Introduction 1Client Confidential 6 σ (3.4 defects per million) ‘The Dabbawallah’ (Lunch...

50

Introduction 1 Client Confidential 6σ (3.4 defects per million) ‘The Dabbawallah’ (Lunch Logistics)

-

Upload

carmella-roberts -

Category

Documents

-

view

226 -

download

5

Transcript of Introduction 1Client Confidential 6 σ (3.4 defects per million) ‘The Dabbawallah’ (Lunch...

Introduction

1Client Confidential

6σ(3.4 defects per million)

‘The Dabbawallah’

(Lunch Logistics)

Poll

Have you been to India yet?

2Client Confidential

Content

• Financials – Basics

• Logistics – Infrastructure

• Regulatory – Authorities

• Customs – Compliance

3Client Confidential

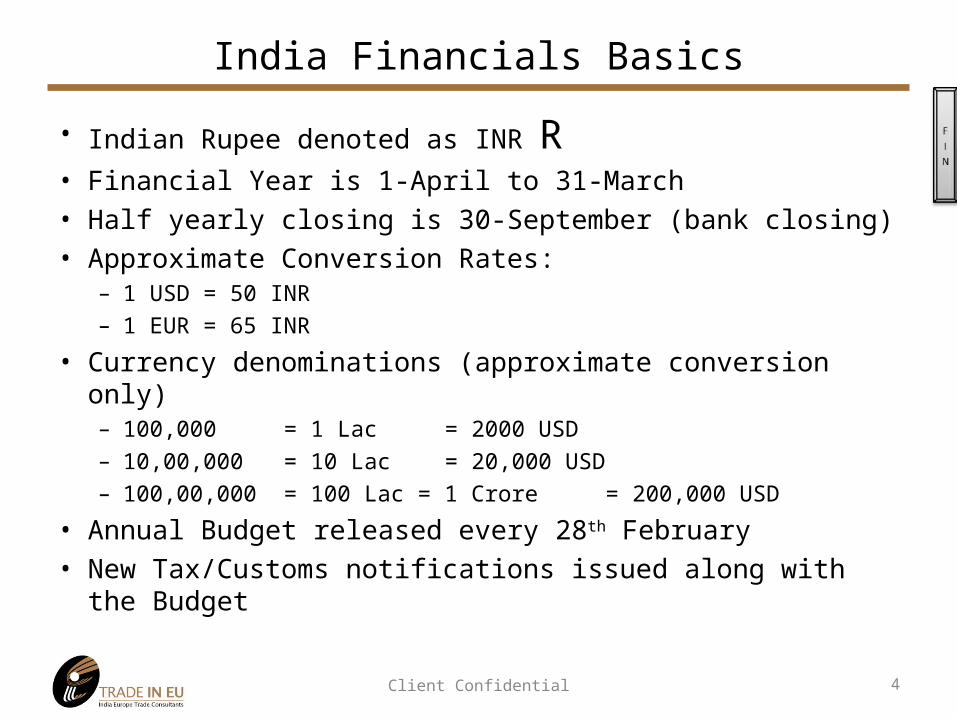

India Financials Basics

Client Confidential

• Indian Rupee denoted as INR R• Financial Year is 1-April to 31-March• Half yearly closing is 30-September (bank closing)• Approximate Conversion Rates:

– 1 USD = 50 INR– 1 EUR = 65 INR

• Currency denominations (approximate conversion only)– 100,000 = 1 Lac = 2000 USD– 10,00,000 = 10 Lac = 20,000 USD– 100,00,000 = 100 Lac = 1 Crore = 200,000 USD

• Annual Budget released every 28th February• New Tax/Customs notifications issued along with the Budget

4

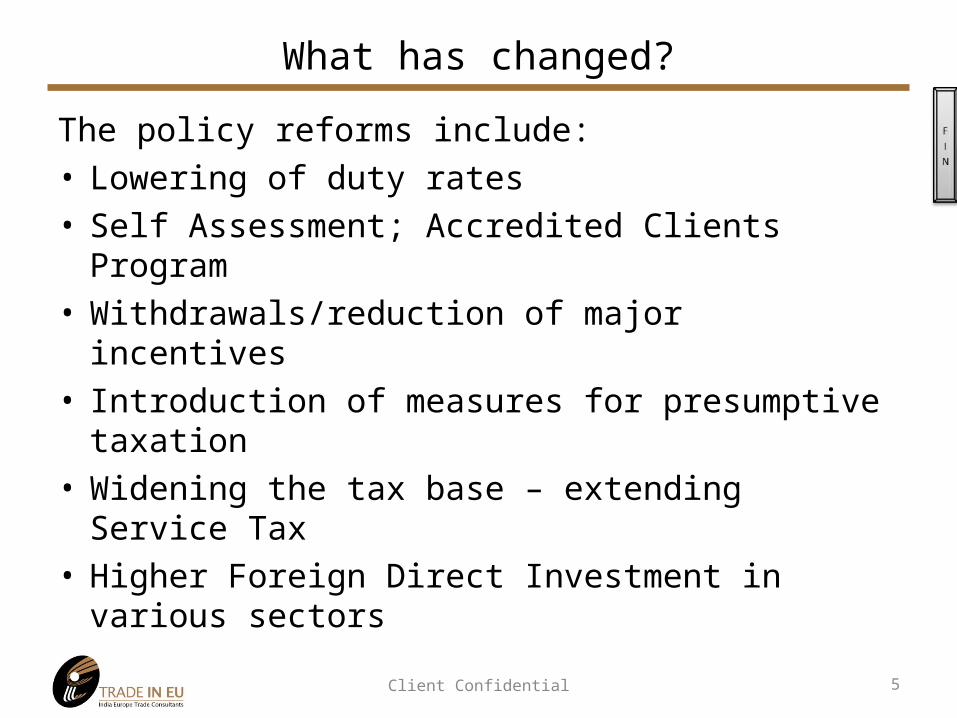

What has changed?

The policy reforms include:• Lowering of duty rates• Self Assessment; Accredited Clients Program• Withdrawals/reduction of major incentives• Introduction of measures for presumptive taxation• Widening the tax base – extending Service Tax• Higher Foreign Direct Investment in various sectors

5Client Confidential

Poll

Does your company or a group company, have Indian operations (Joint Venture or

Wholly Owned Subsidiary)?

6Client Confidential

LOGISTICS – INFRASTRUCTURE

7Client Confidential

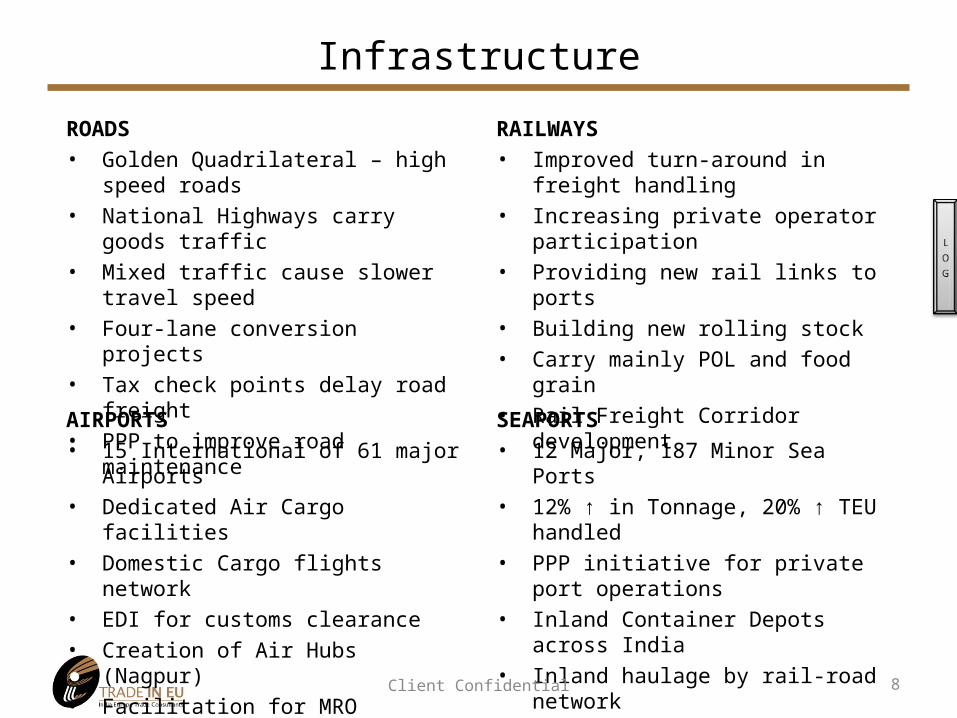

Infrastructure

8

ROADS• Golden Quadrilateral – high speed roads• National Highways carry goods traffic• Mixed traffic cause slower travel speed• Four-lane conversion projects• Tax check points delay road freight• PPP to improve road maintenance

RAILWAYS• Improved turn-around in freight handling• Increasing private operator participation• Providing new rail links to ports• Building new rolling stock• Carry mainly POL and food grain• Rail Freight Corridor development

AIRPORTS• 15 International of 61 major Airports• Dedicated Air Cargo facilities• Domestic Cargo flights network• EDI for customs clearance• Creation of Air Hubs (Nagpur)• Facilitation for MRO logistics

SEAPORTS• 12 Major, 187 Minor Sea Ports• 12% ↑ in Tonnage, 20% ↑ TEU handled• PPP initiative for private port operations• Inland Container Depots across India• Inland haulage by rail-road network• Private Logistics parks at/near new ports

Client Confidential

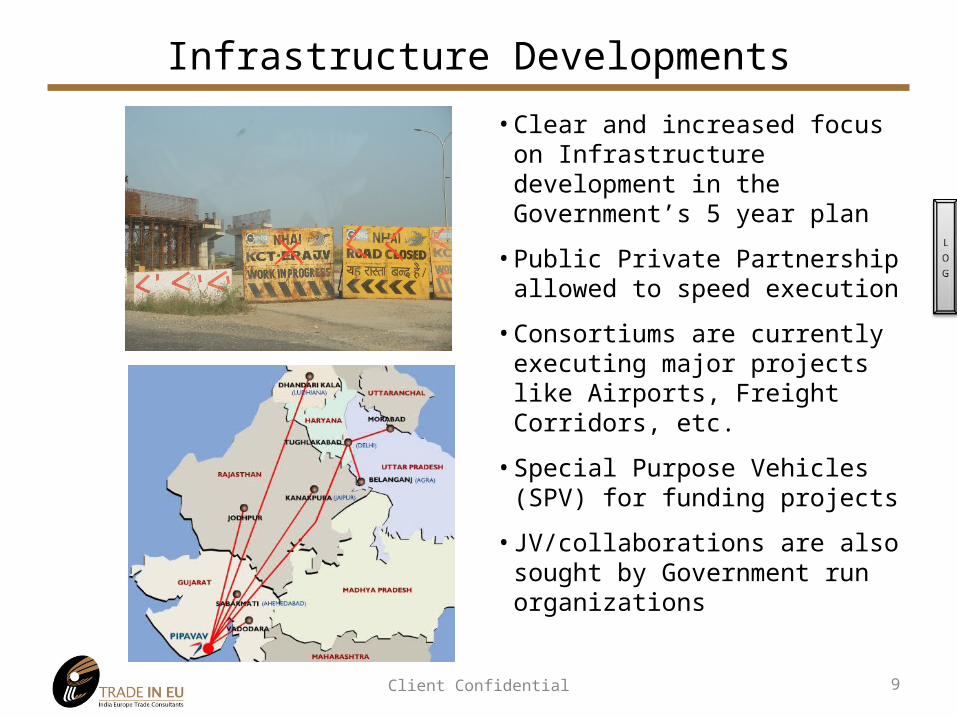

Infrastructure Developments

• Clear and increased focus on Infrastructure development in the Government’s 5 year plan

• Public Private Partnership allowed to speed execution

• Consortiums are currently executing major projects like Airports, Freight Corridors, etc.

• Special Purpose Vehicles (SPV) for funding projects

• JV/collaborations are also sought by Government run organizations

9Client Confidential

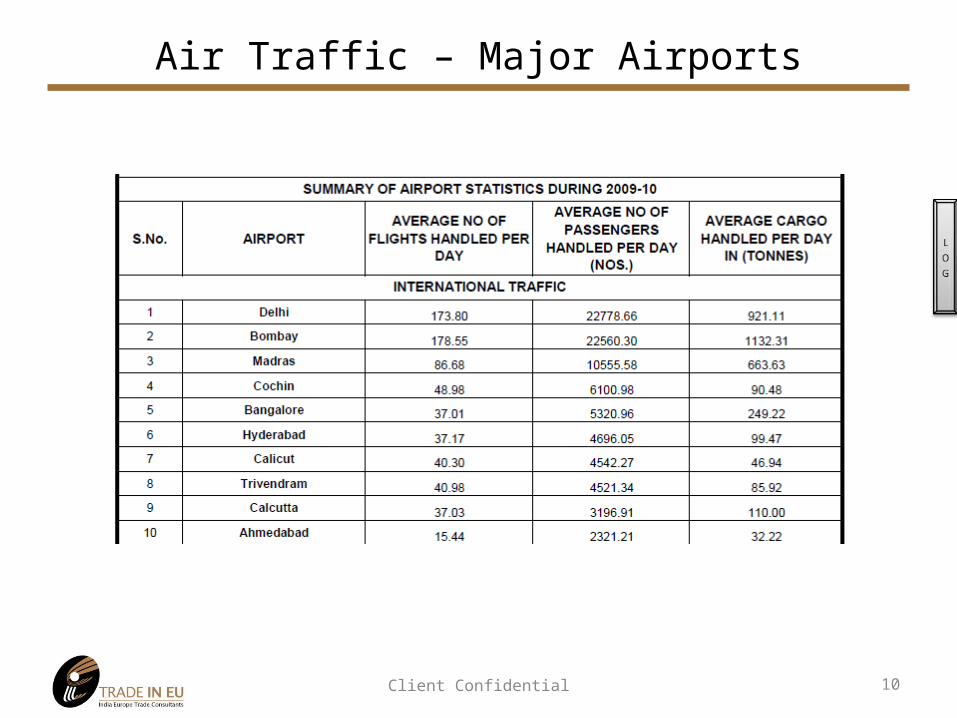

Air Traffic – Major Airports

10Client Confidential

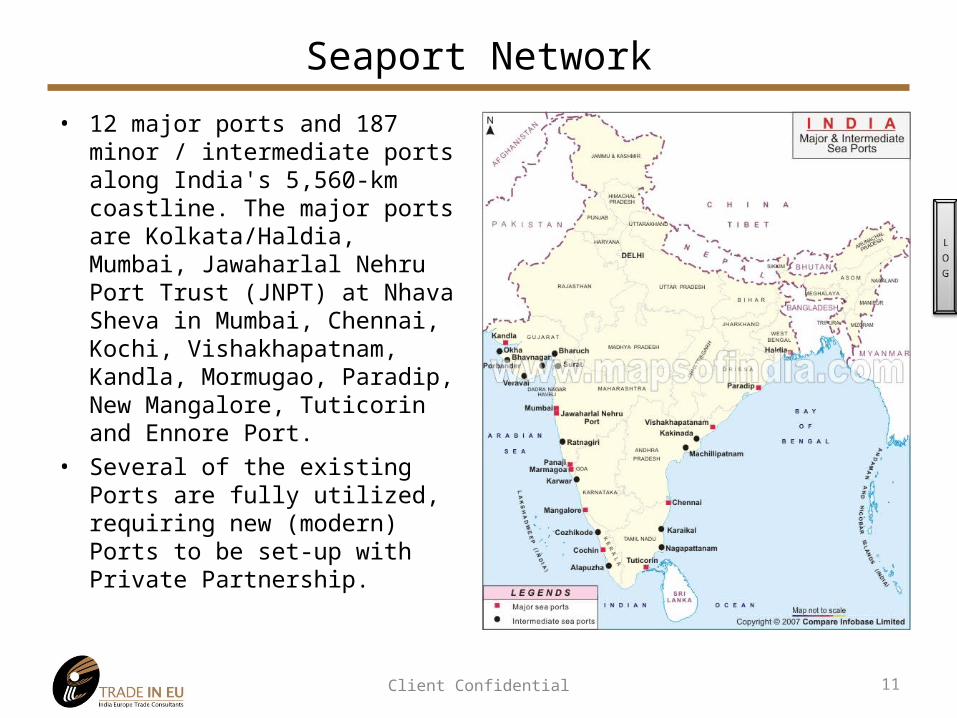

Seaport Network

• 12 major ports and 187 minor / intermediate ports along India's 5,560-km coastline. The major ports are Kolkata/Haldia, Mumbai, Jawaharlal Nehru Port Trust (JNPT) at Nhava Sheva in Mumbai, Chennai, Kochi, Vishakhapatnam, Kandla, Mormugao, Paradip, New Mangalore, Tuticorin and Ennore Port.

• Several of the existing Ports are fully utilized, requiring new (modern) Ports to be set-up with Private Partnership.

11Client Confidential

Poll

Do your shipments to India suffer delays?

12Client Confidential

Logistical Challenges

13Client Confidential

Warehousing & Distribution

• Select Partners with right capabilities for warehousing & distribution

14Client Confidential

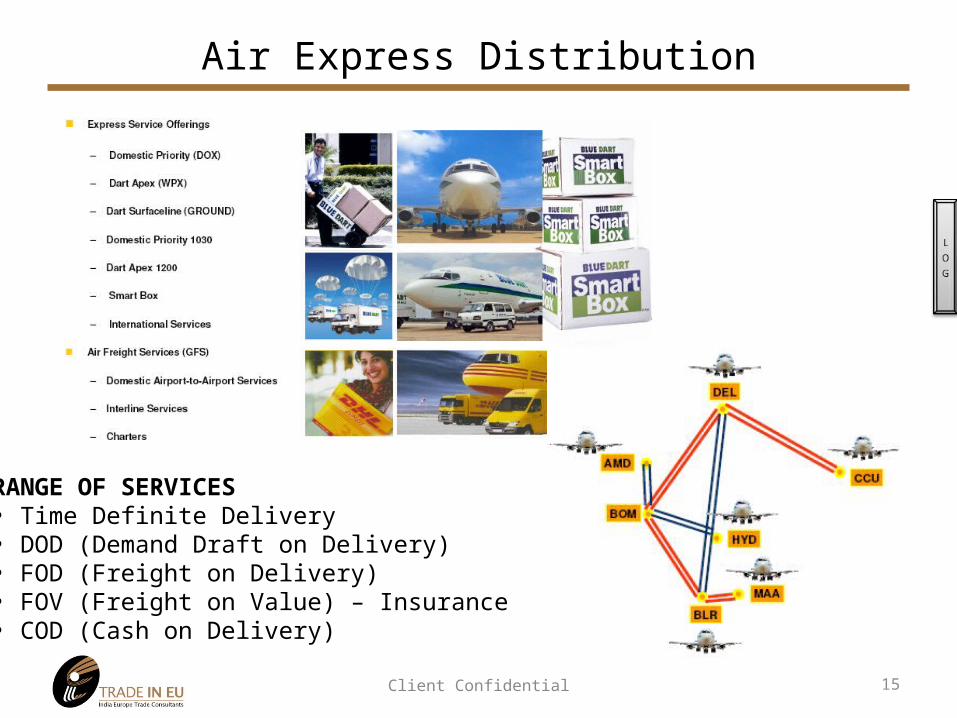

Air Express Distribution

15

RANGE OF SERVICES• Time Definite Delivery• DOD (Demand Draft on Delivery)• FOD (Freight on Delivery)• FOV (Freight on Value) – Insurance• COD (Cash on Delivery)

Client Confidential

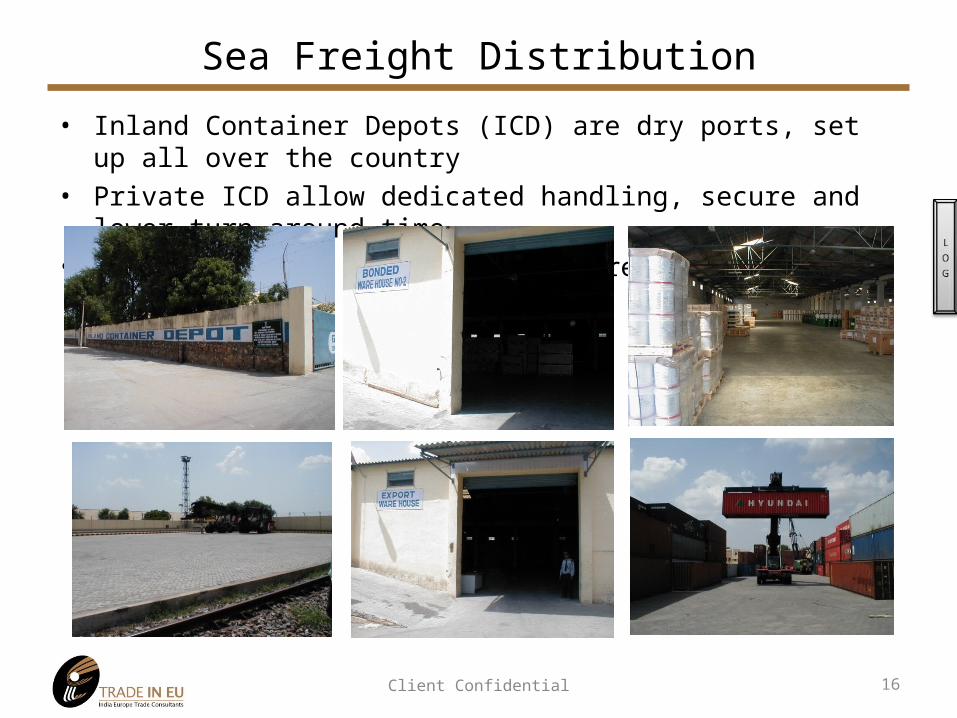

Sea Freight Distribution

16

• Inland Container Depots (ICD) are dry ports, set up all over the country• Private ICD allow dedicated handling, secure and lower turn-around time• Shipments moved swiftly and cleared at final destination

Client Confidential

Poll

Does your logistics service provider have an India Operation?

17Client Confidential

Regulatory – Authorities

18Client Confidential

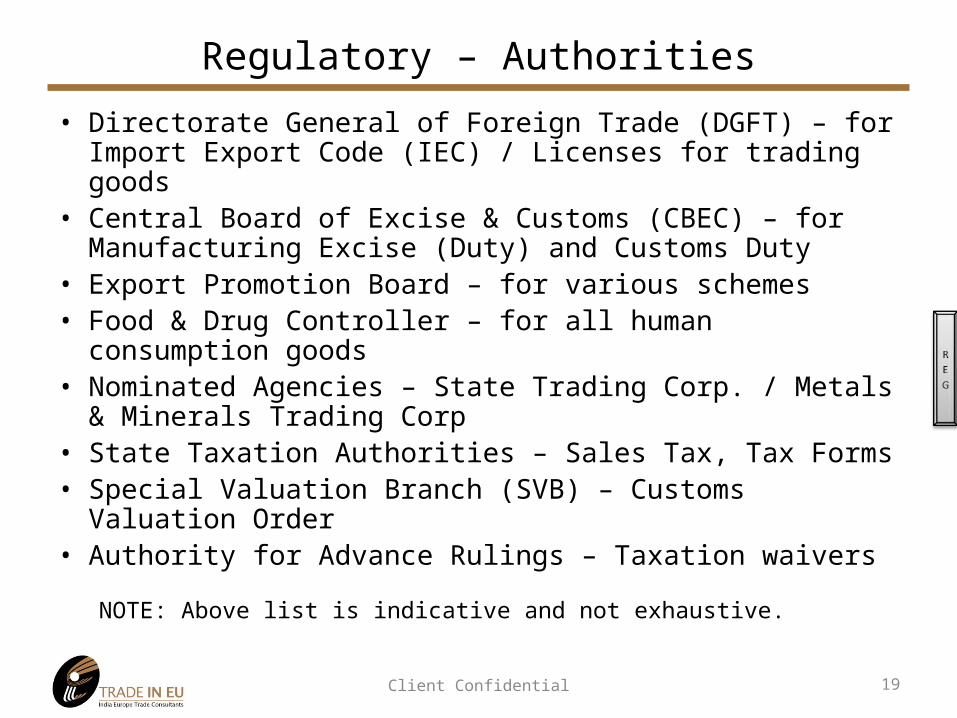

Regulatory – Authorities

• Directorate General of Foreign Trade (DGFT) – for Import Export Code (IEC) / Licenses for trading goods

• Central Board of Excise & Customs (CBEC) – for Manufacturing Excise (Duty) and Customs Duty

• Export Promotion Board – for various schemes• Food & Drug Controller – for all human consumption goods• Nominated Agencies – State Trading Corp. / Metals &

Minerals Trading Corp• State Taxation Authorities – Sales Tax, Tax Forms• Special Valuation Branch (SVB) – Customs Valuation Order• Authority for Advance Rulings – Taxation waivers

NOTE: Above list is indicative and not exhaustive.

19Client Confidential

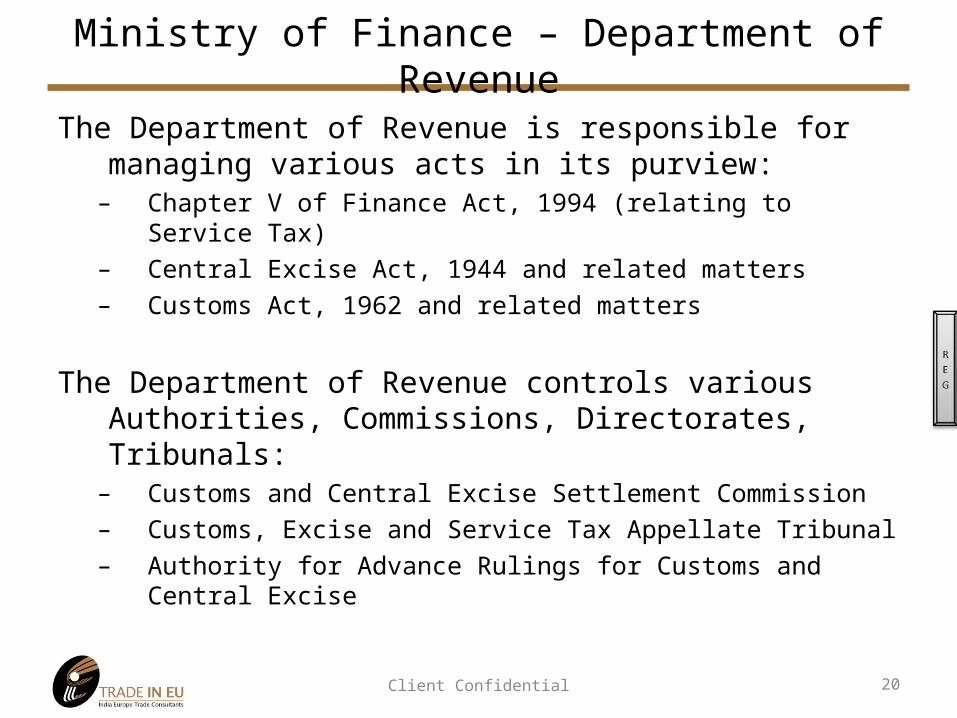

Ministry of Finance – Department of Revenue

The Department of Revenue is responsible for managing various acts in its purview:

– Chapter V of Finance Act, 1994 (relating to Service Tax)– Central Excise Act, 1944 and related matters– Customs Act, 1962 and related matters

The Department of Revenue controls various Authorities, Commissions, Directorates, Tribunals:

– Customs and Central Excise Settlement Commission– Customs, Excise and Service Tax Appellate Tribunal– Authority for Advance Rulings for Customs and Central Excise

20Client Confidential

Import Export Regulations

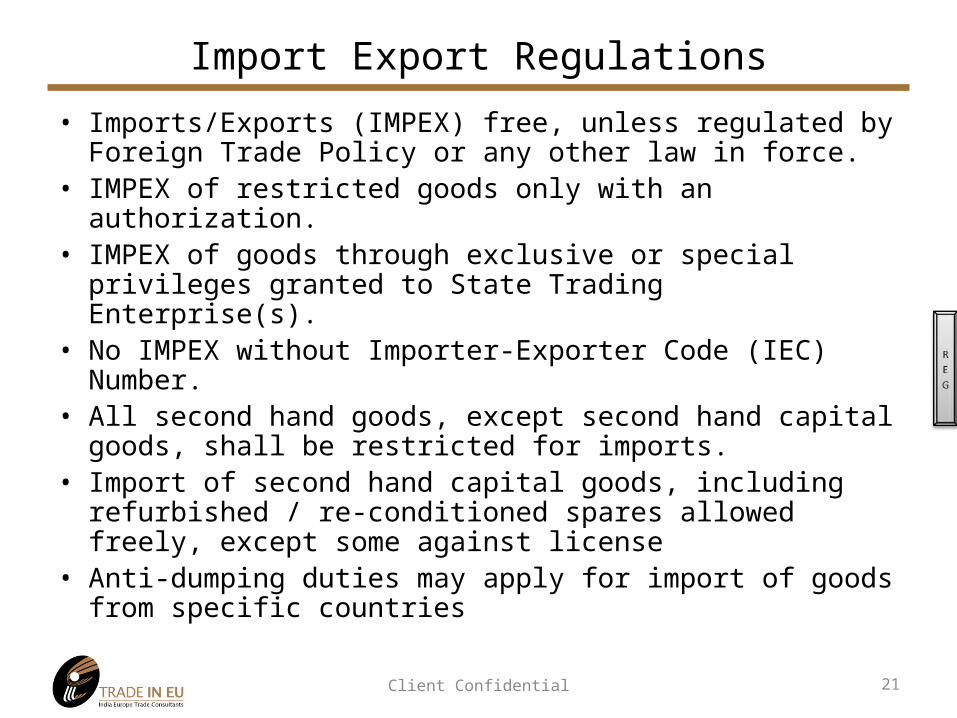

• Imports/Exports (IMPEX) free, unless regulated by Foreign Trade Policy or any other law in force.

• IMPEX of restricted goods only with an authorization.• IMPEX of goods through exclusive or special privileges

granted to State Trading Enterprise(s).• No IMPEX without Importer-Exporter Code (IEC) Number.• All second hand goods, except second hand capital goods,

shall be restricted for imports.• Import of second hand capital goods, including refurbished /

re-conditioned spares allowed freely, except some against license

• Anti-dumping duties may apply for import of goods from specific countries

21Client Confidential

Poll

Are your shipments often held by Customs?

22Client Confidential

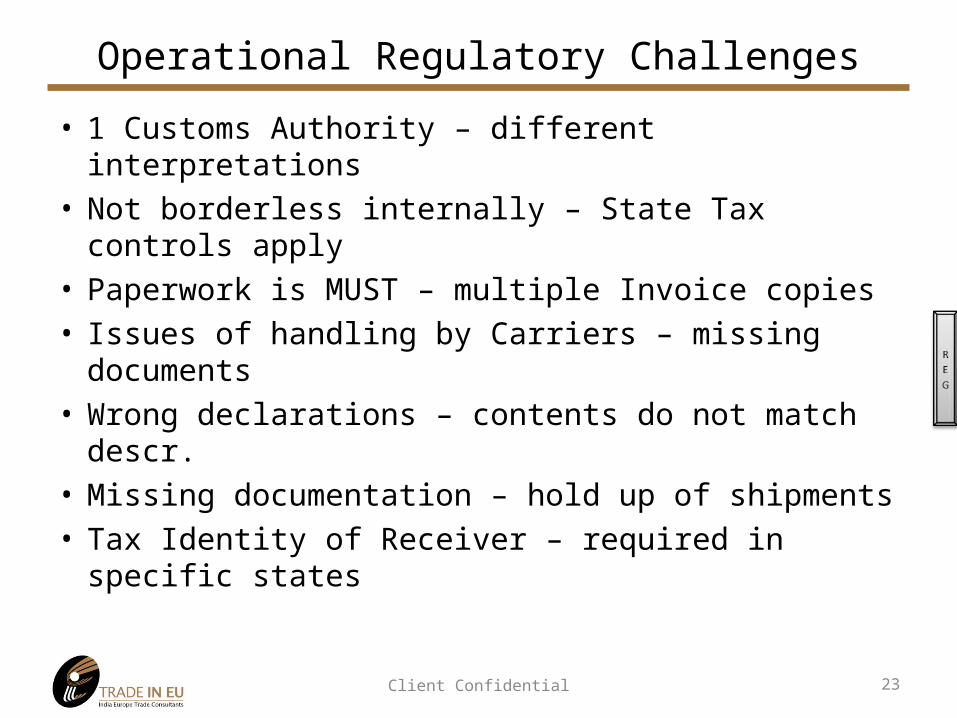

Operational Regulatory Challenges

• 1 Customs Authority – different interpretations• Not borderless internally – State Tax controls apply• Paperwork is MUST – multiple Invoice copies• Issues of handling by Carriers – missing documents• Wrong declarations – contents do not match descr.• Missing documentation – hold up of shipments• Tax Identity of Receiver – required in specific states

23Client Confidential

Customs – Compliance

• Indian Customs– Organization Structure– Field Organization– Directorate of Revenue Intelligence

• Compliance– Pricing / Valuation

• Special Provisions– Various Options– Appeals & Grievances – GST / SEZ / FTA

• Suggestions– Shipping Paperwork

24Client Confidential

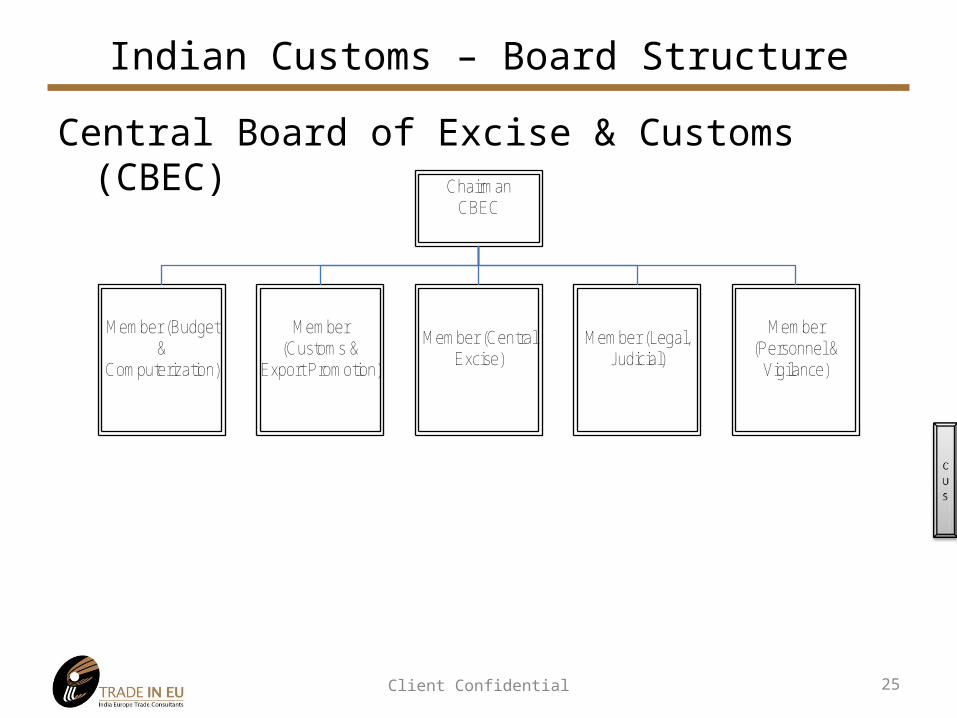

Indian Customs – Board Structure

Central Board of Excise & Customs (CBEC)Chairman

CBEC

Member (Central Excise)

Member (Legal, Judicial)

Member (Customs &

Export Promotion)

Member (Personnel &

Vigilance)

Member (Budget &

Computerization)

25Client Confidential

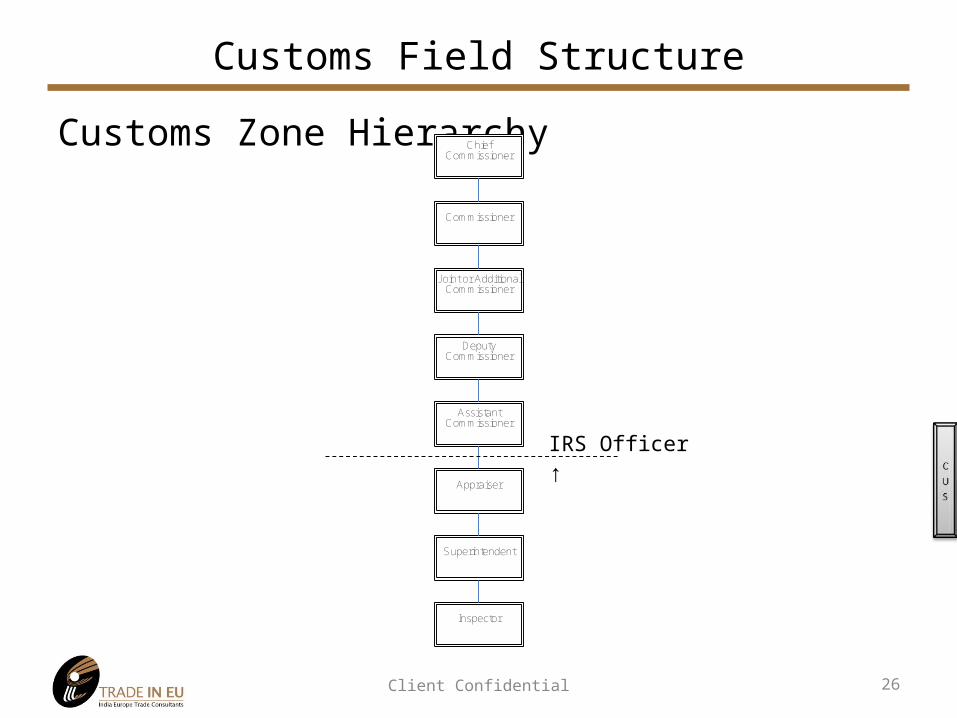

Customs Field Structure

Customs Zone Hierarchy Chief Commissioner

Commissioner

Joint or Additional Commissioner

Deputy Commissioner

Assistant Commissioner

Appraiser

Superintendent

Inspector

IRS Officer ↑

26Client Confidential

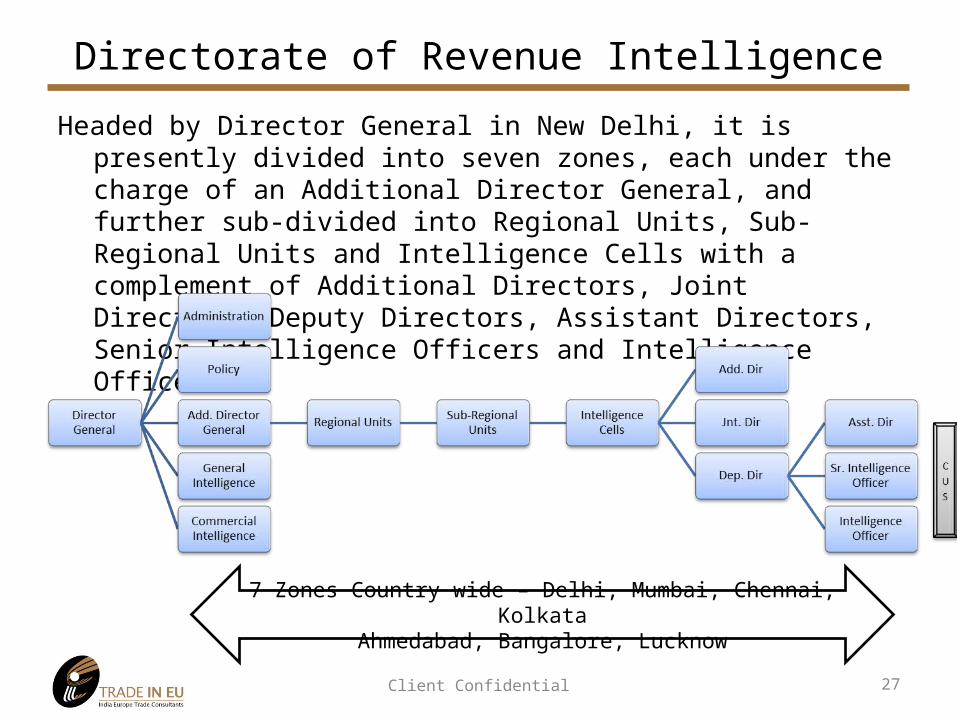

Directorate of Revenue Intelligence

Headed by Director General in New Delhi, it is presently divided into seven zones, each under the charge of an Additional Director General, and further sub-divided into Regional Units, Sub-Regional Units and Intelligence Cells with a complement of Additional Directors, Joint Directors, Deputy Directors, Assistant Directors, Senior Intelligence Officers and Intelligence Officers.

7 Zones Country wide – Delhi, Mumbai, Chennai, KolkataAhmedabad, Bangalore, Lucknow

27Client Confidential

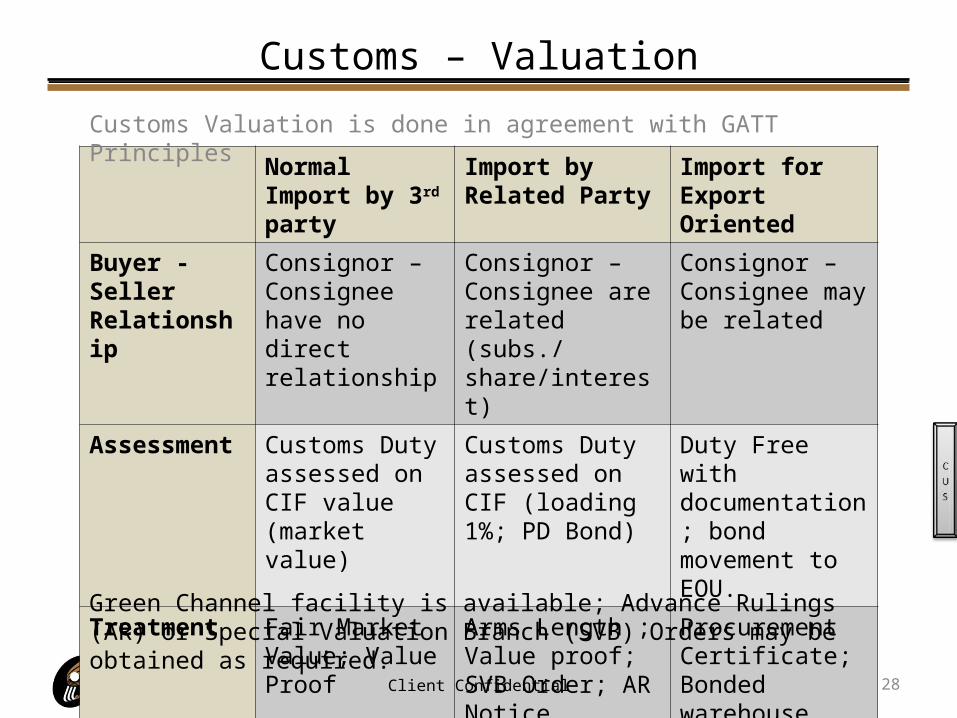

Customs – Valuation

Normal Import by 3rd party

Import by Related Party

Import for Export Oriented

Buyer - Seller Relationship

Consignor – Consignee have no direct relationship

Consignor – Consignee are related (subs./ share/interest)

Consignor – Consignee may be related

Assessment Customs Duty assessed on CIF value (market value)

Customs Duty assessed on CIF (loading 1%; PD Bond)

Duty Free with documentation; bond movement to EOU.

Treatment Fair Market Value; Value Proof

Arms Length ; Value proof; SVB Order; AR Notice

Procurement Certificate; Bonded warehouse

Green Channel facility is available; Advance Rulings (AR) or Special Valuation Branch (SVB) Orders may be obtained as required.

Customs Valuation is done in agreement with GATT Principles

Client Confidential 28

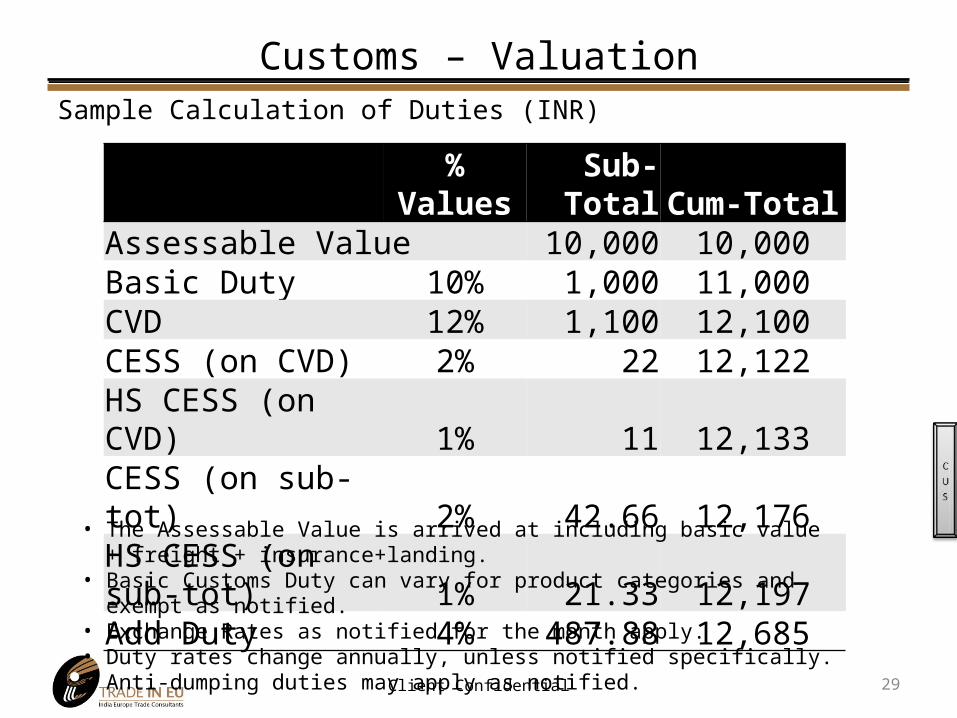

Customs – ValuationSample Calculation of Duties (INR)

% Values Sub-Total Cum-TotalAssessable Value 10,000 10,000Basic Duty 10% 1,000 11,000CVD 12% 1,100 12,100CESS (on CVD) 2% 22 12,122HS CESS (on CVD) 1% 11 12,133CESS (on sub-tot) 2% 42.66 12,176HS CESS (on sub-tot) 1% 21.33 12,197Add Duty 4% 487.88 12,685

• The Assessable Value is arrived at including basic value + freight + insurance+landing.• Basic Customs Duty can vary for product categories and exempt as notified.• Exchange Rates as notified for the month apply.• Duty rates change annually, unless notified specifically.• Anti-dumping duties may apply as notified.

29Client Confidential

Poll

Is valuation often an issue?

30Client Confidential

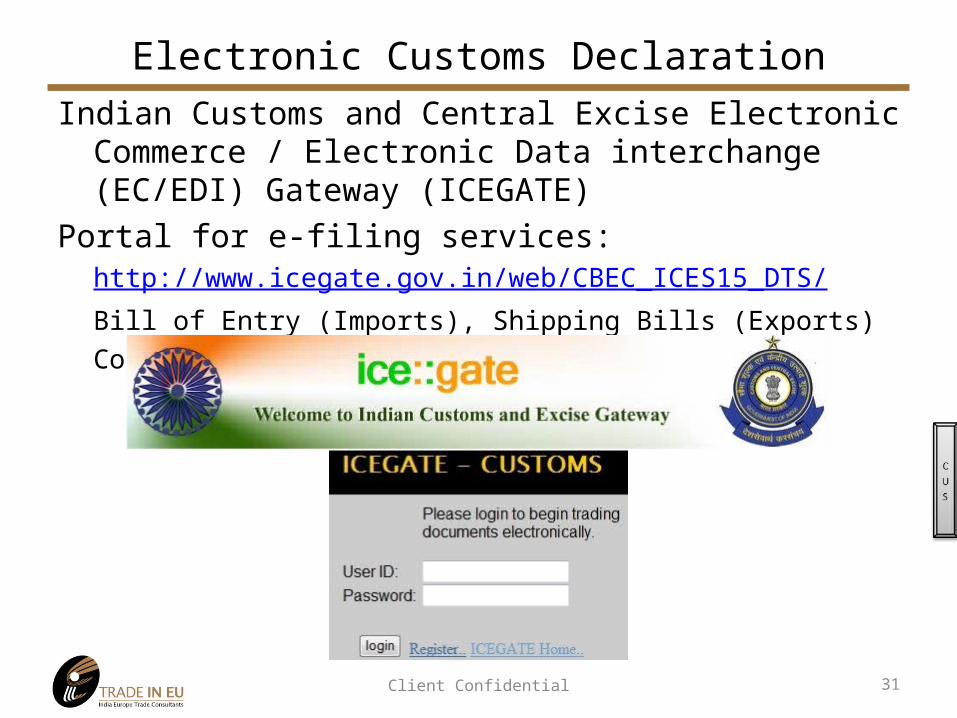

Electronic Customs Declaration

31Client Confidential

Indian Customs and Central Excise Electronic Commerce / Electronic Data interchange (EC/EDI) Gateway (ICEGATE)

Portal for e-filing services:http://www.icegate.gov.in/web/CBEC_ICES15_DTS/Bill of Entry (Imports), Shipping Bills (Exports)Communication of documents, Data Exchange

Special Provisions / Appeals / GrievancesSpecial provisions available under Indian Customs• Authority for Advance Ruling (AR)• Special Valuation Branch (SVB) Orders• Accredited Clients Program (ACP)

Appeals Mechanism• Commissioner Appeals• Appellate Tribunal• High Court

Grievances Mechanism• Complaints of corrupt practices against officers • Delay in decision making by officers. • Grievances against merits of the decision taken by officers.

© 32Client Confidential

Advance RulingAdvance Ruling – determination by the authority, of a question

of law or fact specified in the application regarding the liability to pay duty in relation to an activity (exports/imports) proposed to be undertaken, by the applicant.

Obtaining an advance ruling (Chapter V-B of the Indian Customs Act, 1962) by applicant in prescribed form, stating the question on which the advance ruling is sought.

The Applicant can be:• non-resident setting up a JV in collaboration with non-

resident or resident; or• resident setting up a JV in collaboration with non-resident; or• wholly owned subsidiary Indian company, of which the

holding company is a foreign company who proposes to undertake business activity in India.

© 33Client Confidential

Advance RulingThe question on which the advance ruling is sought shall be in respect of,-• classification of goods under the Customs Tariff Act, 1975 (51 of 1975);• applicability of a notification issued under sub-section (1) of section 25,

having a bearing on the rate of duty;• the principles to be adopted for the purposes of determination of value of

the goods under the provisions of this Act;• applicability of notifications issued in respect of duties under this Act, the

Customs Tariff Act, 1975 and any duty chargeable under any other law for the time being in force in the same manner as duty of customs chargeable under this Act;

• determination of origin of the goods in terms of the rules notified under the Customs Tariff Act, 1975 and matters relating thereto;

The application shall be made in 4 copies with a fee of INR 2,500.An application may be withdrawn within 30 days from the date of

application.

© 34Client Confidential

Special Valuation Branch (SVB)Special Valuation Branch (of Custom House), specializes in examining the

influence of relationship on the invoice value of the imported goods in respect of transactions between related parties.

Persons/parties shall be deemed to be "related" only if:• they are officers or directors of one another's businesses• they are legally recognized partners in business;• they are employer and employee;• any person directly or indirectly owns, controls or holds 5 per cent or

more of the outstanding voting stock or shares of both of them;• one of them directly or indirectly controls the other;• both of them are directly or indirectly controlled by a third person;• together they directly or indirectly control a third person;• they are members of the same family.

© 35Client Confidential

SVB OrderThe Special Valuation Branch is located only at 5 major Customs

House (Delhi, Bangalore, Chennai, Kolkata, Mumbai)A Special Valuation is usually triggered when the arms length

transaction value (price) cannot be established as outlined vide Circular 11/2001-CUS.

The SVB investigates additions to declared transaction value, if:• royalty and license fee• value of goods (resale, disposal, use) accrues to seller• other payments as condition of sale made or to be made in

future to seller The Customs Appraising group raises a reference to SVB.A case is registered by SVB.

© 36Client Confidential

Special Valuation Branch (SVB)

• SVB issues Provisional Duty (PD) Circular for provisional assessment and questionnaire for Importer to respond.

• Importer must clear goods on PD Bond + 1% extra duty deposit on assessable val.

• Importer must reply to the questionnaire from SVB within 30 days and/or appear in personal hearing as required.

• SVB must issue an Order-in-Original and decide on assessment within 4 months of filing, or the Importer can stop extra duty payments.

• Importer must quote SVB Order for all subsequent Imports.• The SVB Order is generally valid for 3 years.

37Client Confidential

Accredited Client Program (ACP)Accredited Client Program - Risk Management System (RMS).Greater degree of control; smoother trade flows for accredited.Importers with clean track record and history of compliance.Assured facilitation by RMS - Customs EDI accepts declared

classification, valuation & assessable duty on self-declaration.The import consignments not subject to examination (except

small number).Delivery of cargo is also speeded at various ports/airports.One approval for ACP eligible for all ICES locationsACP permission valid for 1 year (or if revoked for non

compliance/violation).ACP extended case to case basis by screening committee based

on review of the continuing compliance record.© 38Client Confidential

Accredited Client Program (ACP)Conditions for ACP application (approval time 4 weeks):• In previous financial year (PFY):

– imported goods valued at INR 100M (assessable value); Or– paid more than INR 10M Customs duty; Or,– Importers also Central Excise assessed, paid Central Excise Duties over INR

10M from Ledger.– filed at least 25 Bills of Entry in one or more Indian Customs stations.

• No cases of Customs, Central Excise or Service Tax booked against in 3 PFYs.• Cases booked should be at least a show cause notice, invoking penal provisions,

issued to an importer.• No cases booked under any of the Allied Acts being implemented by Customs.• Good Quality of submissions made to Customs (the number of amendments made

in the bills of entry submitted in relation to classification of goods, valuation and claim for exemption benefits).

• The number amendments not to exceed 20% of the bills of entry during the PFY.• No duty demands pending on account of non-fulfillment of Export obligation.• Have reliable systems of record keeping and internal controls and accounting

systems should conform to recognized standards of accounting. Provide necessary certificate from Chartered Accountants as per format.

© 39Client Confidential

ACP Compliance

Example of Correct Bill of Entry Filing (details to be specified)CTH Customs Tariff HeadingCETH Central Excise Tariff HeadingItem DescriptionGeneric descriptionManufacturer name Supplier detailsModel/Specification/gradeBrandCountry of OriginNumber of units/Total quantityUnit quantity codeUnit PriceNotifications and Serial numbersSVB details (if any)

© 40Client Confidential

AppealsAppeals or Revisions may be made to higher officials like

Joint/Additional Commissioner Customs / Appeals or to the Customs Appellate Tribunal.

Commissioner Appeals - section 128 Form No. C.A.-1 (2 copies)+ 2 copies of decision / order by adjudicating authority1 copy of the order passed by the Commissioner of Customs directing such authority to apply to Commissioner Appeals

Appellate Tribunal – section 129A Form No. C.A.-3 (4 copies).

© 41Client Confidential

GrievancesPublic Relations Officer (PRO) – for information on technical or

administrative matter.Public Grievance Committees (PGC) - every Customs House

(monthly) and reports to the Regional Advisory Committees.Watch Dog Committee - available at Customs House weekly.Customs and Central Excise Central Advisory Council - available

at apex level for addressing policy level changes.Director General of Vigilance is also the Chief Vigilance Officer of

the Central Board of Excise & Customs.

© 42Client Confidential

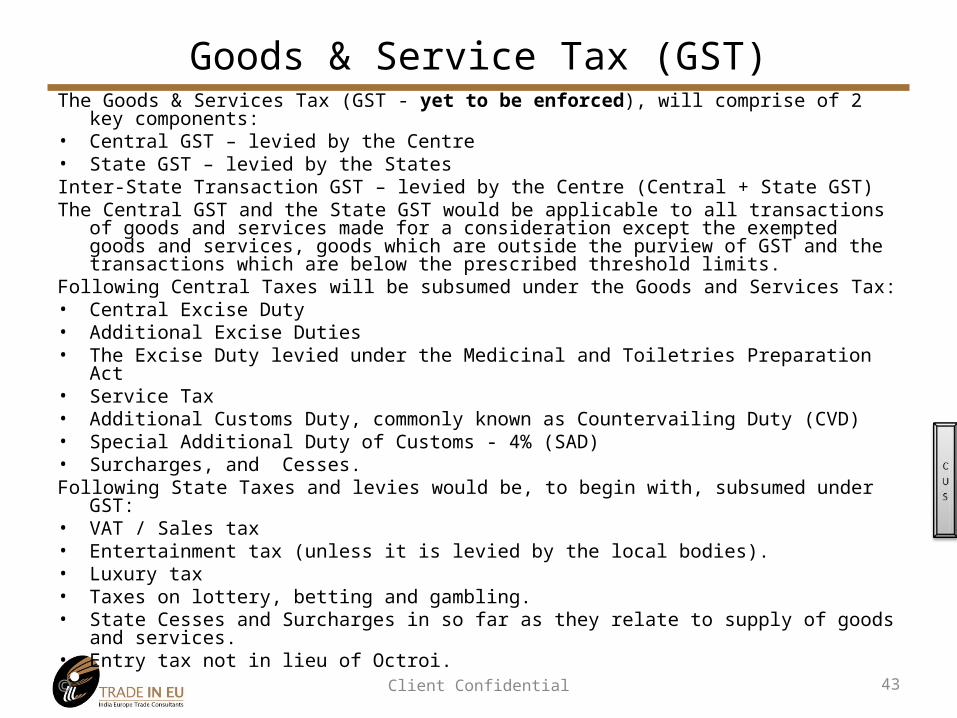

Goods & Service Tax (GST)The Goods & Services Tax (GST - yet to be enforced), will comprise of 2 key components:• Central GST – levied by the Centre• State GST – levied by the StatesInter-State Transaction GST – levied by the Centre (Central + State GST)The Central GST and the State GST would be applicable to all transactions of goods and services

made for a consideration except the exempted goods and services, goods which are outside the purview of GST and the transactions which are below the prescribed threshold limits.

Following Central Taxes will be subsumed under the Goods and Services Tax:• Central Excise Duty• Additional Excise Duties• The Excise Duty levied under the Medicinal and Toiletries Preparation Act• Service Tax• Additional Customs Duty, commonly known as Countervailing Duty (CVD)• Special Additional Duty of Customs - 4% (SAD)• Surcharges, and Cesses.Following State Taxes and levies would be, to begin with, subsumed under GST:• VAT / Sales tax• Entertainment tax (unless it is levied by the local bodies).• Luxury tax• Taxes on lottery, betting and gambling. • State Cesses and Surcharges in so far as they relate to supply of goods and services.• Entry tax not in lieu of Octroi.

© 43Client Confidential

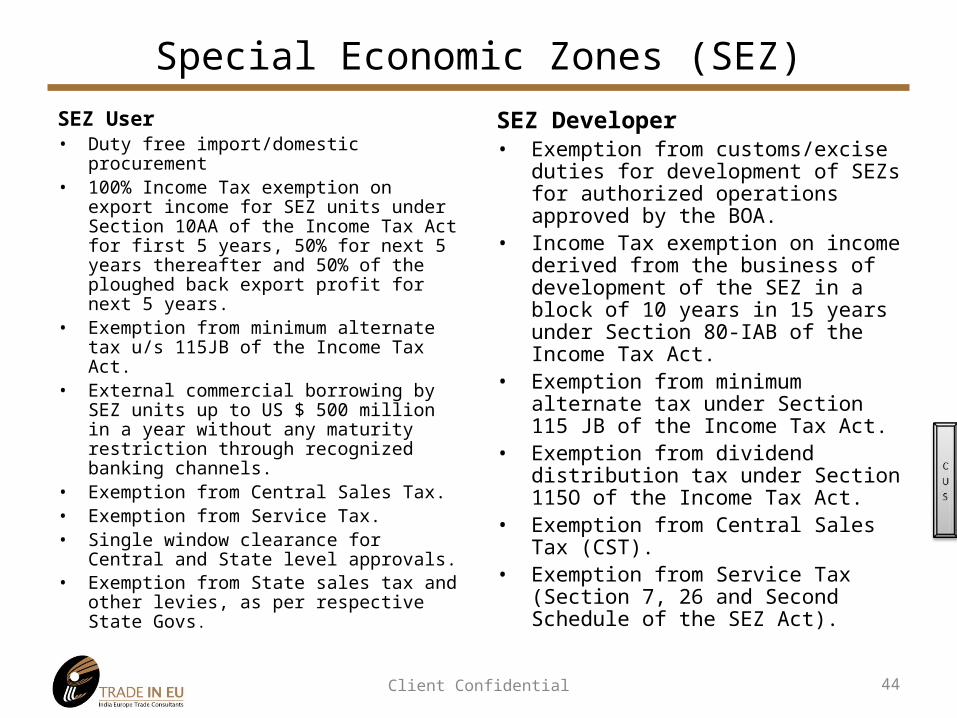

Special Economic Zones (SEZ)

SEZ User• Duty free import/domestic procurement• 100% Income Tax exemption on export

income for SEZ units under Section 10AA of the Income Tax Act for first 5 years, 50% for next 5 years thereafter and 50% of the ploughed back export profit for next 5 years.

• Exemption from minimum alternate tax u/s 115JB of the Income Tax Act.

• External commercial borrowing by SEZ units up to US $ 500 million in a year without any maturity restriction through recognized banking channels.

• Exemption from Central Sales Tax. • Exemption from Service Tax. • Single window clearance for Central and

State level approvals.• Exemption from State sales tax and other

levies, as per respective State Govs.

SEZ Developer• Exemption from customs/excise duties for

development of SEZs for authorized operations approved by the BOA.

• Income Tax exemption on income derived from the business of development of the SEZ in a block of 10 years in 15 years under Section 80-IAB of the Income Tax Act.

• Exemption from minimum alternate tax under Section 115 JB of the Income Tax Act.

• Exemption from dividend distribution tax under Section 115O of the Income Tax Act.

• Exemption from Central Sales Tax (CST). • Exemption from Service Tax (Section 7, 26

and Second Schedule of the SEZ Act).

44Client Confidential

Trade Agreements• India EU Trade and Investment

Agreement TIA• India-EU Strategic Partnership Joint

Action Plan• Framework agreement with Chile• Framework Agreement with GCC

States• Framework Agreement with Thailand• Framework Agreement with ASEAN• India-MERCOSUR PTA• India Chile PTA• India-Afghanistan PTA• Asia Pacific Trade Agreement (APTA)• India-Sri Lanka FTA• India-Bhutan Trade Agreement• India-Bangladesh Trade Agreement

• India-United States Commercial Dialogue

• India-US Trade Policy Forum Joint Statement

• India-Mongolia Trade Agreement• India-Nepal Trade Treaty• India-China Trade Agreement• India-Maldives Trade Agreement• India-Korea Trade Agreement• India-DPR Korea Trade Agreement• India-Japan Trade Agreement• India-Korea Joint Study Group• India-Ceylon Trade Agreement• CECA between The Republic of India

and the Republic of Singapore• India Pakistan Trading Arrangement

45Client Confidential

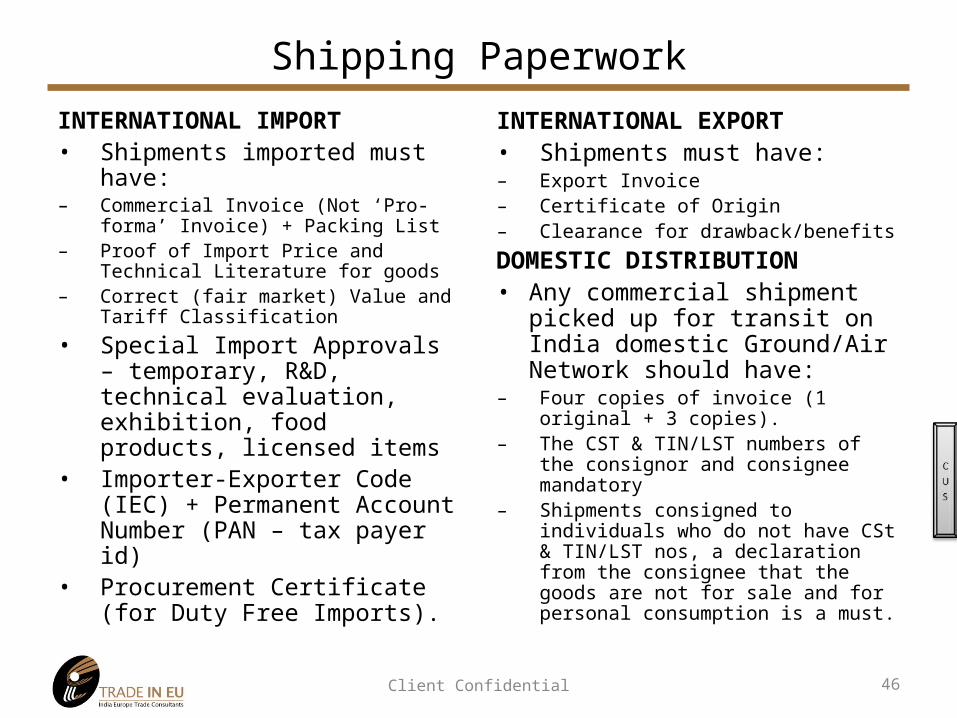

Shipping Paperwork

INTERNATIONAL IMPORT• Shipments imported must have:– Commercial Invoice (Not ‘Pro-forma’

Invoice) + Packing List– Proof of Import Price and Technical

Literature for goods– Correct (fair market) Value and Tariff

Classification

• Special Import Approvals – temporary, R&D, technical evaluation, exhibition, food products, licensed items

• Importer-Exporter Code (IEC) + Permanent Account Number (PAN – tax payer id)

• Procurement Certificate (for Duty Free Imports).

INTERNATIONAL EXPORT• Shipments must have:– Export Invoice– Certificate of Origin– Clearance for drawback/benefits

DOMESTIC DISTRIBUTION• Any commercial shipment picked

up for transit on India domestic Ground/Air Network should have:

– Four copies of invoice (1 original + 3 copies).

– The CST & TIN/LST numbers of the consignor and consignee mandatory

– Shipments consigned to individuals who do not have CSt & TIN/LST nos, a declaration from the consignee that the goods are not for sale and for personal consumption is a must.

46Client Confidential

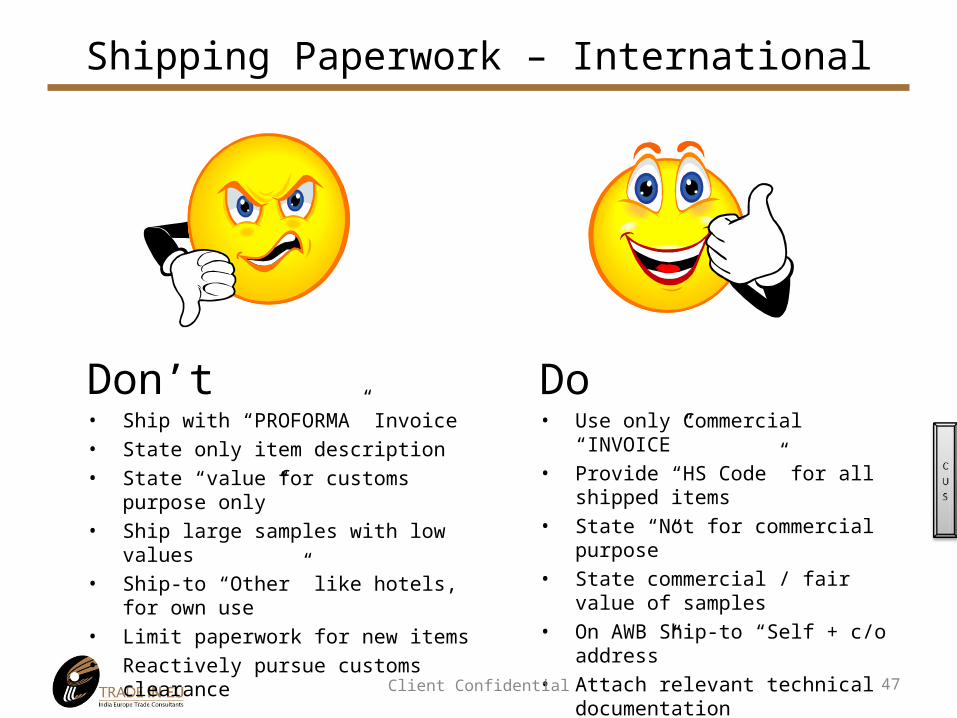

Shipping Paperwork – International

47

Don’t• Ship with “PROFORMA” Invoice• State only item description• State “value for customs purpose only”• Ship large samples with low values• Ship-to “Other” like hotels, for own use• Limit paperwork for new items• Reactively pursue customs clearance

Do• Use only Commercial “INVOICE”• Provide “HS Code” for all shipped items• State “Not for commercial purpose”• State commercial / fair value of samples• On AWB Ship-to “Self + c/o address”• Attach relevant technical

documentation• Pro-actively support customs clearance

Client Confidential

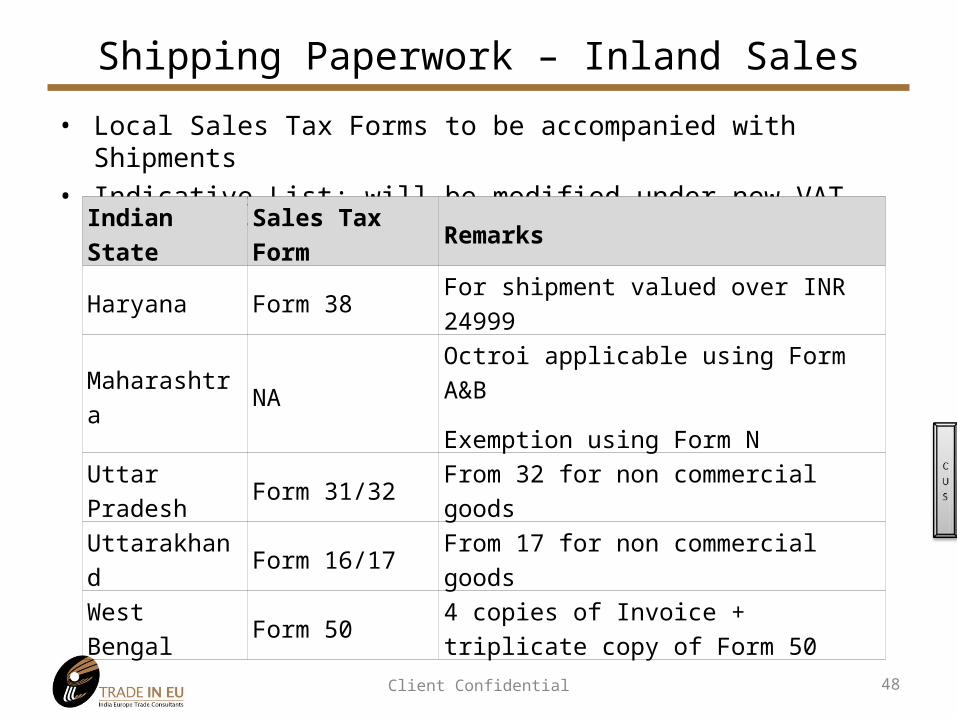

Shipping Paperwork – Inland Sales

• Local Sales Tax Forms to be accompanied with Shipments• Indicative List; will be modified under new VAT regulations

48

Indian State Sales Tax Form Remarks

Haryana Form 38 For shipment valued over INR 24999

Maharashtra NAOctroi applicable using Form A&B

Exemption using Form N

Uttar Pradesh Form 31/32 From 32 for non commercial goods

Uttarakhand Form 16/17 From 17 for non commercial goods

West Bengal Form 504 copies of Invoice + triplicate copy of

Form 50

Client Confidential

Q&A

49Client Confidential

Questions / Comments…

Contact

Vivek Luthra(India Market Specialist)Trade IN EU (TIE)India Europe Trade ConsultantsGodesberger Allee 139,53175, Bonn-GermanyT: +49-228-8236-9359M: +49-160-9068-7676E: [email protected]: www.tradeineu.com

© 50Client Confidential

DISCLAIMERS:• All information in the presentation is for reference only.• Please validate duty structures and calculations thereof.• The presentation may not be copied and distributed without written permission.