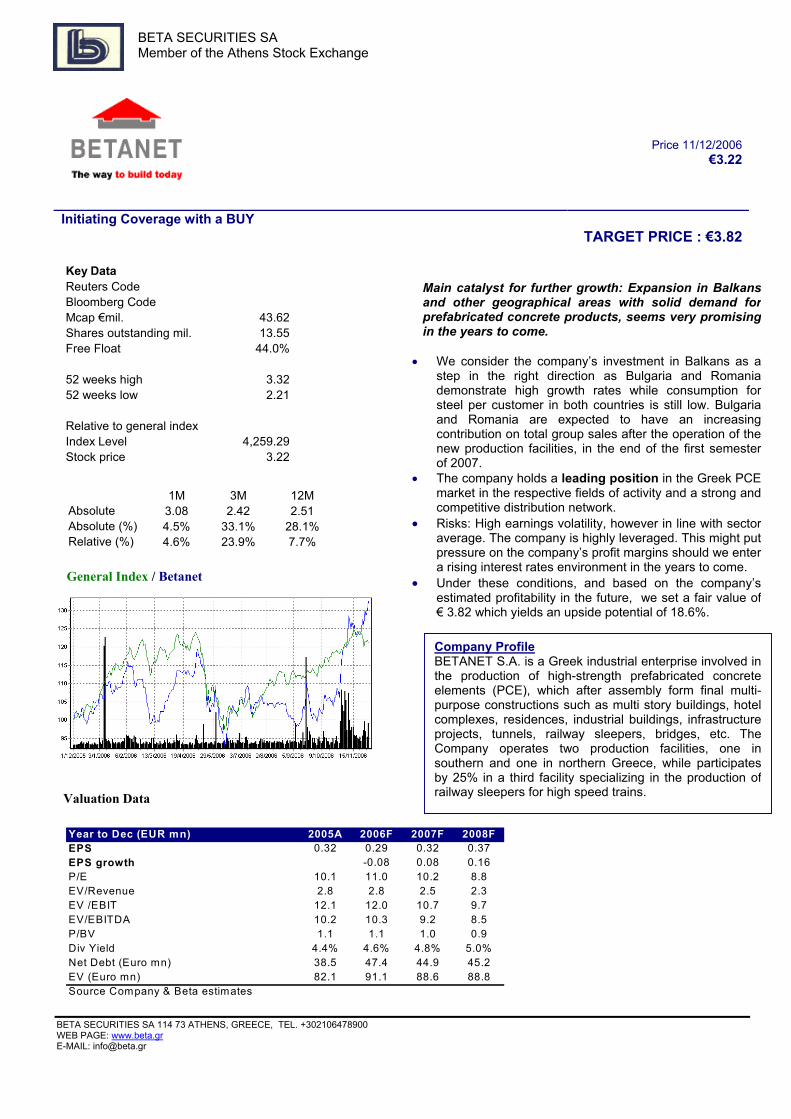

€3.22 Initiating Coverage with a BUY TARGET PRICE : €3 · It holds a leading position in the...

12

BETA SECURITIES SA Member of the Athens Stock Exchange General Index / Betanet Valuation Data Price 11/12/2006 €3.22 Initiating Coverage with a BUY TARGET PRICE : €3.82 1Μ 3Μ 12Μ Absolute 3.08 2.42 2.51 Absolute (%) 4.5% 33.1% 28.1% Relative (%) 4.6% 23.9% 7.7% Key Data Reuters Code Bloomberg Code Mcap €mil. 43.62 Shares outstanding mil. 13.55 Free Float 44.0% 52 weeks high 3.32 52 weeks low 2.21 Relative to general index Index Level 4,259.29 Stock price 3.22 Company Profile BETANET S.A. is a Greek industrial enterprise involved in the production of high-strength prefabricated concrete elements (PCE), which after assembly form final multi- purpose constructions such as multi story buildings, hotel complexes, residences, industrial buildings, infrastructure projects, tunnels, railway sleepers, bridges, etc. The Company operates two production facilities, one in southern and one in northern Greece, while participates by 25% in a third facility specializing in the production of railway sleepers for high speed trains. Main catalyst for further growth: Expansion in Balkans and other geographical areas with solid demand for prefabricated concrete products, seems very promising in the years to come. • We consider the company’s investment in Balkans as a step in the right direction as Bulgaria and Romania demonstrate high growth rates while consumption for steel per customer in both countries is still low. Bulgaria and Romania are expected to have an increasing contribution on total group sales after the operation of the new production facilities, in the end of the first semester of 2007. • • The company holds a leading position in the Greek PCE market in the respective fields of activity and a strong and competitive distribution network. Risks: High earnings volatility, however in line with sector average. The company is highly leveraged. This might put pressure on the company’s profit margins should we enter a rising interest rates environment in the years to come. • Under these conditions, and based on the company’s estimated profitability in the future, we set a fair value of € 3.82 which yields an upside potential of 18.6%. Year to Dec (EUR mn) 2005A 2006F 2007F 2008F EPS 0.32 0.29 0.32 0.37 EPS growth -0.08 0.08 0.16 P/E 10.1 11.0 10.2 8.8 EV/Revenue 2.8 2.8 2.5 2.3 EV /EBIT 12.1 12.0 10.7 9.7 EV/EBITDA 10.2 10.3 9.2 8.5 P/BV 1.1 1.1 1.0 0.9 Div Yield 4.4% 4.6% 4.8% 5.0% Net Debt (Euro mn) 38.5 47.4 44.9 45.2 EV (Euro mn) 82.1 91.1 88.6 88.8 Source Company & Beta estimates BETA SECURITIES SA 114 73 ATHENS, GREECE, TEL. +302106478900 WEB PAGE: www.beta.gr E-MAIL: [email protected]

Transcript of €3.22 Initiating Coverage with a BUY TARGET PRICE : €3 · It holds a leading position in the...

BETA SECURITIES SA Member of the Athens Stock Exchange

General Index / Betanet

Valuation Data

Price 11/12/2006 €3.22

Initiating Coverage with a BUY TARGET PRICE : €3.82

1Μ 3Μ 12ΜAbsolute 3.08 2.42 2.51Absolute (%) 4.5% 33.1% 28.1%Relative (%) 4.6% 23.9% 7.7%

Key DataReuters CodeBloomberg CodeMcap €mil. 43.62Shares outstanding mil. 13.55Free Float 44.0%

52 weeks high 3.3252 weeks low 2.21

Relative to general indexIndex Level 4,259.29Stock price 3.22

Company Profile BETANET S.A. is a Greek industrial enterprise involved inthe production of high-strength prefabricated concreteelements (PCE), which after assembly form final multi-purpose constructions such as multi story buildings, hotelcomplexes, residences, industrial buildings, infrastructureprojects, tunnels, railway sleepers, bridges, etc. TheCompany operates two production facilities, one insouthern and one in northern Greece, while participatesby 25% in a third facility specializing in the production ofrailway sleepers for high speed trains.

Main catalyst for further growth: Expansion in Balkansand other geographical areas with solid demand forprefabricated concrete products, seems very promisingin the years to come.

• We consider the company’s investment in Balkans as astep in the right direction as Bulgaria and Romaniademonstrate high growth rates while consumption forsteel per customer in both countries is still low. Bulgariaand Romania are expected to have an increasingcontribution on total group sales after the operation of thenew production facilities, in the end of the first semesterof 2007.

•

•

The company holds a leading position in the Greek PCEmarket in the respective fields of activity and a strong andcompetitive distribution network. Risks: High earnings volatility, however in line with sectoraverage. The company is highly leveraged. This might putpressure on the company’s profit margins should we entera rising interest rates environment in the years to come.

• Under these conditions, and based on the company’sestimated profitability in the future, we set a fair value of€ 3.82 which yields an upside potential of 18.6%.

Year to Dec (EUR mn) 2005A 2006F 2007F 2008FEPS 0.32 0.29 0.32 0.37EPS growth -0.08 0.08 0.16P/E 10.1 11.0 10.2 8.8EV/Revenue 2.8 2.8 2.5 2.3EV /EBIT 12.1 12.0 10.7 9.7EV/EBITDA 10.2 10.3 9.2 8.5P/BV 1.1 1.1 1.0 0.9Div Yield 4.4% 4.6% 4.8% 5.0%Net Debt (Euro mn) 38.5 47.4 44.9 45.2EV (Euro mn) 82.1 91.1 88.6 88.8Source Company & Beta estimates

BETA SECURITIES SA 114 73 ATHENS, GREECE, TEL. +302106478900 WEB PAGE: www.beta.gr E-MAIL: [email protected]

BETA SECURITIES SA BETANET SA

History - Short profile The company was established in 1982. It has been acquired early 1993 by the Civil Engineers Evangelos and Constantine Zavliaris, the major shareholders and managers of the company since the date of acquisition. The company is active in the production of precast concrete elements made up of high performance reinforced and pre stressed concrete, assembling single or multi story buildings of any kind of use and multiple infrastructure works as well. It holds a leading position in the precast concrete production in the Greek market, it is holding two production facilities one in Sximatari, Attica and one in Komotini Industrial Area. The company also participates by 25% in a third facility (SY.PRO S.A) located in Larisa, specified in the production of precast concrete sleepers for high speed trains. BETANET S.A. is also the unique ASE listed company of the Greek heavy precast sector.

Sectors of activity & Products

The company’s activities can be classified as follows:

1. Industrial Activities The company produces high-strength precast concrete elements, which are transported and assembled on site by means of cranes of specific technical characteristics. The final construction formed is permanent and of particular high anti seismic and fire resistance. The main fields of applications are:

Residences – City and country houses • • • • • • • •

Multi Story Buildings – Hotels, shopping centers, etc. Urban and Resort Hotels Industrial and Ware House Buildings – Logistics centers Buildings of specific use like churches and institutional use buildings Sports Facilities Products of use in infrastructure projects (tunnels, railway sleepers, spun poles, bridges) Other special products (BETATYP) for application in the conventional concrete structure.

Housing in Varkiza, Athens Multi storey hotel on Kifisias Avenue, Athens

Public School in Attica A class hotel complex in Rhodes

Logistics center in Attica Logistics center for the Greek Railways Organization

Page 2

BETA SECURITIES SA BETANET SA

2. Research & Development The company is involved also in continuously researching and developing special methods and prefabricated elements and products for new applications. For this reason BETANET S.A. cooperates with specialized international enterprises and organizations. In particular, the company has already participated in international research programs and task groups, funded by the European Union and has cooperated with many famous European Universities, technical institutes, contractors, etc. (e.g. Universities of Grenoble, Zurich, Aachen, Taylor Woodrow, Ciba-Geigy, etc.).

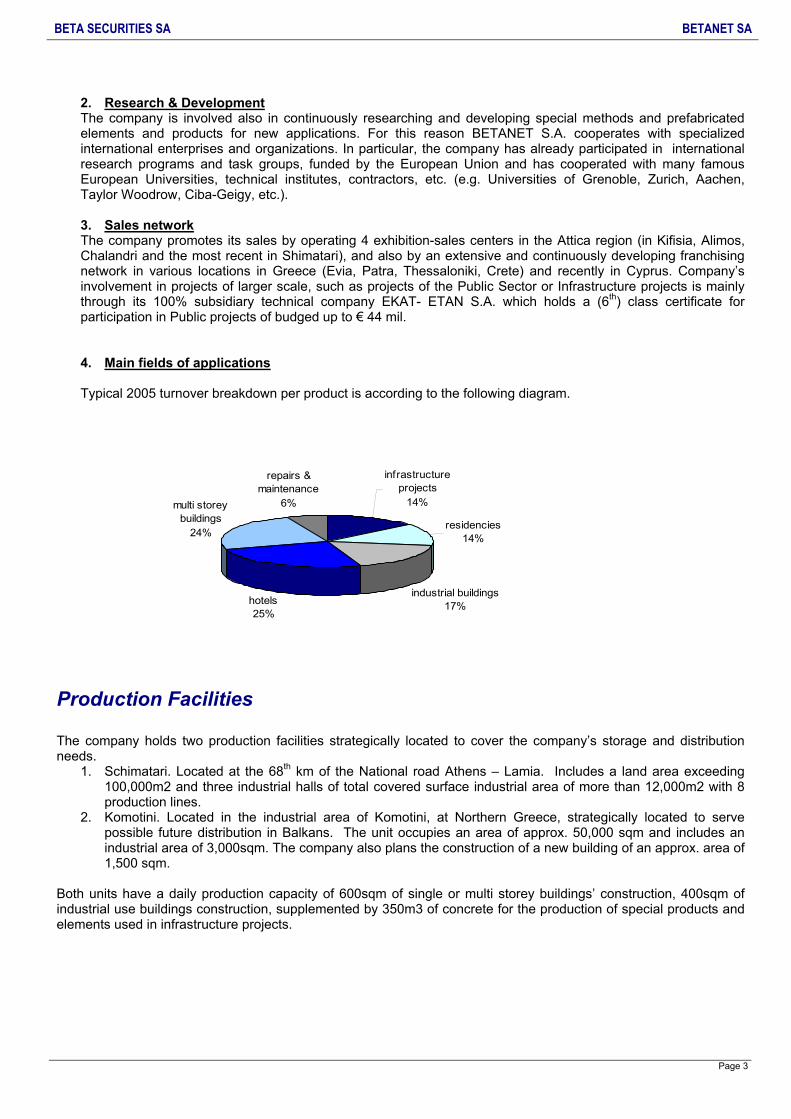

3. Sales network The company promotes its sales by operating 4 exhibition-sales centers in the Attica region (in Kifisia, Alimos, Chalandri and the most recent in Shimatari), and also by an extensive and continuously developing franchising network in various locations in Greece (Evia, Patra, Thessaloniki, Crete) and recently in Cyprus. Company’s involvement in projects of larger scale, such as projects of the Public Sector or Infrastructure projects is mainly through its 100% subsidiary technical company EKAT- ETAN S.A. which holds a (6th) class certificate for participation in Public projects of budged up to € 44 mil. 4. Main fields of applications Typical 2005 turnover breakdown per product is according to the following diagram.

infrastructure projects

14%

residencies14%

industrial buildings17%hotels

25%

multi storey buildings

24%

repairs & maintenance

6%

Production Facilities The company holds two production facilities strategically located to cover the company’s storage and distribution needs.

1. Schimatari. Located at the 68th km of the National road Athens – Lamia. Includes a land area exceeding 100,000m2 and three industrial halls of total covered surface industrial area of more than 12,000m2 with 8 production lines.

2. Komotini. Located in the industrial area of Komotini, at Northern Greece, strategically located to serve possible future distribution in Balkans. The unit occupies an area of approx. 50,000 sqm and includes an industrial area of 3,000sqm. The company also plans the construction of a new building of an approx. area of 1,500 sqm.

Both units have a daily production capacity of 600sqm of single or multi storey buildings’ construction, 400sqm of industrial use buildings construction, supplemented by 350m3 of concrete for the production of special products and elements used in infrastructure projects.

Page 3

BETA SECURITIES SA BETANET SA

BETANET systems’ superiority The company delivers finished projects which are assembled from high strength prefabricated concrete elements, which have increased resistance against earthquake and fire and high durability. Buildings are constructed only a few weeks after signing the contract, with a significantly low cost (20% lower than conventional constructions) and much shorter completion time (approximately 50%-60% less respectively).The project’s value is predetermined, without deviation and their operation and maintenance costs after the construction are particularly low. Projects – Recent Developments The number of projects for 2005 exceeds the 100, covering all the basic sectors of its activities (residences, hotels, industrial buildings, etc). The majority of the projects are for private clients (approximately 70% of total annual turnover. BETANET S.A’s main turnover comes from activities in Greece (55% Central Greece, 35% South Greece, and 10% North Greece) and a small part from activities abroad (Cyprus). During 2005 the company has undertaken an important project in Cyprus, which was completed early 2006, while it has submitted a number of tenders for projects in Balkans , Northern Europe, the Middle East and Africa. On December 4, the company announced its partnership with the Greek construction company DIEKAT S.A. for the construction of residences and other precast concrete projects in Romania. The new project will commerce during the first half of 2007. Both company’s will participate with a 50% stake in the venture. Table 1: Some major private and public projects Owner Project Plaisio SA Building complex for computer assembly, logistics and distribution facilities

center, in Magoula, Attica Katselis SA Storage facilities extension and deep freeze storage facilities in Acharnai, Attica. Golf Residencies SA A and B phase of a 4 Star furnished apartments complex, in Hersonissos, Crete Unilog SA Office and logistics center in Markopoulo Attica Demos SA New industrial Building in Krioneri, Attica Fashion car SA Exhibition center and car service area in Metamorphosi, Attiki”

Seracom SA Storage facilities of Michelin tires in Avlona, Attica Cybargo SA Supplementary construction of Lukas Hotels in Falliraki, Rhodes Athens 2004 Hellenic Olympic Committee Hotel in Kifisias Ave, Athens Athens 2004 Logistics facilities of National Railways in Thiasio, Attica MEGA SA Storage and Logistics facilities in Aharnes, Attica Athens METRO SA Precast segments rings for Sepolia – Peristeri line Athens Mental Hospital A new, complete and fully equipped mental unit General Foods SA New refrigeration chamber facilities in Salonica Public Power Coorporation Production of spun poles for their electric network across Greece Public Schools Organization Different school buildings throughout Greece

Page 4

BETA SECURITIES SA BETANET SA

Prefabricated Concrete Element Market The Prefabricated Concrete Element Market (PCE) exists at very early stages of development in Greece and BETANET S.A is the market leader. The ratio of the local PCE market comparing to the Construction market is expected to converge from the current low levels of less than 2% towards the European average (15% - 25%) in the next years. The current value of the PCE market is now estimated at € 80 mil. The competition is rather limited because only a few number of companies with similar activity exist, due to the lack of technical expertise and the high amounts of the necessary investments required. Apart from BETANET S.A. other companies in the field are: J&P Avax S.A., Edrasi Psalidas S.A, Asprocat S.A., Preconstructa S.A.etc. Construction activity Greek construction activity has risen consistently the last 10 years, up to 2004. After 2005 a slight recession followed the 2004 Olympics Games in Athens. Growth over the last ten years outpaced GDP growth yet facing constraints from the state’s desire to meet other economic objectives. Greece lags 25% behind the EU average. However we believe that Greek construction growth will take off in the next year as a result of :

Strong predictions for GDP growth in the next years (4%pa) • •

•

•

A new push for Greek hotel and tourism infrastructure in order to capture post Olympics appeal for tourism, as the most large investments were made over 20 years ago. Land planning restrictions have also reduced construction activity however we expect law simplifications in the future. New EU subsidies. Following the 3rd CSF, Greece will be eligible to receive € 20.1bn of subsidies (from 2009 until 2015) which will represent 50% of the project’s value. The construction sector is estimated to receive half of those subsidies. PPP (Public Private Partnership) projects are also under way. So far only a few large projects took place in Greece.

(Left blank intentionally)

Page 5

BETA SECURITIES SA BETANET SA

SWOT Analysis

Strengths:

Brand Recognition: The company enjoys a sound brand name in the Greek market. 1.

2.

3.

4.

5.

6.

7.

8.

Strong Management Team: The company’s management is comprised of professionals counting several years of experience in their respective fields, holding a strong academic background.

Private Clientele: The company’s private clientele accounts for a 70% approximately on total turnover and thus the company had limited impact on its effectiveness after the recession in the construction activity followed the post Olympic period.

System superiority: Compared to the conventional construction methods, BETANET S.A’s precast concrete building systems offer important advantages such as significantly reduced construction time, reduced costs, maximum quality, high durability, reduced maintenance costs and high aesthetics. BETANET S.A. also holds the new ISO 9001:2000 Quality Management System Certificate

Patents: The company has been awarded two patent diplomas regarding its precast concrete methods.

Awards: The Company was awarded a full membership (unique for Greece) by “BIBM” (Bureau International Du Beton Manufacture), the leading international organization in the precast concrete industry and is also listed among Europe’s 500 fastest growing companies for 2005 ( folowing the respective awarding of 2000, 2001, 2002 and 2003 ) as listed by the non-profit European Organization "Europe’s 500 Enterpreuners for Growth".

Strong distribution network and facilities: The company covers sales countrywide and holds a strong distribution network.

Market Leader: The company holds the leading position in the Greek prefabricated concrete elements market.

Weaknesses: 1. Highly leveraged: BETANET S.A’s performance in terms of profitability is quite satisfactory. The most important risk comes from the fact that it is highly leveraged. The company faces an average Net Debt-to-EBITDA ratio of 4.7x, which is considered as, relatively, high. Opportunities: 1. Increase of the building activity in Greece: An increase in the public sector projects and a potential upturn in the Greek building cycle will boost the company’s profitability. 2. Expansion in Balkans, Cyprus and Middle East: The company should take advantage of its already existing activities in N. Greece in order to expand in Balkans. Bulgaria and Romania face a real growth rate of 5.5% and 4.1% of GDP for 2005 respectively while prospects for future growth are excellent. Labor costs remain cheap and property taxation is still at low levels. Real estate activity is increasing as foreign investors are seeking modern buildings and residences to house their offices and personnel. Also through strategic alliances the company may expand in Cyprus and Middle East were the construction activity accelerates. 3. High margins of activity: Prefabricated sector (especially precast residential construction) is in early stages of development. 4. Housing Activity: During 2005, BETANET S.A has given particular emphasis on housing activity. We reckon this move as a step in the right direction, as the increasing demand in mortgages, during the last years betrays that housing remains a traditional yet popular investment for Greeks.

Page 6

BETA SECURITIES SA BETANET SA

5. Public projects: An increase in the public sector projects and a potential upturn in the Greek building cycle will boost the company’s profitability. 6. Office buildings activity: Athens lacks of big modern buildings. Many office buildings in the center of Athens are unoccupied as they do not include parking spaces or they do not cover the basic anti seismic regulations. We expect an upturn in the Greek office market in the years to come, as the demand for such buildings from international companies and Greek large caps companies will increase. Greece is expected to follow the dramatic increase for modern office facilities we have already observed in Balkans and Russia. 7. New points of sale: Precast concrete constructions are not widespread in Greece. The company may use marketing efforts in order to increase the number of its outlets in the coming years. Threats: 1. Limited trading volumes: Greek small cap stock often face limited interest and trading volumes. 2. Unstable international oil prices: Energy costs have negative effects on the company’s bottom line numbers due to the increase in transportation costs. 3. Domestic economic conditions: The building and construction activity in Greece is dependent by the country’s economic conditions and in particular on the sectors of Real Estate , Public and Private investments. 4. Expansion inability: We highlight the fact that the company may be unable to expand successfully in the potential markets mentioned above and ensure long term growth rates.

Page 7

BETA SECURITIES SA BETANET SA

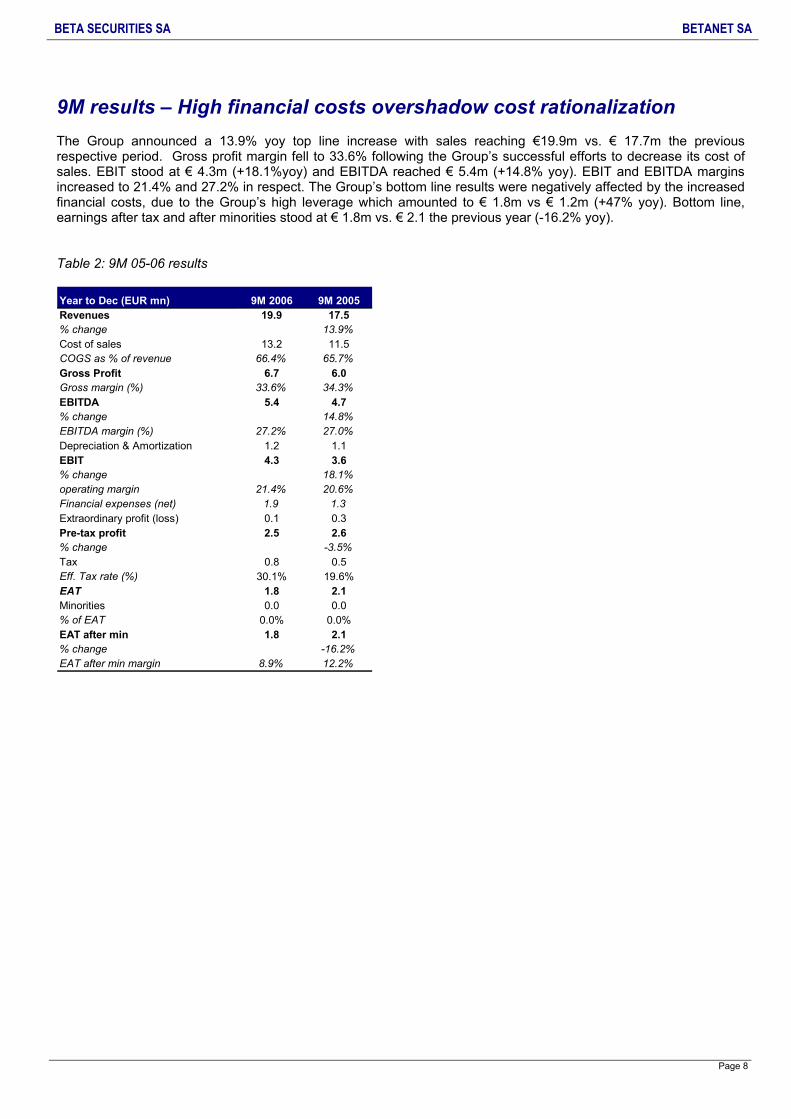

9M results – High financial costs overshadow cost rationalization The Group announced a 13.9% yoy top line increase with sales reaching €19.9m vs. € 17.7m the previous respective period. Gross profit margin fell to 33.6% following the Group’s successful efforts to decrease its cost of sales. EBIT stood at € 4.3m (+18.1%yoy) and EBITDA reached € 5.4m (+14.8% yoy). EBIT and EBITDA margins increased to 21.4% and 27.2% in respect. The Group’s bottom line results were negatively affected by the increased financial costs, due to the Group’s high leverage which amounted to € 1.8m vs € 1.2m (+47% yoy). Bottom line, earnings after tax and after minorities stood at € 1.8m vs. € 2.1 the previous year (-16.2% yoy). Table 2: 9M 05-06 results Year to Dec (EUR mn) 9M 2006 9M 2005Revenues 19.9 17.5% change 13.9%Cost of sales 13.2 11.5COGS as % of revenue 66.4% 65.7%Gross Profit 6.7 6.0Gross margin (%) 33.6% 34.3%EBITDA 5.4 4.7% change 14.8%EBITDA margin (%) 27.2% 27.0%Depreciation & Amortization 1.2 1.1EBIT 4.3 3.6% change 18.1%operating margin 21.4% 20.6%Financial expenses (net) 1.9 1.3Extraordinary profit (loss) 0.1 0.3Pre-tax profit 2.5 2.6% change -3.5%Tax 0.8 0.5Eff. Tax rate (%) 30.1% 19.6%EAT 1.8 2.1Minorities 0.0 0.0% of EAT 0.0% 0.0%EAT after min 1.8 2.1% change -16.2%EAT after min margin 8.9% 12.2%

Page 8

BETA SECURITIES SA BETANET SA

Valuation

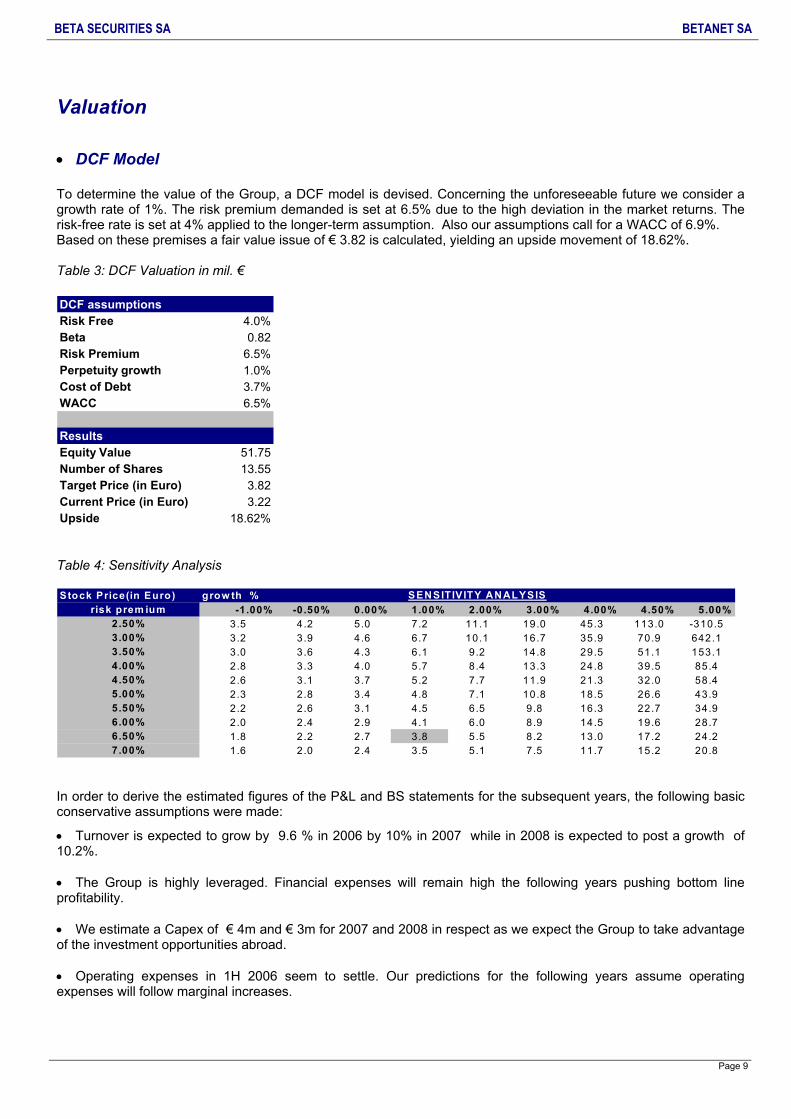

DCF Model • To determine the value of the Group, a DCF model is devised. Concerning the unforeseeable future we consider a growth rate of 1%. The risk premium demanded is set at 6.5% due to the high deviation in the market returns. The risk-free rate is set at 4% applied to the longer-term assumption. Also our assumptions call for a WACC of 6.9%. Based on these premises a fair value issue of € 3.82 is calculated, yielding an upside movement of 18.62%. Table 3: DCF Valuation in mil. € DCF assumptionsRisk Free 4.0%Beta 0.82Risk Premium 6.5%Perpetuity growth 1.0%Cost of Debt 3.7%WACC 6.5%

Results (mil. Euros)Equity Value 51.75Number of Shares 13.55Target Price (in Euro) 3.82Current Price (in Euro) 3.22Upside 18.62% Table 4: Sensitivity Analysis Stock Price(in Euro) grow th %

risk prem ium -1.00% -0.50% 0.00% 1.00% 2.00% 3.00% 4.00% 4.50% 5.00%2.50% 3.5 4.2 5.0 7.2 11.1 19.0 45.3 113.0 -310.53.00% 3.2 3.9 4.6 6.7 10.1 16.7 35.9 70.9 642.13.50% 3.0 3.6 4.3 6.1 9.2 14.8 29.5 51.1 153.14.00% 2.8 3.3 4.0 5.7 8.4 13.3 24.8 39.5 85.44.50% 2.6 3.1 3.7 5.2 7.7 11.9 21.3 32.0 58.45.00% 2.3 2.8 3.4 4.8 7.1 10.8 18.5 26.6 43.95.50% 2.2 2.6 3.1 4.5 6.5 9.8 16.3 22.7 34.96.00% 2.0 2.4 2.9 4.1 6.0 8.9 14.5 19.6 28.76.50% 1.8 2.2 2.7 3.8 5.5 8.2 13.0 17.2 24.27.00% 1.6 2.0 2.4 3.5 5.1 7.5 11.7 15.2 20.8

SENSITIVITY ANALYSIS

In order to derive the estimated figures of the P&L and BS statements for the subsequent years, the following basic conservative assumptions were made:

• Turnover is expected to grow by 9.6 % in 2006 by 10% in 2007 while in 2008 is expected to post a growth of 10.2%. • The Group is highly leveraged. Financial expenses will remain high the following years pushing bottom line profitability. • We estimate a Capex of € 4m and € 3m for 2007 and 2008 in respect as we expect the Group to take advantage of the investment opportunities abroad. • Operating expenses in 1H 2006 seem to settle. Our predictions for the following years assume operating expenses will follow marginal increases.

Page 9

BETA SECURITIES SA BETANET SA

• 3Q06 results indicate a slow down in profitability for the whole year. In 2007 we expect a recovery with eps increasing by 7.8% yoy while eps in 2007 will follow a 15.8% yoy increase. Our View on the Stock We are positive on the stock taking into consideration the management’s ability to increase profitability by expanding in Balkans and try to keep operating expenses at stable levels. Based on current prices the company’s stock trades at a 2006e 11 multiple. Taking into consideration the associated risks we give a BUY recommendation.

(Left blank intentionally)

Page 10

BETA SECURITIES SA BETANET SA

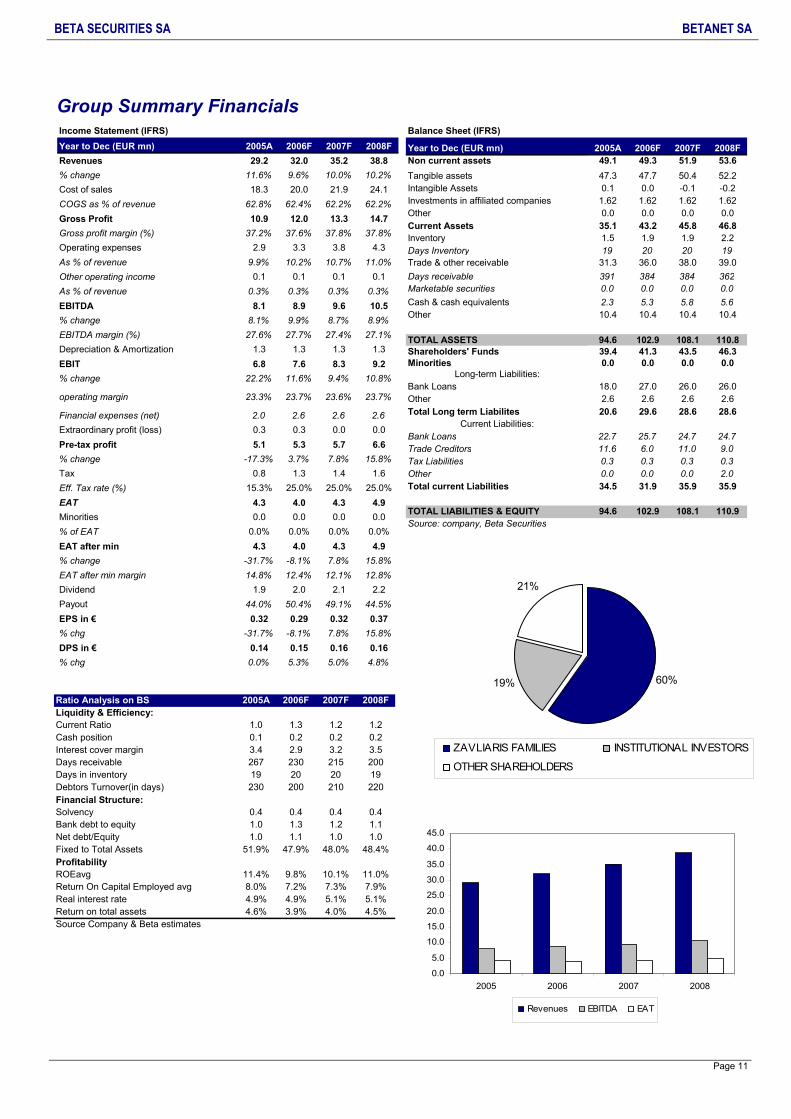

Group Summary Financials

Page 11

Income Statement (IFRS)Year to Dec (EUR mn) 2005A 2006F 2007F 2008FRevenues 29.2 32.0 35.2 38.8% change 11.6% 9.6% 10.0% 10.2%Cost of sales 18.3 20.0 21.9 24.1COGS as % of revenue 62.8% 62.4% 62.2% 62.2%Gross Profit 10.9 12.0 13.3 14.7Gross profit margin (%) 37.2% 37.6% 37.8% 37.8%Operating expenses 2.9 3.3 3.8 4.3As % of revenue 9.9% 10.2% 10.7% 11.0%Other operating income 0.1 0.1 0.1 0.1As % of revenue 0.3% 0.3% 0.3% 0.3%EBITDA 8.1 8.9 9.6 10.5% change 8.1% 9.9% 8.7% 8.9%EBITDA margin (%) 27.6% 27.7% 27.4% 27.1%Depreciation & Amortization 1.3 1.3 1.3 1.3EBIT 6.8 7.6 8.3 9.2% change 22.2% 11.6% 9.4% 10.8%

operating margin 23.3% 23.7% 23.6% 23.7%

Financial expenses (net) 2.0 2.6 2.6 2.6Extraordinary profit (loss) 0.3 0.3 0.0 0.0Pre-tax profit 5.1 5.3 5.7 6.6% change -17.3% 3.7% 7.8% 15.8%Tax 0.8 1.3 1.4 1.6Eff. Tax rate (%) 15.3% 25.0% 25.0% 25.0%EAT 4.3 4.0 4.3 4.9Minorities 0.0 0.0 0.0 0.0% of EAT 0.0% 0.0% 0.0% 0.0%EAT after min 4.3 4.0 4.3 4.9% change -31.7% -8.1% 7.8% 15.8%EAT after min margin 14.8% 12.4% 12.1% 12.8%Dividend 1.9 2.0 2.1 2.2Payout 44.0% 50.4% 49.1% 44.5%EPS in € 0.32 0.29 0.32 0.37% chg -31.7% -8.1% 7.8% 15.8%DPS in € 0.14 0.15 0.16 0.16% chg 0.0% 5.3% 5.0% 4.8%

Balance Sheet (IFRS)

Year to Dec (EUR mn) 2005A 2006F 2007F 2008FNon current assets 49.1 49.3 51.9 53.6Tangible assets 47.3 47.7 50.4 52.2Intangible Assets 0.1 0.0 -0.1 -0.2Investments in affiliated companies 1.62 1.62 1.62 1.62Other 0.0 0.0 0.0 0.0Current Assets 35.1 43.2 45.8 46.8Inventory 1.5 1.9 1.9 2.2Days Inventory 19 20 20 19Trade & other receivable 31.3 36.0 38.0 39.0Days receivable 391 384 384 362Marketable securities 0.0 0.0 0.0 0.0Cash & cash equivalents 2.3 5.3 5.8 5.6Other 10.4 10.4 10.4 10.4

TOTAL ASSETS 94.6 102.9 108.1 110.8Shareholders' Funds 39.4 41.3 43.5 46.3Minorities 0.0 0.0 0.0 0.0

Long-term Liabilities:Bank Loans 18.0 27.0 26.0 26.0Other 2.6 2.6 2.6 2.6Total Long term Liabilites 20.6 29.6 28.6 28.6

Current Liabilities:Bank Loans 22.7 25.7 24.7 24.7Trade Creditors 11.6 6.0 11.0 9.0Tax Liabilities 0.3 0.3 0.3 0.3Other 0.0 0.0 0.0 2.0Total current Liabilities 34.5 31.9 35.9 35.9

TOTAL LIABILITIES & EQUITY 94.6 102.9 108.1 110.9Source: company, Beta Securities

60%19%

21%

ZAVLIARIS FAMILIES INSTITUTIONAL INVESTORS

OTHER SHAREHOLDERS

4.5%4.0%3.9%4.6%Return on total assets5.1%5.1%4.9%4.9%

11.0%7.9%

10.1%7.3%

9.8%7.2%

11.4%8.0%

48.4%48.0%47.9%51.9%1.01.01.11.0

0.41.1

0.41.2

0.41.3

0.41.0

Financial Structure:Solvency Bank debt to equityNet debt/Equity Fixed to Total AssetsProfitability ROEavg Return On Capital Employed avg Real interest rate

220210200230Debtors Turnover(in days)20 192019Days in inventory

3.5200

3.2215

2.9230

3.4267

Interest cover marginDays receivable

0.20.20.20.1Cash position1.21.21.31.0

2008F2007F2006F2005ARatio Analysis on BS Liquidity & Efficiency: Current Ratio

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2005 2006 2007 2008

Revenues EBITDA EAT

Source Company & Beta estimates

BETA SECURITIES SA BETANET SA

Disclaimer: Beta Securities SA does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm might have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Beta Securities SA has prepared the above research material and its contents are for information purposes only and should not be construed as an offer to sell or a solicitation to buy any securities. Beta Securities SA or persons connected with it and/or directors and/or employees and/or clients may have a position, make markets, or engage in transactions in any of the securities mentioned herein or any related investment, or solicit business from any company mentioned herein. The information or opinions contained in this report have been obtained or compiled from sources that Beta Securities SA believes to be reliable, but their accuracy, completeness or correctness cannot be guaranteed and are subject to change without further notice. The report is intended for professional investors only and it is not to be reproduced or copied or reprinted or transmitted for any purpose. Beta Securities SA does not accept any liability whatsoever for any direct or consequential loss arising from any use of this document or this contents. This publication is issued in Greece by Beta Securities SA, which is a member of the Athens Stock Exchange regulated by the Hellenic Capital Market Commission and the Athens Exchange authorities. BETA SECURITIES SA – Alexandras Avenue 29, PC 114 73, Athens, Greece, Tel: +30-210-6478900, Fax +30 – 210-6448791 Ε-mail: [email protected] Disclosure Appendix Analyst Certification The analyst responsible for the content of this research report (in whole or in part), certifies that a) all the views about the companies and securities contained in this report accurately reflect our personal views and b) no part of our compensation was or will be directly or indirectly related to the specific recommendations or view of this report Important Regulatory Disclosures on Subject Company The information and opinions in this report were prepared by Beta Securities SA, a member of the Athens Exchange SA and regulated by the Hellenic Capital Market Commission. Company Mentioned: Betanet Rating: BUY Price: €3.22 Target Price: €3.82 Disclosures: 3

1. Beta Securities SA owns 5% or more of the total share capital of the company 2. The company covered in the report and its affiliated companies own 5% or more of the total share capital of Beta Securities SA 3. Beta Securities SA acts as a market maker for the securities of the company 4. Beta Securities SA has provided underwriting services to the company covered in the report 5. Beta Securities has received compensation from the company for financial advisory services during the past 12 months 6. Beta Securities has received compensation from the company for the preparation of the research report 7. The research analysts who prepared this report have financial interests in the company

Internal procedures: a) The research department is situated in an area where only employees of the department have access in order to ensure secured confidentiality. The data and records of the department are out of reach of the other departments. Chinese Walls are set between the research department and other departments so that Beta Securities SA can abide by the provisions regarding confidential information and market abuse. Analyst Stock Ratings In purpose of determining the relative performance of the stock a Sharpe ratio analysis is used. Stock Sharpe ratio=(Upside potential-risk free rate)/volatility of the stock Market Sharpe ratio=Risk premium/volatility of the market S=Stock Sharpe ratio/Market Sharpe ratio

S>10<S<1 S<0

The volatility is calculated using historical data Buy: S>1 Hold: 0<S<1 Sell: S<0

BETA SECURITIES SA – Alexandras Avenue 29, PC 114 73, Athens, Greece, Tel: +30-210-6478900, Fax +30 – 210-6448791 Ε-mail: [email protected] Web site: www.beta.gr Bloomberg Page: BTGR

Page 12

Research Dept : Vassilis Vlastarakis, Elena Chatzistefanou, George Drakopoulos