Continuing Work in Robust Portfolio Optimizationdano/talks/w.pdfContinuing Work in Robust Portfolio...

127

Continuing Work in Robust Portfolio Optimization Daniel Bienstock Columbia University, New York 30 June 2008 Daniel Bienstock ( Columbia University, New York) Continuing Work in Robust Portfolio Optimization 30 June 2008 1 / 58

Transcript of Continuing Work in Robust Portfolio Optimizationdano/talks/w.pdfContinuing Work in Robust Portfolio...

Continuing Work in Robust PortfolioOptimization

Daniel Bienstock

Columbia University, New York

30 June 2008

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 1 / 58

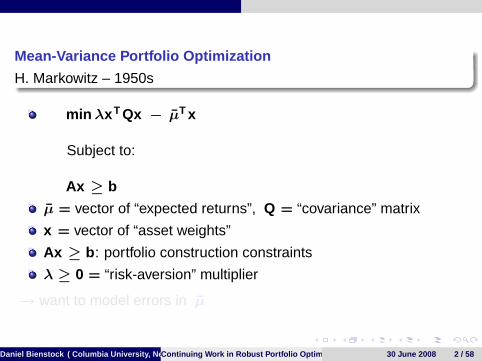

Mean-Variance Portfolio Optimization

H. Markowitz – 1950s

min λx T Qx − µT x

Subject to:

Ax ≥ b

µ = vector of “expected returns”, Q = “covariance” matrix

x = vector of “asset weights”

Ax ≥ b : portfolio construction constraints

λ ≥ 0 = “risk-aversion” multiplier

→ want to model errors in µ

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 2 / 58

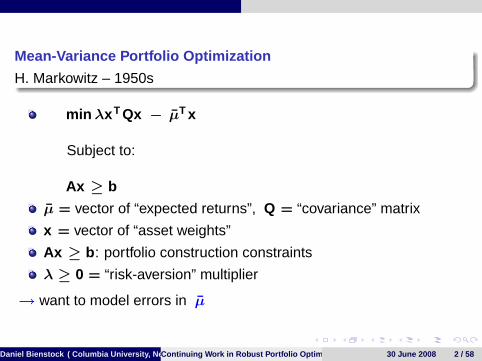

Mean-Variance Portfolio Optimization

H. Markowitz – 1950s

min λx T Qx − µT x

Subject to:

Ax ≥ b

µ = vector of “expected returns”, Q = “covariance” matrix

x = vector of “asset weights”

Ax ≥ b : portfolio construction constraints

λ ≥ 0 = “risk-aversion” multiplier

→ want to model errors in µ

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 2 / 58

Robust Optimization

Optimization under parameter (data) uncertainty

Ben-Tal and Nemirovsky, El Ghaoui et al

Bertsimas et al

Uncertainty is modeled by assuming that data is not knownprecisely, and will instead lie in known sets.

Example: a coefficient ai is uncertain. We allow ai ∈ [l i , u i ].

Typically, a minimization problem becomes a min-max problem.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 3 / 58

Robust Optimization

Optimization under parameter (data) uncertainty

Ben-Tal and Nemirovsky, El Ghaoui et al

Bertsimas et al

Uncertainty is modeled by assuming that data is not knownprecisely, and will instead lie in known sets.

Example: a coefficient ai is uncertain. We allow ai ∈ [l i , u i ].

Typically, a minimization problem becomes a min-max problem.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 3 / 58

Robust Optimization

Optimization under parameter (data) uncertainty

Ben-Tal and Nemirovsky, El Ghaoui et al

Bertsimas et al

Uncertainty is modeled by assuming that data is not knownprecisely, and will instead lie in known sets.

Example: a coefficient ai is uncertain. We allow ai ∈ [l i , u i ].

Typically, a minimization problem becomes a min-max problem.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 3 / 58

Robust Optimization

Optimization under parameter (data) uncertainty

Ben-Tal and Nemirovsky, El Ghaoui et al

Bertsimas et al

Uncertainty is modeled by assuming that data is not knownprecisely, and will instead lie in known sets.

Example: a coefficient ai is uncertain. We allow ai ∈ [l i , u i ].

Typically, a minimization problem becomes a min-max problem.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 3 / 58

Robust Optimization

Optimization under parameter (data) uncertainty

Ben-Tal and Nemirovsky, El Ghaoui et al

Bertsimas et al

Uncertainty is modeled by assuming that data is not knownprecisely, and will instead lie in known sets.

Example: a coefficient ai is uncertain. We allow ai ∈ [l i , u i ].

Typically, a minimization problem becomes a min-max problem.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 3 / 58

Robust Optimization

Optimization under parameter (data) uncertainty

Ben-Tal and Nemirovsky, El Ghaoui et al

Bertsimas et al

Uncertainty is modeled by assuming that data is not knownprecisely, and will instead lie in known sets.

Example: a coefficient ai is uncertain. We allow ai ∈ [l i , u i ].

Typically, a minimization problem becomes a min-max problem.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 3 / 58

Robust Portfolio Optimization

How to handle uncertain returns

min λx T Qx − µT xSubject to:Ax ≥ b

→ M = set of allowable return vectors (“around” µ)

min x maxµ∈M{λx T Qx − µT x

}Subject to:Ax ≥ b

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 4 / 58

Robust Portfolio Optimization

How to handle uncertain returns

min λx T Qx − µT xSubject to:Ax ≥ b

→ M = set of allowable return vectors (“around” µ)

min x maxµ∈M{λx T Qx − µT x

}Subject to:Ax ≥ b

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 4 / 58

Robust Portfolio Optimization

How to handle uncertain returns

min λx T Qx − µT xSubject to:Ax ≥ b

→ M = set of allowable return vectors (“around” µ)

min x maxµ∈M{λx T Qx − µT x

}Subject to:Ax ≥ b

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 4 / 58

Robust Portfolio Optimization

How to handle uncertain returns

min λx T Qx − µT xSubject to:Ax ≥ b

→ M = set of allowable return vectors (“around” µ)

min x{λx T Qx − min µ∈M µT x

}Subject to:Ax ≥ b

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 5 / 58

Robust Portfolio Optimization

How to handle uncertain returns

min λx T Qx − µT xSubject to:Ax ≥ b

→ M = set of allowable return vectors (“around” µ)

1 The investor chooses a vector x of assets

2 The adversary chooses a returns vector µ ∈M so as minimizereturn: obtain µmin (x )

Robust problem: min x λx T Qx − µmin (x )

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 6 / 58

Robust Portfolio Optimization

How to handle uncertain returns

min λx T Qx − µT xSubject to:Ax ≥ b

→ M = set of allowable return vectors (“around” µ)

1 The investor chooses a vector x of assets

2 The adversary chooses a returns vector µ ∈M so as minimizereturn: obtain µmin (x )

Robust problem: min x λx T Qx − µmin (x )

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 6 / 58

Robust Portfolio Optimization

How to handle uncertain returns

min λx T Qx − µT xSubject to:Ax ≥ b

→ M = set of allowable return vectors (“around” µ)

1 The investor chooses a vector x of assets

2 The adversary chooses a returns vector µ ∈M so as minimizereturn: obtain µmin (x )

Robust problem: min x λx T Qx − µmin (x )

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 6 / 58

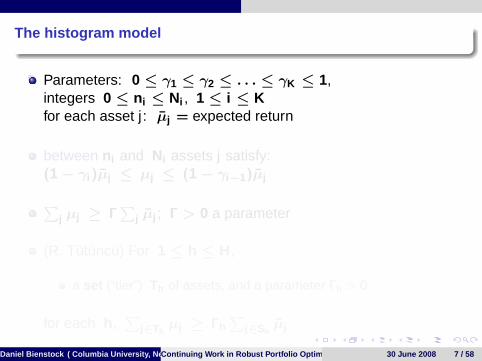

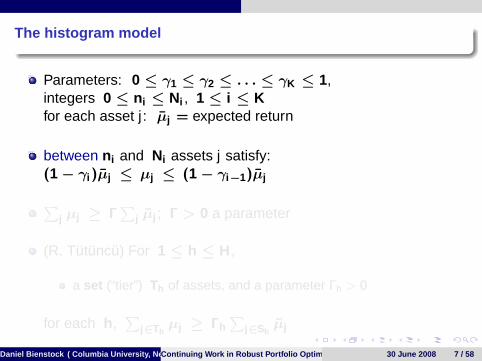

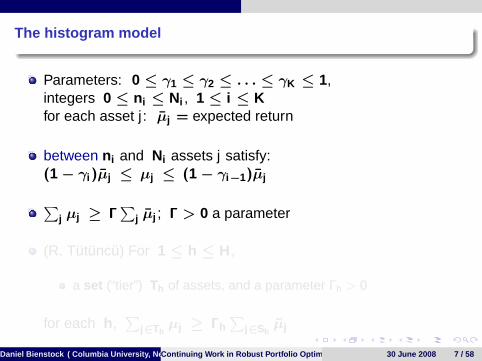

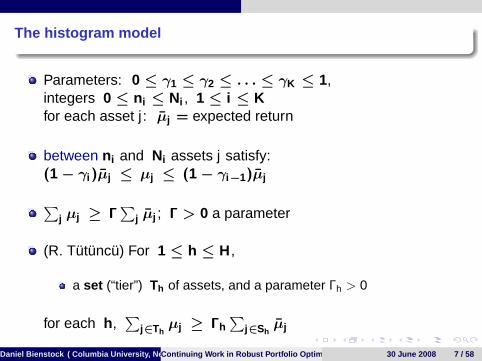

The histogram model

Parameters: 0 ≤ γ1 ≤ γ2 ≤ . . . ≤ γK ≤ 1,integers 0 ≤ n i ≤ Ni , 1 ≤ i ≤ Kfor each asset j : µj = expected return

between n i and Ni assets j satisfy:(1− γi )µj ≤ µj ≤ (1− γi−1)µj∑

j µj ≥ Γ∑

j µj ; Γ > 0 a parameter

(R. Tutuncu) For 1 ≤ h ≤ H,

a set (“tier”) Th of assets, and a parameter Γh > 0

for each h,∑

j∈Thµj ≥ Γh

∑j∈Sh

µj

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 7 / 58

The histogram model

Parameters: 0 ≤ γ1 ≤ γ2 ≤ . . . ≤ γK ≤ 1,integers 0 ≤ n i ≤ Ni , 1 ≤ i ≤ Kfor each asset j : µj = expected return

between n i and Ni assets j satisfy:(1− γi )µj ≤ µj ≤ (1− γi−1)µj∑

j µj ≥ Γ∑

j µj ; Γ > 0 a parameter

(R. Tutuncu) For 1 ≤ h ≤ H,

a set (“tier”) Th of assets, and a parameter Γh > 0

for each h,∑

j∈Thµj ≥ Γh

∑j∈Sh

µj

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 7 / 58

The histogram model

Parameters: 0 ≤ γ1 ≤ γ2 ≤ . . . ≤ γK ≤ 1,integers 0 ≤ n i ≤ Ni , 1 ≤ i ≤ Kfor each asset j : µj = expected return

between n i and Ni assets j satisfy:(1− γi )µj ≤ µj ≤ (1− γi−1)µj∑

j µj ≥ Γ∑

j µj ; Γ > 0 a parameter

(R. Tutuncu) For 1 ≤ h ≤ H,

a set (“tier”) Th of assets, and a parameter Γh > 0

for each h,∑

j∈Thµj ≥ Γh

∑j∈Sh

µj

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 7 / 58

The histogram model

Parameters: 0 ≤ γ1 ≤ γ2 ≤ . . . ≤ γK ≤ 1,integers 0 ≤ n i ≤ Ni , 1 ≤ i ≤ Kfor each asset j : µj = expected return

between n i and Ni assets j satisfy:(1− γi )µj ≤ µj ≤ (1− γi−1)µj∑

j µj ≥ Γ∑

j µj ; Γ > 0 a parameter

(R. Tutuncu) For 1 ≤ h ≤ H,

a set (“tier”) Th of assets, and a parameter Γh > 0

for each h,∑

j∈Thµj ≥ Γh

∑j∈Sh

µj

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 7 / 58

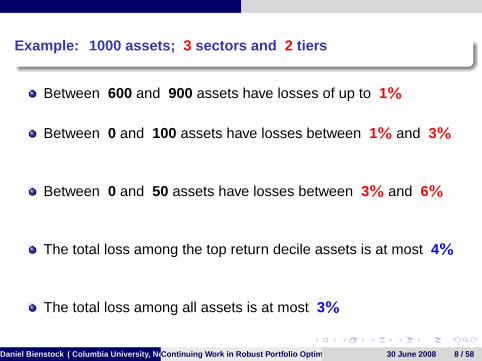

Example: 1000 assets; 3 sectors and 2 tiers

Between 600 and 900 assets have losses of up to 1%

Between 0 and 100 assets have losses between 1% and 3%

Between 0 and 50 assets have losses between 3% and 6%

The total loss among the top return decile assets is at most 4%

The total loss among all assets is at most 3%

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 8 / 58

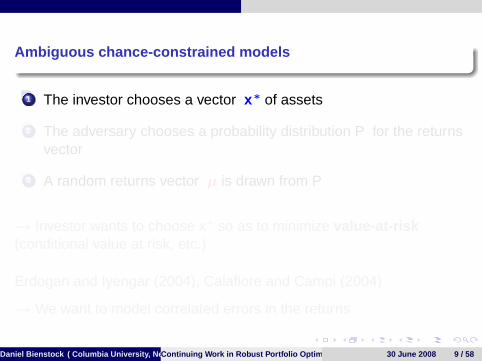

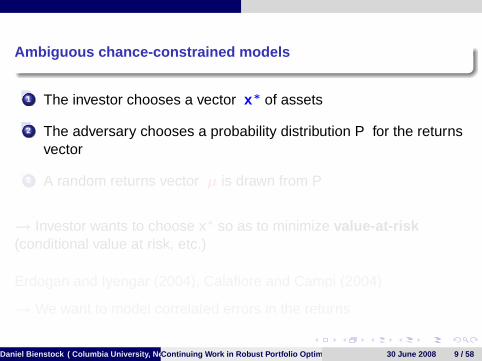

Ambiguous chance-constrained models

1 The investor chooses a vector x ∗ of assets

2 The adversary chooses a probability distribution P for the returnsvector

3 A random returns vector µ is drawn from P

→ Investor wants to choose x∗ so as to minimize value-at-risk(conditional value at risk, etc.)

Erdogan and Iyengar (2004), Calafiore and Campi (2004)

→We want to model correlated errors in the returns

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 9 / 58

Ambiguous chance-constrained models

1 The investor chooses a vector x ∗ of assets

2 The adversary chooses a probability distribution P for the returnsvector

3 A random returns vector µ is drawn from P

→ Investor wants to choose x∗ so as to minimize value-at-risk(conditional value at risk, etc.)

Erdogan and Iyengar (2004), Calafiore and Campi (2004)

→We want to model correlated errors in the returns

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 9 / 58

Ambiguous chance-constrained models

1 The investor chooses a vector x ∗ of assets

2 The adversary chooses a probability distribution P for the returnsvector

3 A random returns vector µ is drawn from P

→ Investor wants to choose x∗ so as to minimize value-at-risk(conditional value at risk, etc.)

Erdogan and Iyengar (2004), Calafiore and Campi (2004)

→We want to model correlated errors in the returns

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 9 / 58

Ambiguous chance-constrained models

1 The investor chooses a vector x ∗ of assets

2 The adversary chooses a probability distribution P for the returnsvector

3 A random returns vector µ is drawn from P

→ Investor wants to choose x∗ so as to minimize value-at-risk(conditional value at risk, etc.)

Erdogan and Iyengar (2004), Calafiore and Campi (2004)

→We want to model correlated errors in the returns

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 9 / 58

Ambiguous chance-constrained models

1 The investor chooses a vector x ∗ of assets

2 The adversary chooses a probability distribution P for the returnsvector

3 A random returns vector µ is drawn from P

→ Investor wants to choose x∗ so as to minimize value-at-risk(conditional value at risk, etc.)

Erdogan and Iyengar (2004), Calafiore and Campi (2004)

→We want to model correlated errors in the returns

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 9 / 58

Ambiguous chance-constrained models

1 The investor chooses a vector x ∗ of assets

2 The adversary chooses a probability distribution P for the returnsvector

3 A random returns vector µ is drawn from P

→ Investor wants to choose x∗ so as to minimize value-at-risk(conditional value at risk, etc.)

Erdogan and Iyengar (2004), Calafiore and Campi (2004)

→We want to model correlated errors in the returns

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 9 / 58

Uncertainty set

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

Definition (Rockafellar and Uryasev): Given reals ν and 0 ≤ θ ≤ 1the value-at-risk of x∗ is the real ρ ≥ 0 such that

Prob(ν − µT x ∗ ≥ ρ) ≥ θ

→ The adversary wants to maximize VaR

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 10 / 58

Uncertainty set

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

Definition (Rockafellar and Uryasev): Given reals ν and 0 ≤ θ ≤ 1the value-at-risk of x∗ is the real ρ ≥ 0 such that

Prob(ν − µT x ∗ ≥ ρ) ≥ θ

→ The adversary wants to maximize VaR

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 10 / 58

Uncertainty set

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

Definition (Rockafellar and Uryasev): Given reals ν and 0 ≤ θ ≤ 1the value-at-risk of x∗ is the real ρ ≥ 0 such that

Prob(ν − µT x ∗ ≥ ρ) ≥ θ

→ The adversary wants to maximize VaR

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 10 / 58

Uncertainty set

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

Definition (Rockafellar and Uryasev): Given reals ν and 0 ≤ θ ≤ 1the value-at-risk of x∗ is the real ρ ≥ 0 such that

Prob(ν − µT x ∗ ≥ ρ) ≥ θ

→ The adversary wants to maximize VaR

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 10 / 58

Uncertainty set

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

Definition (Rockafellar and Uryasev): Given reals ν and 0 ≤ θ ≤ 1the value-at-risk of x∗ is the real ρ ≥ 0 such that

Prob(ν − µT x ∗ ≥ ρ) ≥ θ

→ The adversary wants to maximize VaR

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 10 / 58

Uncertainty set

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

Definition (Rockafellar and Uryasev): Given reals ν and 0 ≤ θ ≤ 1the value-at-risk of x∗ is the real ρ ≥ 0 such that

Prob(ν − µT x ∗ ≥ ρ) ≥ θ

→ The adversary wants to maximize VaR

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 10 / 58

Uncertainty set

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

Definition: Given reals ν and 0 ≤ θ ≤ 1 the conditional value-at-riskof x∗ equals

E(ν − µT x ∗ | ν − µT x ∗ ≥ ρ) where ρ = VaR

→ The adversary wants to maximize CVaR

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 11 / 58

Robust optimization problem (VaR case):Given 0 < ε,

min V

Subject to:

λx T Qx − µT x ≤ v ∗ + ε

Ax ≥ b

V ≥ VaRmax (x )

Here, v ∗ .= min λx T Qx − µT x

Subject to:

Ax ≥ b

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 12 / 58

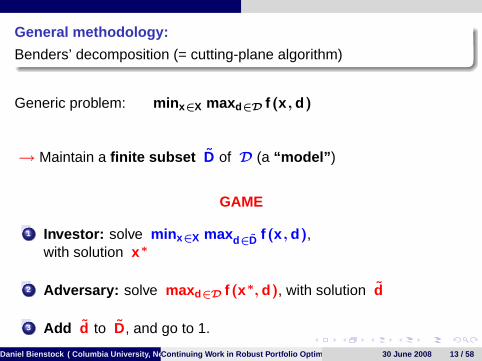

General methodology:

Benders’ decomposition (= cutting-plane algorithm)

Generic problem: min x∈X maxd∈D f (x , d )

→ Maintain a finite subset D of D (a “model” )

GAME

1 Investor: solve min x∈X maxd∈D f (x , d ),with solution x ∗

2 Adversary: solve maxd∈D f (x ∗, d ), with solution d

3 Add d to D, and go to 1.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 13 / 58

General methodology:

Benders’ decomposition (= cutting-plane algorithm)

Generic problem: min x∈X maxd∈D f (x , d )

→ Maintain a finite subset D of D (a “model” )

GAME

1 Investor: solve min x∈X maxd∈D f (x , d ),with solution x ∗

2 Adversary: solve maxd∈D f (x ∗, d ), with solution d

3 Add d to D, and go to 1.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 13 / 58

General methodology:

Benders’ decomposition (= cutting-plane algorithm)

Generic problem: min x∈X maxd∈D f (x , d )

→ Maintain a finite subset D of D (a “model” )

GAME

1 Investor: solve min x∈X maxd∈D f (x , d ),with solution x ∗

2 Adversary: solve maxd∈D f (x ∗, d ), with solution d

3 Add d to D, and go to 1.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 13 / 58

General methodology:

Benders’ decomposition (= cutting-plane algorithm)

Generic problem: min x∈X maxd∈D f (x , d )

→ Maintain a finite subset D of D (a “model” )

GAME

1 Investor: solve min x∈X maxd∈D f (x , d ),with solution x ∗

2 Adversary: solve maxd∈D f (x ∗, d ), with solution d

3 Add d to D, and go to 1.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 13 / 58

General methodology:

Benders’ decomposition (= cutting-plane algorithm)

Generic problem: min x∈X maxd∈D f (x , d )

→ Maintain a finite subset D of D (a “model” )

GAME

1 Investor: solve min x∈X maxd∈D f (x , d ),with solution x ∗

2 Adversary: solve maxd∈D f (x ∗, d ), with solution d

3 Add d to D, and go to 1.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 13 / 58

Why this approach

Decoupling of investor and adversary yields considerably simpler,and smaller, problems

Decoupling allows us to use more sophisticated uncertaintymodels

If number of iterations is small, investor’s problem is a small“convex” problem

Most progress will be achieved in initial iterations – permits “soft”termination criteria

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 14 / 58

Why this approach

Decoupling of investor and adversary yields considerably simpler,and smaller, problems

Decoupling allows us to use more sophisticated uncertaintymodels

If number of iterations is small, investor’s problem is a small“convex” problem

Most progress will be achieved in initial iterations – permits “soft”termination criteria

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 14 / 58

Why this approach

Decoupling of investor and adversary yields considerably simpler,and smaller, problems

Decoupling allows us to use more sophisticated uncertaintymodels

If number of iterations is small, investor’s problem is a small“convex” problem

Most progress will be achieved in initial iterations – permits “soft”termination criteria

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 14 / 58

Why this approach

Decoupling of investor and adversary yields considerably simpler,and smaller, problems

Decoupling allows us to use more sophisticated uncertaintymodels

If number of iterations is small, investor’s problem is a small“convex” problem

Most progress will be achieved in initial iterations – permits “soft”termination criteria

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 14 / 58

Why this approach

Decoupling of investor and adversary yields considerably simpler,and smaller, problems

Decoupling allows us to use more sophisticated uncertaintymodels

If number of iterations is small, investor’s problem is a small“convex” problem

Most progress will be achieved in initial iterations – permits “soft”termination criteria

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 14 / 58

The game, applied to the robust optimization problem

Histogram version

Robust problem:

min x{λx T Qx − min µ∈M µT x

}Subject to:Ax ≥ b

Investor’s problem: M is replaced by a finite subset M

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 15 / 58

The game, applied to the robust optimization problem

Histogram version

Robust problem:

min x{λx T Qx − min µ∈M µT x

}Subject to:Ax ≥ b

Investor’s problem: M is replaced by a finite subset M

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 15 / 58

Investor’s problem

A convex quadratic program

At iteration m, solve

min λx T Qx − r

Subject to:

Ax ≥ b

r ≤ µT(i )x , i = 1, . . . , m

Here, µ(1), . . . , µ(m) are given return vectors

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 16 / 58

The game, applied to the robust optimization problem

Histogram version

Robust problem:

min x{λx T Qx − min µ∈M µT x

}Subject to:Ax ≥ b

Adversary’s problem: Given asset vector x , solve min µ∈M µT x

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 17 / 58

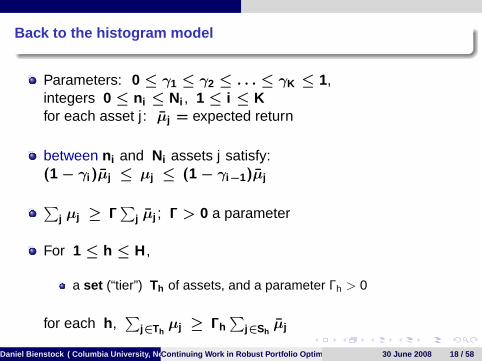

Back to the histogram model

Parameters: 0 ≤ γ1 ≤ γ2 ≤ . . . ≤ γK ≤ 1,integers 0 ≤ n i ≤ Ni , 1 ≤ i ≤ Kfor each asset j : µj = expected return

between n i and Ni assets j satisfy:(1− γi )µj ≤ µj ≤ (1− γi−1)µj∑

j µj ≥ Γ∑

j µj ; Γ > 0 a parameter

For 1 ≤ h ≤ H,

a set (“tier”) Th of assets, and a parameter Γh > 0

for each h,∑

j∈Thµj ≥ Γh

∑j∈Sh

µj

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 18 / 58

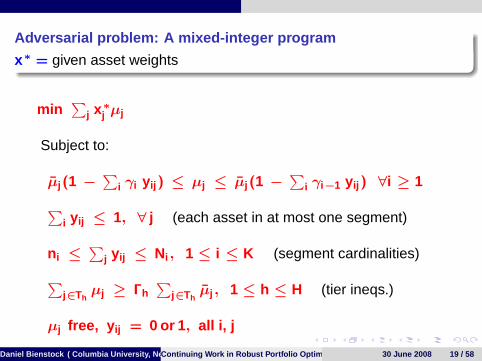

Adversarial problem: A mixed-integer program

x ∗ = given asset weights

min∑

j x ∗j µj

Subject to:

µj (1 −∑

i γi y ij ) ≤ µj ≤ µj (1 −∑

i γi−1 y ij ) ∀i ≥ 1∑i y ij ≤ 1, ∀ j (each asset in at most one segment)

n i ≤∑

j y ij ≤ Ni , 1 ≤ i ≤ K (segment cardinalities)∑j∈Th

µj ≥ Γh∑

j∈Thµj , 1 ≤ h ≤ H (tier ineqs.)

µj free, y ij = 0 or 1 , all i, j

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 19 / 58

Why the adversarial problem is “easy”

( K = no. of segments, H = no. of tiers)

Theorem . For every fixed K and H, and for every ε > 0, there is analgorithm that finds a solution to the adversarial problem with optimalityrelative error ≤ ε, in time polynomial in ε−1 and n (= no. of assets).

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 20 / 58

The simplest case

max∑

j x ∗j δj

Subject to:∑j δj ≤ Γ

0 ≤ δj ≤ u j y j , y j = 0 or 1 , all j∑j y j ≤ N

· · · a cardinality constrained knapsack problemB. (1995), DeFarias and Nemhauser (2004)

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 21 / 58

Summary

At each iteration of the game, we solve:

1 A convex quadratic program – a new constraint added everyiteration

2 A mixed-integer program, always of the same size.

Questions:

How fast (slow?) is each iteration?

How many iterations?

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 22 / 58

Summary

At each iteration of the game, we solve:

1 A convex quadratic program – a new constraint added everyiteration

2 A mixed-integer program, always of the same size.

Questions:

How fast (slow?) is each iteration?

How many iterations?

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 22 / 58

Summary

At each iteration of the game, we solve:

1 A convex quadratic program – a new constraint added everyiteration

2 A mixed-integer program, always of the same size.

Questions:

How fast (slow?) is each iteration?

How many iterations?

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 22 / 58

Summary

At each iteration of the game, we solve:

1 A convex quadratic program – a new constraint added everyiteration

2 A mixed-integer program, always of the same size.

Questions:

How fast (slow?) is each iteration?

How many iterations?

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 22 / 58

Summary

At each iteration of the game, we solve:

1 A convex quadratic program – a new constraint added everyiteration

2 A mixed-integer program, always of the same size.

Questions:

How fast (slow?) is each iteration?

How many iterations?

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 22 / 58

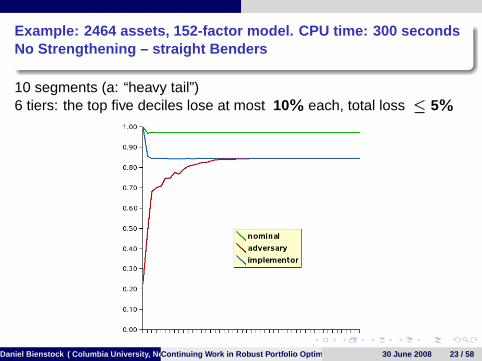

Example: 2464 assets, 152-factor model. CPU time: 300 secondsNo Strengthening – straight Benders

10 segments (a: “heavy tail”)6 tiers: the top five deciles lose at most 10% each, total loss ≤ 5%

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 23 / 58

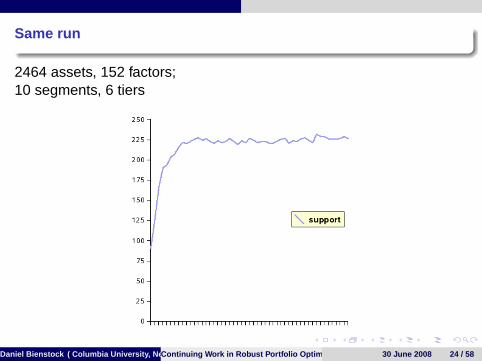

Same run

2464 assets, 152 factors;10 segments, 6 tiers

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 24 / 58

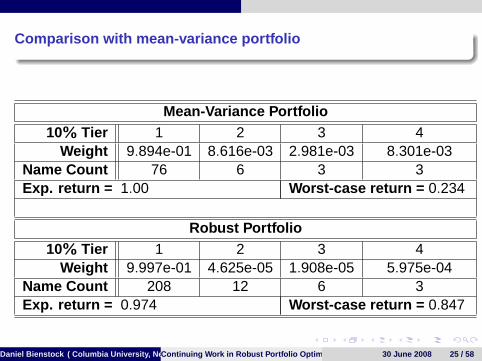

Comparison with mean-variance portfolio

Mean-Variance Portfolio10% Tier 1 2 3 4

Weight 9.894e-01 8.616e-03 2.981e-03 8.301e-03Name Count 76 6 3 3Exp. return = 1.00 Worst-case return = 0.234

Robust Portfolio10% Tier 1 2 3 4

Weight 9.997e-01 4.625e-05 1.908e-05 5.975e-04Name Count 208 12 6 3Exp. return = 0.974 Worst-case return = 0.847

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 25 / 58

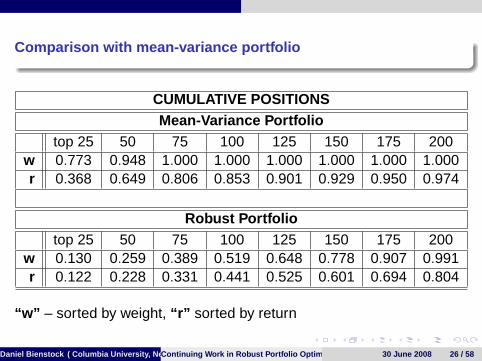

Comparison with mean-variance portfolio

CUMULATIVE POSITIONSMean-Variance Portfolio

top 25 50 75 100 125 150 175 200w 0.773 0.948 1.000 1.000 1.000 1.000 1.000 1.000r 0.368 0.649 0.806 0.853 0.901 0.929 0.950 0.974

Robust Portfoliotop 25 50 75 100 125 150 175 200

w 0.130 0.259 0.389 0.519 0.648 0.778 0.907 0.991r 0.122 0.228 0.331 0.441 0.525 0.601 0.694 0.804

“w” – sorted by weight, “r” sorted by return

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 26 / 58

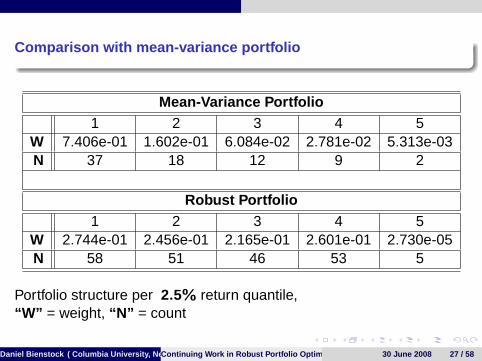

Comparison with mean-variance portfolio

Mean-Variance Portfolio1 2 3 4 5

W 7.406e-01 1.602e-01 6.084e-02 2.781e-02 5.313e-03N 37 18 12 9 2

Robust Portfolio1 2 3 4 5

W 2.744e-01 2.456e-01 2.165e-01 2.601e-01 2.730e-05N 58 51 46 53 5

Portfolio structure per 2.5% return quantile,“W” = weight, “N” = count

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 27 / 58

A popular heuristic

→ Impose the constraint x j ≤ w for all assets j

Here, w is a “small” value

Nomenclature: heuristic portfolio U-w

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 28 / 58

A popular heuristic

→ Impose the constraint x j ≤ w for all assets j

Here, w is a “small” value

Nomenclature: heuristic portfolio U-w

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 28 / 58

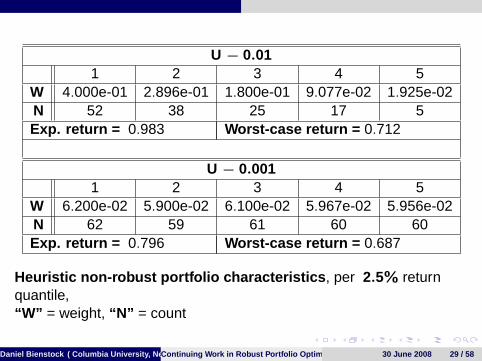

U − 0.011 2 3 4 5

W 4.000e-01 2.896e-01 1.800e-01 9.077e-02 1.925e-02N 52 38 25 17 5Exp. return = 0.983 Worst-case return = 0.712

U − 0.0011 2 3 4 5

W 6.200e-02 5.900e-02 6.100e-02 5.967e-02 5.956e-02N 62 59 61 60 60Exp. return = 0.796 Worst-case return = 0.687

Heuristic non-robust portfolio characteristics , per 2.5% returnquantile,“W” = weight, “N” = count

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 29 / 58

Updated heuristic

→ Impose the constraint x j ≤ w for all assets j in return decile 1

Nomenclature: heuristic portfolio T-w

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 30 / 58

Updated heuristic

→ Impose the constraint x j ≤ w for all assets j in return decile 1

Nomenclature: heuristic portfolio T-w

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 30 / 58

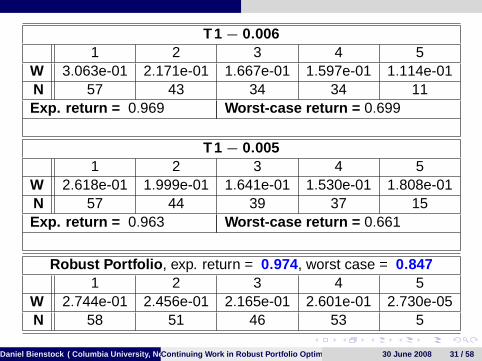

T 1− 0.0061 2 3 4 5

W 3.063e-01 2.171e-01 1.667e-01 1.597e-01 1.114e-01N 57 43 34 34 11Exp. return = 0.969 Worst-case return = 0.699

T 1− 0.0051 2 3 4 5

W 2.618e-01 1.999e-01 1.641e-01 1.530e-01 1.808e-01N 57 44 39 37 15Exp. return = 0.963 Worst-case return = 0.661

Robust Portfolio , exp. return = 0.974, worst case = 0.8471 2 3 4 5

W 2.744e-01 2.456e-01 2.165e-01 2.601e-01 2.730e-05N 58 51 46 53 5

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 31 / 58

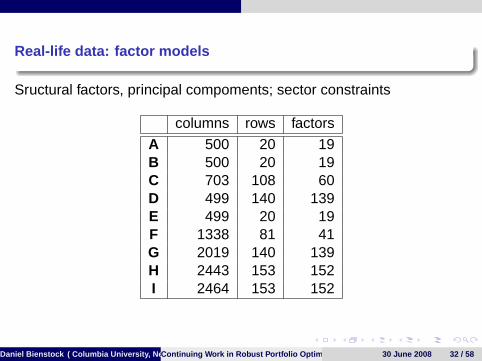

Real-life data: factor models

Sructural factors, principal compoments; sector constraints

columns rows factors

A 500 20 19B 500 20 19C 703 108 60D 499 140 139E 499 20 19F 1338 81 41G 2019 140 139H 2443 153 152I 2464 153 152

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 32 / 58

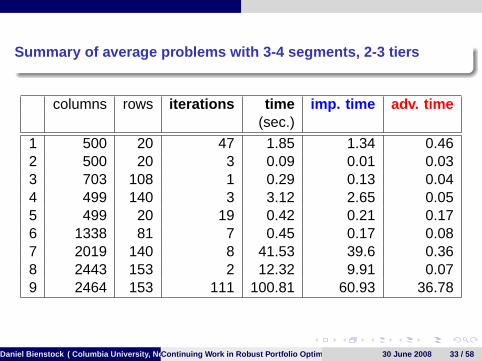

Summary of average problems with 3-4 segments, 2-3 tiers

columns rows iterations time imp. time adv. time(sec.)

1 500 20 47 1.85 1.34 0.462 500 20 3 0.09 0.01 0.033 703 108 1 0.29 0.13 0.044 499 140 3 3.12 2.65 0.055 499 20 19 0.42 0.21 0.176 1338 81 7 0.45 0.17 0.087 2019 140 8 41.53 39.6 0.368 2443 153 2 12.32 9.91 0.079 2464 153 111 100.81 60.93 36.78

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 33 / 58

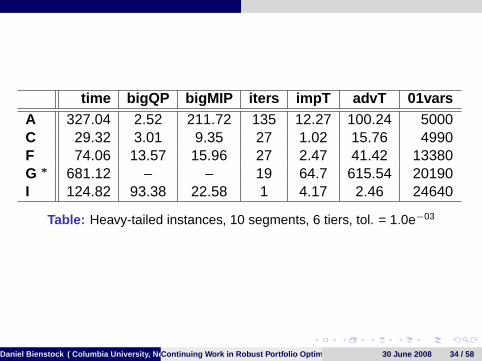

time bigQP bigMIP iters impT advT 01varsA 327.04 2.52 211.72 135 12.27 100.24 5000C 29.32 3.01 9.35 27 1.02 15.76 4990F 74.06 13.57 15.96 27 2.47 41.42 13380G ∗ 681.12 – – 19 64.7 615.54 20190I 124.82 93.38 22.58 1 4.17 2.46 24640

Table: Heavy-tailed instances, 10 segments, 6 tiers, tol. = 1.0e−03

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 34 / 58

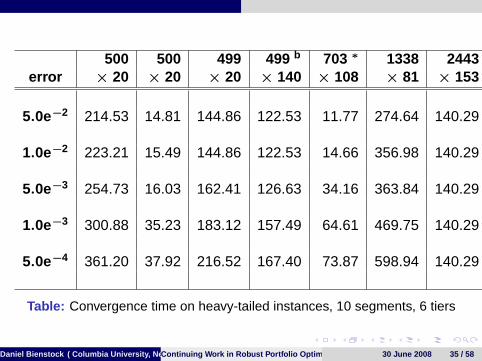

500 500 499 499 b 703 ∗ 1338 2443error × 20 × 20 × 20 × 140 × 108 × 81 × 153

5.0e−2 214.53 14.81 144.86 122.53 11.77 274.64 140.29

1.0e−2 223.21 15.49 144.86 122.53 14.66 356.98 140.29

5.0e−3 254.73 16.03 162.41 126.63 34.16 363.84 140.29

1.0e−3 300.88 35.23 183.12 157.49 64.61 469.75 140.29

5.0e−4 361.20 37.92 216.52 167.40 73.87 598.94 140.29

Table: Convergence time on heavy-tailed instances, 10 segments, 6 tiers

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 35 / 58

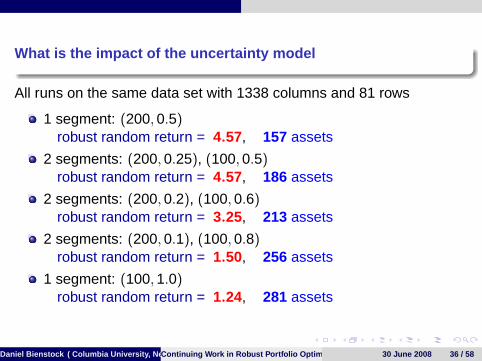

What is the impact of the uncertainty model

All runs on the same data set with 1338 columns and 81 rows

1 segment: (200, 0.5)robust random return = 4.57, 157 assets

2 segments: (200, 0.25), (100, 0.5)robust random return = 4.57, 186 assets

2 segments: (200, 0.2), (100, 0.6)robust random return = 3.25, 213 assets

2 segments: (200, 0.1), (100, 0.8)robust random return = 1.50, 256 assets

1 segment: (100, 1.0)robust random return = 1.24, 281 assets

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 36 / 58

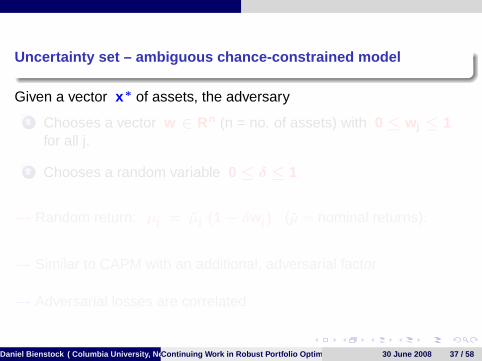

Uncertainty set – ambiguous chance-constrained model

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

→ Similar to CAPM with an additional, adversarial factor

→ Adversarial losses are correlated

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 37 / 58

Uncertainty set – ambiguous chance-constrained model

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

→ Similar to CAPM with an additional, adversarial factor

→ Adversarial losses are correlated

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 37 / 58

Uncertainty set – ambiguous chance-constrained model

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

→ Similar to CAPM with an additional, adversarial factor

→ Adversarial losses are correlated

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 37 / 58

Uncertainty set – ambiguous chance-constrained model

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

→ Similar to CAPM with an additional, adversarial factor

→ Adversarial losses are correlated

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 37 / 58

Uncertainty set – ambiguous chance-constrained model

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

→ Similar to CAPM with an additional, adversarial factor

→ Adversarial losses are correlated

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 37 / 58

Uncertainty set – ambiguous chance-constrained model

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

→ Similar to CAPM with an additional, adversarial factor

→ Adversarial losses are correlated

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 37 / 58

Uncertainty set – ambiguous chance-constrained model

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

Definition (Rockafellar and Uryasev): Given reals ν and 0 ≤ θ ≤ 1the value-at-risk of x∗ is the real ρ ≥ 0 such that

Prob(ν − µT x ∗ ≥ ρ) ≥ θ

→ The adversary wants to maximize VaR

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 38 / 58

Uncertainty set – ambiguous chance-constrained model

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

Definition (Rockafellar and Uryasev): Given reals ν and 0 ≤ θ ≤ 1the value-at-risk of x∗ is the real ρ ≥ 0 such that

Prob(ν − µT x ∗ ≥ ρ) ≥ θ

→ The adversary wants to maximize VaR

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 38 / 58

Uncertainty set – ambiguous chance-constrained model

Given a vector x ∗ of assets, the adversary

1 Chooses a vector w ∈ Rn (n = no. of assets) with 0 ≤ w j ≤ 1for all j.

2 Chooses a random variable 0 ≤ δ ≤ 1

→ Random return: µj = µj (1− δw j ) (µ = nominal returns).

Definition (Rockafellar and Uryasev): Given reals ν and 0 ≤ θ ≤ 1the value-at-risk of x∗ is the real ρ ≥ 0 such that

Prob(ν − µT x ∗ ≥ ρ) ≥ θ

→ The adversary wants to maximize VaR

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 38 / 58

Fleshing out the uncertainty model:

→ Random returnj = µj (1− δw j ) where 0 ≤ w j ≤ 1 ∀ j , and0 ≤ δ ≤ 1 is a random variable.

A discrete distribution:

We are given fixed values 0 = δ0 ≤ δ2 ≤ ... ≤ δK = 1example: δi = i

K

Adversary chooses πi = Prob(δ = δi ), 0 ≤ i ≤ K

The πi are constrained: we have fixed bounds, πli ≤ πi ≤ πu

i(and possibly other constraints)

Tier constraints: for sets (“tiers”) Th of assets, 1 ≤ h ≤ H, werequire:E(δ

∑j∈Th

w j ) ≤ Γh (given)

or, (∑

i δi πi )∑

j∈Thw j ≤ Γh

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 39 / 58

Fleshing out the uncertainty model:

→ Random returnj = µj (1− δw j ) where 0 ≤ w j ≤ 1 ∀ j , and0 ≤ δ ≤ 1 is a random variable.

A discrete distribution:

We are given fixed values 0 = δ0 ≤ δ2 ≤ ... ≤ δK = 1example: δi = i

K

Adversary chooses πi = Prob(δ = δi ), 0 ≤ i ≤ K

The πi are constrained: we have fixed bounds, πli ≤ πi ≤ πu

i(and possibly other constraints)

Tier constraints: for sets (“tiers”) Th of assets, 1 ≤ h ≤ H, werequire:E(δ

∑j∈Th

w j ) ≤ Γh (given)

or, (∑

i δi πi )∑

j∈Thw j ≤ Γh

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 39 / 58

Fleshing out the uncertainty model:

→ Random returnj = µj (1− δw j ) where 0 ≤ w j ≤ 1 ∀ j , and0 ≤ δ ≤ 1 is a random variable.

A discrete distribution:

We are given fixed values 0 = δ0 ≤ δ2 ≤ ... ≤ δK = 1example: δi = i

K

Adversary chooses πi = Prob(δ = δi ), 0 ≤ i ≤ K

The πi are constrained: we have fixed bounds, πli ≤ πi ≤ πu

i(and possibly other constraints)

Tier constraints: for sets (“tiers”) Th of assets, 1 ≤ h ≤ H, werequire:E(δ

∑j∈Th

w j ) ≤ Γh (given)

or, (∑

i δi πi )∑

j∈Thw j ≤ Γh

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 39 / 58

Fleshing out the uncertainty model:

→ Random returnj = µj (1− δw j ) where 0 ≤ w j ≤ 1 ∀ j , and0 ≤ δ ≤ 1 is a random variable.

A discrete distribution:

We are given fixed values 0 = δ0 ≤ δ2 ≤ ... ≤ δK = 1example: δi = i

K

Adversary chooses πi = Prob(δ = δi ), 0 ≤ i ≤ K

The πi are constrained: we have fixed bounds, πli ≤ πi ≤ πu

i(and possibly other constraints)

Tier constraints: for sets (“tiers”) Th of assets, 1 ≤ h ≤ H, werequire:E(δ

∑j∈Th

w j ) ≤ Γh (given)

or, (∑

i δi πi )∑

j∈Thw j ≤ Γh

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 39 / 58

Fleshing out the uncertainty model:

→ Random returnj = µj (1− δw j ) where 0 ≤ w j ≤ 1 ∀ j , and0 ≤ δ ≤ 1 is a random variable.

A discrete distribution:

We are given fixed values 0 = δ0 ≤ δ2 ≤ ... ≤ δK = 1example: δi = i

K

Adversary chooses πi = Prob(δ = δi ), 0 ≤ i ≤ K

The πi are constrained: we have fixed bounds, πli ≤ πi ≤ πu

i(and possibly other constraints)

Tier constraints: for sets (“tiers”) Th of assets, 1 ≤ h ≤ H, werequire:E(δ

∑j∈Th

w j ) ≤ Γh (given)

or, (∑

i δi πi )∑

j∈Thw j ≤ Γh

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 39 / 58

Fleshing out the uncertainty model:

→ Random returnj = µj (1− δw j ) where 0 ≤ w j ≤ 1 ∀ j , and0 ≤ δ ≤ 1 is a random variable.

A discrete distribution:

We are given fixed values 0 = δ0 ≤ δ2 ≤ ... ≤ δK = 1example: δi = i

K

Adversary chooses πi = Prob(δ = δi ), 0 ≤ i ≤ K

The πi are constrained: we have fixed bounds, πli ≤ πi ≤ πu

i(and possibly other constraints)

Tier constraints: for sets (“tiers”) Th of assets, 1 ≤ h ≤ H, werequire:E(δ

∑j∈Th

w j ) ≤ Γh (given)

or, (∑

i δi πi )∑

j∈Thw j ≤ Γh

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 39 / 58

Fleshing out the uncertainty model:

→ Random returnj = µj (1− δw j ) where 0 ≤ w j ≤ 1 ∀ j , and0 ≤ δ ≤ 1 is a random variable.

A discrete distribution:

We are given fixed values 0 = δ0 ≤ δ2 ≤ ... ≤ δK = 1example: δi = i

K

Adversary chooses πi = Prob(δ = δi ), 0 ≤ i ≤ K

The πi are constrained: we have fixed bounds, πli ≤ πi ≤ πu

i(and possibly other constraints)

Tier constraints: for sets (“tiers”) Th of assets, 1 ≤ h ≤ H, werequire:E(δ

∑j∈Th

w j ) ≤ Γh (given)

or, (∑

i δi πi )∑

j∈Thw j ≤ Γh

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 39 / 58

Robust optimization problem (VaR case):Given 0 < ε,

min V

Subject to:

λx T Qx − µT x ≤ v ∗ + ε

Ax ≥ b

V ≥ VaRmax (x )

Here, v ∗ .= min λx T Qx − µT x

Subject to:

Ax ≥ b

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 40 / 58

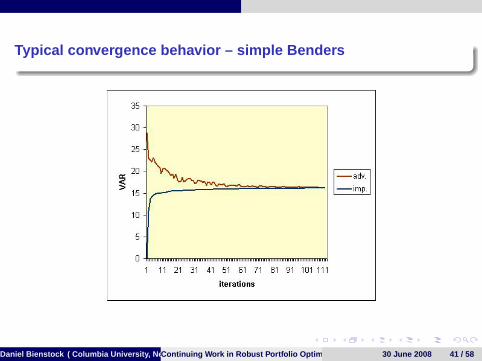

Typical convergence behavior – simple Benders

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 41 / 58

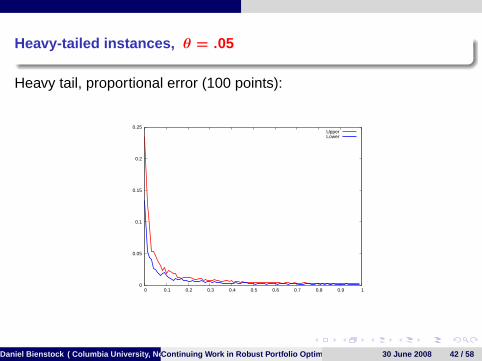

Heavy-tailed instances, θ = .05

Heavy tail, proportional error (100 points):

0

0.05

0.1

0.15

0.2

0.25

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

UpperLower

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 42 / 58

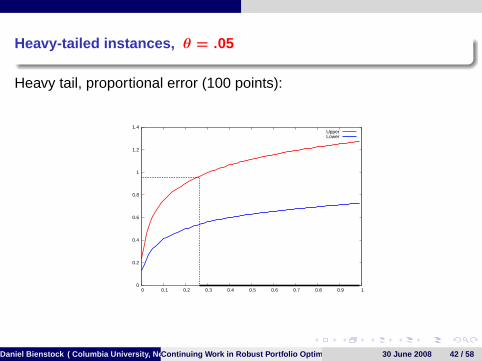

Heavy-tailed instances, θ = .05

Heavy tail, proportional error (100 points):

0

0.2

0.4

0.6

0.8

1

1.2

1.4

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

UpperLower

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 42 / 58

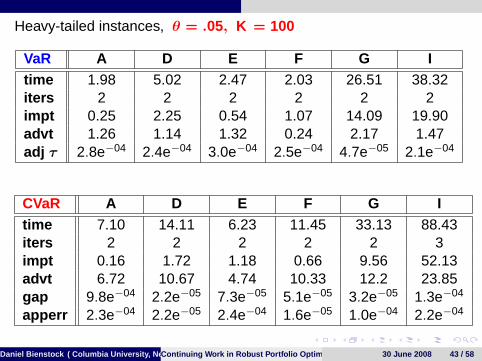

Heavy-tailed instances, θ = .05, K = 100

VaR A D E F G Itime 1.98 5.02 2.47 2.03 26.51 38.32iters 2 2 2 2 2 2impt 0.25 2.25 0.54 1.07 14.09 19.90advt 1.26 1.14 1.32 0.24 2.17 1.47adj τ 2.8e−04 2.4e−04 3.0e−04 2.5e−04 4.7e−05 2.1e−04

CVaR A D E F G Itime 7.10 14.11 6.23 11.45 33.13 88.43iters 2 2 2 2 2 3impt 0.16 1.72 1.18 0.66 9.56 52.13advt 6.72 10.67 4.74 10.33 12.2 23.85gap 9.8e−04 2.2e−05 7.3e−05 5.1e−05 3.2e−05 1.3e−04

apperr 2.3e−04 2.2e−05 2.4e−04 1.6e−05 1.0e−04 2.2e−04

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 43 / 58

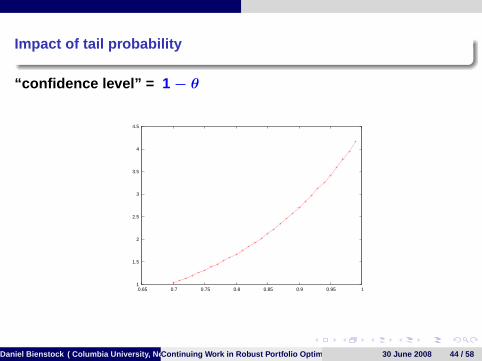

Impact of tail probability

“confidence level” = 1− θ

1

1.5

2

2.5

3

3.5

4

4.5

0.65 0.7 0.75 0.8 0.85 0.9 0.95 1

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 44 / 58

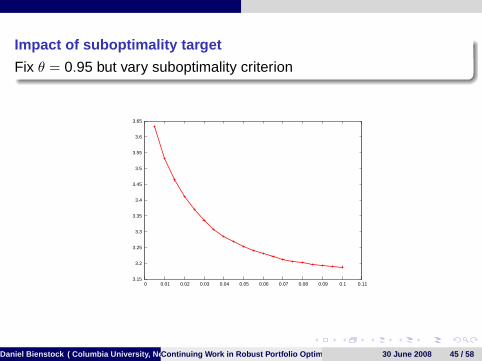

Impact of suboptimality target

Fix θ = 0.95 but vary suboptimality criterion

3.15

3.2

3.25

3.3

3.35

3.4

3.45

3.5

3.55

3.6

3.65

0 0.01 0.02 0.03 0.04 0.05 0.06 0.07 0.08 0.09 0.1 0.11

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 45 / 58

Experiment: sensitivity of model to parameters

Adversary chooses πi = P(δ = δi ), πli ≤ πi ≤ πu

i

Experiment: choose ∆ ≥ 0, and solve robust problems for

πli ← max{πl

i −∆, 0}, πui ← πu

i + ∆

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 46 / 58

Experiment: sensitivity of model to parameters

Adversary chooses πi = P(δ = δi ), πli ≤ πi ≤ πu

i

Experiment: choose ∆ ≥ 0, and solve robust problems for

πli ← max{πl

i −∆, 0}, πui ← πu

i + ∆

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 46 / 58

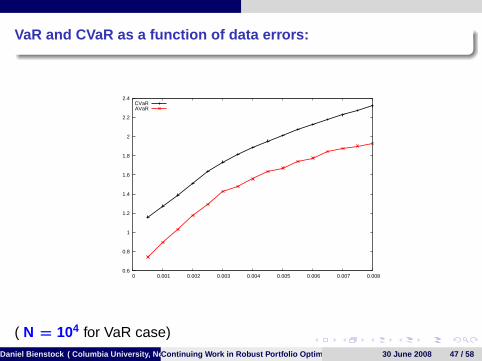

VaR and CVaR as a function of data errors:

0.6

0.8

1

1.2

1.4

1.6

1.8

2

2.2

2.4

0 0.001 0.002 0.003 0.004 0.005 0.006 0.007 0.008

CVaRAVaR

( N = 104 for VaR case)Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 47 / 58

Part II: Methodology

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 48 / 58

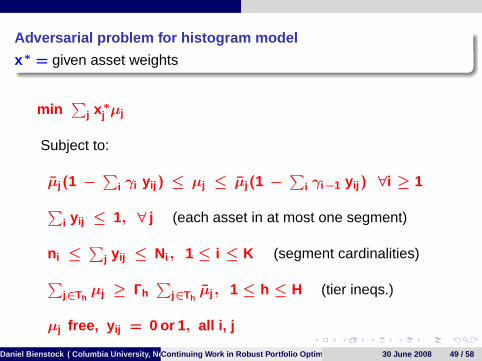

Adversarial problem for histogram model

x ∗ = given asset weights

min∑

j x ∗j µj

Subject to:

µj (1 −∑

i γi y ij ) ≤ µj ≤ µj (1 −∑

i γi−1 y ij ) ∀i ≥ 1∑i y ij ≤ 1, ∀ j (each asset in at most one segment)

n i ≤∑

j y ij ≤ Ni , 1 ≤ i ≤ K (segment cardinalities)∑j∈Th

µj ≥ Γh∑

j∈Thµj , 1 ≤ h ≤ H (tier ineqs.)

µj free, y ij = 0 or 1 , all i, j

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 49 / 58

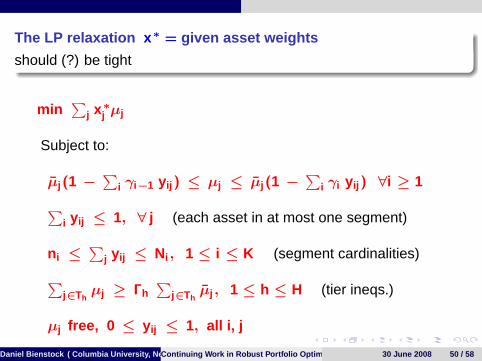

The LP relaxation x ∗ = given asset weights

should (?) be tight

min∑

j x ∗j µj

Subject to:

µj (1 −∑

i γi−1 y ij ) ≤ µj ≤ µj (1 −∑

i γi y ij ) ∀i ≥ 1∑i y ij ≤ 1, ∀ j (each asset in at most one segment)

n i ≤∑

j y ij ≤ Ni , 1 ≤ i ≤ K (segment cardinalities)∑j∈Th

µj ≥ Γh∑

j∈Thµj , 1 ≤ h ≤ H (tier ineqs.)

µj free, 0 ≤ y ij ≤ 1, all i, j

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 50 / 58

Robust problem:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ µT x , ∀ µ achievable by adversary

Robust problem for relaxed adversary:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ µT x , ∀ µ achievable by relaxed adversary

V ∗ ≥ V , perhaps V ∗ ≈ V ,

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 51 / 58

Robust problem:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ µT x , ∀ µ achievable by adversary

Robust problem for relaxed adversary:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ µT x , ∀ µ achievable by relaxed adversary

V ∗ ≥ V , perhaps V ∗ ≈ V ,

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 51 / 58

Robust problem:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ µT x , ∀ µ achievable by adversary

Robust problem for relaxed adversary:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ µT x , ∀ µ achievable by relaxed adversary

V ∗ ≥ V , perhaps V ∗ ≈ V ,

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 51 / 58

Robust problem for relaxed adversary:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ µT x , ∀ µ achievable by relaxed adversary

or , V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ minimum return(x)

but, minimum return(x) = min∑

j x ∗j µj

Subject to: M1µ + M2y ≥ Ψ

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 52 / 58

Robust problem for relaxed adversary:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ µT x , ∀ µ achievable by relaxed adversary

or , V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ minimum return(x)

but, minimum return(x) = min∑

j x ∗j µj

Subject to: M1µ + M2y ≥ Ψ

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 52 / 58

Robust problem for relaxed adversary:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ µT x , ∀ µ achievable by relaxed adversary

or , V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ minimum return(x)

but, minimum return(x) = min∑

j x ∗j µj

Subject to: M1µ + M2y ≥ Ψ

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 52 / 58

Robust problem for relaxed adversary:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ µT x , ∀ µ achievable by relaxed adversary

or , V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ minimum return(x)

duality: minimum return(x) = max ΨT α

Subject to: MT1 α = x , MT

2 α = 0, α ≥ 0

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 53 / 58

Robust problem for relaxed adversary:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ minimum return(x)

Robust problem:

min λx T Qx − rSubject to:Ax ≥ b

r − ΨT α ≤ 0

MT1 α − x = 0, MT

2 α = 0, α ≥ 0Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 54 / 58

Robust problem for relaxed adversary:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ minimum return(x)

Robust problem:

min λx T Qx − rSubject to:Ax ≥ b

r − ΨT α ≤ 0

MT1 α − x = 0, MT

2 α = 0, α ≥ 0Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 54 / 58

Robust problem for relaxed adversary:

V.= min λx T Qx − r

Subject to: Ax ≥ br ≤ minimum return(x)

Robust problem:

min λx T Qx − rSubject to:Ax ≥ b

r − ΨT α ≤ 0

MT1 α − x = 0, MT

2 α = 0, α ≥ 0Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 54 / 58

Robust problem for relaxed adversary:

V ∗ .= min λx T Qx − r

Subject to: Ax ≥ br − ΨT α ≤ 0

(∗∗) MT1 α − x = 0

MT2 α = 0, α ≥ 0

Let µ = optimal duals for (**)

V ∗ = min λx T Qx − rSubject to: Ax ≥ br − µT x ≤ 0

( r − µT x ≤ 0, ∀µ available to strict adversary)

Problem: Find µ available to strict adversary, and with µ ≈ µ

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 55 / 58

Robust problem for relaxed adversary:

V ∗ .= min λx T Qx − r

Subject to: Ax ≥ br − ΨT α ≤ 0

(∗∗) MT1 α − x = 0

MT2 α = 0, α ≥ 0

Let µ = optimal duals for (**)

V ∗ = min λx T Qx − rSubject to: Ax ≥ br − µT x ≤ 0

( r − µT x ≤ 0, ∀µ available to strict adversary)

Problem: Find µ available to strict adversary, and with µ ≈ µ

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 55 / 58

Robust problem for relaxed adversary:

V ∗ .= min λx T Qx − r

Subject to: Ax ≥ br − ΨT α ≤ 0

(∗∗) MT1 α − x = 0

MT2 α = 0, α ≥ 0

Let µ = optimal duals for (**)

V ∗ = min λx T Qx − rSubject to: Ax ≥ br − µT x ≤ 0

( r − µT x ≤ 0, ∀µ available to strict adversary)

Problem: Find µ available to strict adversary, and with µ ≈ µ

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 55 / 58

Robust problem for relaxed adversary:

V ∗ .= min λx T Qx − r

Subject to: Ax ≥ br − ΨT α ≤ 0

(∗∗) MT1 α − x = 0

MT2 α = 0, α ≥ 0

Let µ = optimal duals for (**)

V ∗ = min λx T Qx − rSubject to: Ax ≥ br − µT x ≤ 0

( r − µT x ≤ 0, ∀µ available to strict adversary)

Problem: Find µ available to strict adversary, and with µ ≈ µ

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 55 / 58

Robust problem for relaxed adversary:

V ∗ .= min λx T Qx − r

Subject to: Ax ≥ br − ΨT α ≤ 0

(∗∗) MT1 α − x = 0

MT2 α = 0, α ≥ 0

Let µ = optimal duals for (**)

V ∗ = min λx T Qx − rSubject to: Ax ≥ br − µT x ≤ 0

( r − µT x ≤ 0, ∀µ available to strict adversary)

Problem: Find µ available to strict adversary, and with µ ≈ µ

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 55 / 58

Benders’ algorithm with strengthening

Step 1. Solve relaxed robust problem; answer = µ

Step 2. Solve MIP to obtain vector µ which is legal for histogrammodel, and with µ ≈ µ

Step 3. Run Benders beginning with the cut r − µT x ≤ 0

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 56 / 58

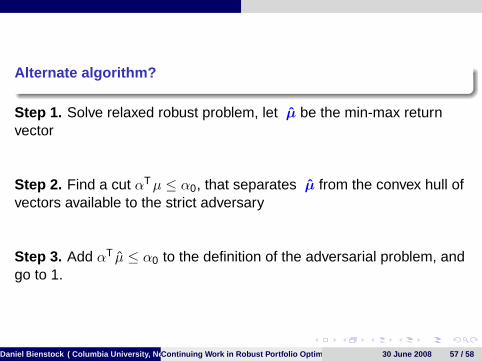

Alternate algorithm?

Step 1. Solve relaxed robust problem, let µ be the min-max returnvector

Step 2. Find a cut αT µ ≤ α0, that separates µ from the convex hull ofvectors available to the strict adversary

Step 3. Add αT µ ≤ α0 to the definition of the adversarial problem, andgo to 1.

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 57 / 58

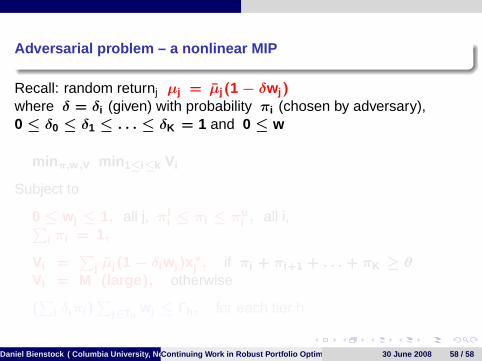

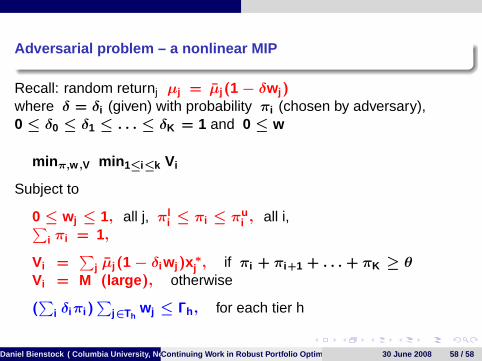

Adversarial problem – a nonlinear MIP

Recall: random returnj µj = µj (1− δw j )where δ = δi (given) with probability πi (chosen by adversary),0 ≤ δ0 ≤ δ1 ≤ . . . ≤ δK = 1 and 0 ≤ w

min π,w ,V min 1≤i≤k Vi

Subject to

0 ≤ w j ≤ 1, all j, πli ≤ πi ≤ πu

i , all i,∑i πi = 1,

Vi =∑

j µj (1− δi w j )x ∗j , if πi + πi+1 + . . . + πK ≥ θ

Vi = M (large ), otherwise

(∑

i δi πi )∑

j∈Thw j ≤ Γh , for each tier h

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 58 / 58

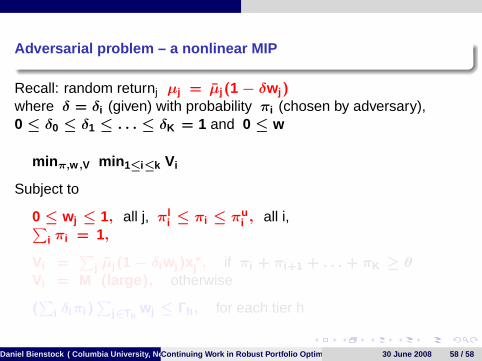

Adversarial problem – a nonlinear MIP

Recall: random returnj µj = µj (1− δw j )where δ = δi (given) with probability πi (chosen by adversary),0 ≤ δ0 ≤ δ1 ≤ . . . ≤ δK = 1 and 0 ≤ w

min π,w ,V min 1≤i≤k Vi

Subject to

0 ≤ w j ≤ 1, all j, πli ≤ πi ≤ πu

i , all i,∑i πi = 1,

Vi =∑

j µj (1− δi w j )x ∗j , if πi + πi+1 + . . . + πK ≥ θ

Vi = M (large ), otherwise

(∑

i δi πi )∑

j∈Thw j ≤ Γh , for each tier h

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 58 / 58

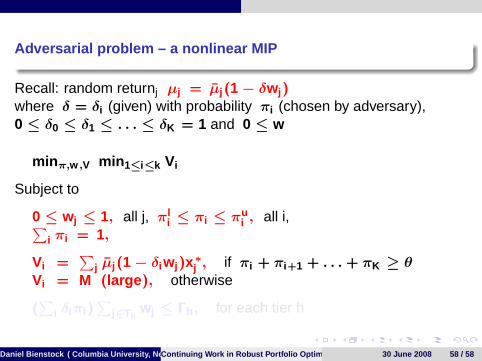

Adversarial problem – a nonlinear MIP

Recall: random returnj µj = µj (1− δw j )where δ = δi (given) with probability πi (chosen by adversary),0 ≤ δ0 ≤ δ1 ≤ . . . ≤ δK = 1 and 0 ≤ w

min π,w ,V min 1≤i≤k Vi

Subject to

0 ≤ w j ≤ 1, all j, πli ≤ πi ≤ πu

i , all i,∑i πi = 1,

Vi =∑

j µj (1− δi w j )x ∗j , if πi + πi+1 + . . . + πK ≥ θ

Vi = M (large ), otherwise

(∑

i δi πi )∑

j∈Thw j ≤ Γh , for each tier h

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 58 / 58

Adversarial problem – a nonlinear MIP

Recall: random returnj µj = µj (1− δw j )where δ = δi (given) with probability πi (chosen by adversary),0 ≤ δ0 ≤ δ1 ≤ . . . ≤ δK = 1 and 0 ≤ w

min π,w ,V min 1≤i≤k Vi

Subject to

0 ≤ w j ≤ 1, all j, πli ≤ πi ≤ πu

i , all i,∑i πi = 1,

Vi =∑

j µj (1− δi w j )x ∗j , if πi + πi+1 + . . . + πK ≥ θ

Vi = M (large ), otherwise

(∑

i δi πi )∑

j∈Thw j ≤ Γh , for each tier h

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 58 / 58

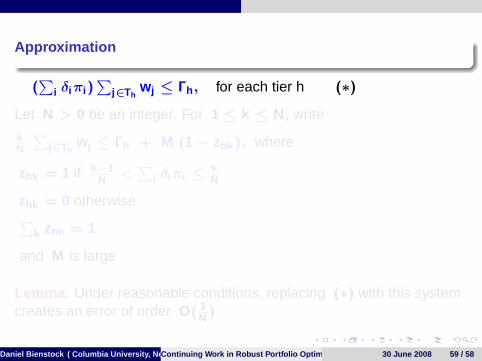

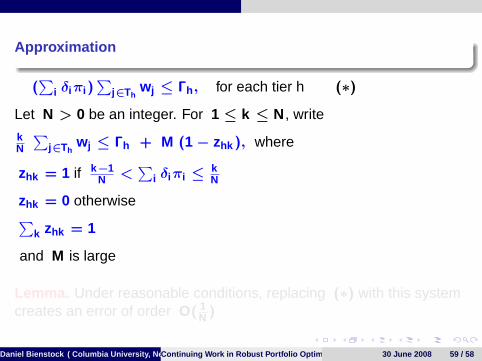

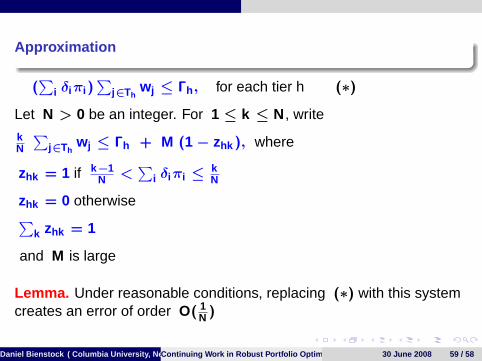

Approximation

(∑

i δi πi )∑

j∈Thw j ≤ Γh , for each tier h (∗)

Let N > 0 be an integer. For 1 ≤ k ≤ N , write

kN

∑j∈Th

w j ≤ Γh + M (1− zhk ), where

zhk = 1 if k −1N <

∑i δi πi ≤ k

N

zhk = 0 otherwise∑k zhk = 1

and M is large

Lemma. Under reasonable conditions, replacing (∗) with this systemcreates an error of order O( 1

N )

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 59 / 58

Approximation

(∑

i δi πi )∑

j∈Thw j ≤ Γh , for each tier h (∗)

Let N > 0 be an integer. For 1 ≤ k ≤ N , write

kN

∑j∈Th

w j ≤ Γh + M (1− zhk ), where

zhk = 1 if k −1N <

∑i δi πi ≤ k

N

zhk = 0 otherwise∑k zhk = 1

and M is large

Lemma. Under reasonable conditions, replacing (∗) with this systemcreates an error of order O( 1

N )

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 59 / 58

Approximation

(∑

i δi πi )∑

j∈Thw j ≤ Γh , for each tier h (∗)

Let N > 0 be an integer. For 1 ≤ k ≤ N , write

kN

∑j∈Th

w j ≤ Γh + M (1− zhk ), where

zhk = 1 if k −1N <

∑i δi πi ≤ k

N

zhk = 0 otherwise∑k zhk = 1

and M is large

Lemma. Under reasonable conditions, replacing (∗) with this systemcreates an error of order O( 1

N )

Daniel Bienstock ( Columbia University, New York)Continuing Work in Robust Portfolio Optimization 30 June 2008 59 / 58