“A TALE OF TWO CDDS”...“a tale of two cdds”: lessons learned for mitigating the risk of...

33

“A T ALE OF TWO CDDS”: LESSONS LEARNED FOR MITIGATING THE RISK OF FRAUD AND CORRUPTION IN CDD OPERATIONS RIMA AL-AZAR PREVENTIVE SERVICES UNIT Ι INTEGRITY VICE PRESIDENCY Ι 16 December 2011 Ι ROME, ITALY

Transcript of “A TALE OF TWO CDDS”...“a tale of two cdds”: lessons learned for mitigating the risk of...

“A TALE OF TWO CDDS”: LESSONS LEARNED FOR MITIGATING THE RISK OF FRAUD AND CORRUPTION IN CDD OPERATIONS

RIMA AL-AZAR

PREVENTIVE SERVICES UNIT Ι INTEGRITY VICE PRESIDENCY Ι 16 December 2011 Ι ROME, ITALY

INT: Vice-Presidency for Institutional Integrity

The Division was created in 2001; became a Vice-Presidency in 2008

Its mandate is to:

– Conduct investigations based on allegations of fraud and corruption related to Bank financing and/or Bank staff

– Carry out preventive activities, including training, operational advice and lessons learned from investigations

Operationally, it is an independent Vice-Presidency and reports directly to the World Bank’s president

2

Risk Aversion

Risk Management

4

Outline

Background: The Two Projects Forensic Audit Findings 1. Project Design 2. Participatory planning 3. Procurement 4. Financial Management 5. HR Issues 6. Monitoring and Supervision 7. Auditing 8. Access to Information 9. Social Accountability 10. Effective Grievance Redress Mechanism

The Two CDD Projects

Arid Lands Resource Management Project Phase II (ALRMP II). The ALRMP II project was designed to be implemented over six years (September 2003 to December 2010). The total Bank financing was US$120 million, of which about one-third was allocated to the CDD component.

Western Kenya Community-Driven Development and Flood Mitigation Project (WKCDD). Following the reported success of the ALRMP II in Kenya’s arid and semiarid regions, the WKCDD project was designed to be implemented in the western region over six years (August 2007 to June 2015). The total Bank financing was US$85.8 million, of which more than 40% was allocated to the CDD component.

6

Forensic Audit Findings

Arid Lands project audited by INT (examined 28,000 transactions over 2 FYs and in 7/28 districts + HQ):

42% of expenditures were questionable (out of which 29% suspected fraudulent)

At the district level (excluding HQ), 66% were questionable (out of which 49% were suspected fraudulent)

Fraudulent behaviors in all expense categories including fuel, vehicle repairs, training (capacity building), allowances and per diem, payroll, and noncurrent assets

Similar findings in the WKCDD - audited by Government of Kenya

Questionable Expenditures Goods or services purchased did not meet one of the

categories defined in the legal agreement.

There was insufficient evidence that the expenditure was incurred.

There was evidence that some or all of the expenditure was embezzled.

Goods or services had not been provided.

Funds had not been expended by the end of the financial period.

Expenditures breached government regulations.

8

1. Project Design

Importance of institutional issues (role of Community Development Community)

Technical design should be based on the communities’ capacities and not the other way round

Private vs. Public Goods (clear procedures, harmonize with other donors’ initiatives)

Community contribution (cash and/or in-kind; %, how to calculate)

Importance of Project Operational Manual (technical, procurement and FM)

No “one-size-fits-all” (infrastructure, density, security, capacity, etc…); political economy analysis

Role of Community Development Committee (CDC)

A community bakery was built on the land of the chairman of the CDC

He and his family were the sole users of the bakery

Conflict of Interest

Collusion with District Officials

Accountable CDCs

Clear role and responsibilities

Regular elections

Downward and upward accountability

Clear membership criteria

Assess whether it is needed

The Community Contribution Well-explained, based on poverty level

The 30% community contribution was highly susceptible to fraud and manipulation

Scheme Variation I Scheme Variation II Scheme Variation III

Community cannot afford cash contribution but contributes in kind (i.e. labor); however, labor is minimal

Community does not make any contribution; yet, the funds are released

No community contribution is solicited; instead, a business fronts the 30% contribution; subsequently, funds released are shared between project officials and the business. A fictitious beneficiary list is produced

2. Participatory planning and capacity building

A key objective of CDD projects

In theory if done right, it minimizes integrity risks

However, rarely monitored (M&E indicators focus on output and not processes)

Prone to manipulation (“facipulation”)

Fake participants, fake venue and even fake event: double impact

Duration, inclusion, staggering of training, clarifying procedures and responsibilities

Requires capacity building, proactive engagement and facilitation at community level

3. Procurement

Local Procurement

WB vs. government procedures Simple, user-friendly templates Establish unit cost database In-kind community contribution calculation Up-to-date rolling procurement plan List of all signed contracts

Value for Money (VFM)

Specify eligibility/non-eligibility of land purchases; Voluntary Land Issues

Value for Money (VFM)

A

Toilet in community A Toilet in community B

4. Financial Management

Fixed asset management (registry, branding)

Fleet management: vehicle maintenance and fuel issues

Better donor coordination and financial reporting

Double – dipping

Monitor funds flow

Value Added Tax

Financial reporting: linking physical progress with financial reporting

Project Fixed Assets

World Bank policy on asset management and disposal

Asset registry with unique product identifier (serial number) and branding

Part of the MIS

Procedures for project staff to hand over project assets

Undertake stock-taking before second phase

Fleet Management: Vehicle and Fuel Cars can get very expensive

The issues The red flags Some suggestions

1. Ineligible expenses from incomplete work tickets and log books

2. Insufficient details of the vehicle to which the expense is related

3. Repairs for cars that did not belong to the project

4. Quantities and prices on receipts not matching or being excessive

What can go wrong?

Easy to create receipts for maintenance not received

Easy to manipulate receipts and inflate amounts paid

Maintenance for vehicles that do not belong to the project

Failure to follow government’s or other applicable repairs or maintenance guidelines

Lack of details of vehicles receiving repairs and maintenance on invoices

Use of unauthorized mechanics Most repairs performed in the last

quarter of fiscal year Repeated repairs on same cars

within a short timeframe Purchase of tires when mileage

suggests this is unnecessary Replacement of expensive parts on

the same vehicles No logbooks, incomplete logbooks or

missing logbooks

Look for the red flags Analyze maintenance costs per

kilometer Detailed analysis of the usage

of project vehicles (kms) with maintenance costs

Analyze if most repairs performed in the last quarter of fiscal year

Analyze if liters recorded as supplied to a vehicle is greater than the size of its fuel tank

Report issue

Training Per diem and allowances

Minimize imprests and cash use (e.g., in one district 35%)

Direct payment to hotel

Wire per diem and allowances to trainees’ bank account

or

Explore the use of mobile money

Closed training participation

List of participants ready before training

List pre-approved, if feasible

Take and file a dated photo of participants at training venue

Mitigating risks

Enhanced coordination

Branding

Geo-referencing linked to publicly available map

Double-dipping:

Cheque details from two Bank projects

Tana River district

Cheques for which no payment vouchers were provided to INT

Date Date Cheque Payee Amount

(per butt) (per BS) Number (KSH)

9-Sep-07 1577 Kumbi Primary School 330,000

7-Sep-07 1578 Lenda Primary School 330,000

8-Sep-07 1579 Chanani Primary School 330,000

9-Sep-07 3-Oct-07 1601 Subo Primary School 330,000

31-Oct-07 6-Nov-07 1627 Kumbi Primary School 330,000

21-Dec-07 2-Jan-08 1686 Lenda Primary School 330,000

21-Dec-07 12-Mar-08 1687 Chanani Primary School 330,000

21-Dec-07 5-Mar-08 1688 Subo Primary School 330,000

2,640,000

Lack of coordination of community interventions between different donors and/or different projects increases the risk of double dipping

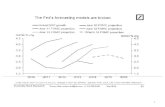

Funds Flow FMR expenditures highly concentrated in Q4

Risks:

Hasty spending

Mistakes

Unaccounted expenses

Paying before delivery

Value for Money issues

Weak control environment/Conditions enabling commission of fraud

Q3

-FY

04

Q4

-FY

04

Q1-

FY

05

Q2

-FY

05

Q3

-FY

05

Q4

-FY

05

Q1-

FY

06

Q2

-FY

06

Q3

-FY

06

Q4

-FY

06

Q1-

FY

07

Q2

-FY

07

Q3

-FY

07

Q4

-FY

07

Q1-

FY

08

Q2

-FY

08

Q3

-FY

08

Q4

-FY

08

Q1-

FY

09

Q2

-FY

09

Q3

-FY

09

Cat. 1 - Civil Works Cat 2 - Goods and Equipment Cat 3 - Community Driven Development Microprojects Cat 4 - Drought Contigency Fund Cat 5 - Training and Consultancy Cat (6a) - Vehicle Operating and Maintenance Cat (6b) - Other Operating and Maintenance

Financial Reporting Not only eligible expenditures

Provide standard templates for financial reporting (excel with formula)

Restrict ability to edit and modify data

Link to Financial Management Report (FMR) categories to avoid manual calculations

FMR should reflect output/results-based performance as well as eligible categories

5. Human Resources issues CDDs are human resource intensive!

District staff from the same region (to leverage language and local knowledge) but not from the same district

Limit tenure of District Coordinator (in project one Coordinator in same post for 11 years)

Recruitment to be done through private agent, if possible

HR policy and procedures developed for project

Include segregation of responsibilities (e.g., Procurement Officer should not be signing checks)

Hiring/firing/rotations/salary increases to get the TTL “No Objection”

Must be a specific focus of project design, monitoring and supervision

Continuous induction due to high staff turnover

6. Monitoring and Supervision “It was the best of projects; it was the worst of projects…”

MIS

Use information to flag potential areas that need attention Disbursement Expenditures Procurement plan vs. actual procurement

Different supervision model: Risk-based and focus on processes

Follow up on unimplemented mission recommendations

Tone from the top: Annual field visit with director level line minister to discuss governance issues

Innovative ICT methods http://developmentseed.org/

Conflict zones: Satellite image proving that a school that was 100% paid for did not exist

What are they Benefits

Continuous assessment of project implementation

Element of surprise

Random sampling

Bottom-up approach

Compliment annual audits

Timely vs. ex post facto

Regularly conducted

Independent

Enhance financial discipline, management, and accountability

Strengthen capacity building and training

Deterrent effect: Increase perception of detection

7. Audits & Rolling Audits Importance of CDD-specific audit TORs

8. Access to Information at all levels

Donors

Central Government

Decentralized Government

Grassroots/Civil Society

Publish what you fund

Website

Website/other (SMS, etc)

SMS

Publish what you receive Publish what you fund

Publish what you receive Publish what you fund

Publish what you receive

Website

What How/ Where

Who

9. Social Accountability Information is key

Assess and piggy back on other donors’ and NGOs initiatives

Third party monitoring to support project monitoring and supervision

Use of innovative ICT (e.g., mobile money)

Caveat access and by-in of users

Public disclosure

Website Community boards, local radio, CDC briefings to community

Preferable that information on project and grievance redress mechanism be carried out by third party

Transparency “Sunlight is the Best Disinfectant”

Funds

Flow Information

GRM Information

Information

regarding INT

Procurement

Information

Decision-making

Meetings’ Minutes

Sharing

Disclosure of

Project Staff

& Position

Billboard

Displaying Micro-

project Information

Project Operation

Manual Available on

Website

Transparency is

key

10. Effective Grievance Redress Mechanism Project Level

Establish one

Hotline and complaint boxes not enough!

Learn from other projects/donors’ experiences

Set up database of complaints and link it to the project MIS

Link Project GRM to existing local structures and to national ones

Example: Human Rights Commission , Commission for Justice and Peace

Protect whistle-blowers

Project staff who blew the whistle was fired

Main Learning Points

Transparency, Accountability and Participation (TAP) in CDD projects needs to work at all levels All levels need to be transparent and accountable, and at least accept the premise that participation at the community level is vital to success. Degree of participation of national and subnational level entities will depend on the nature of the project.

Keep the project simple and appropriate Don't overestimate or underestimate the beneficiaries. Keep in mind social, economic and logistical aspects. Test all materials and systems on a small scale through pilots before rolling out. Avoid the Christmas tree approach.

Keep fiduciary systems simple and appropriate Get funds to the beneficiaries in a way that avoids unnecessary hurdles or bureaucracy. Ensure that any rules are reasonable and can be monitored at each level of the project. Do not neglect national or subnational level systems. Do not neglect the more mundane aspects such as inventory and accounting for expenses.

Main Learning Points

Ensure appropriate facilitation Have an appropriate system in place for mobilizing, training, paying, managing, monitoring, rewarding/sanctioning, demobilizing the facilitators. Make sure that this works and is not nepotistic.

Get the materials right Make sure that the project manuals, posters, booklets, etc., are clear and all promote the same principles. In particular, make sure that the rules and lines of reporting/accountability are spelled out clearly.

Implement a new supervision model Supervision should be carried out using a risk-based model and assess the processes as well as the physical outputs.

Keep tweaking Most projects are multi-year so keep improving the systems based on experience. Make sure there are events planned to allow for sharing of knowledge between levels. Revise manuals and (re)training, as appropriate. Assume you will need a budget and make time for these aspects.

32

ANONYMITY. If you wish to remain anonymous, we encourage use of a free email service (such as Hotmail or Yahoo) to create a temporary email account using a pseudonym, so that we may correspond with you as necessary. This can be helpful in pursuing your allegation.

E-mail: [email protected]

+1 (202) 458-7677

Fax: (202) 522-7140

How To Report an Allegation

Thank you

Any comments/questions?

33