CHAPTER 10: ESTIMATION AND HYPOTHESIS TESTING: TWO POPULATIONS.

RS – Chapter 2 – Random Variables 8/14/2019

1

Chapter 2

Random Variables

Random Variables

• A random variable is a convenient way to express the elements of Ω as numbers rather than abstract elements of sets.

Definition: Let AX; AY be nonempty families of subsets of X and Y, respectively. A function f: X → Y is (AX;AY )-measurable if f -1

A ∈ AX for all A ∈ AY.

Definition: Random Variable•A random variable X is a measurable function from the probability space (Ω, Σ ,P) into the probability space (χ, AX, PX), where χ in R is the range of X (which is a subset of the real line) AX is a Borel field of X, and PX is the probability measure on χ induced by X.Specifically, X: Ω→ χ.

RS – Chapter 2 – Random Variables 8/14/2019

2

Remarks:

- A random variable X is a function.

- It is a numerical quantity whose value is determined by a random experiment.

- It takes single elements in Ω and maps them to single points in R.

- P is the probability measure over the sample space and PX is the probability measure over the range of the random variable.

- The induced measure PX is just a way of relating measure on the real line –the range of X– back to the original probability measure over the abstract events in the σ-algebra of the sample space.

Random Variables - Remarks

Interpretation

The induced measure PX allows us to relate a measure on the real line –the range of X– back to the original probability measure over the abstract events in the σ-algebra of the sample space:

PX[A] = P [X-1(A)] =P[ω∈ Ω: X(ω) ∈ A.

That is, we take the probability weights associated with events and assign them to real numbers. Recall that when we deal with probabilities on some random variable X, we are really dealing with the PX measure.

We measure the "size" of the set (using P as our measure) of ω's such that the random variable X returns values in A.

Random Variables - Interpretation

RS – Chapter 2 – Random Variables 8/14/2019

3

Interpretation

P is the probability measure over the sample space and PX is the probability measure over the range of the random variable.

Thus, we write P[A] (where A is a subset of the range of X) but we

mean PX[A], which is equivalent to P[ω∈ Ω: X(ω) ∈ A].

Notational shortcut: We use P[A] instead of PX [A]

(This notation can be misleading if there's confusion about whether A is in the sample space or in the range of X.)

Random Variables - Interpretation

Example: Back to the previous example where two coins are tossed. We defined the sample space (Ω) as all possible outcomes and the sigma algebra of all possible subsets of the sample space. A simple probability measure (P) was applied to the events in the sigma algebra.

Let the random variable X be "number of heads." Recall that X

takes Ω into χ and induces PX from P. In this example, χ = 0; 1; 2 and A = Φ; 0; 1; 2; 0;1; 0;2; 1;2; 0;1;2.

The induced probability measure PX from the measure defined above would look like:

Random Variables – Example 1

RS – Chapter 2 – Random Variables 8/14/2019

4

Example: Back to the previous example where two coins are tossed.

Prob. of 0 heads = PX[0] = P[TT] = 1/4

Prob. of 1 heads = PX[1] = P[HT; TH] = 1/2

Prob. of 2 heads = PX[2] = P[HH] = ¼

Prob. of 0 or 1 heads = PX[0; 1] = P[TT; TH; HT] = 3/4

Prob. of 0 or 2 heads = PX[0; 2] = P[TT; HH] = 1/2

Prob. of 1 or 2 heads = PX[1; 2] = P[TH; HT; HH] = 3/4

Prob. of 1, 2, or 3 heads = PX[0; 1; 2] = P[HH; TH; HT; TT] = 1

Prob. of "nothing" = PX[Φ] = P[Φ] = 0

The empty set is simply needed to complete the σ-algebra. Its interpretation is not important since P[Φ] = 0 for any reasonable P.

Random Variables – Example 1

Example: Probability Space

One standard probability space is the Borel field over the unit interval of the real line under the Lebesgue measure λ. That is ([0, 1]; B; λ).

The Borel field over the unit interval gives us a set of all possible intervals taken from [0,1]. The Lebesgue measure measures the size of any given interval. For any interval [a; b] in [0,1] with b ≥ a,

λ[[a, b]] = b – a.

This probability space is well known: “uniform distribution,” the probability of any interval of values is the size of the interval.

Random Variables – Example 2

RS – Chapter 2 – Random Variables 8/14/2019

5

1. Two dice are rolled and X is the sum of the two upward faces.

2. A coin is tossed n = 3 times and X is the number of times that a head occurs.

3. A point is selected at random from a square whose sides are of length 1. X is the distance of the point from the lower left hand corner.

4. X is the number of times the price of IBM increases during a time interval, say a day.

5. Today, the DJ Index is 19,504.17, X is the value of the index in thirty days.

point

X

Random Variables – More Examples

Ω is the sample space –the set of possible outcomes from an experiment.

– An event A is a set containing outcomes from the sample space.

• Σ is a σ -algebra of subsets of the sample space. Think of Σ as the collection of all possible events involving outcomes chosen from Ω.

• P is a probability measure over Σ. P assigns a number between [0,1]

to each event in Σ.

• We have functions (random variables) that allow us to look at real

numbers instead of abstract events in Σ.

Random Variables: Summary

RS – Chapter 2 – Random Variables 8/14/2019

6

• For each random variable X, there exists a new probability measure

PX: PX [A] where A ∈ R simply relates back to P[ω∈ Ω: X(ω) ∈A.

We calculate PX[A], but we are really interested in the probability

P[ω∈ Ω: X(ω) ∈ A,

where A simply represents ω∈ Ω: X(ω) ∈ A through the inverse transformation X-1.

Random Variables: Summary

Definition – The probability function, p(x), of a RV, X.For any random variable, X, and any real number, x, we define

where X = x = the set of all outcomes (event) with X = x.

p x P X x P X x

Definition – The cumulative distribution function (CDF), F(x), of a RV, X.For any random variable, X, and any real number, x, we define

where X ≤ x = the set of all outcomes (event) with X ≤ x.

F x P X x P X x

Random Variables: Probability Function & CDF

RS – Chapter 2 – Random Variables 8/14/2019

7

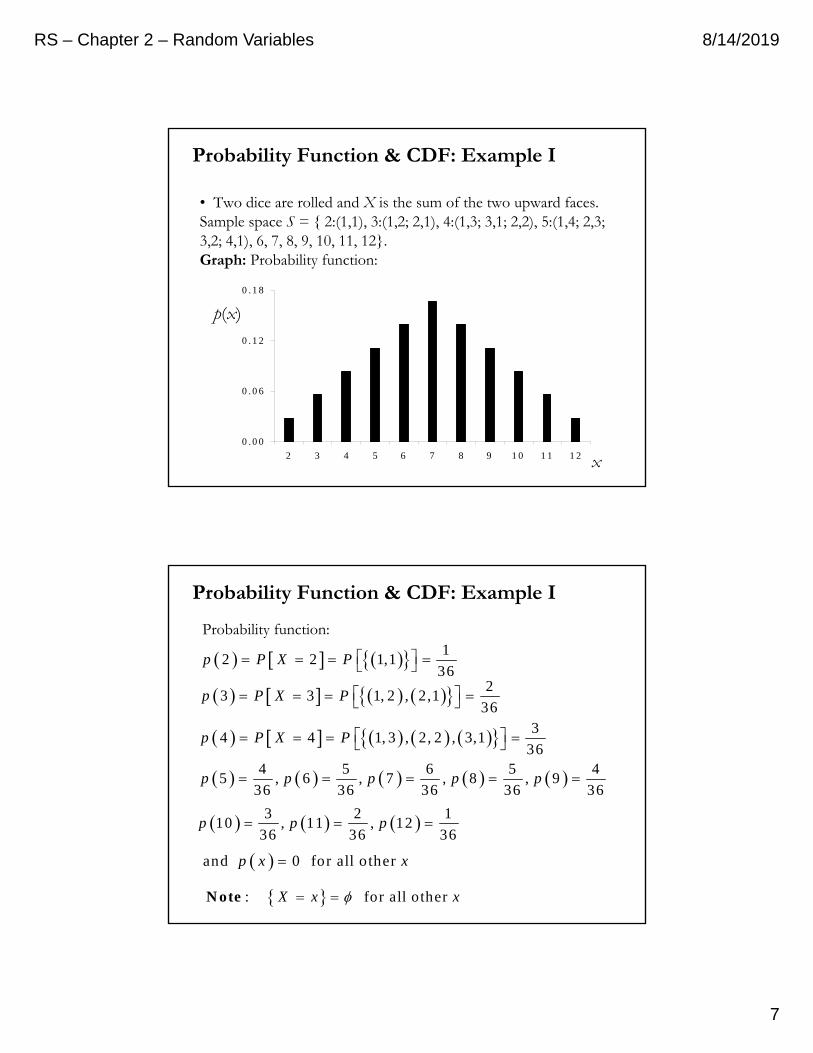

• Two dice are rolled and X is the sum of the two upward faces. Sample space S = 2:(1,1), 3:(1,2; 2,1), 4:(1,3; 3,1; 2,2), 5:(1,4; 2,3; 3,2; 4,1), 6, 7, 8, 9, 10, 11, 12.Graph: Probability function:

0 . 0 0

0 . 0 6

0 . 1 2

0 . 1 8

2 3 4 5 6 7 8 9 1 0 1 1 1 2 x

p(x)

Probability Function & CDF: Example I

12 2 1,1

36p P X P

23 3 1, 2 , 2,1

36p P X P

34 4 1, 3 , 2, 2 , 3,1

36p P X P

4 5 6 5 45 , 6 , 7 , 8 , 9

36 36 36 36 36p p p p p

3 2 110 , 11 , 12

36 36 36p p p

and 0 for all other p x x

: for all other X x x N ote

Probability function:

Probability Function & CDF: Example I

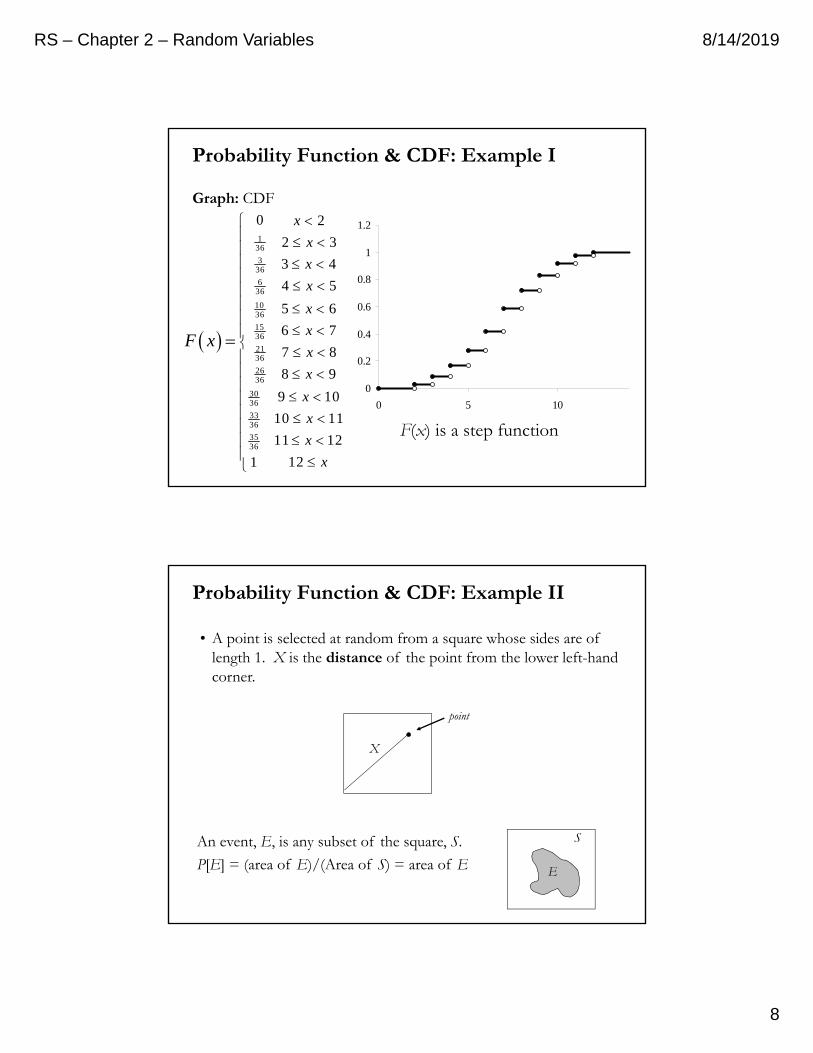

RS – Chapter 2 – Random Variables 8/14/2019

8

0

0.2

0.4

0.6

0.8

1

1.2

0 5 10

Graph: CDF

F x

136

336

636

1036

1536

2136

2636

3036

3336

3536

0 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

121

x

x

x

x

x

x

x

x

x

x

x

x

F(x) is a step function

Probability Function & CDF: Example I

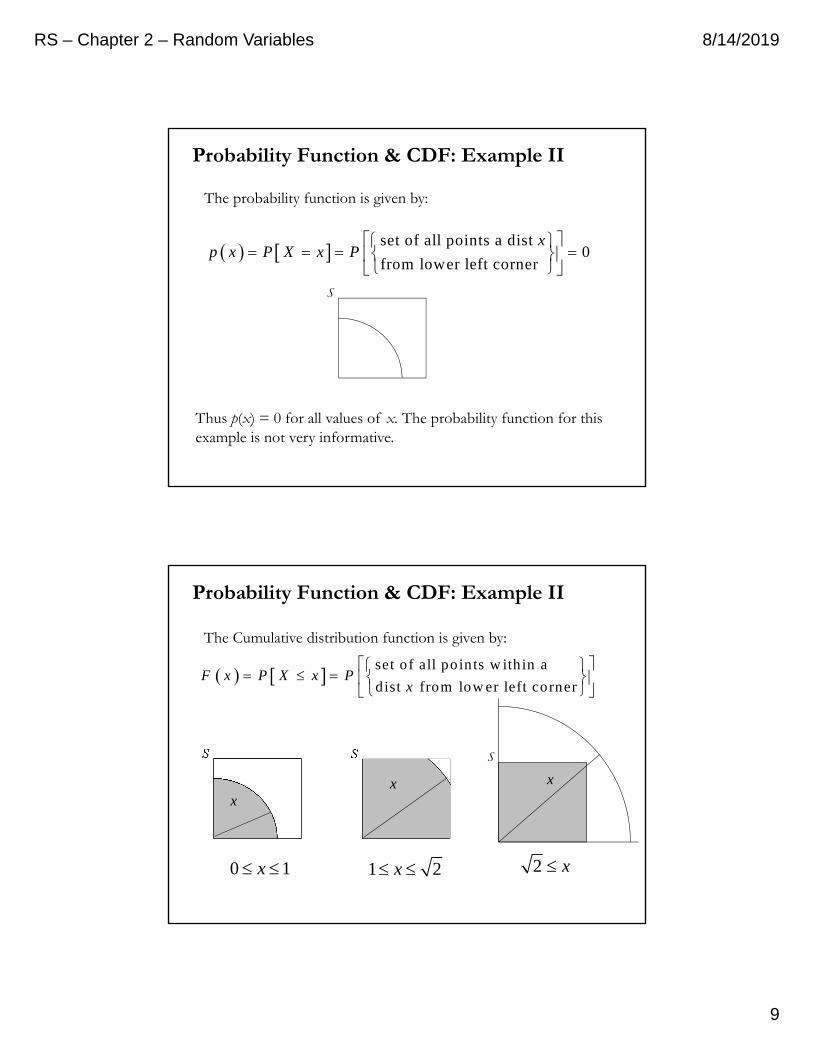

• A point is selected at random from a square whose sides are of length 1. X is the distance of the point from the lower left-hand corner.

An event, E, is any subset of the square, S.

P[E] = (area of E)/(Area of S) = area of E

point

X

S

E

Probability Function & CDF: Example II

RS – Chapter 2 – Random Variables 8/14/2019

9

Thus p(x) = 0 for all values of x. The probability function for this example is not very informative.

set of all points a dist 0

from lower left corner

xp x P X x P

S

The probability function is given by:

Probability Function & CDF: Example II

set of all poin ts w ith in a

d ist from low er left cornerF x P X x P

x

The Cumulative distribution function is given by:

S

0 1x 1 2x 2 x

xx x

Probability Function & CDF: Example II

RS – Chapter 2 – Random Variables 8/14/2019

10

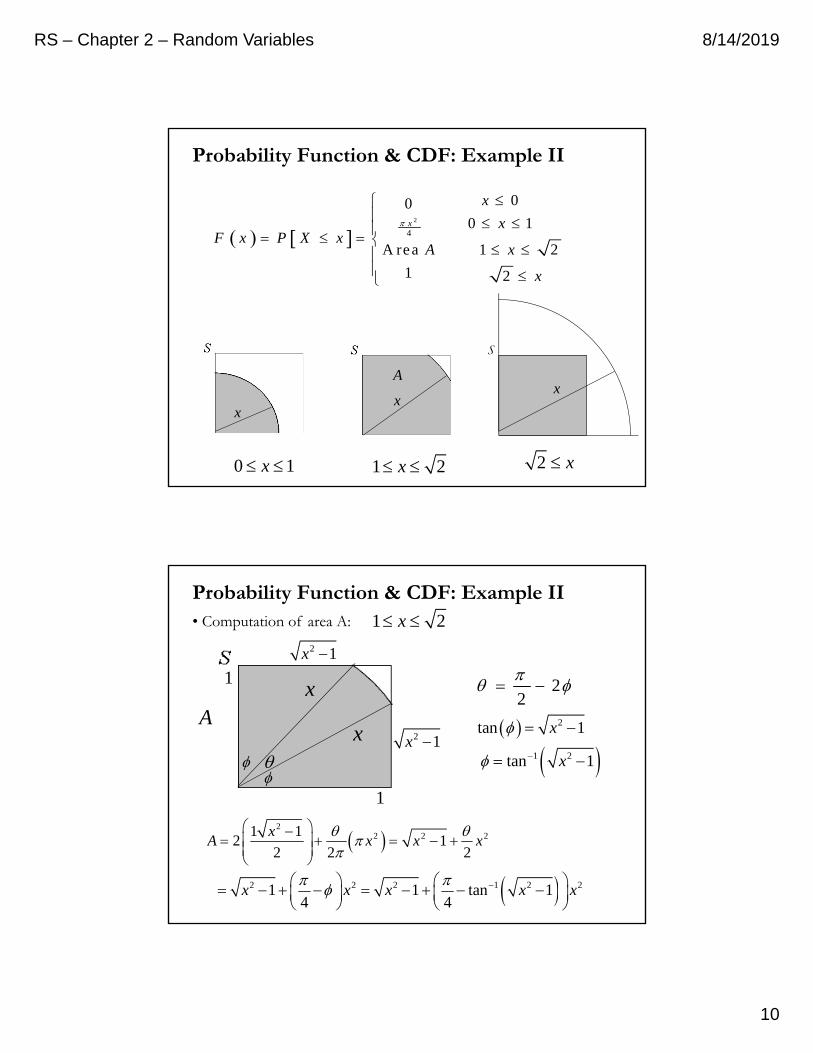

2

4

000 1

A rea 1 2

1 2

x

x

xF x P X x

A x

x

S

0 1x 1 2x 2 x

xx

xA

Probability Function & CDF: Example II

1 2x

xA

x1

22

2 1x

2 1x

2

2 2 21 12 1

2 2 2

xA x x x

2 2 2 1 2 21 1 tan 14 4

x x x x x

2tan 1x

1 2tan 1x

1

Probability Function & CDF: Example II

• Computation of area A:

RS – Chapter 2 – Random Variables 8/14/2019

11

0

1

-1 0 1 2

2

2 1 2 2

0 0

0 14

1 tan 1 1 24

1 2

x

xx

F x P X xx x x x

x

F x

Probability Function & CDF: Example II

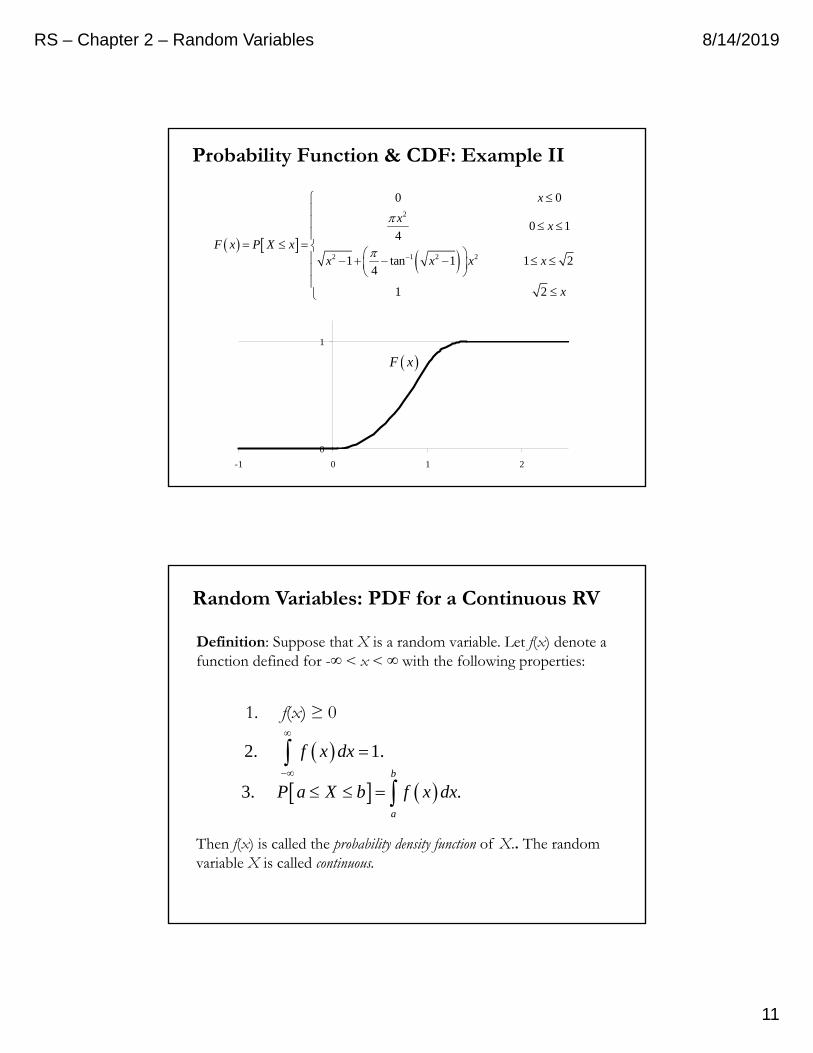

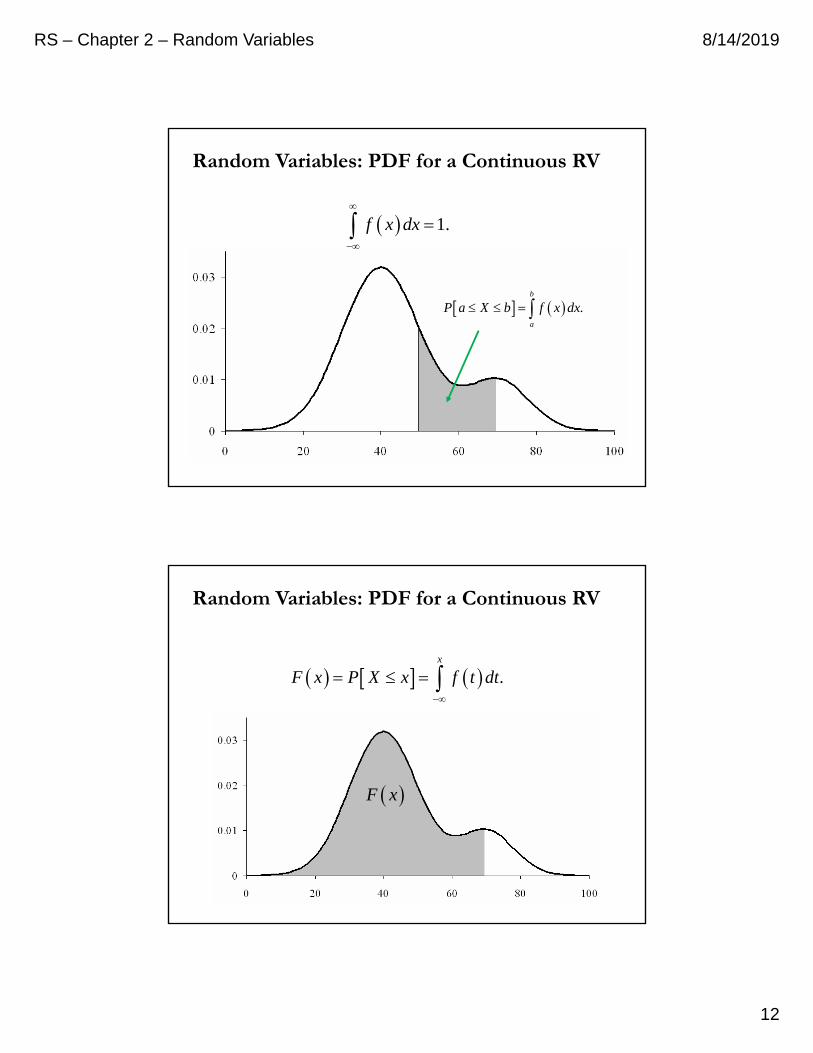

Definition: Suppose that X is a random variable. Let f(x) denote a function defined for -∞ < x < ∞ with the following properties:

1. f(x) ≥ 0

2. 1.f x dx

3. .

b

a

P a X b f x dx

Then f(x) is called the probability density function of X.. The random variable X is called continuous.

Random Variables: PDF for a Continuous RV

RS – Chapter 2 – Random Variables 8/14/2019

12

1.f x dx

.b

a

P a X b f x dx

Random Variables: PDF for a Continuous RV

F x

.x

F x P X x f t dt

Random Variables: PDF for a Continuous RV

RS – Chapter 2 – Random Variables 8/14/2019

13

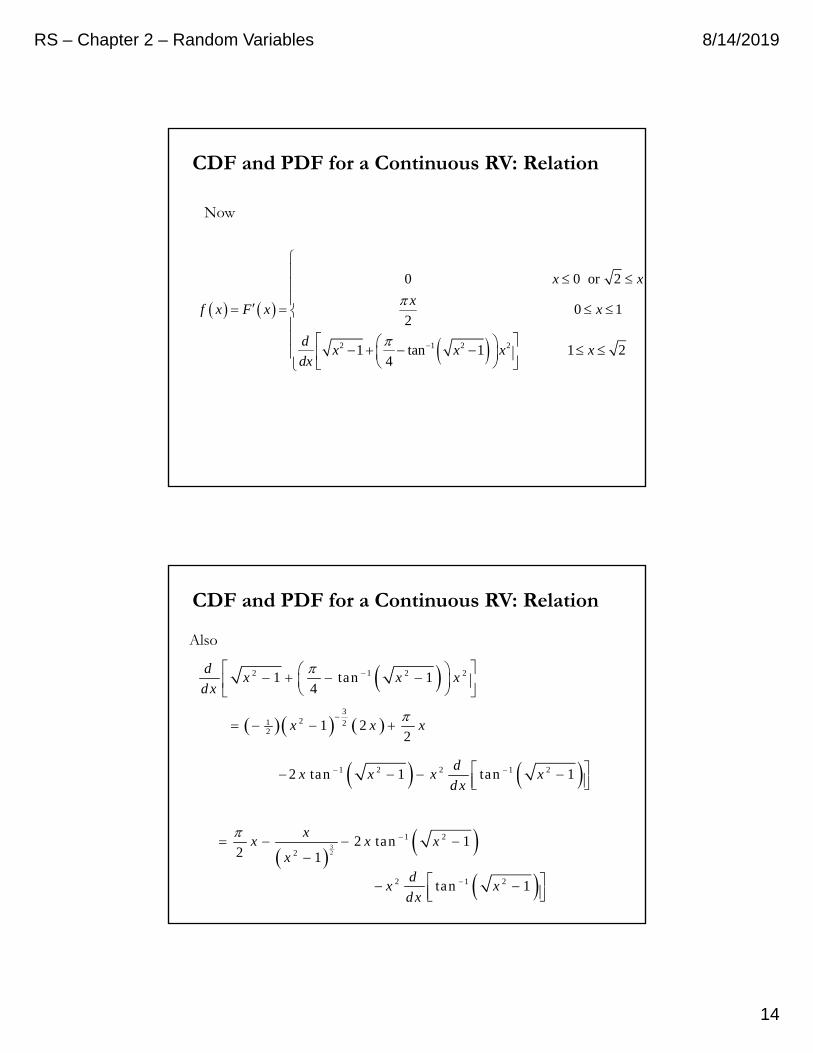

Thus if X is a continuous random variable with probability density function, f(x), the cumulative distribution function of X is given by:

.x

F x P X x f t dt

Also because of the FTC (fundamental theorem of calculus):

dF xF x f x

dx

CDF and PDF for a Continuous RV: Relation

Example: Deriving a pdf from a CDF

A point is selected at random from a square whose sides are of length 1. X is the distance of the point from the lower left hand corner.

point

X

2

2 1 2 2

00

0 14 1 2

1 tan 14 2

1

xxx

F x P X xx

x x xx

CDF and PDF for a Continuous RV: Relation

RS – Chapter 2 – Random Variables 8/14/2019

14

Now

2 1 2 2

0 0 or 2

0 12

1 tan 1 1 24

x x

xf x F x x

dx x x x

dx

CDF and PDF for a Continuous RV: Relation

2 1 2 21 tan 14

dx x x

dx

3

21 22 1 2

2x x x

1 2 2 1 22 tan 1 tan 1d

x x x xdx

Also

3

2

1 2

22 tan 1

2 1

xx x x

x

2 1 2tan 1d

x xdx

CDF and PDF for a Continuous RV: Relation

RS – Chapter 2 – Random Variables 8/14/2019

15

Now

321 2 2

2

1 1tan 1 1 2

21 1

dx x x

dx x

12

1tan

1

du

du u

and

32

2 1 2

2tan 1

1

d xx x

dx x

2 1 2 21 tan 14

dx x x

dx

1 22 tan 12

x x x

CDF and PDF for a Continuous RV: Relation

Finally

1 2

0 0 or 2

0 12

2 tan 1 1 22

x x

xf x F x x

x x x x

CDF and PDF for a Continuous RV: Relation

RS – Chapter 2 – Random Variables 8/14/2019

16

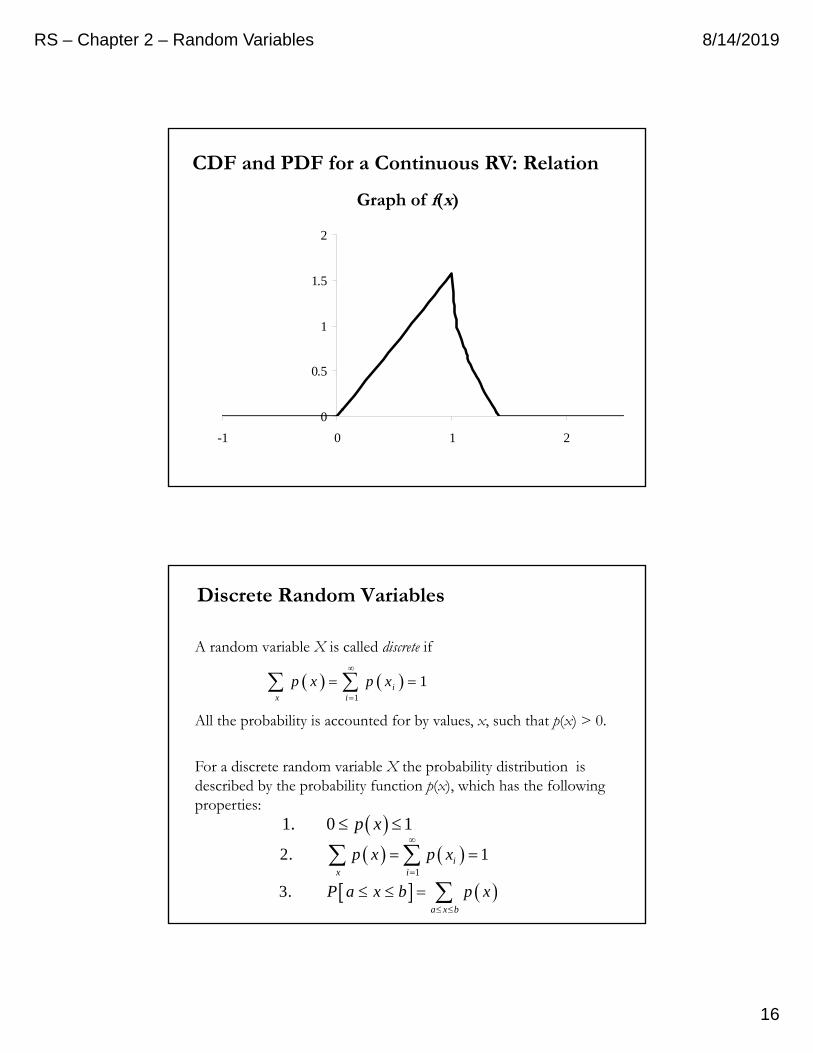

Graph of f(x)

0

0.5

1

1.5

2

-1 0 1 2

CDF and PDF for a Continuous RV: Relation

Discrete Random Variables

A random variable X is called discrete if

All the probability is accounted for by values, x, such that p(x) > 0.

For a discrete random variable X the probability distribution is described by the probability function p(x), which has the following properties:

1

1ix i

p x p x

1. 0 1p x

1

2. 1ix i

p x p x

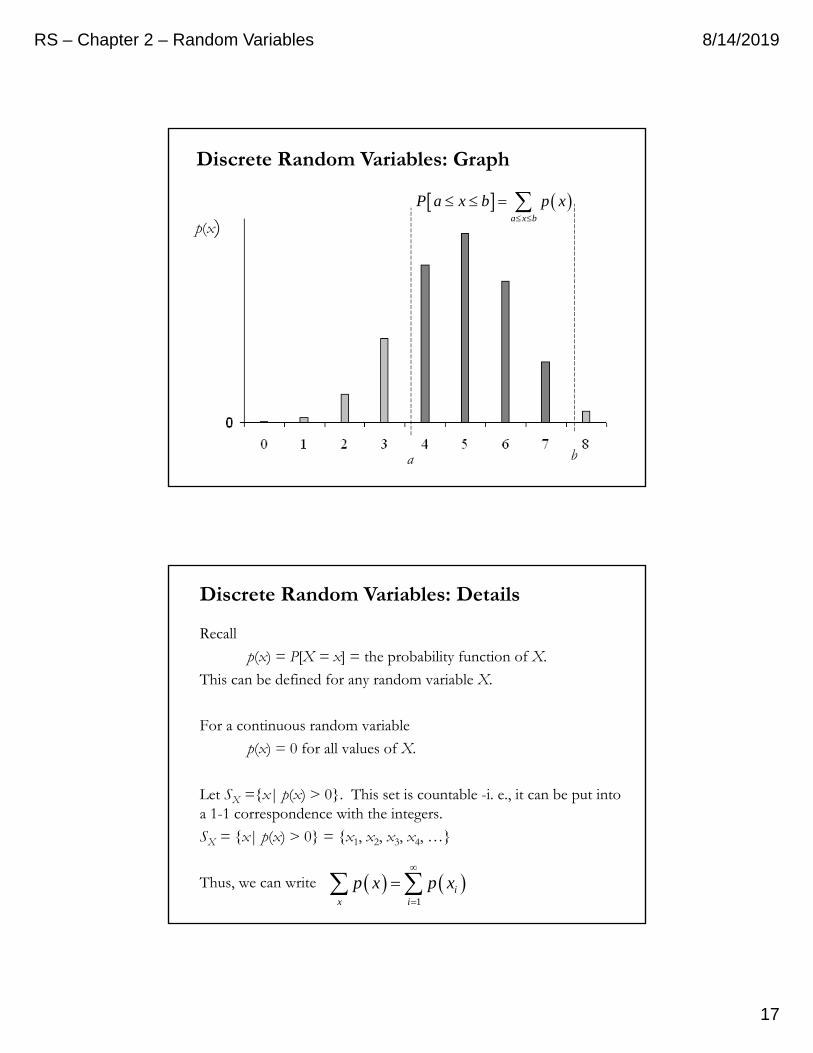

3.

a x b

P a x b p x

RS – Chapter 2 – Random Variables 8/14/2019

17

p(x)

a x b

P a x b p x

a b

Discrete Random Variables: Graph

Recall

p(x) = P[X = x] = the probability function of X.

This can be defined for any random variable X.

For a continuous random variable

p(x) = 0 for all values of X.

Let SX =x| p(x) > 0. This set is countable -i. e., it can be put into a 1-1 correspondence with the integers.

SX = x| p(x) > 0 = x1, x2, x3, x4, …

Thus, we can write 1

ix i

p x p x

Discrete Random Variables: Details

RS – Chapter 2 – Random Variables 8/14/2019

18

Thus the elements of SX = S1 S2 S3 S3 …

can be arranged x1, x2, x3, x4, …

by choosing the first elements to be the elements of S1 ,

the next elements to be the elements of S2 ,

the next elements to be the elements of S3 ,

the next elements to be the elements of S4 ,

etc

This allows us to write

1

for ix i

p x p x

Discrete Random Variables: Details

A Probability distribution is similar to a distribution of mass.

A Discrete distribution is similar to a point distribution of mass.

Positive amounts of mass are put at discrete points.

x1 x2 x3x4

p(x1) p(x2) p(x3) p(x4)

Discrete & Continuous Random Variables

RS – Chapter 2 – Random Variables 8/14/2019

19

• A Continuous distribution is similar to a continuous distribution of mass.

The total mass of 1 is spread over a continuum. The mass assigned to any point is zero but has a non-zero density

f(x)

Discrete & Continuous Random Variables

Distribution function F(x): Properties

• This is defined for any random variable, X: F(x) = P[X ≤ x]

Properties

1. F(-∞) = 0 and F(∞) = 1.

Since X ≤ - ∞= and X ≤ ∞ =S F(- ∞) = 0 and F(∞) = 1.

2. F(x) is non-decreasing (i. e., if x1 < x2 F(x1) ≤ F(x2) )

If x1 < x2 then X ≤ x2 = X ≤ x1 x1 < X ≤ x2

Thus,

P[X ≤ x2] = P[X ≤ x1] + P[x1 < X ≤ x2]

or F(x2) = F(x1) + P[x1 < X ≤ x2]

Since P[x1 < X ≤ x2] ≥ 0 F(x2) ≥ F(x1).

RS – Chapter 2 – Random Variables 8/14/2019

20

3. F(b) – F(a) = P[a < X ≤ b].

If a < b then using the argument above

F(b) = F(a) + P[a < X ≤ b]

F(b) – F(a) = P[a < X ≤ b].

4. p(x) = P[X = x] =F(x) – F(x-)

Here, limu x

F x F u

5. If p(x) = 0 for all x (i.e., X is continuous) then F(x) is continuous. A function F is continuous if

lim limu x u x

F x F u F x F u

One can show that p(x) = 0 implies

F x F x F x

Distribution function F(x): Properties

F(x) is a non-decreasing step function with

u x

F x P X x p u

jump in at .p x F x F x F x x

0 and 1F F

0

0.2

0.4

0.6

0.8

1

1.2

-1 0 1 2 3 4

F(x)

p(x)

Distribution function F(x): Discrete RV

RS – Chapter 2 – Random Variables 8/14/2019

21

F(x) is a non-decreasing continuous function with

x

F x P X x f u du

.f x F x

0 and 1F F

F(x)

f(x) slope

0

1

-1 0 1 2x

Distribution function F(x): Continuous RV

Some Important Discrete Distributions

RS – Chapter 2 – Random Variables 8/14/2019

22

The Binomial distribution

Jacob Bernoulli (1654– 1705)

Suppose that we have a Bernoulli trial (an experiment) that has 2 results:1. Success (S)2. Failure (F)

Suppose that p is the probability of success (S) and q = 1 – p is the probability of failure (F). Then, the probability distribution with probability function

0

1

q xp x P X x

p x

is called the Bernoulli distribution.

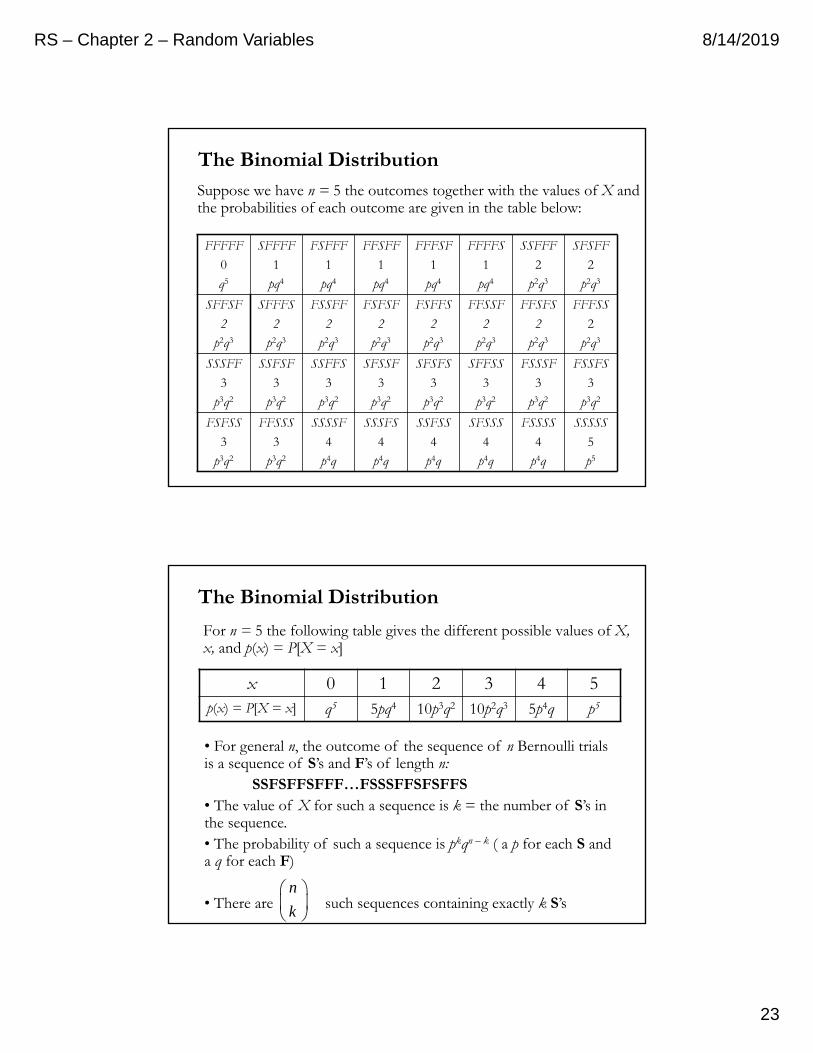

• Now assume that the Bernoulli trial is repeated independently n times.Let X be the number of successes ocurring in the n trials. (The possible values of X are 0, 1, 2, …, n)

Bernouille Distribution

RS – Chapter 2 – Random Variables 8/14/2019

23

Suppose we have n = 5 the outcomes together with the values of X and the probabilities of each outcome are given in the table below:

FFFFF

0

q5

SFFFF

1

pq4

FSFFF

1

pq4

FFSFF

1

pq4

FFFSF

1

pq4

FFFFS

1

pq4

SSFFF

2

p2q3

SFSFF

2

p2q3

SFFSF

2

p2q3

SFFFS

2

p2q3

FSSFF

2

p2q3

FSFSF

2

p2q3

FSFFS

2

p2q3

FFSSF

2

p2q3

FFSFS

2

p2q3

FFFSS

2

p2q3

SSSFF

3

p3q2

SSFSF

3

p3q2

SSFFS

3

p3q2

SFSSF

3

p3q2

SFSFS

3

p3q2

SFFSS

3

p3q2

FSSSF

3

p3q2

FSSFS

3

p3q2

FSFSS

3

p3q2

FFSSS

3

p3q2

SSSSF

4

p4q

SSSFS

4

p4q

SSFSS

4

p4q

SFSSS

4

p4q

FSSSS

4

p4q

SSSSS

5

p5

The Binomial Distribution

For n = 5 the following table gives the different possible values of X, x, and p(x) = P[X = x]

x 0 1 2 3 4 5p(x) = P[X = x] q5 5pq4 10p3q2 10p2q3 5p4q p5

• For general n, the outcome of the sequence of n Bernoulli trials is a sequence of S’s and F’s of length n:

SSFSFFSFFF…FSSSFFSFSFFS• The value of X for such a sequence is k = the number of S’s in the sequence. • The probability of such a sequence is pkqn – k ( a p for each S and a q for each F)

• There are such sequences containing exactly k S’sn

k

The Binomial Distribution

RS – Chapter 2 – Random Variables 8/14/2019

24

0,1, 2,3, , 1,k n knp k P X k p q k n n

k

K

These are the terms in the expansion of (p + q)n using the Binomial Theorem

0 1 1 2 2 0

0 1 2n n n n nn n n n

p q p q p q p q p qn

K

For this reason the probability function

0,1, 2, ,x n xnp x P X x p q x n

x

K

is called the probability function for the Binomial distribution

is the number of ways of selecting the k positions for the S’s (the remaining n – k positions are for the F’s). Thus,

n

k

The Binomial Distribution

SummaryWe observe a Bernoulli trial (S,F) n times. Let X denote the number of successes in the n trials.Then, X has a binomial distribution:

0,1, 2, ,x n xnp x P X x p q x n

x

K

where1. p = the probability of success (S), and2. q = 1 – p = the probability of failure (F)

The Binomial Distribution

RS – Chapter 2 – Random Variables 8/14/2019

25

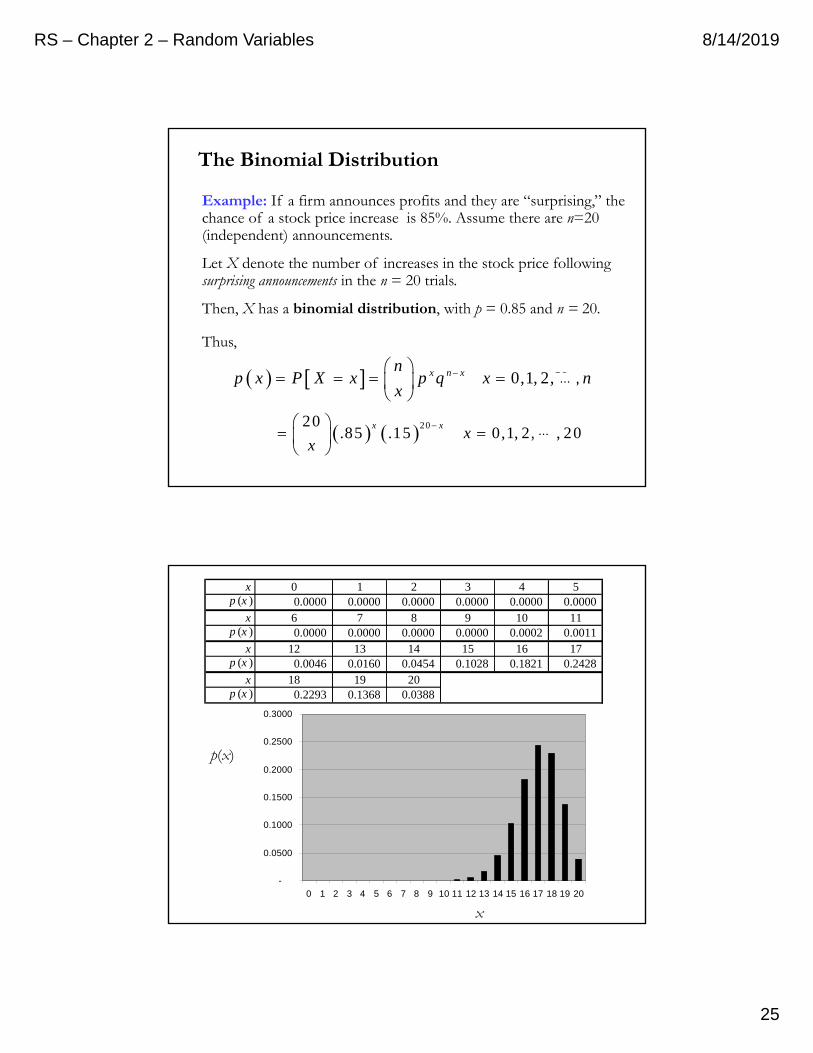

Example: If a firm announces profits and they are “surprising,” the chance of a stock price increase is 85%. Assume there are n=20 (independent) announcements.

Let X denote the number of increases in the stock price following surprising announcements in the n = 20 trials.

Then, X has a binomial distribution, with p = 0.85 and n = 20.

0,1, 2, ,x n xnp x P X x p q x n

x

K

Thus,

2020.85 .15 0,1, 2, , 20

x xx

x

K

The Binomial Distribution

⋯

⋯

-

0.0500

0.1000

0.1500

0.2000

0.2500

0.3000

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

p(x)

x

x 0 1 2 3 4 5p (x ) 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000

x 6 7 8 9 10 11p (x ) 0.0000 0.0000 0.0000 0.0000 0.0002 0.0011

x 12 13 14 15 16 17p (x ) 0.0046 0.0160 0.0454 0.1028 0.1821 0.2428

x 18 19 20p (x ) 0.2293 0.1368 0.0388

RS – Chapter 2 – Random Variables 8/14/2019

26

The Poisson distribution

Siméon Denis Poisson (1781-1840)

The Poisson distribution

• Suppose events are occurring randomly and uniformly in time.

• The events occur with a known average.

• Let X be the number of events occurring (arrivals) in a fixed period of time (time-interval of given length).

• Typical example: X = Number of crime cases coming before a criminal court per year (original Poisson’s application in 1838.)

• Then, X will have a Poisson distribution with parameter .

• The parameter λ represents the expected number of occurrences in a fixed period of time. The parameter λ is a positive real number.

0,1, 2, 3, 4,!

x

p x e xx

K⋯

RS – Chapter 2 – Random Variables 8/14/2019

27

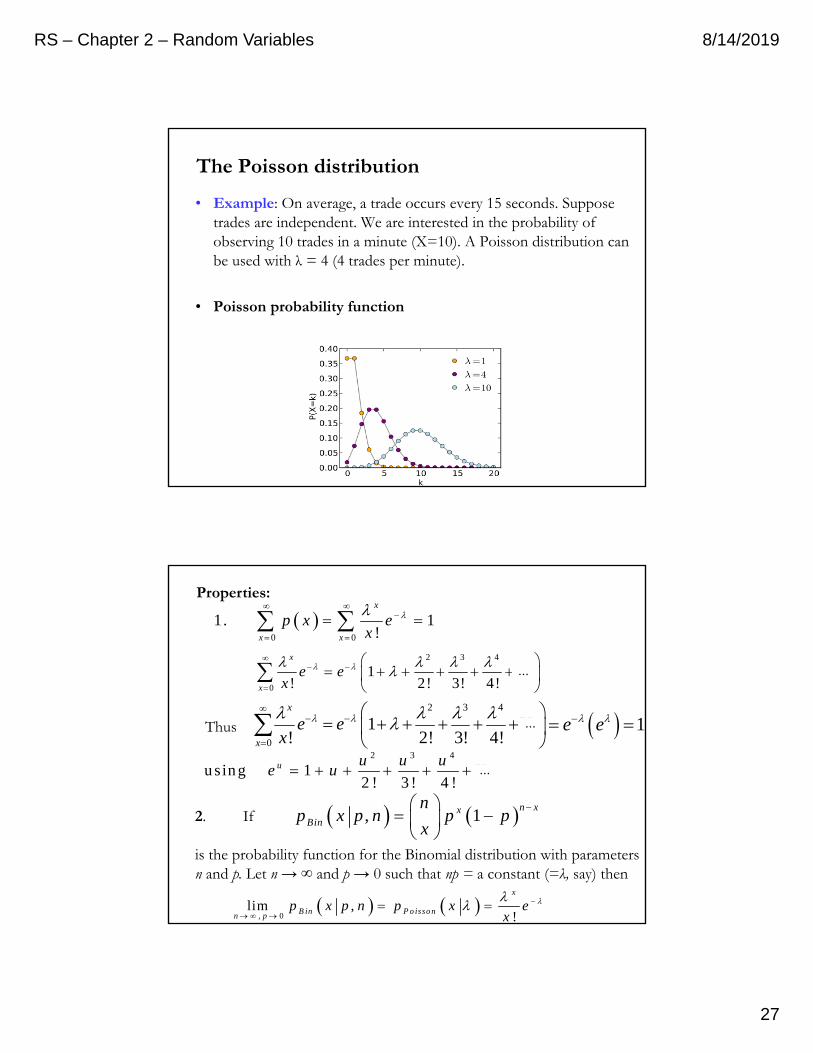

The Poisson distribution

• Example: On average, a trade occurs every 15 seconds. Suppose trades are independent. We are interested in the probability of observing 10 trades in a minute (X=10). A Poisson distribution can be used with λ = 4 (4 trades per minute).

• Poisson probability function

1e e 2 3 4

0

1! 2! 3! 4!

x

x

e ex

K

2 3 4

u sin g 12 ! 3 ! 4 !

u u u ue u K

Thus

2. If

is the probability function for the Binomial distribution with parameters n and p. Let n → ∞ and p → 0 such that np = a constant (=λ, say) then

, 1n xx

Bin

np x p n p p

x

, 0

lim ,!

x

B in P o issonn p

p x p n p x ex

0 0

1. 1!

x

x x

p x ex

2 3 4

0

1! 2! 3! 4!

x

x

e ex

K

Properties:

⋯

⋯

⋯

RS – Chapter 2 – Random Variables 8/14/2019

28

Proof: , 1n xx

Bin

np x p n p p

x

Suppose or np pn

!

, , 1! !

x n x

Bin Bin

np x p n p x n

x n x n n

!

1 1! !

x nx

x

n

x n n x n n

1 11 1

!

x nx n n n x

x n n n n n

L

L

1 11 1 1 1 1

!

x nx x

x n n n n

L

⋯

⋯

⋯

Now lim ,Binn

p x n

1 1lim 1 1 1 1

!

x nx

n

x

x n n n n

L

lim 1!

nx

nx n

Using the classic limit lim 1n

u

n

ue

n

lim , lim 1! !

nx x

Bin Poissonn n

p x n e p xx n x

Note: In many applications, when n is large and p is very small --and the expectation np is not big. Then, the binomial distribution may be approximated by the easier Poisson distribution. This is called the law of rare events, since each of the n individual Bernoulli events rarely occurs.

⋯

RS – Chapter 2 – Random Variables 8/14/2019

29

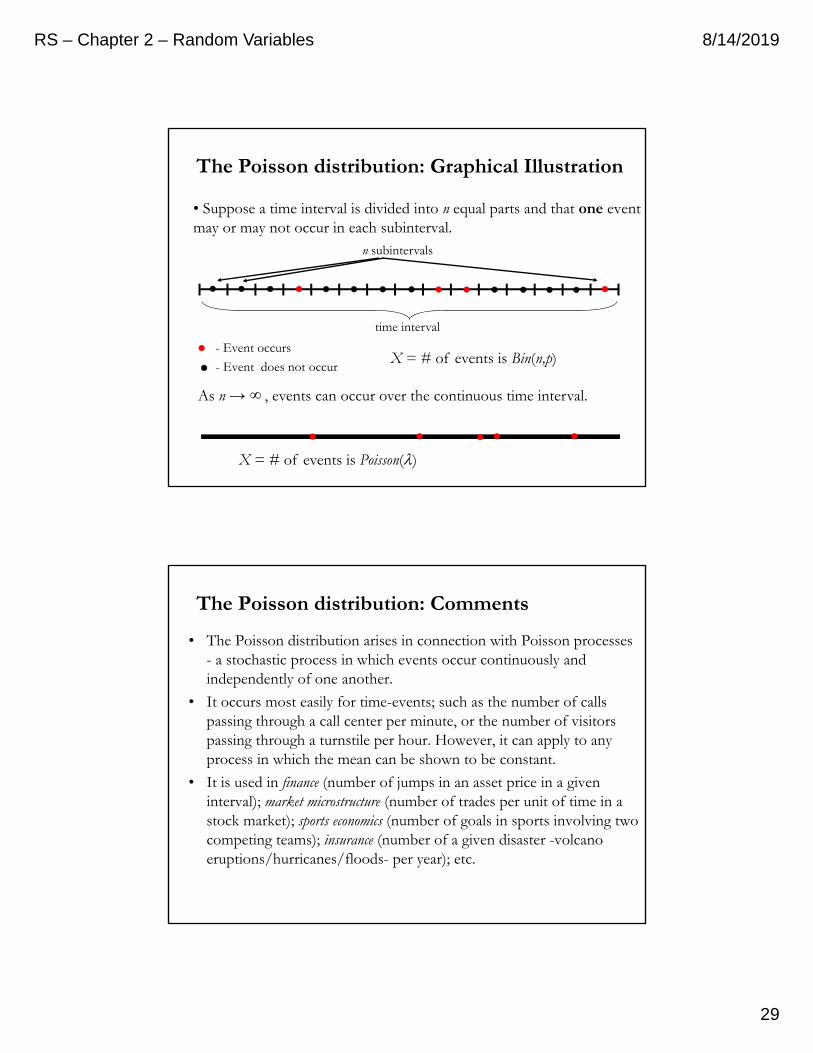

• Suppose a time interval is divided into n equal parts and that one event may or may not occur in each subinterval.

time interval

n subintervals

- Event occurs

- Event does not occur

As n → ∞ , events can occur over the continuous time interval.

X = # of events is Bin(n,p)

X = # of events is Poisson()

The Poisson distribution: Graphical Illustration

The Poisson distribution: Comments

• The Poisson distribution arises in connection with Poisson processes - a stochastic process in which events occur continuously and independently of one another.

• It occurs most easily for time-events; such as the number of calls passing through a call center per minute, or the number of visitors passing through a turnstile per hour. However, it can apply to any process in which the mean can be shown to be constant.

• It is used in finance (number of jumps in an asset price in a given interval); market microstructure (number of trades per unit of time in a stock market); sports economics (number of goals in sports involving two competing teams); insurance (number of a given disaster -volcano eruptions/hurricanes/floods- per year); etc.

RS – Chapter 2 – Random Variables 8/14/2019

30

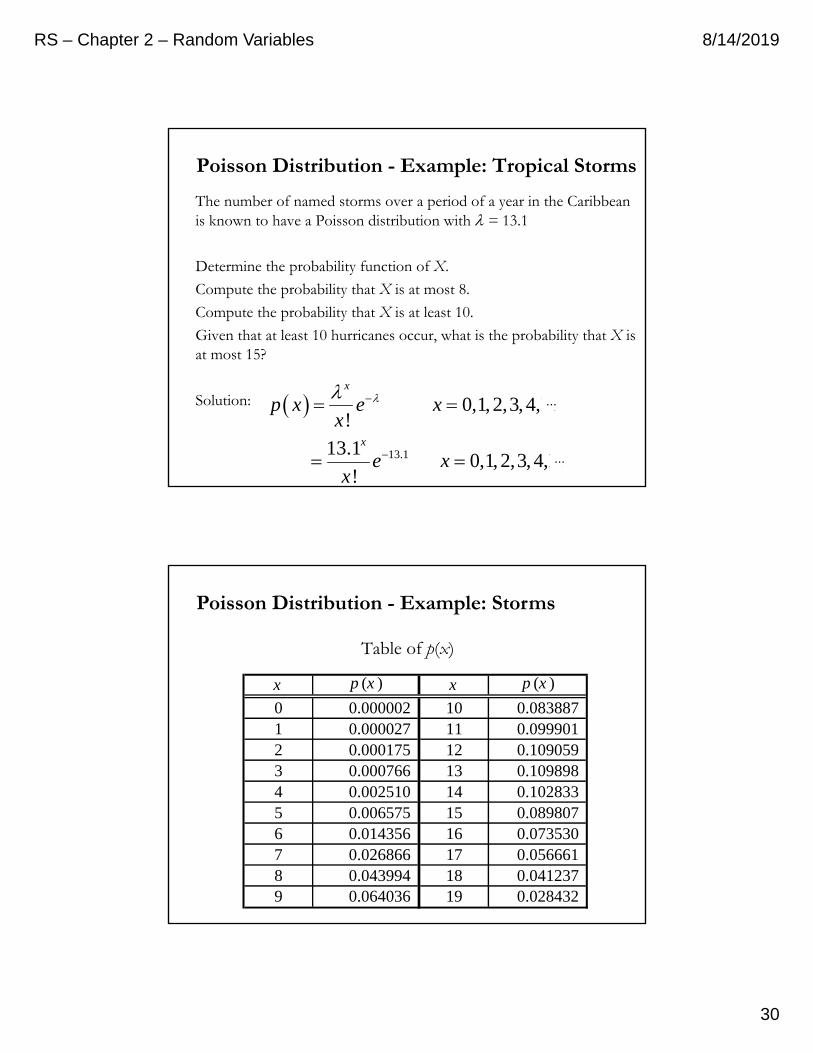

Poisson Distribution - Example: Tropical Storms

The number of named storms over a period of a year in the Caribbean is known to have a Poisson distribution with = 13.1

Determine the probability function of X.

Compute the probability that X is at most 8.

Compute the probability that X is at least 10.

Given that at least 10 hurricanes occur, what is the probability that X is at most 15?

Solution: 0,1, 2,3, 4,!

x

p x e xx

K

13.113.1 0,1, 2,3, 4,

!

x

e xx

K

⋯

⋯

Table of p(x)

x p (x ) x p (x )

0 0.000002 10 0.083887 1 0.000027 11 0.099901 2 0.000175 12 0.109059 3 0.000766 13 0.109898 4 0.002510 14 0.102833 5 0.006575 15 0.089807 6 0.014356 16 0.073530 7 0.026866 17 0.056661 8 0.043994 18 0.041237 9 0.064036 19 0.028432

Poisson Distribution - Example: Storms

RS – Chapter 2 – Random Variables 8/14/2019

31

at m o st 8 8P P X

0 1 8 .0 9 5 2 7p p p L

at least 1 0 10 1 9P P X P X

1 0 1 9 .84 00p p p L

at m o st 1 5 at leas t 1 0 1 5 1 0P P X X

1 5 1 0 10 15

1 0 1 0

P X X P X

P X P X

10 11 150 .7 0 8

.8 4 0 0

p p p

L

Poisson Distribution - Example: Storms

![[ T ] Two tiny tigers take two taxis to town `Two `tiny `tigers take `two `taxis to town.](https://static.fdocument.org/doc/165x107/56649d135503460f949e6998/-t-two-tiny-tigers-take-two-taxis-to-town-two-tiny-tigers-take-two-taxis.jpg)