (Heraklion,Chania), Western Greece (Kalamata, Patra, Korinthos, Astakos, Igoumenitsa) andNorthern Greece (Volos, Thessaloniki, Kavala, Alexandroupoli).

Cosco Pacific Ltd which is already exploiting Pier II of the Piraeus container terminal has announced an additional 230 mil € investment in the port of Piraeus until 2015 including:- the construction and exploitation of Pier III- the upgrade with new machinery of Pier II and East Pier III plus installation of Super- post Paramax cranes- the construction of a Petroleum Pier

The capacity of Piers II & III will increase from 3.7 mil TEU to 6.2 mil TEU.Piraeus is becoming a bigger trade gateway and the Southern Europe entry pointserving the Balkans and the Black Sea.

RailwaysThe new freight centre (Athens West) of TRAINOSE (subsidiary of the Hellenic Railways Organization) in Thriassio is expected to complete by the end of 2015. The 257 mil € investment includes sorting stations, container management stations, terminals, customs office and warehouses. TRAINOSE and the Piraeus Port Authority have reached an agreement for the construction of two railway stations in the port of Piraeus; one for container transportation and one for car transportation. The 17 kilometer railway route will link Piraeus Port with the Thriassio freight centre and the national railway network where 1.7 mil TEU per annum are estimated to be transported to SE Europe via the national railway network.

Cosco and Hewlett-Packard along with other SE Asian companies have reachedan agreement for a logistics centre in the modern freight centre in Triassio. To ease the process of the previous mentioned plans, the Greek Government is preparing to sell 49% of the publicly owned TRAINOSE in order to privatize the company.

The strategic location of the new freight centre in Thriassio in terms of roadnetwork, rail linkage and access to Greece's biggest port has raised an international investment appetite for the area.

Piraeus Container Terminal (in TEUs)

2002 2003 2004

Total

% change

2005 2006 2007 2009 2011 201220102008

1,404,939

n/a

1,605,135

14.2%

1,541,563

-4%

1,394,512

-9.5%

1,403,408

0.6%

1,373,138

-2.2%

433,582

-68.4%

664,895

53.3%

513,319

-22.8%

490,904

-4.4%

625,914

27.5%

Source: Piraeus Port Authority SA, edited by NAI Hellas

16 Hotels & Leisure

In 2012 Greek Tourism contributed to GDP

by 16.4% and to employment by 18.3%. The

Association of Greek Tourism Enterprises

reported that income from tourism in the year

reached 10.4 bil € coming from 16.9 mil

visitors. Greece holds a market share in

Europe of 2.9% and 1.5% globally, offering

9,670 hotels spread around the country.

Traditionally 80% of visitors to Greece are for

holiday; on the contrary only 6.8% travel to

Greece on business.

The number of tourists arriving in Greece

has been growing rapidly since the 2004

Olympic Games of Athens and it is estimated

that c.5% more tourists visited Greece in

2013 compared to 2012.

International Tourist Arrivals 2000-2012

Year Arrivals

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013E

2014F

12,378,282

13,019,202

12,556,494

12,468,411

11,735,556

14,388,182

15,226,241

16,165,265

15,938,806

14,914,537

15,007,493

16,427,247

16,946,543

17,500,000

18,500,000

% change

n/a

5.2%

-3.6%

-0.7%

-5.9%

22.6%

5.8%

6.2%

-1.4%

-6.4%

0.6%

9.5%

3.2%

3.3%

5.7%

Tourism Receipts according to travel purpose in 2011

Holiday

Academic

Visiting Family

Business Reasons

Other Reasons

The continuing increase in the

number of foreign visitors to Greece

created a need for more hotel

accommodation. Therefore, the

number of hotel units in Greece has

been growing since 2004; it is worth

noting that between 2000-2012 the

number of hotel units in Greece

increased by almost 20%.

All Type Hotel Evolution (Δ% change 2000-2012)

30%

25%

20%

15%

10%

5%

0%

No. of Hotels No. of Rooms No. of Beds

Source: Hellenic Statistical Authority, processed by NAI Hellas

Source: The Association of Greek Tourism Enterprises, processed by NAI Hellas

Source: Hellenic Chamber of Hotels, processed by NAI Hellas

Evolution in Hotel Numbers by Category 2000-2012

5,000

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

02003 2004 2005 2006 2007 2008 2010 2011 20122009

5* No. Hotels 1* No. Hotels2* No. Hotels4* No. Hotels 3* No. Hotels

Source: Hellenic Chamber of Hotels, processed by NAI Hellas

17Hotels & Leisure

Since the crisis started in 2008, while arrivals increased steadily to 18 mil. a year,

tourism receipts published have remained stable at around 10 mil. €, suggesting

people are spending less and stay less time.

The 2008 recession had an effect on tourism, as shown in the graphs below.

The years 2009 and 2010 were the most

difficult for the Tourism Industry in Greece.

However the market appears to be

recovering and Tourism Receipts increased

in 2012 by 3.2% compared to 2011

according to the World Tourism Organization

(UNTWO), which further continued in 2013.

Travel balance for the period Jan-May 2013

presented a surplus of 306 mil. € compared

to the same period in 2012 according to the

Bank of Greece which mainly comes from an

increase in tourism receipts of 15.4% in H1 of

2013.

The average occupancy of hotels in Greece before the recession ranged from

45% to 50%. After 2009 occupancy fell as low as 34% in 2012. In 2013 however,

occupancy reached almost 40% and is expected to increase further in 2014.

Occupancy Rates of Greek Hotels

60%

50%

40%

30%

20%

10%

0%

Greek Tourism Receipts 2000-2012 (bil.€)

14

12

10

8

6

4

2

02005 2006 2007 2008 2010 2011 201220092000 2001 2002 2003 2004

Source: The Association of Greek Tourism Enterprises, processed by NAI Hellas

Non-Residents’ Overnight Stay in Greece - All Type Hotels (mil.)

160

155

150

145

140

135

130

125

165

2005 2006 2007 2008 2010 2011 20122009

Source: The Association of Greek Tourism Enterprises, processed by NAI Hellas

Greek Tourism Ranking

based on

International Tourism Receipts

2007-2012

2012

2011

2010

2009

2008

2007

23

19

21

15

12

12

Year

Country

Ranking

World

Country

Ranking

Europe

11

9

10

8

8

8

Source: World Tourism Organization, processed by NAI Hellas

Source: Hellenic Chamber of Hotels, processed by NAI Hellas

18 Hotels & Leisure

The annual Revenue per Available Room (RevPAR) in a 5* Hotel is estimated to

exceed 30,000 from 2013 onwards and over 20,000 for a 4* Hotel room. € €

Change in RevPAR of Greek Hotels

2008 2009 2010 2011 2013E 2014F2012

35,000

25,000 €

20,000 €

15,000 €

10,000 €

5,000 €

0 €

€

30,000 €

RevPAR 5* Hotels RevPAR 4* Hotels

Source: NAI Hellas

2008 2009 2010 2011 2013E 2014F2012

1

160 €

140 €

120 €

100 €

80 €

60 €

40 €

20 €

0 €

80 €

RevPAR 5* Hotels RevPAR 4* Hotels

ADR of Greek Hotels

Moreover, the Average Daily Rate (ADR) of a 5* Hotel room in 2013 is estimated to

reach 150€ while for a 4* Hotel room the rate is estimated to exceed 90€.

Source: NAI Hellas

Lastly, the implied EBITDA multiplier for a 5* Hotel is estimated to increase to 10.5 in

2013 compared to 9 in the years 2010, 2011 and 2012. Likewise, the implied EBITDA

multiplier for a 4* Hotel is estimated to reach 10 in 2013 compared to 8 in the years

2010, 2011 and 2012.

2008 2009 2010 2011 2013E 2014F2012

1

11.0

10.5

10.0

9.5

9.0

8.5

8.0

7.5

7.0

1.5

5* Hotels 4* Hotels

EBITDA multiplier in Greek Hotels

Source: NAI Hellas

19Opportunities in the

Greek R.E. Market

Refurbishment&

Re-Development

Grade A Office@ discount

Prime Logistics@ discount

Prime Retail@ discount

InvestmentOpportunities

Hotels&

Leisure

2014 is the year of stabilizationin capital and rental values.

INVESTMENTRECOVERY GROWTH

Growth will emerge as a resultof the new base of valuesestablished.

The investment opportunity liesin buying property at current lowprices and benefiting from therise in capital and rental valuesto come with recovery.

Deloitte Athens Headquarters

21

The past years the legislative framework of the taxation of real estate ownership in Greece has significantly

changed. As from 1.1.2014 onwards new types of taxes are applicable both for the acquisition of real property

and its ownership. Investing in real estate in Greece requires careful design and planning from the very

beginning. Different rules apply for individual and corporate investors, while the scope of the investment (whether

short term or long term) merit different approach in the design phase. The following paragraphs aim to outline the

main tax aspects of real property acquisition and ownership in Greece and to provide the potential investors with

an overview of the key points of the applicable legislation.

The taxation of real estate in Greece

Upon acquisition of real property located in Greece, the potential investor will be

liable for the payment of either Real Estate Transfer Tax at 3% (for land and “old”

buildings on the higher of the tax value of the property or the value depicted in the

notarial deed) or Value Added Tax at 23% (for the supply of “new” buildings). If the

investor is an individual Greek tax resident, he should also consider the imputed

income provisions that require the taxpayer to be able to prove that he has the

funds available to acquire the property in question.

Acquisition of the real property

A Greek tax resident individual owner selling real property is subject to a 15% tax on the capital gain derived from

the sale. Certain exceptions apply for low capital gains or for real estate held for a long period of time. The same

tax applies if the object of the sale is a company, whose value significantly comprises from real estate (>50%).

For corporate owners, the gain from the sale of real property is deemed as business income and is subject to the

prevailing 26% Corporate Income Tax rate. The change of ownership due to a donation or inheritance is subject to

the special donation or inheritance tax imposed under Greek law.

Disposal of real property

For further information please contact:

Thomas Leventis, Tax Partner [direct: +30 210 6781262 / [email protected]]

Kostas Roumpis, Tax Manager [direct: +30 210 6781272 / [email protected]]

Taxes on the ownership of real property may be divided in two

main categories:

-Taxation of rental income

-Capital ownership taxes

For individuals, the annual rental income up to €12,000 is taxed

at 11% and any income above €12,000 at 33%. For corporate

investors, the rental income is deemed as business income,

taxed at the prevailing 26% rate. It is also noted that commercial

leases are either subject to 23% VAT (if such an election is made

and allowed) or to 3.6% stamp tax. Residential leases are exempt

from both VAT and stamp tax. The Capital ownership tax is

comprised by the Main Tax and the Supplementary Tax. The Main

Tax is computed on a per property basis, whereas the

Supplementary Tax is computed on the total tax value of the

property held. The Main Tax is computed taking into account a

variety of factors (such as the address of the property, its use, the floor and the total surface) and the

Supplementary Tax for individuals range from 0.1% for total property value of €300,000 to 1% for total property

value exceeding €1MN. For corporate owners, the tax is 0.5% on the total value of the property which is not

self-used by the owner. Finally, it is underlined that for individual Greek tax resident owners, imputed income is

also computed for the real property self-used. In addition, there is a special property tax (the so called “off-shore”

tax) which applies to corporate owners. Several exemptions apply, the most usual being based on disclosure of

the ultimate individual owner.

Ownership of real property

Transfer of real estate

Investor

ValueAdded Tax

Real EstateTransfer Tax

Real Property exploitation

Income taxon rentalincome

Stamp taxor VAT for

commercialleases

Annual RealProperty Tax

22

EU Schengen States

Non - EU Schengen States

Schengen candidate States

Non - EU Schengen States

Acquisition of Residence Permits through Real Estate OwnershipThe application of articles 16 (B) and 20 (B) of the Greek Immigration and Social Integration Code

Guide to Residence Permits for Real Estate investors in Greece[Article 20 of the Greek Immigration and Social Integration Code (“Immigration Code”)]

The Greek State introduced a procedure for granting five year renewable residence permits to citizensof non EU member States who invest in real estate in Greece, the value of which is at least 250,000€.

Third country citizens that either personally or througha legal entity:- Own Real Estate property of 250,000€ value;- Have a time-sharing contract of 250,000€ minimum value;- Have a 10 year at minimum lease of hotel accomodationor furnished tourist accomodations (houses) in touristaccomodation complexes of 250,000€ minimum value;

Can obtain a five year renewable residence permit forthem as well as their spouse and children.

minimum

Residence permit allows access to the 26 Schengenmember states for 3 months every 6 months.

Schengen Area as of 1/7/2013

For further information please contact:

Spyros Alexandris, Partner [direct: +30 210 3318170 / [email protected]]

Residence permit is valid for 5 years but can be renewedfor the same duration as long as the real estate propertyremains in the ownership of the applicant or the saidleases are active.

As per article 16 (B) of the Immigration Code, a strategicinvestor, (who invests from 3 mil.€ to 100 mil.€ dependingon the type of investment) can be granted up to 10residence permits for individuals key to the investmentwho may be escorted by their family members.Such residence permits shall have a 10 year renewableduration.

Thomas ZiogasBusiness Development [email protected]

Eleni [email protected]

George [email protected]

NAI Hellas/AVENT S.A. is a full service commercial real estate brokerage andconsultancy firm, member of NAI Global the world's largest network ofindependent commercial real estate service providers.

Our Services

Contacts

Disclaimer

All data contained in this report has been compiled by NAI Hellas/AVENT S.A.

and is published for general information purposes only. While every effort has

been made to ensure the accuracy of the data and other material contained in

this report, NAI Hellas/AVENT S.A. does not accept any liability (whether in

contract, tort or otherwise) to any person for any loss or damage suffered as a

result of any errors or omissions. The information, opinions and forecasts set out

in the report should not be relied upon to replace professional advice on specific

matters, and no responsibility for loss occasioned to any person acting, or

refraining from acting, as a result of any material in this publication can be

accepted by NAI Hellas/AVENT S.A.

© NAI Hellas/AVENT S.A. March 2014

Sale & purchase

Rentals

Investment sales & advisory

Valuation of fixed assets

Landlord & Tenant Representation

Development Appraisals

Feasibility Studies

Planning and land use advice

Market research

Expert witness

Corporate Real Estate Services

Public Private Partnerships (PPP)/Private Finance Initiative (PFI)

Due Diligence

Asset Management

Value Preservation & Enhancement

Property Finance

Hotel & Leisure

4, Nikitara & Psaron str.152 32 ChalandriAthens, Greecetel +30 210 6811760fax +30 210 6811722

www.naiglobal.com