2015 LEADINGAGE MICHIGAN ANNUAL …...organizations • Largest 150 “LZ 150” range from 18,286...

69

2015 MEGA TRENDS IN SENIOR LIVING (W1) 2015 LEADINGAGE MICHIGAN ANNUAL LEADERSHIP INSTITUTE Ι AUGUST 12-15, 2015 B.C. Ziegler and Company | Member of SIPC & FINRA T OM MEYERS Managing Director 312-596-1537 [email protected] PRESENTED BY: August 12, 2015

Transcript of 2015 LEADINGAGE MICHIGAN ANNUAL …...organizations • Largest 150 “LZ 150” range from 18,286...

2015 MEGA TRENDS IN SENIOR LIVING (W1)2015 LEADINGAGE MICHIGAN ANNUAL LEADERSHIP INSTITUTE Ι AUGUST 12-15, 2015

B.C. Ziegler and Company | Member of SIPC & FINRA

TOM MEYERSManaging [email protected]

PRESENTED BY:

August 12, 2015

DISCLOSURE LANGUAGE1. The information contained herein is intended to be general, factual, and educational in nature, and does not reflect any

assumptions, opinions, or views of B.C. Ziegler and Company (“Ziegler”) with respect to the recipient municipal entity’s or obligated person’s particular situation. Further,

a) Ziegler is not recommending an action to the municipal entity or obligated person; b) Ziegler is not acting as an advisor to the municipal entity or obligated person and does not owe a fiduciary duty pursuant

to Section 15B of the Exchange Act to the municipal entity or obligated person with respect to the information and material contained in this communication;

c) Ziegler is acting for its own interests; andd) The municipal entity or obligated person should discuss any information and material contained in this communication

with any and all internal or external advisors and experts that the municipal entity or obligated person deems appropriate before acting on this information or material.

2. B.C. Ziegler and Company (“Ziegler”) seeks to serve as an underwriter on a future transaction and not as a financial advisor or municipal advisor. The information provided is for discussion purposes only in anticipation of being engaged to serve as underwriter.

3

Ziegler is one of the nation’s oldest and largest investment banking firms serving healthcare providers

• Full service financial services firm• Founded in 1902 with a focus on

healthcare since 1928– Over 350 professionals and support

staff dedicated to serving our clients

• National presence, demonstrated execution expertise and broad-based experience

• Strong underwriting and sales & trading capabilities.

– Primary and secondary market efforts focused exclusively on muni sector

• Ziegler’s mission is to provide tailored financial solutions

• Ziegler’s goal is to be our client’s trusted advisor and partner

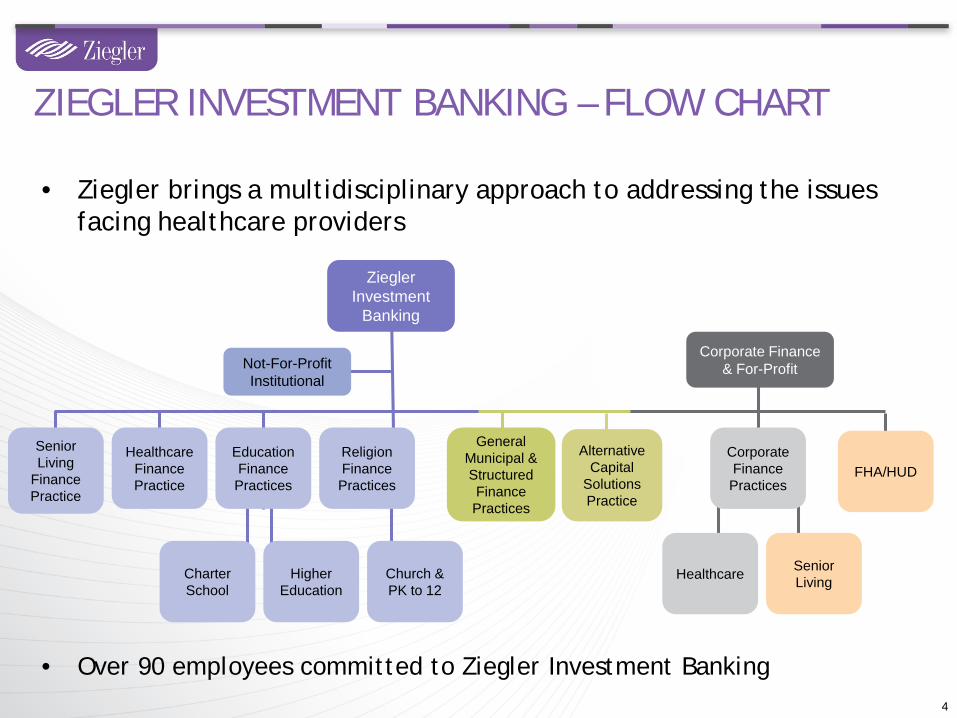

WHO IS ZIEGLER?

4

• Over 90 employees committed to Ziegler Investment Banking

• Ziegler brings a multidisciplinary approach to addressing the issues facing healthcare providers

ZIEGLER INVESTMENT BANKING – FLOW CHART

Ziegler Investment

Banking

Senior Living

Finance Practice

Not-For-Profit Institutional

Healthcare Finance Practice

Charter School

Higher Education

EducationFinance Practices

ReligionFinance Practices

Church & PK to 12

General Municipal &Structured Finance Practices

Healthcare

Corporate Finance & For-Profit

CorporateFinance Practices

AlternativeCapital

Solutions Practice

Senior Living

FHA/HUD

CORPORATE FINANCE-SL:Bill Mulligan, Managing DirectorDan Revie, Senior Vice President

CORPORATE FINANCE-HC:Neil Borg, Managing DirectorChris Hendrickson, Senior Vice President

SENIOR LIVING RESEARCH & DEVELOPMENTLisa McCracken, Senior Vice President

Senior Living Research and DevelopmentCathy Owen, Senior Research AssociateKat Dymond, Research Analyst Ι Event Coordinator

INTEREST RATE PRODUCTS:Craig Naish, Managing DirectorScott Determan, DirectorMaureen Egan, Trading SpecialistFHA/HOUSING:Bill Mulligan, Managing DirectorJeremy Frankel, Senior Vice PresidentBernie Gawley, SVP, Sr HUD Underwriter

ZIEGLER CAPITAL MANAGEMENT:(Not a part of Ziegler)Scott Roberts, Senior Managing DirectorCraig Vanucci, Managing DirectorPaula Horn, Managing DirectorMatt O’Neil, Senior Vice PresidentKevin Carlson, Senior Vice President

West

Southeast Gulf States

Midwest

North-East

Mid-Atlantic

5

SENIOR LIVING FINANCE PRACTICENATIONAL COVERAGE - REGIONAL AND PRODUCT FOCUS

Midwest: (312) 263-0110Dan Hermann, Senior Managing Director,

Head of Investment BankingTom Meyers, Managing DirectorWill Carney, Managing DirectorSteve Johnson, Managing DirectorJennifer Lavelle, DirectorMatt Mulé, AssociateMichael Montgomery, Senior AnalystJason Choi, Senior AnalystSravanthi Putumbaka, Senior AnalystReanae Seth, Analyst

Mid-Atlantic: (312) 705:Michael Kelly, Managing Director (7260)Steve Jeffrey, Managing Director (7265)Amy Castleberry, Senior Vice President (7258)(804) 793:Tommy Brewer, Managing Director (8490)Tad Melton, Director (8487)Adam Garcia, Vice President (8495)Thomas Rogers, Analyst (8496)

West: (800) 327-3666Mary Muñoz, Managing DirectorSarkis Garabedian, Senior Vice PresidentDaren Bell, Vice President

Southeast Gulf States:Rich Scanlon, Managing Director: 312-596-1572Brandon Powell, Director: 804-793-8499Terry Herndon, Director: 312-705-7340

Northeast: (212) 512-0400Keith Robertson, Managing DirectorChad Himel, DirectorTyler Simons, Assistant Vice President

6

• 2015 MEGA TRENDS IN SENIOR LIVING

TOPIC 1

• QUICK SENIOR LIVING CAPITAL MARKETS UPDATE

TOPIC 2

DISCUSSION

AGENDA

TOPIC 1: 2015 MEGA TRENDS IN SENIOR LIVING

8

GROWTH DEFINED

Expansions/ Repositions

New Community Locations

Growth

Sponsorship Transitions/ Affiliations

For-profit Ventures

HCBSOfferings

Joint Ventures

9

• LeadingAge and Ziegler partner each year to identify the size & growth of not-for-profit senior living systems• Additional listings for single-sites

and affordable housing

• 2014 publication marks the 11th year• Expansion to the largest 150 NFP

organizations

• Largest 150 “LZ 150” range from 18,286 to 550 total market-rate units

• Largest 150 represent a total of 1,140 total market-rate properties• 600 total CCRCs, which accounts for

40% of the total CCRCs in the country

Source: 2014 LeadingAge Ziegler 150 Publication

• Full report available on Ziegler and LeadingAge websites

NFP TRENDS: 2014 LZ 150 PUBLICATION

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

220,000

1980 1985 1990 1995 2000 2005 2010

Uni

ts

Year

ILU ALU NCB All Units

2014 LZ 150GROWTH: GROWTH OF LARGEST 100 SYSTEMS, COMBINED UNIT MIXFROM 1980 (EXCLUDES EVANGELICAL LUTHERAN GOOD SAMARITAN SOCIETY)

Partial histories used if complete data was unavailable

Source: 2014 LeadingAge Ziegler 100 Publication (data as of 12/31/13) 10

0

200

400

600

800

1,000

1,200

1980-1989 1990-1999 2000-2009 2010-2013 2013

Expansions New Communities Merg/Acq/Affil Dispositions

SYSTEM TRENDS 2014: TYPE OF GROWTH2014 LZ 100: Types of Growth

10 YearsLast Year

4 Years

Source: 2014 LeadingAge Ziegler 150 Publication (data as of 12/31/13) 11

12

CT - 28

DE - 12

MA - 31

NJ - 39

MD - 42

1,930 Total CCRCs

18

36

133

11228

23

107

67

70

74 20

62

39

51

4

63

57

149

21

23

192

41

31

49

59

91

9

HI - 5

6

4 6

19

NH - 19

11

26

23

16

DC - 6

8

7

RI - 8

1

VT - 2

1 to 25

26 to 50

51 to 75

76 to 100

Over 100

None

Source: Ziegler Investment Banking, as of 3/20/15

ZIEGLER NATIONAL CCRC DATABASENUMBER OF CCRCS PER STATE

0

20

40

60

80

100

120

140

160

180

200

621

46 51 43 5170

9269 65 74

94

3654

28

52

85 7074

9381

89

5446 33

10

9

15

Loca

tions

Purpose built Non-purpose built

73

131121 117

144 151

181

123111 107 104

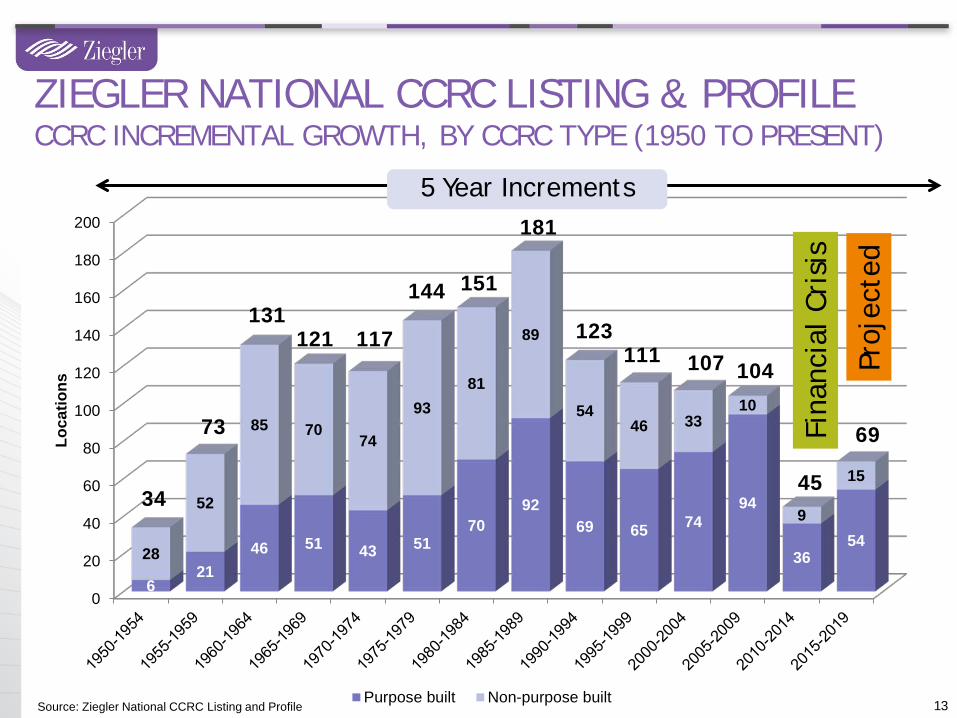

Source: Ziegler National CCRC Listing and Profile

45

Proj

ecte

d

5 Year Increments

Fina

ncia

l Cri

sis

34

69

ZIEGLER NATIONAL CCRC LISTING & PROFILECCRC INCREMENTAL GROWTH, BY CCRC TYPE (1950 TO PRESENT)

13

1414

CT - 2

DE

MA - 1

NJ - 2

MD - 3

83 in Total

52

4

5

2

2

2 2

4

25

11

2

1

2

3

2

2

5HI - 1

1

1 NH

1

1

1

DC

1

RI - 1

VT - 1

Source: Ziegler Investment Banking and Public Sources 7/8/15

3

2

TRACKING NEW CCRC GROWTHAT VARYING STAGES OF PLANNING

FP, 30.8

%

NFP, 69.2%

Future CCRCs: Profit Mix

2

• System dominance is greater in the FP sector (76% have more than one property)

• For NFPs, post-2000, 74% of new CCRCs were sponsored by multi-site organizations• 78% for 2010 YTD

• Single-sites opening during this time period, primarily sponsored by:• Hospital/health system• Religious entity w/ capital

(religious order, Federation)• Foundation or benefactor

• Estimated 125 managed by third party, primarily single-sites

SOURCE: Ziegler National CCRC Listing, as of 8/15/14

45% 44% 44% 43% 42% 41% 40%

55% 56% 56% 57% 58% 59% 60%

0%

10%

20%

30%

40%

50%

60%

70%

1985 1990 1995 2000 2005 2010 2014

Not-For-Profit CCRCs

Single-site Multi-site

SENIOR LIVING CCRC TRENDSNFP MARKET SHARE: SYSTEMS VS. SINGLE-SITES

15

CURRENT LZ 150 THAT GREW INTO MULTI-SITES IN PAST 15 YEARS (2000-2015)#23 Shell Point (FL) – Affiliation#30 Senior Quality Lifestyles Corporation (TX) – Development#31 Concordia Lutheran Ministries (PA) – Acquisition, Affiliation#48 Greencroft Communities (IN) – Affiliation#54 Lutheran Life Communities (IL) – Affiliation & Development#57 Friendship Senior Options (IL) – Development#58 SantaFe Senior Living (FL) – Affiliation & Development#80 United Methodist Memorial Home (IN) - Development#85 Liberty Lutheran (PA) – Affiliation#86 VMP (WI) - Affiliation#87 Oakwood Village Retirement Communities (WI) - Development#88 Westminster Ingleside Retirement Communities (DC) – Development#89 St. Ann’s Community (NY) - Development#91 Living Branches (PA) – Affiliation#93 Simpson Senior Services (PA) – Affiliation & Development#98 Givens Estates (NC) – Acquisition#108 Garden Spot Village (PA) – Affiliation#115 Landis Communities (PA) – Acquisition & Development#117 Saint Therese (MN) – Development#120 Masonic Homes of Kentucky (KY) – Development#121 Messiah Lifeways (PA) – Affiliation#133 The Loomis Communities - Affiliation#134 Heritage Ministries (NY) – Affiliation#149 Medford Leas (NJ) - Affiliation

16

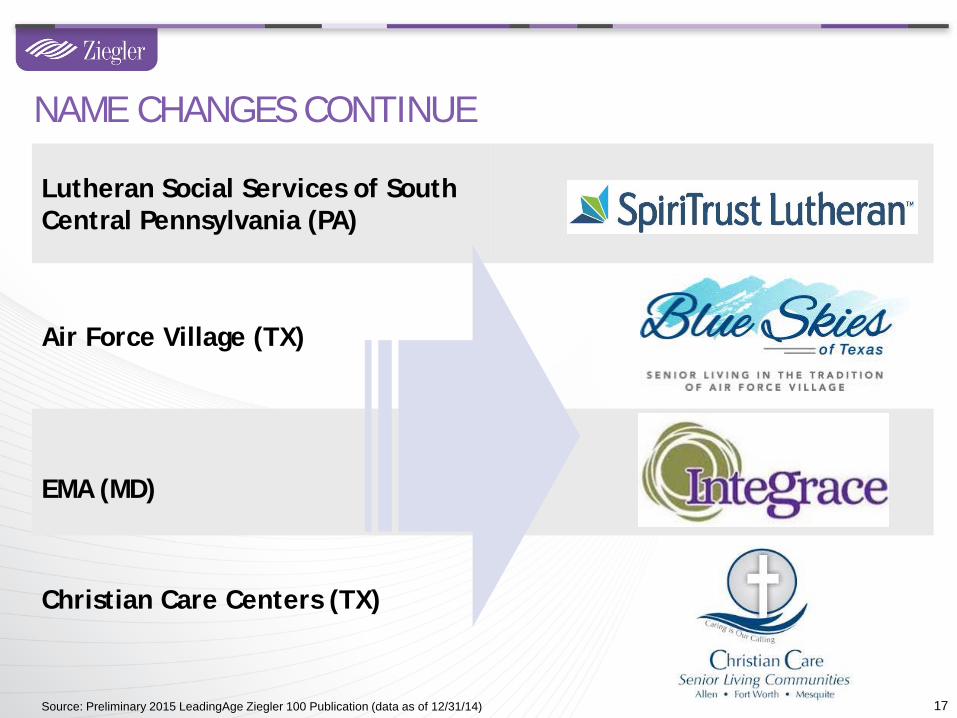

Lutheran Social Services of SouthCentral Pennsylvania (PA)

Air Force Village (TX)

EMA (MD)

Christian Care Centers (TX)

NAME CHANGES CONTINUE

Source: Preliminary 2015 LeadingAge Ziegler 100 Publication (data as of 12/31/14) 17

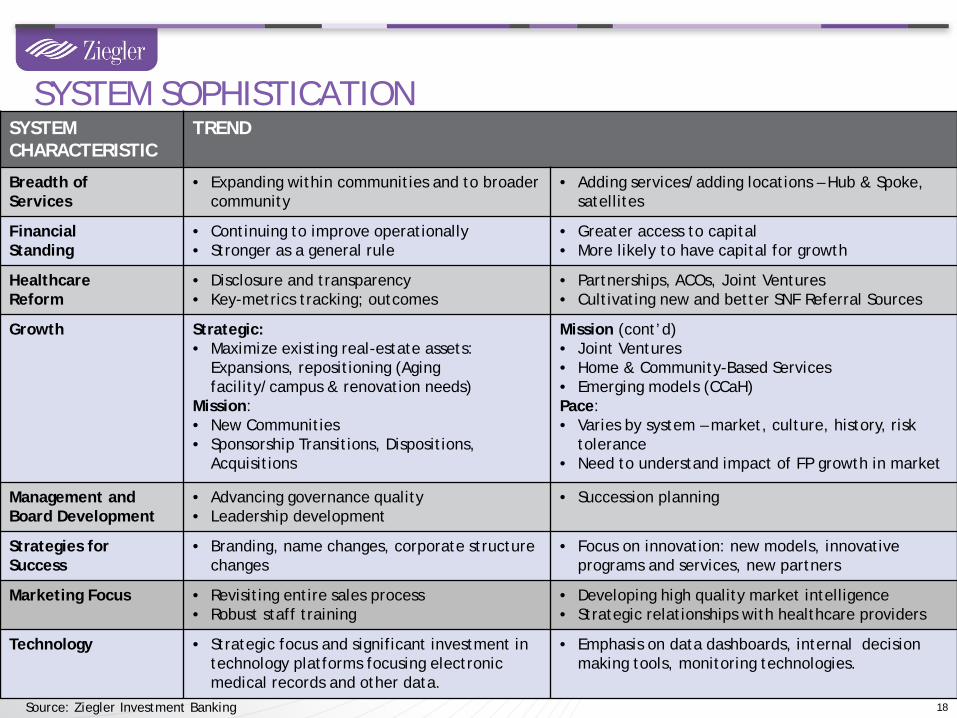

SYSTEMCHARACTERISTIC

TREND

Breadth ofServices

• Expanding within communities and to broader community

• Adding services/adding locations – Hub & Spoke, satellites

FinancialStanding

• Continuing to improve operationally• Stronger as a general rule

• Greater access to capital• More likely to have capital for growth

Healthcare Reform

• Disclosure and transparency• Key-metrics tracking; outcomes

• Partnerships, ACOs, Joint Ventures• Cultivating new and better SNF Referral Sources

Growth Strategic:• Maximize existing real-estate assets:

Expansions, repositioning (Aging facility/campus & renovation needs)

Mission:• New Communities• Sponsorship Transitions, Dispositions,

Acquisitions

Mission (cont’d)• Joint Ventures• Home & Community-Based Services• Emerging models (CCaH)Pace:• Varies by system – market, culture, history, risk

tolerance• Need to understand impact of FP growth in market

Management and Board Development

• Advancing governance quality• Leadership development

• Succession planning

Strategies forSuccess

• Branding, name changes, corporate structure changes

• Focus on innovation: new models, innovative programs and services, new partners

Marketing Focus • Revisiting entire sales process• Robust staff training

• Developing high quality market intelligence• Strategic relationships with healthcare providers

Technology • Strategic focus and significant investment in technology platforms focusing electronic medical records and other data.

• Emphasis on data dashboards, internal decision making tools, monitoring technologies.

18

SYSTEM SOPHISTICATION

Source: Ziegler Investment Banking

AFFILIATION & SPONSORSHIP TRANSITION ACTIVITY

• Pace of consolidation activity is dramatic, both in the for-profit and not-for-profit space

• Multi-site organizations recognizing that growth through sponsorship transition can accelerate pace and is less costly than new campus development

• Single-site providers wanting to benefit from greater scale and sophistication of larger organizations

• Increasingly a consideration when looking to replace a CEO vacancy or plan for succession

19

-10

10

30

50

70

90

110

2010 2011 2012 2013 2014 2015 YTD

Total NFP Owner/Sponsor Transactions

PRO

JEC

TED

90+

Source: Ziegler Investment Banking 5/8/15 20

INCREASING ACTIVITY IN NOT-FOR-PROFITAFFILIATIONS, DISPOSITIONS, SPONSORSHIP TRANSITIONS

21

TYPE OF NOT-FOR-PROFIT TRANSACTIONNFP CHANGE OF OWNER TRANSACTIONS: 2010-2015 YTD

5.1%

9.7%

20.9%

64.3%

FP to NFP

Closure

NFP toNFP

NFP to FP

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0% 100.0%

N=41

N=19

10

Source: Ziegler Investment Banking, 5/15/2015

199 total transactions

N=126

22

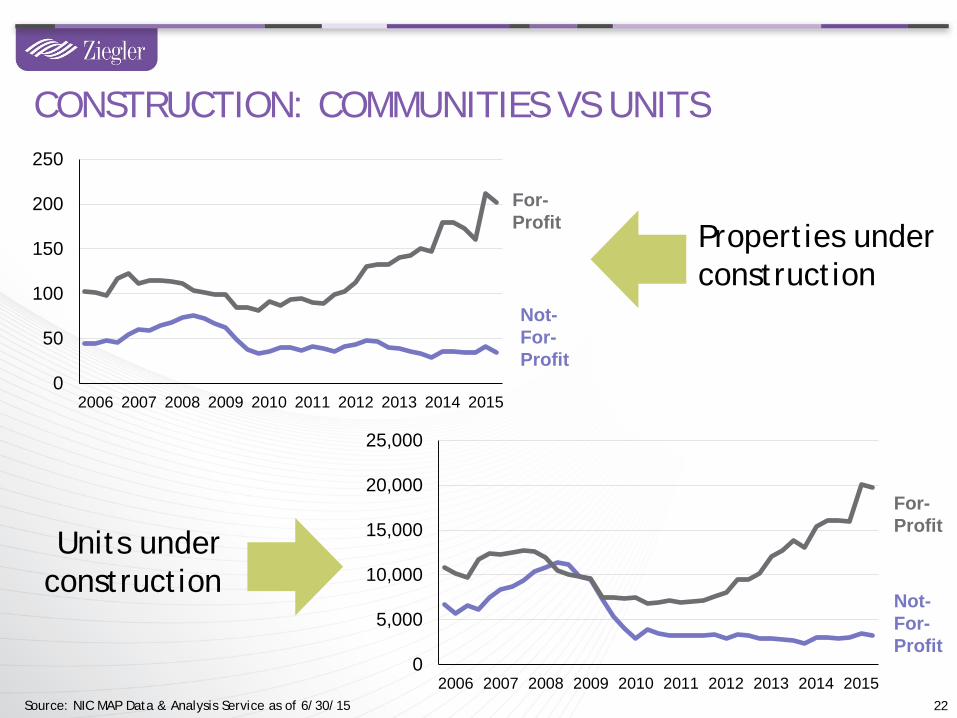

Properties under construction

Units under construction

CONSTRUCTION: COMMUNITIES VS UNITS

Source: NIC MAP Data & Analysis Service as of 6/30/15

0

50

100

150

200

250

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Not-For-Profit

For-Profit

0

5,000

10,000

15,000

20,000

25,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Not-For-Profit

For-Profit

Company Headquarters Properties UnitsBrookdale Senior Living Inc. Brentwood, TN 647 66,333

Emeritus Senior Living Seattle, WA 499 45,296

Holiday Retirement Lake Oswego, OR 307 37,488

LCS Des Moines, IA 119 31,792

Five Star Senior Living Newton, MA 226 27,348

Sunrise Senior Living, LLC McLean, VA 246 22,700

Erickson Living Baltimore, MD 17 20,118

Atria Senior Living, Inc. Louisville, KY 150 17,469

Senior Lifestyle Corporation Chicago, IL 163 16,811

Evangelical Good Samaritan Society Sioux Falls, SD 132 16,336

Capital Senior Living Corporation Dallas, TX 113 11,582

ACTS Retirement-Life Communities West Point, PA 23 8,000

Presbyterian Homes & Services Roseville, MN 41 7,026

Meridian Senior Living Hickory, NC 137 6,937

Watermark Retirement Communities, Inc. Tucson, AZ 33 6,704

Source: 2014 American Seniors Housing Association, “ASHA 50”

15 LARGEST SENIOR LIVING OPERATORS

23

Company Headquarters Properties UnitsVentas Inc. Chicago, IL 695 61,938

Health Care REIT Inc. Toledo, OH 572 56,479

Brookdale Senior Living Inc. Brentwood, TN 647 66,333

HCP Inc. Irvine, CA 444 45,580

Boston Capital Boston, MA 512 30,794

Senior Housing Properties Trust Newton, MA 217 26,671

Holiday Retirement Lake Oswego, OR 307 37,488

Emeritus Senior Living Seattle, WA 499 45,296

Evangelical Good Samaritan Society Sioux Falls, SD 132 16,336

Senior Lifestyle Corporation Chicago, IL 163 16,811

Harrison Street Real Estate Capital Chicago, IL 103 11,669

Highridge Costa Companies Gardena, CA 89 8,597

ACTS Retirement-Life Communities West Point, PA 23 8,000

CNL Orlando, FL 86 7,843

Enlivant Chicago, IL 172 7,812

Source: 2014 American Seniors Housing Association, “ASHA 50”

15 LARGEST SENIOR LIVING OWNERS

24

25

NOT-FOR-PROFIT CCRCS BY STATE

95% - 100%90% - 94%85% - 89%80% - 84%75% - 79%70% - 74%Below 70%

Source: Ziegler Investment Banking, as of 2/10/15

26

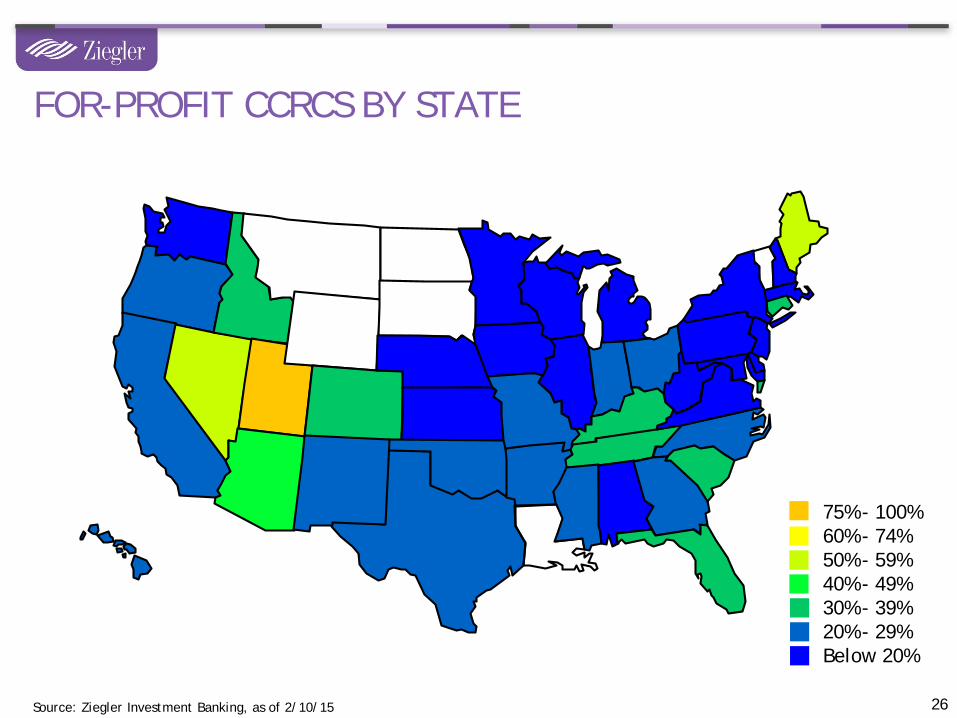

FOR-PROFIT CCRCS BY STATE

75% - 100%60% - 74%50% - 59%40% - 49%30% - 39%20% - 29%Below 20%

Source: Ziegler Investment Banking, as of 2/10/15

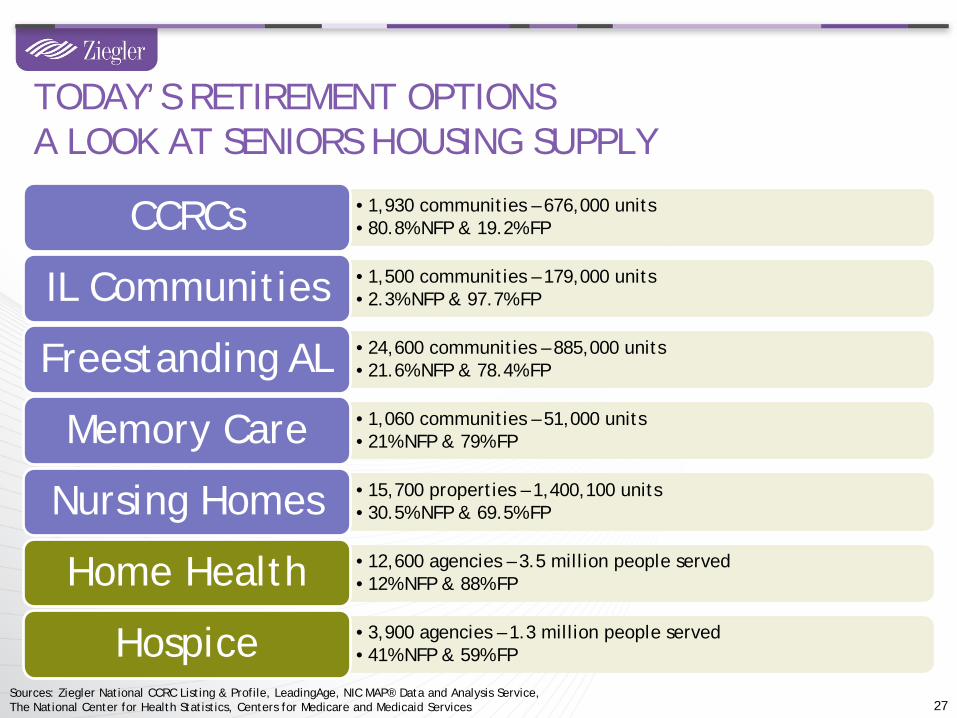

TODAY’S RETIREMENT OPTIONSA LOOK AT SENIORS HOUSING SUPPLY

27Sources: Ziegler National CCRC Listing & Profile, LeadingAge, NIC MAP® Data and Analysis Service, The National Center for Health Statistics, Centers for Medicare and Medicaid Services

•1,930 communities – 676,000 units•80.8% NFP & 19.2% FPCCRCs•1,500 communities – 179,000 units•2.3% NFP & 97.7% FPIL Communities•24,600 communities – 885,000 units•21.6% NFP & 78.4% FPFreestanding AL•1,060 communities – 51,000 units•21% NFP & 79% FPMemory Care•15,700 properties – 1,400,100 units•30.5% NFP & 69.5% FPNursing Homes•12,600 agencies – 3.5 million people served•12% NFP & 88% FPHome Health•3,900 agencies – 1.3 million people served•41% NFP & 59% FPHospice

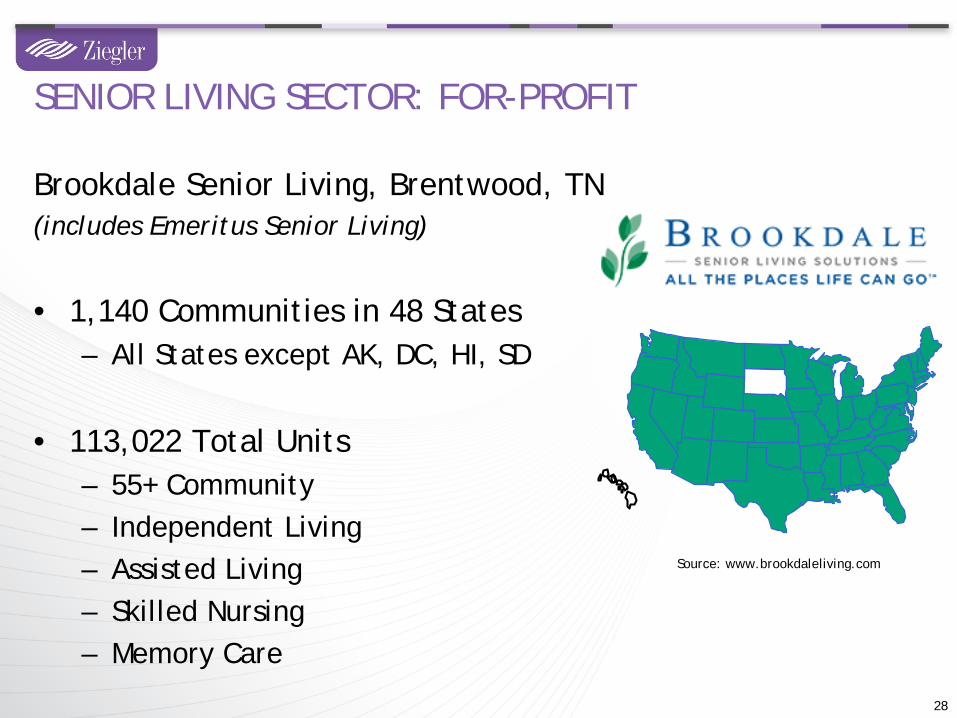

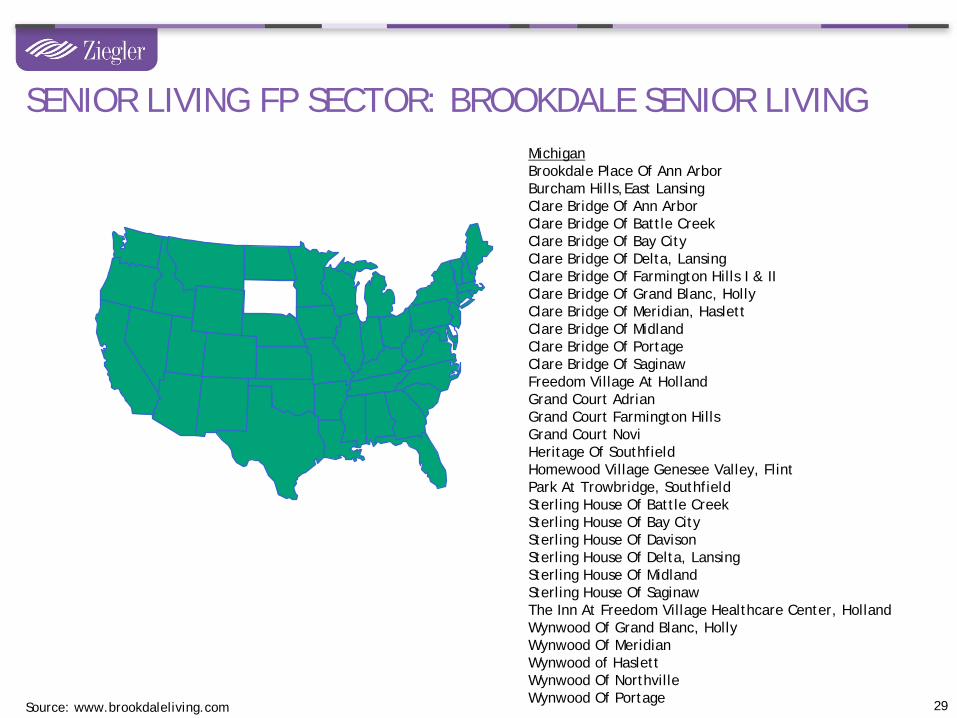

Brookdale Senior Living, Brentwood, TN(includes Emeritus Senior Living)

• 1,140 Communities in 48 States– All States except AK, DC, HI, SD

• 113,022 Total Units– 55+ Community– Independent Living– Assisted Living– Skilled Nursing– Memory Care

28

SENIOR LIVING SECTOR: FOR-PROFIT

Source: www.brookdaleliving.com

MichiganBrookdale Place Of Ann ArborBurcham Hills,East LansingClare Bridge Of Ann ArborClare Bridge Of Battle CreekClare Bridge Of Bay CityClare Bridge Of Delta, LansingClare Bridge Of Farmington Hills I & IIClare Bridge Of Grand Blanc, HollyClare Bridge Of Meridian, HaslettClare Bridge Of MidlandClare Bridge Of PortageClare Bridge Of SaginawFreedom Village At HollandGrand Court AdrianGrand Court Farmington HillsGrand Court NoviHeritage Of SouthfieldHomewood Village Genesee Valley, FlintPark At Trowbridge, SouthfieldSterling House Of Battle CreekSterling House Of Bay CitySterling House Of DavisonSterling House Of Delta, LansingSterling House Of MidlandSterling House Of SaginawThe Inn At Freedom Village Healthcare Center, HollandWynwood Of Grand Blanc, HollyWynwood Of MeridianWynwood of HaslettWynwood Of NorthvilleWynwood Of Portage

SENIOR LIVING FP SECTOR: BROOKDALE SENIOR LIVING

Source: www.brookdaleliving.com 29

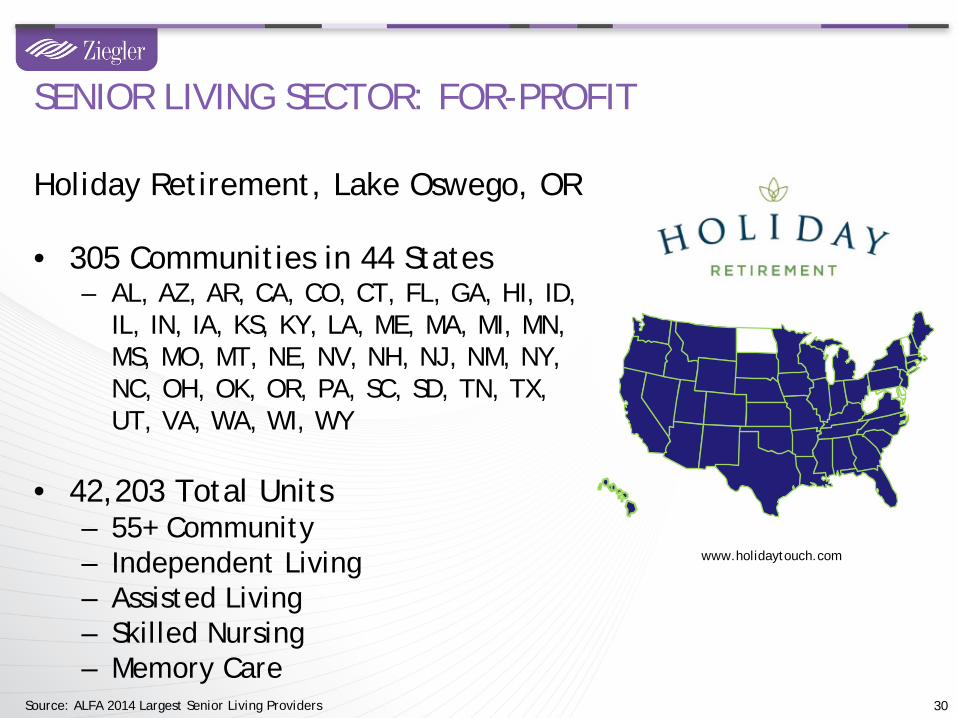

Holiday Retirement, Lake Oswego, OR

• 305 Communities in 44 States– AL, AZ, AR, CA, CO, CT, FL, GA, HI, ID,

IL, IN, IA, KS, KY, LA, ME, MA, MI, MN, MS, MO, MT, NE, NV, NH, NJ, NM, NY, NC, OH, OK, OR, PA, SC, SD, TN, TX, UT, VA, WA, WI, WY

• 42,203 Total Units– 55+ Community– Independent Living– Assisted Living– Skilled Nursing– Memory Care

30

SENIOR LIVING SECTOR: FOR-PROFIT

www.holidaytouch.com

Source: ALFA 2014 Largest Senior Living Providers

31

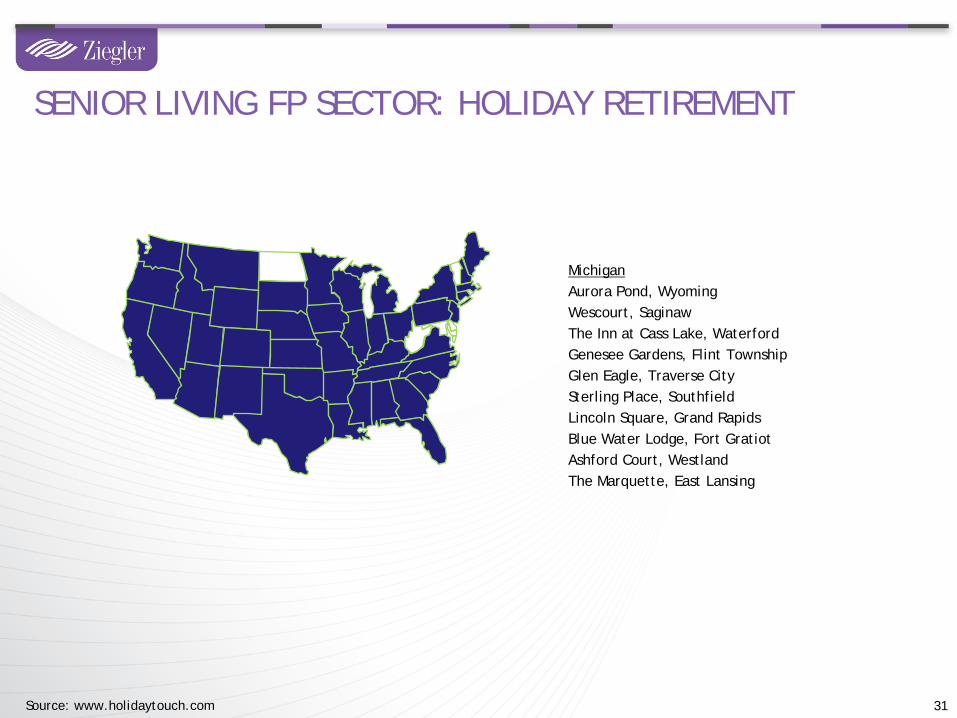

SENIOR LIVING FP SECTOR: HOLIDAY RETIREMENT

Source: www.holidaytouch.com

MichiganAurora Pond, WyomingWescourt, SaginawThe Inn at Cass Lake, WaterfordGenesee Gardens, Flint TownshipGlen Eagle, Traverse CitySterling Place, SouthfieldLincoln Square, Grand RapidsBlue Water Lodge, Fort GratiotAshford Court, WestlandThe Marquette, East Lansing

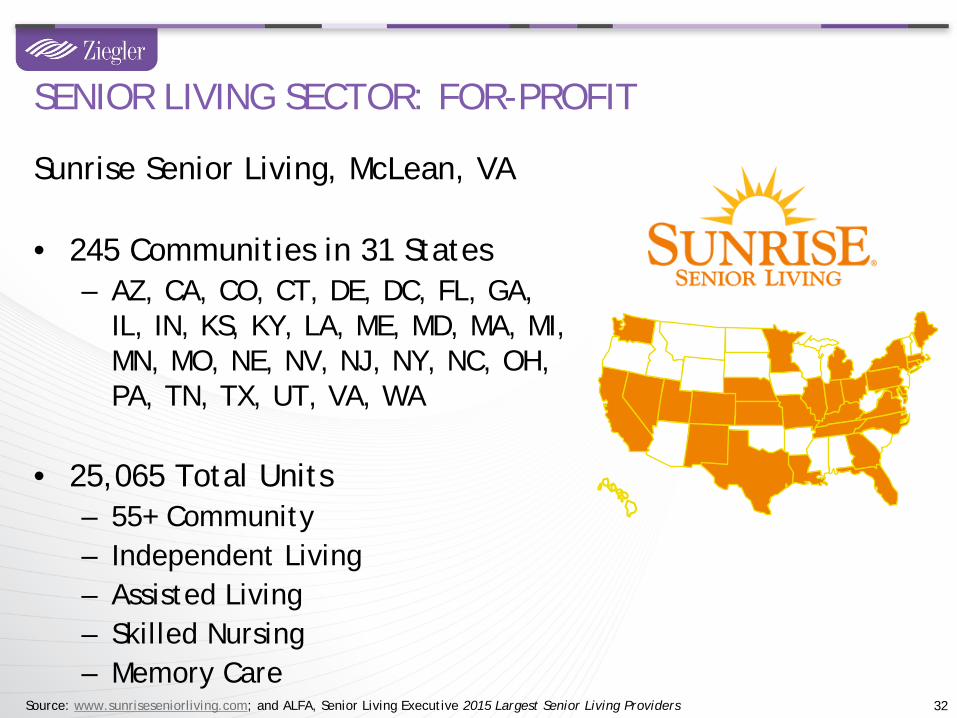

Sunrise Senior Living, McLean, VA

• 245 Communities in 31 States– AZ, CA, CO, CT, DE, DC, FL, GA,

IL, IN, KS, KY, LA, ME, MD, MA, MI, MN, MO, NE, NV, NJ, NY, NC, OH, PA, TN, TX, UT, VA, WA

• 25,065 Total Units– 55+ Community– Independent Living– Assisted Living– Skilled Nursing– Memory Care

32

SENIOR LIVING SECTOR: FOR-PROFIT

Source: www.sunriseseniorliving.com; and ALFA, Senior Living Executive 2015 Largest Senior Living Providers

33

SENIOR LIVING FP SECTOR: SUNRISE SENIOR LIVING

Source: www.sunriseseniorliving.com

MichiganSunrise of BloomfieldSunrise of Bloomfield HillsBrighton Gardens of Northville, PlymouthSunrise of Cascade, Grand RapidsSunrise of Grosse Pointe WoodsSunrise at North Farmington HillsSunrise of Northville, PlymouthSunrise of RochesterSunrise of Shelby TownshipSunrise of Vernier, Grosse Pointe WoodsSunrise of TroySunrise of West Bloomfield

Meridian Senior Living, Hickory, NC

• 132 Communities in 14 States– CA, IL, MI, MN, MO, NC, ND, OH,

OK, SC, TX, VA, WI, WV

• 9,711 Total Units– 55+ Community– Independent Living– Assisted Living– Skilled Nursing– Memory Care

34

SENIOR LIVING SECTOR: FOR-PROFIT

www.meridiansenior.com

Source: ALFA 2014 Largest Senior Living Providers

35

SENIOR LIVING FP SECTOR: MERIDIAN SENIOR LIVING

Source: www.meridiansenior.com

MichiganBuchanan Meadows, BuchananPrestige Commons, Chesterfield TownshipPrestige Place, ClarePrestige Pines, DeWittGolden Orchards, FennvilleCrystal Springs, Grand RapidsWhispering Woods, Grand RapidsLakeSide Vista, HollandPrestige Way, HoltPrestige Centre, Mount PleasantWaldon Woods, Wyoming

HCR ManorCare, Toledo, OH

• 77 Communities in 31 States– AZ, CA, CO, CT, DE, FL, GA,

IA, IN, KS, KY, MD, MI, MN, MO, NC, ND, NJ, NM, NV, OH, OK, PA, SC, SD, TX, UT, VA, WA, WI, WV

• 4,976 Total Units– 55+ Community– Independent Living– Assisted Living– Skilled Nursing– Memory Care

36

SENIOR LIVING SECTOR: FOR-PROFIT

www.hcr-manorcare.com

Source: ALFA 2014 Largest Senior Living Providers

37

SENIOR LIVING FP SECTOR:HCR MANORCARE

Source: www.hcr-manorcare.com

MichiganHeartland Rehabilitation Services of MI-Bedford, LambertvilleHeartland Health Care Center-Allen ParkHeartland Health Care Center-Three RiversHeartland Health Care Center-Ann ArborHeartland Hospice Serving Ann ArborHeartland Home Health Care Center-Ann ArborHeartland Health Care Center-Dearborn HeightsHeartland Health Care Center-JacksonHeartland Health Care Center-PlymouthHeartland Health Care Center-LivoniaHeartland Health Care Center-Grosse Pointe WoodsArden Courts of LivoniaHeartland Health Care Center-Livonia NEHeartland Hospice Serving Metropolitan Detroit, SouthfieldHeartland Home Health Care Serving Metropolitan Detroit, SouthfieldHeartland Hospice Serving Southwest Michigan, PortageArden Courts of Bingham FarmsArdent Courts of Sterling HeightsHeartland West BloomfieldMarvin & Betty Danto Health Care Center, West BloomfieldHeartland Health Care Center-Bloomfield HillsHeartland Health Care Center-Sterling HeightsHeartland Health Care Center-Battle CreekHeartland Health Care Center-KalamazooHeartland Health Care Center-Oakland, TroyHeartland Hospice Serving Greater Lansing and Jackson, MasonHeartland Home Health Care Serving Greater Lansing and Jackson, MasonHeartland Hospice Serving Central Eastern Michigan, LapeerHeartland Home Health Care Serving Central Eastern Michigan, FlintHeartland Hospice Serving Central Eastern Michigan, FlintHeartland Health Care Center-Briarwood, FlintFostrian Court Assisted Living, FlushingHeartland Health Care Center-Fostrian, FlushingHeartland of Holland

Michigan (cont’d)Heartland Health Care Center-IoniaHeartland Health Care Center-Crestview, WyomingHeartland Health Care Center-Grand RapidsHeartland Hospice Serving West Michigan, Grand RapidsHeartland Home Health Care Serving West Michigan, Grand RapidsHeartland Health Care Center-Greenview, Grand RapidsHeartland Health Care Center-SaginawHeartland Home Health Care Serving The Thumb, CaroHeartland Health Care Center-Knollview, MuskegonHeartland Health Care Center-Hampton, Bay CityHeartland Hospice Serving Northeastern Michigan, Bay CityHeartland Health Care Serving Northeastern Michigan, Bay CityHeartland Home Health Care Serving Northeastern Michigan, Bay CityHeartland Home Health Care Serving Central Michigan, Mt. PleasantHeartland Hospice Serving Central Michigan, Mt. PleasantHeartland Hospice Serving The Thumb, Bad AxeHeartland Hospice Serving West Michigan, FremontHeartland Health Care Center-WhitehallHeartland Hospice Serving Northern Michigan, West BranchHeartland Home Health Care Serving Northern Michigan, West BranchHeartland Hospice Serving Northern Michigan, CadillacHeartland Hospice Serving Northwestern Michigan, Traverse CityHeartland Home Health Care Serving Northwestern Michigan, CadillacManorCare Nursing & Rehabilitation Center, Kingsford

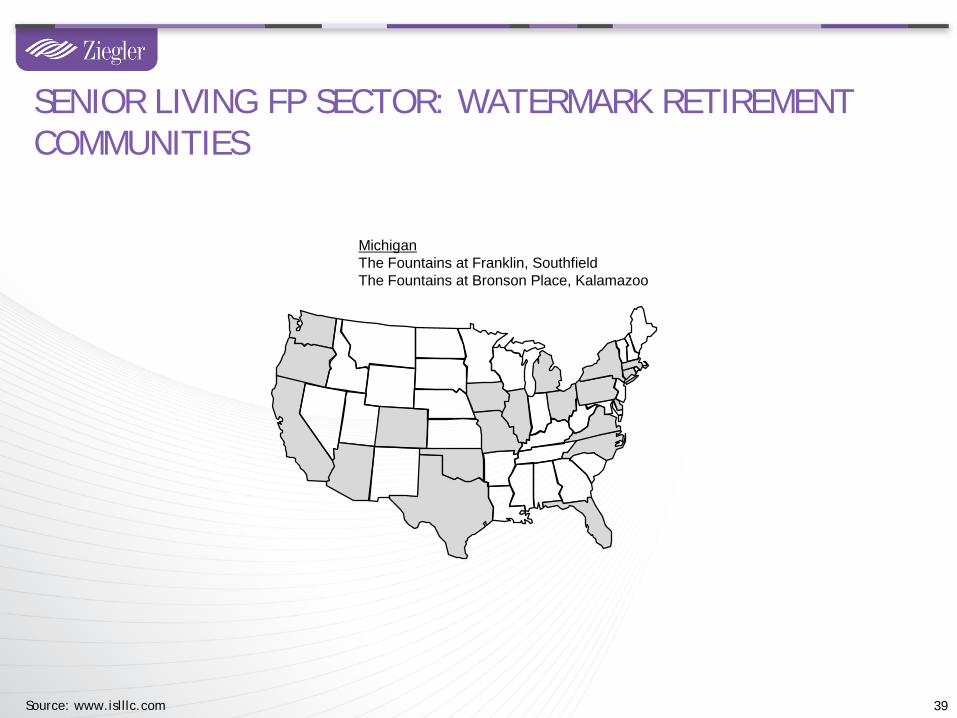

Watermark Retirement Communities, Tucson, AZ

• 33 Communities in 20 States– AZ, CA, CO, CT, DE, FL, IA, IL,

MA, MI, MO, NC, NY, OH, OK, OR, PA, TX. VA, WA

• 5,823 Total Units– 55+ Community– Independent Living– Assisted Living– Skilled Nursing– Memory Care

38

SENIOR LIVING SECTOR: FOR-PROFIT

www.islllc.com

Source: ALFA 2014 Largest Senior Living Providers

39

SENIOR LIVING FP SECTOR: WATERMARK RETIREMENT COMMUNITIES

Source: www.islllc.com

MichiganThe Fountains at Franklin, SouthfieldThe Fountains at Bronson Place, Kalamazoo

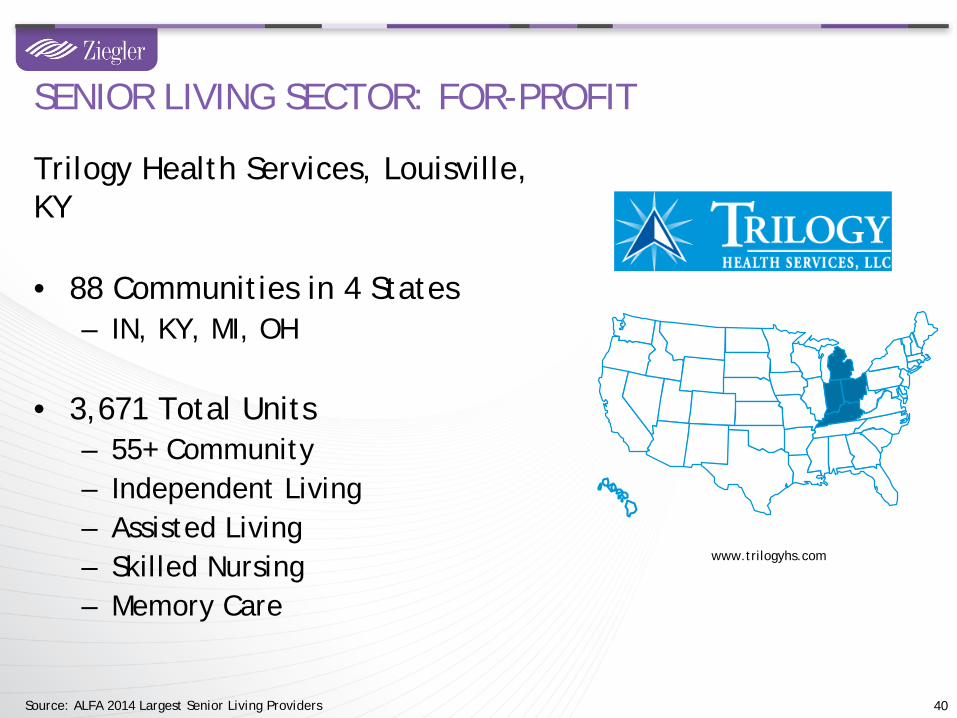

Trilogy Health Services, Louisville, KY

• 88 Communities in 4 States– IN, KY, MI, OH

• 3,671 Total Units– 55+ Community– Independent Living– Assisted Living– Skilled Nursing– Memory Care

40

SENIOR LIVING SECTOR: FOR-PROFIT

www.trilogyhs.com

Source: ALFA 2014 Largest Senior Living Providers

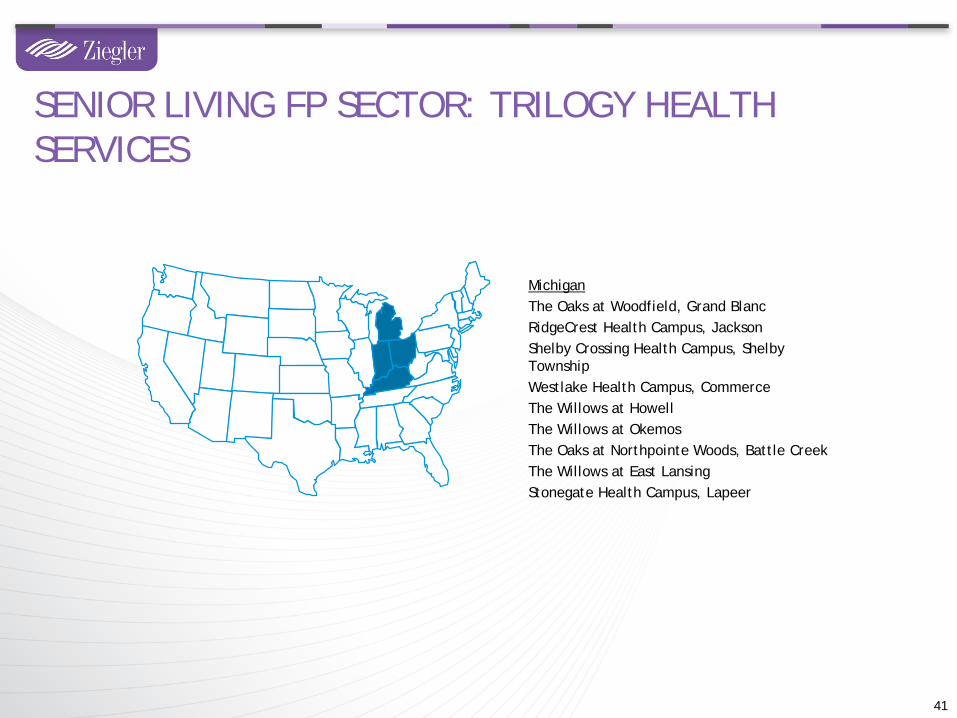

41

MichiganThe Oaks at Woodfield, Grand BlancRidgeCrest Health Campus, JacksonShelby Crossing Health Campus, Shelby TownshipWestlake Health Campus, CommerceThe Willows at HowellThe Willows at OkemosThe Oaks at Northpointe Woods, Battle CreekThe Willows at East LansingStonegate Health Campus, Lapeer

SENIOR LIVING FP SECTOR: TRILOGY HEALTH SERVICES

42

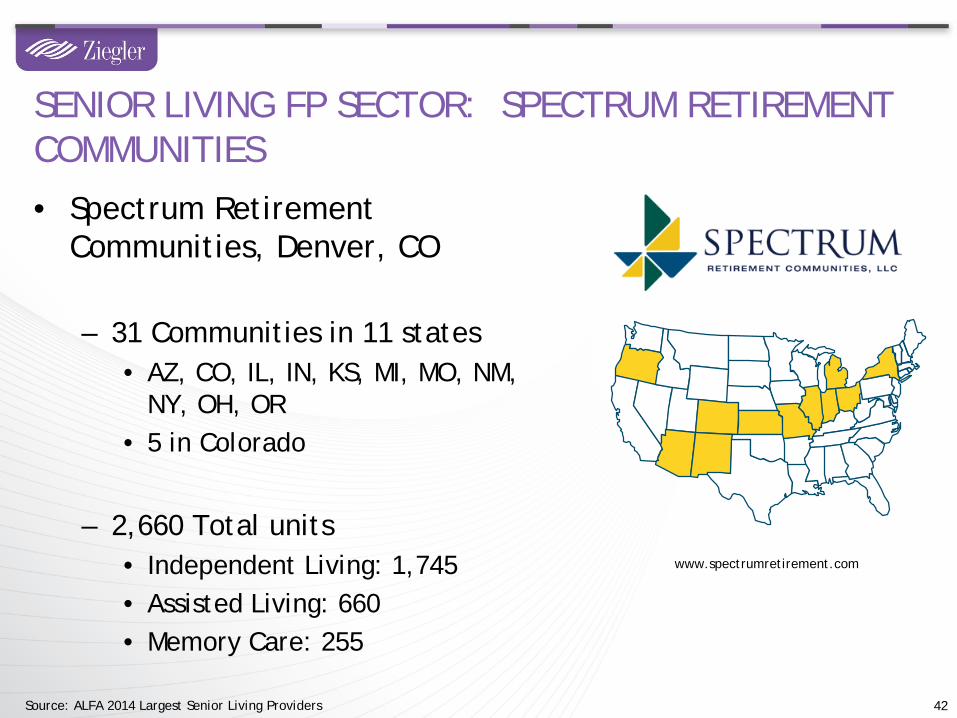

www.spectrumretirement.com

SENIOR LIVING FP SECTOR: SPECTRUM RETIREMENT COMMUNITIES

• Spectrum Retirement Communities, Denver, CO

– 31 Communities in 11 states• AZ, CO, IL, IN, KS, MI, MO, NM,

NY, OH, OR• 5 in Colorado

– 2,660 Total units• Independent Living: 1,745• Assisted Living: 660• Memory Care: 255

Source: ALFA 2014 Largest Senior Living Providers

SENIOR LIVING FP SECTOR: SPECTRUM RETIREMENT COMMUNITIES

43

MichiganMaple Heights Retirement Community, Allen ParkPine Ridge of Garfield Senior Living, Clinton TownshipPine Ridge of Hayes Senior Living, Sterling Heights,Pine Ridge of Plumbrook Retirement Community, Sterling HeightsPine Ridge Villas of Shelby Senior Living, Shelby Township,

Source: http://www.spectrumretirement.com

44

Technology

Care Coordination

Quality Outcomes

Shift to Home-based Care

Bargaining Power: Size matters

HEALTHCARE REFORM IS A GAME CHANGER

• Actively engaging in strategic planning efforts

• Continued expansion into HCBS– Common space for joint ventures

• Developing and experimenting with new models of care

• Looking to diversify revenue streams– Addition of non-traditional services– For-profit ventures

45

HOW ARE NFP PROVIDERS RESPONDING?

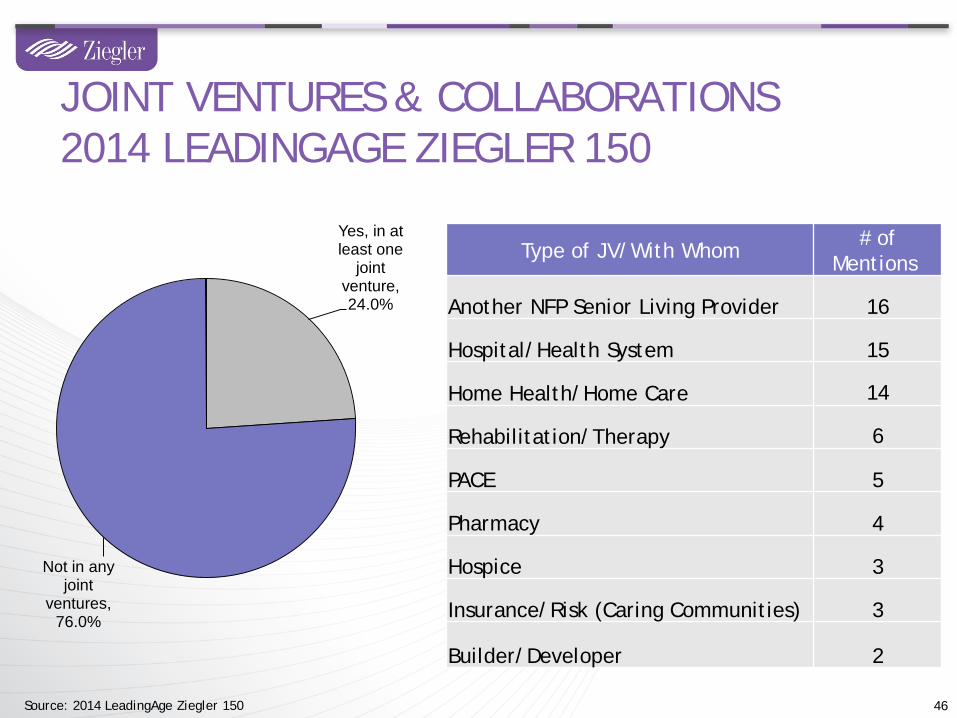

JOINT VENTURES & COLLABORATIONS2014 LEADINGAGE ZIEGLER 150

46

Yes, in at least one

joint venture, 24.0%

Not in any joint

ventures, 76.0%

Type of JV/With Whom # of Mentions

Another NFP Senior Living Provider 16

Hospital/Health System 15

Home Health/Home Care 14

Rehabilitation/Therapy 6

PACE 5

Pharmacy 4

Hospice 3

Insurance/Risk (Caring Communities) 3

Builder/Developer 2

Source: 2014 LeadingAge Ziegler 150

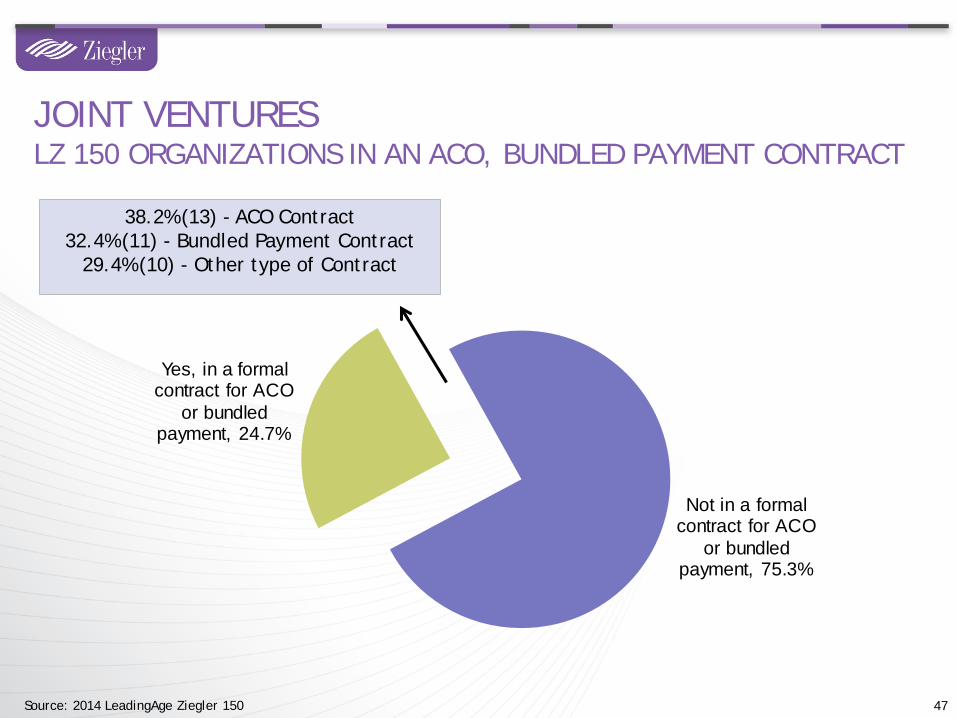

Yes, in a formal contract for ACO

or bundled payment, 24.7%

Not in a formal contract for ACO

or bundled payment, 75.3%

JOINT VENTURESLZ 150 ORGANIZATIONS IN AN ACO, BUNDLED PAYMENT CONTRACT

47Source: 2014 LeadingAge Ziegler 150

38.2% (13) - ACO Contract32.4% (11) - Bundled Payment Contract

29.4% (10) - Other type of Contract

• Many providers are looking to peers or logical other organizations to partner with on providing services– In some cases, may make sense to partner with for-profit

organization (e.g. home health/care agency)

• A way to share risk with others

• Ability to build upon one another’s competencies and resources

• Greater ability to compete and have negotiating power

48

WHY CONSIDER A PARTNERSHIP MODEL?

• Covenant Health Network (CHN) is a non-profit Post-Acute Integrated Delivery System, formed in 1997, now encompasses 91 senior care facilities in four states.

• CHN was created to provide a seamless continuum of post-acute and senior care services in a more cost effective manner, while collaborating to improve quality and reduce administrative costs.

• The majority of CHN Skilled Nursing Facilities (SNF’s) are also part of a campus providing a continuum of care (Assisted Living, Independent Living, etc.) which offers greater opportunities for integrated care delivery.

• CHN is structured with a formal member agreement giving CHN the authority to negotiate on their behalf. It is designed as a “messenger model” assuring all anti-trust considerations are honored.

• CHN has entered into multiple joint venture companies for the purpose of an integrated delivery system, assuring that the continuity of service, quality of service, consistent outcome measures as well as shared risk can occur.

COVENANT HEALTH NETWORK (CHN)

49

• Joint venture between 13 Pennsylvania-based CCRC providers and Covenant Health Network of Arizona.

• Develop relationship as a Partner with hospital systems– Alliance as single point of access and contact for network

• Create joint ventures with business plans creating a seamless system for resident regardless of which JV is serving – Rehab, Home Care, Home Health, Hospice, Pharmacy, Palliative

• Become the strategic initiatives center for members– Technology, Outcomes, Pre-hab, Other

50

COVENANT HEALTH ALLIANCE OF PENNSYLVANIA

EHCO – Extended Health Care ProvidersCollaborative Effort Clark Retirement Community Holland Home Life EMS Porter Hills Sunset Retirement Communities and Services

51Source: Tandem 365

ECHO, LLCDBA “TANDEM 365”

LEVERAGING STRENGTHS

52

ClarkHolland Home Life EMS Porter Hills Sunset

CCRC X X X XHome Care X X X XHospice X X X XPrivate Duty X X X XPACE X XCC @ H XEMS XTransportation XTele-health Oversight XHUD Housing XWaiver XSNF X X X XAL X X X XMemory Care X X

Source: Tandem 365

Home Health

Home Care

Concierge Svcs.

Hospice

CCaH

Adult Day

PACE

HCBS OWNERSHIP LARGELY FOR-PROFIT

53

Primarily NFP

Primarily For-Profit

JOINT VENTURES: HOME HEALTH, HOME CARE & HOSPICE• Home health, home care and hospice joint ventures

are growing at a fairly rapid pace and are among the most common JVs in the senior living sector

54MI OH

AL

• More of this type of partnership between senior living organizations and dialysis companies. Services offered on-site within the community

55

JOINT VENTURES: DIALYSIS ON CAMPUS

• Way to diversify services and revenue streams• Ability to build upon existing strengths• Several providers have significant for-profit subsidiaries for

technology services

56

INNOVATION & GROWTH: FOR-PROFIT VENTURES

57

A GROWING TRENDCONTINUING CARE AT HOME PROGRAMS

Sources: Ziegler Investment Banking, 2/18/2015

• Active (21)• In-development, publicly announced (3)

Anticipated by the end of 2015: 27 programs

58

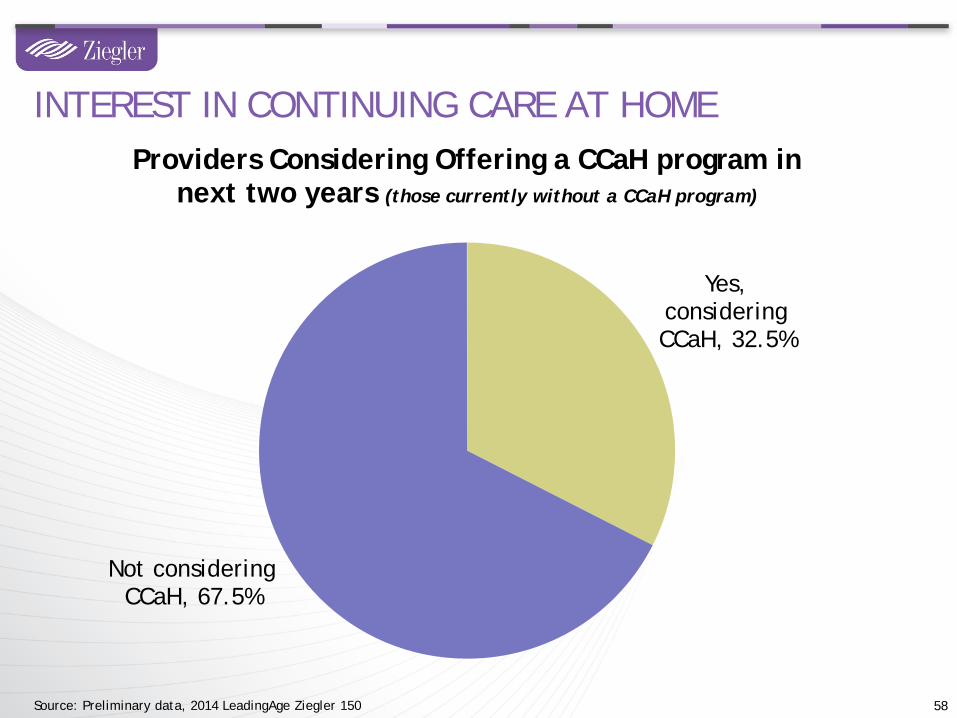

Yes, considering CCaH, 32.5%

Not considering CCaH, 67.5%

Providers Considering Offering a CCaH program in next two years (those currently without a CCaH program)

Source: Preliminary data, 2014 LeadingAge Ziegler 150

INTEREST IN CONTINUING CARE AT HOME

59

• Technology increasingly a differentiator• Not an amenity, but an expectation• Telehealth (Behavioral and Biometric)• Electronic Health Records• Personal Emergency Response Systems• Health Information Exchange• Medication Management• Brain Fitness• Increase in companies offering aging-

related technologies

TECHNOLOGY: ONE OF THE TOP 5 INDUSTRY TRENDS

Fund closed June 30th with total capital commitments of $26,620,000 / 91 investors (of which 70 are non-profit senior providers)

Focus on the Aging Services Continuum

Specialty fund targeting multi-stage equity investments

Meaningful introductions to high profile, innovative companies, potential pilot coordination, ability to gain insights and promote collaboration

ZIEGLER-LINK•AGE LONGEVITY FUND, LP

60

TOPIC 2: QUICK SENIOR LIVING CAPITAL MARKET UPDATE

62

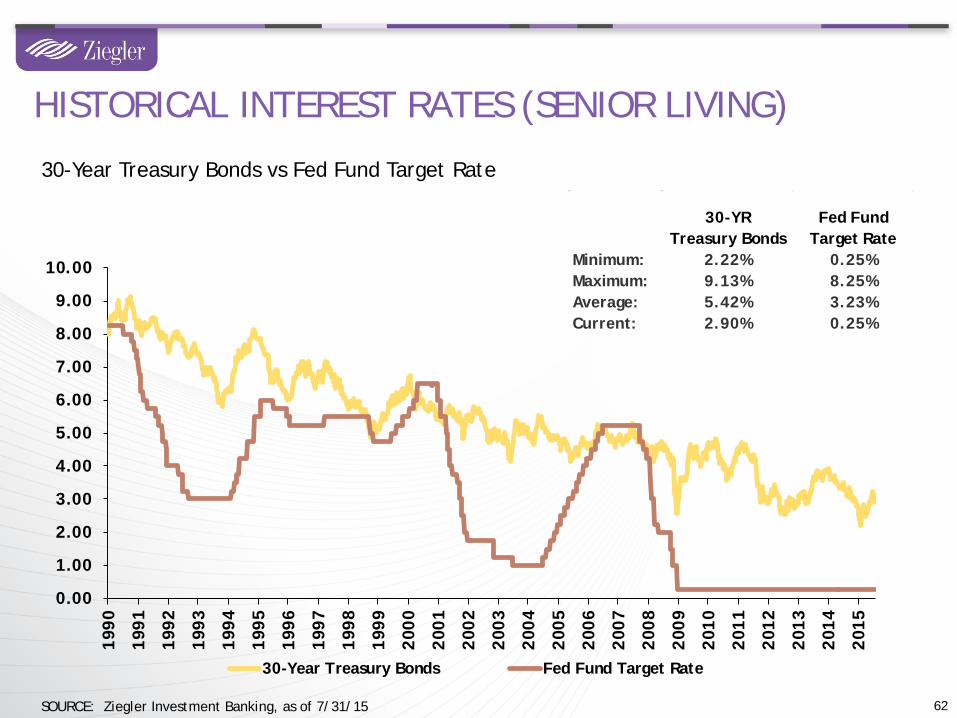

30-Year Treasury Bonds vs Fed Fund Target Rate

SOURCE: Ziegler Investment Banking, as of 7/31/15

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

30-Year Treasury Bonds Fed Fund Target Rate

30-YRTreasury Bonds

Fed FundTarget Rate

Minimum: 2.22% 0.25%Maximum: 9.13% 8.25%Average: 5.42% 3.23%Current: 2.90% 0.25%

HISTORICAL INTEREST RATES (SENIOR LIVING)

0

5

10

15

20

25

30

35

40

2.40

2.50

2.60

2.70

2.80

2.90

3.00

3.10

3.20

3.30

3.40

3.50

3.60

3.70

3.80

3.90

4.00

4.10

4.20

4.30

4.40

4.50

4.60

4.70

4.80

4.90

5.00

5.10

5.20

5.30

5.40

5.50

5.60

5.70

5.80

5.90

6.00

6.10

6.20

6.30

6.40

6.50

6.60

6.70

6.80

6.90

7.00

7.10

7.20

7.30

7.40

7.50

Freq

uenc

y

30-yr "AAA" MMD

30-yr "AAA" MMD Histogram1990 - 2015 YTD

63

HISTORICAL INTEREST RATESUNIQUE MARKET OPPORTUNITY

Source: Thomson Financial Municipal Market Monitor, as of 7/31/15

MMD has only been lower than what it is today less than 6.92% of the time

since 1990.

7/31/15 MMD: 3.14

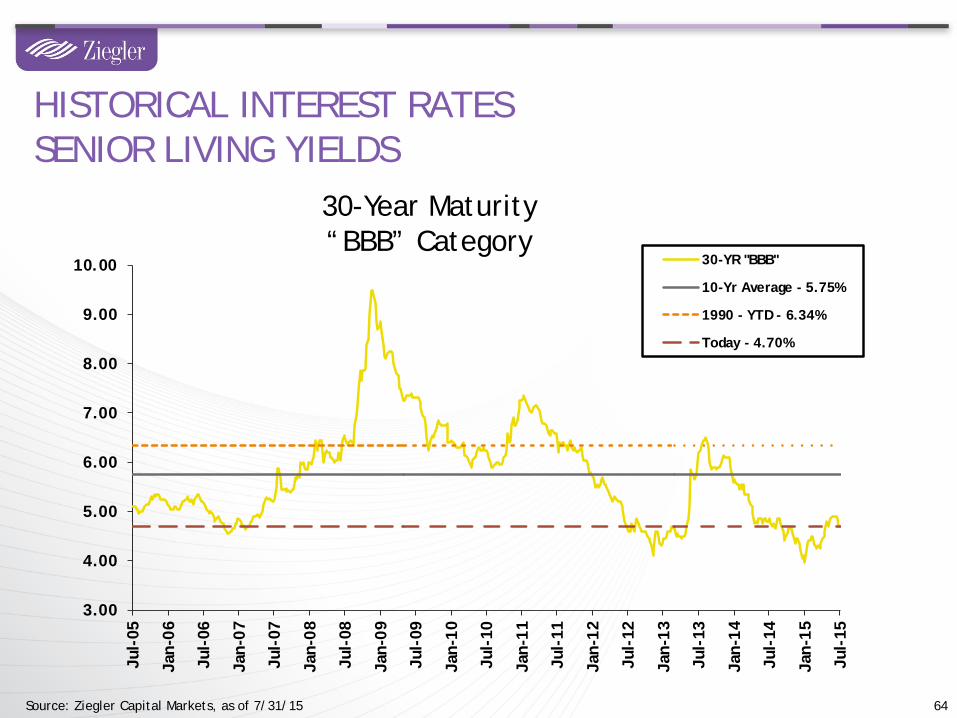

64Source: Ziegler Capital Markets, as of 7/31/15

30-Year Maturity“BBB” Category

HISTORICAL INTEREST RATESSENIOR LIVING YIELDS

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Jul-

05

Jan-

06

Jul-

06

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

Jan-

12

Jul-

12

Jan-

13

Jul-

13

Jan-

14

Jul-

14

Jan-

15

Jul-

15

30-YR "BBB"

10-Yr Average - 5.75%

1990 - YTD - 6.34%

Today - 4.70%

65Source: Ziegler Capital Markets, as of 7/31/15

30-Year MaturityNon-rated Category

HISTORICAL INTEREST RATESSENIOR LIVING YIELDS

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

12.00

Jul-

05

Jan-

06

Jul-

06

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

Jan-

12

Jul-

12

Jan-

13

Jul-

13

Jan-

14

Jul-

14

Jan-

15

Jul-

15

30-YR NR-Institutional

10-Yr Average - 6.61%

1990 - YTD - 7.06%

Today - 5.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

1996-1997

1998-1999

2000-2001

2002-2003

2004-2005

2006-2007

2008 2009 2010 2011 2012 2013 2014

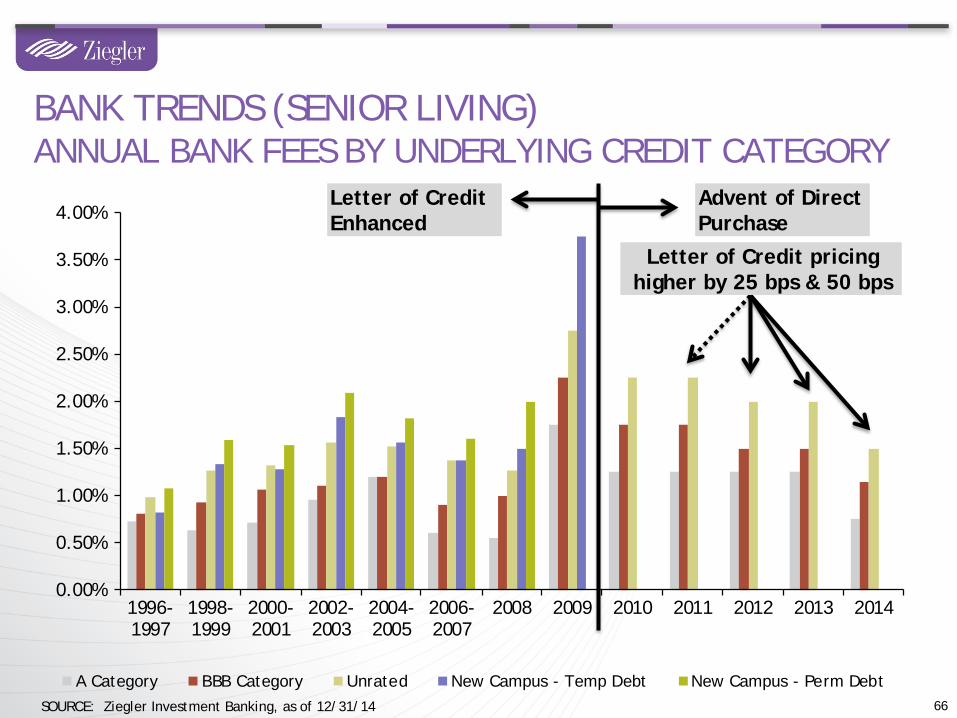

A Category BBB Category Unrated New Campus - Temp Debt New Campus - Perm Debt66

BANK TRENDS (SENIOR LIVING)ANNUAL BANK FEES BY UNDERLYING CREDIT CATEGORY

SOURCE: Ziegler Investment Banking, as of 12/31/14

Letter of CreditEnhanced

Advent of Direct Purchase

Letter of Credit pricing higher by 25 bps & 50 bps

0

2

4

6

8

10

12

14

1996-1997

1998-1999

2000-2001

2002-2003

2004-2005

2006-2007

2008 2009 2010 2011 2012 2013 2014

Year

s

Direct Purchase A Category - LOC BBB Category - LOC NR Category - LOC

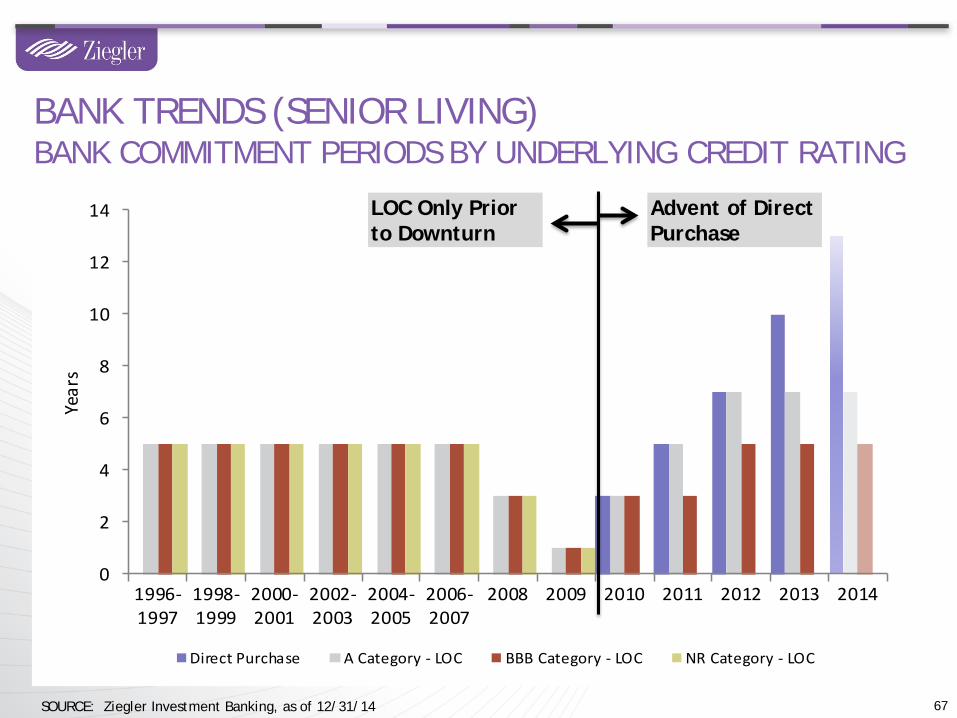

67

Advent of Direct Purchase

BANK TRENDS (SENIOR LIVING)BANK COMMITMENT PERIODS BY UNDERLYING CREDIT RATING

LOC Only Prior to Downturn

SOURCE: Ziegler Investment Banking, as of 12/31/14

DISCUSSION

Investment banking, capital markets and wealth management services offered through B.C. Ziegler and Company. Investment management services offered by Ziegler Capital Management, LLC (ZCM). As of November 30, 2013, ZCM (a registered investment advisor with the Securities and Exchange Commission) is no longer an affiliate of B.C. Ziegler and Company. Notwithstanding, the parties have entered into a Referral Agreement through which referral fees may be paid. FHA mortgage banking services are provided through Ziegler Financing Corporation which is not a registered broker/dealer. Ziegler Financing Corporation and B.C. Ziegler and Company are affiliated and referral fees may be paid by either entity for services provided.

This presentation was prepared based upon information provided to Ziegler Investment Banking (ZIB) and contains certain financial information, including audited and unaudited information, certain statistical information and explanations of such information in narrative form (the “Information”). ZIB believes this information to be correct as of the date or dates contained herein. However, the financial affairs change constantly, and such changes may be material. Today’s discussion may contain forward-looking statements, which may or may not come to fruition depending on certain circumstances, including those outside the control of management. Please be advised that ZIB has not undertaken, assumed no duty and are not obligated to update the Information. In addition, please be advised that past financial results do not predict futurefinancial performance. The material in this presentation is designed to present potential financing structures and options for discussion, however it does not represent a commitment to underwrite bonds, place debt or provide financing and thus should not be relied upon as a promise of financing or underwriting commitment.

DISCLAIMER

69